WKME - WalkMe: A Path To Profitability Into 2024

2023-11-16 01:16:41 ET

Summary

- WalkMe reported Q3 earnings highlighted by the first quarter of positive EPS since the company's 2021 IPO.

- The company is seeing strong demand for its Digital Adoption Platform, helping customers enhance enterprise productivity.

- We are bullish on WKME stock supported by an improving financial outlook into 2024.

WalkMe ( WKME ) is presenting some bullish momentum with shares up nearly 20% over the past month. The company recently reported its latest quarterly result, highlighted by reaching positive adjusted EPS for the first time since the 2021 IPO.

Indeed, while WKME is still down significantly from its peak valuation, the setup here is an emerging turnaround supported by stronger operating and financial trends. A path for WalkMe to reach sustainable profitability going forward should be positive for the stock into 2024.

What Does WalkMe Do?

WKME has found success with its category-defining Digital Adoption Platform ((DAP)). The idea here is that the companies use the tools to optimize their entire software stack through analytical data for the management of the employee workflow.

Through the integration with market-leading ecosystems from companies like Salesforce Inc. ( CRM ), Oracle Corp. ( ORCL ), ServiceNow ( NOW ), or DocuSign Inc. ( DOCU ), for example, the DAP walks through users on how to organize the systems and complete critical tasks.

Ultimately, the selling point of DAP is for customers to achieve productivity benefits including cost savings, and even generate higher revenue. According to WalkMe, new AI features have added to the appeal with a strong customer response.

{kind=link}

WKME Earnings Recap

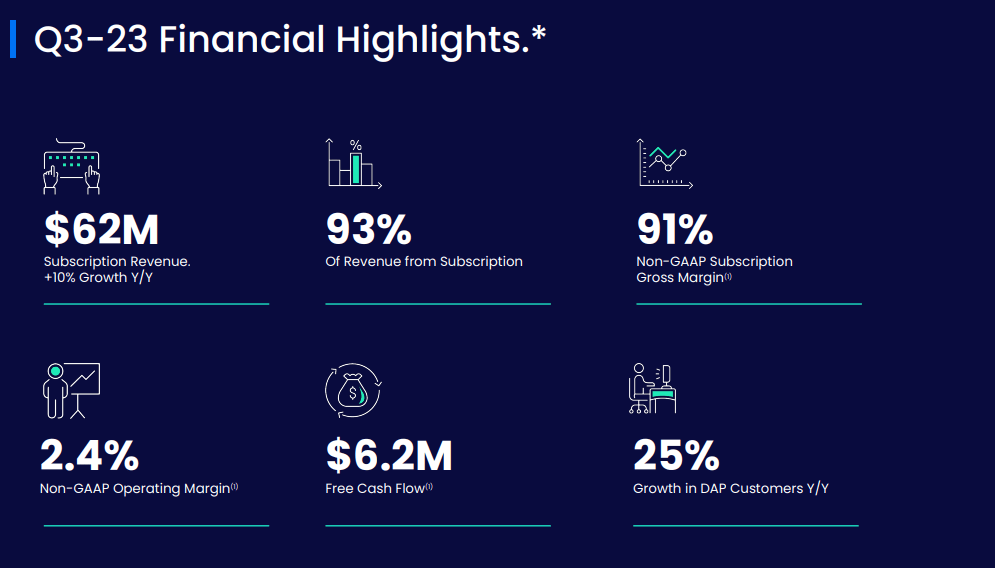

KME reported Q3 non-GAAP EPS of $0.04, which beat the consensus estimates by $0.05. Revenue of $67 million was up 6% year-over-year. Within that amount, subscription revenue at $62.3 million, representing the bulk of the core business, was up an even stronger 11% y/y.

Management called this a "milestone quarter", pointing to the adjusted profitability as well as the second consecutive quarter for positive cash flows.

{kind=link}

The gross margin at 85% was up from 79% in the period last year, reflecting the shifting sales mix, particularly with a trend of large customers generating more than $1 million in annual recurring revenue ((ARR)) adding features.

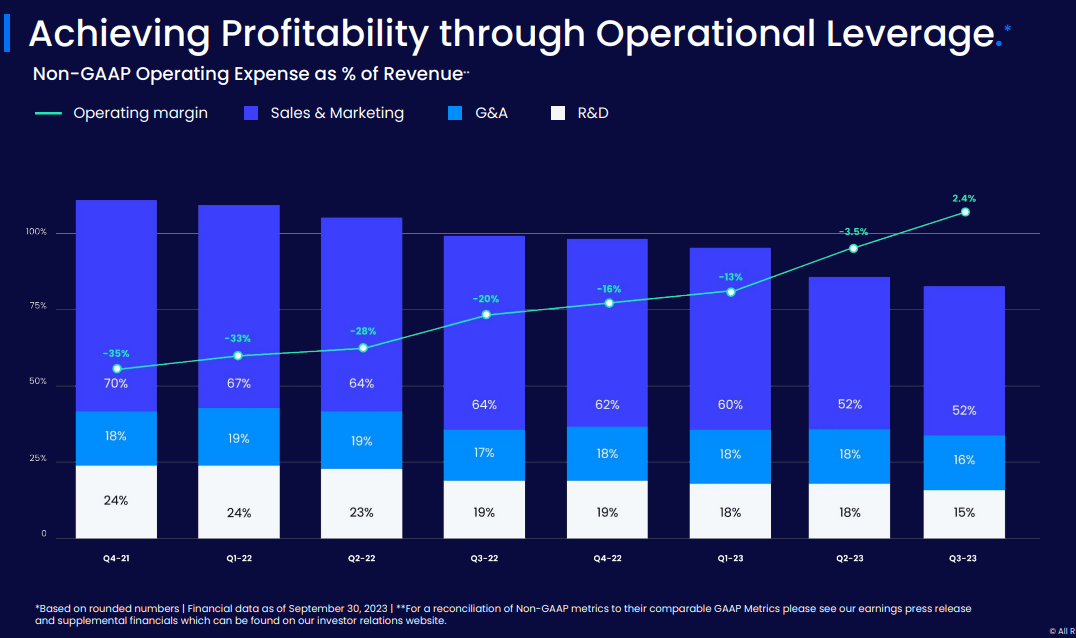

Free cash flow at $6.2 million reversed a loss of -$11.2 million in Q3 2022. There has also been some effort at controlling expenses with G&A, sales & marketing declining as a percentage of revenue through operating leverage.

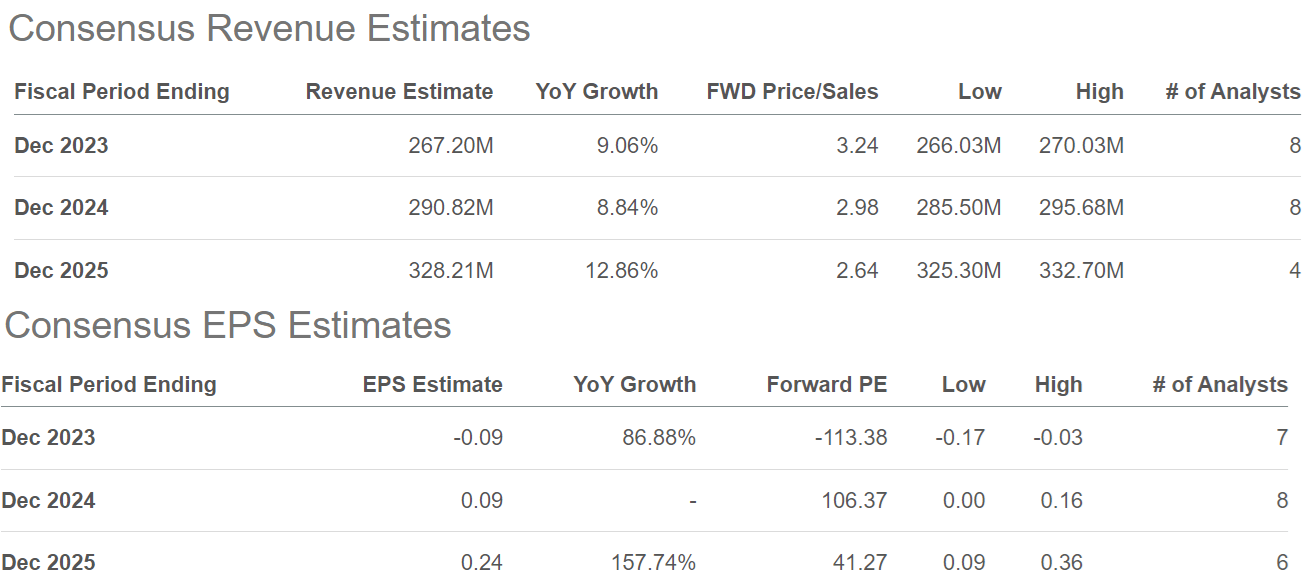

In terms of guidance, the company expects to reach full-year 2023 revenue of $266.1 to $267.1 million, representing a 9% growth rate at the midpoint. The estimated full-year non-GAAP operating loss between -$8.3 million and -$7.3 million, if confirmed, would be a marked improvement compared to the -108 million for 2022. The expectation is that there is room for stronger profitability into next year.

{kind=link}

What's Next For WKME

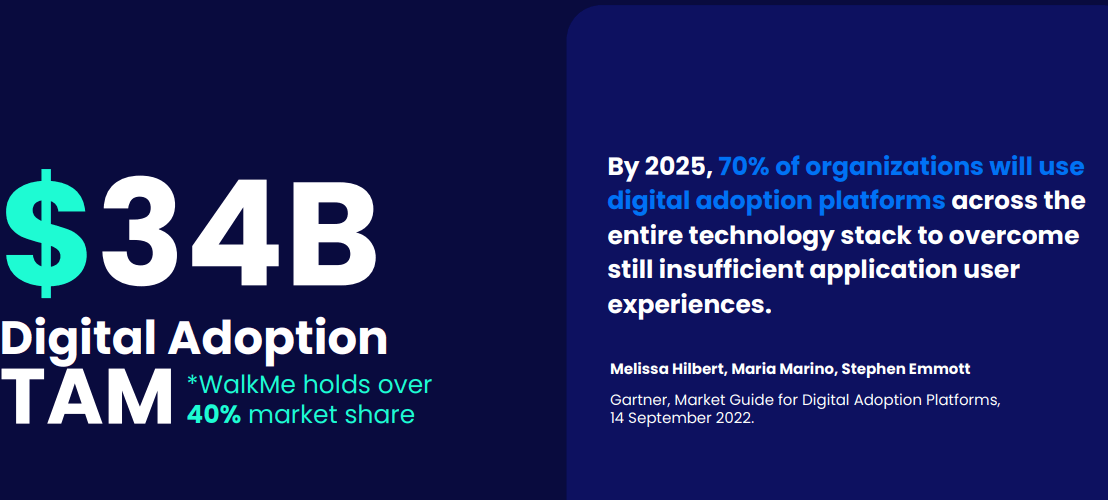

What we like about WKME is the sense that the value proposition of the Digital Adoption Platform is gaining acceptance as a critical enterprise-level productivity tool.

The company shares research suggesting that 70% of organizations will use these types of tools by 2023. The opportunity here is for WalkMe to consolidate its market share in what is estimated to be a $34 billion addressable market.

{kind=link}

A strong point in WalkMe's investment profile is its rock-solid balance sheet, which ended the quarter with $312 million in cash and cash equivalents against effectively zero long-term financial debt. With the underlying business becoming financially sustainable, the cash position offers strategic flexibility while supporting the underlying value in the equity.

We mentioned that path to profitability. The consensus is that WKME will reach EPS of $0.09 in 2023, a level that can accelerate towards $0.24 by fiscal 2025. This would be achieved by otherwise steady growth in the high single digits next year, while margins have room to climb higher.

In terms of valuation, WKME has a current market cap of approximately $870 million, effectively trading at 3x 2023 sales. The premium is even narrower on a net-of-cash basis. A 106x the P/E estimate for 2024 can be considered expensive, but again is in the context of what should be a longer earnings tailwind.

{kind=link}

Overall, we believe these multiples are more than reasonable for a software category tech leader in this stage of its growth cycle.

That being said, the big risk here would be weaker-than-expected growth, pushing back the earnings timetable. A forecast for ~10% revenue growth over the next few years is solid, but hardly an exceptional level among high-growth stocks.

The main weakness with WalkMe, in our opinion, is the question of the strength of the company's competitive moat. While attempting to describe exactly what the DAP is, it's clear that some of the functionality could be replaced by the underlying software stack, essentially fixing their own productivity shortcomings.

This is a concern that will linger for the foreseeable future and is one reason that could limit the upside in the stock. We can also look forward to any future potential acquisitions or strategic initiatives as an important step to secure long-term viability for the company.

Final Thoughts

WalkMe has taken an important step forward in 2023, with the latest quarterly results confirming the financial strategy is working. Monitoring points over the next few quarters include the trend in adjusted operating margin, cash flow, and customer count levels.

We are cautiously bullish on WKME and expect shares to benefit from a broader improving macro environment into 2024 as the potential for lower interest rates is more supportive of small-caps and overall risk sentiment.

For further details see:

WalkMe: A Path To Profitability Into 2024