WKME - WalkMe: Demand Headwinds Weigh In On Profitability Improvements

2023-11-17 03:33:15 ET

Summary

- WalkMe is a cloud-based digital adoption platform with over 40% market share in its category.

- Demand headwinds have been intensifying, which has lead to a significant deceleration in its growth momentum as a result of higher dollar churn and lower net new customer additions.

- The company has done significantly well in managing its cost base to drive profitability ahead of the targets, however, we do not see any signs of demand headwinds abating.

Investment Thesis

We ascribe WalkMe ( WKME ) a Neutral rating on the back of

1) decelerating sales momentum amidst persistent macroeconomic pressures leading to slowing technology spends, dollar churn, low net new customer additions and significantly lower retention rates

2) weakening fundamentals albeit with an improvement in the operating margin profile although improving driven by management's focus on P&L and cash generation

3) potential recovery priced in at current valuation multiple providing limited margin of safety

Company Background

WalkMe Ltd operates a cloud based digital adoption platform providing a customizable no code application overlay giving the designer an ability to create walkthroughs so that end users are able to more seamlessly adopt technology workflows. It is a recognized leader within a new category boasting a market share of over 40% with the rest of 15-20 companies comprising the rest of the market. The company has over 550 customers with ~40 customers with an ARR of $1mn+ and 500+ customers with an ARR of $100k+.

{kind=link}

Key Historical Metrics

ARR Growth

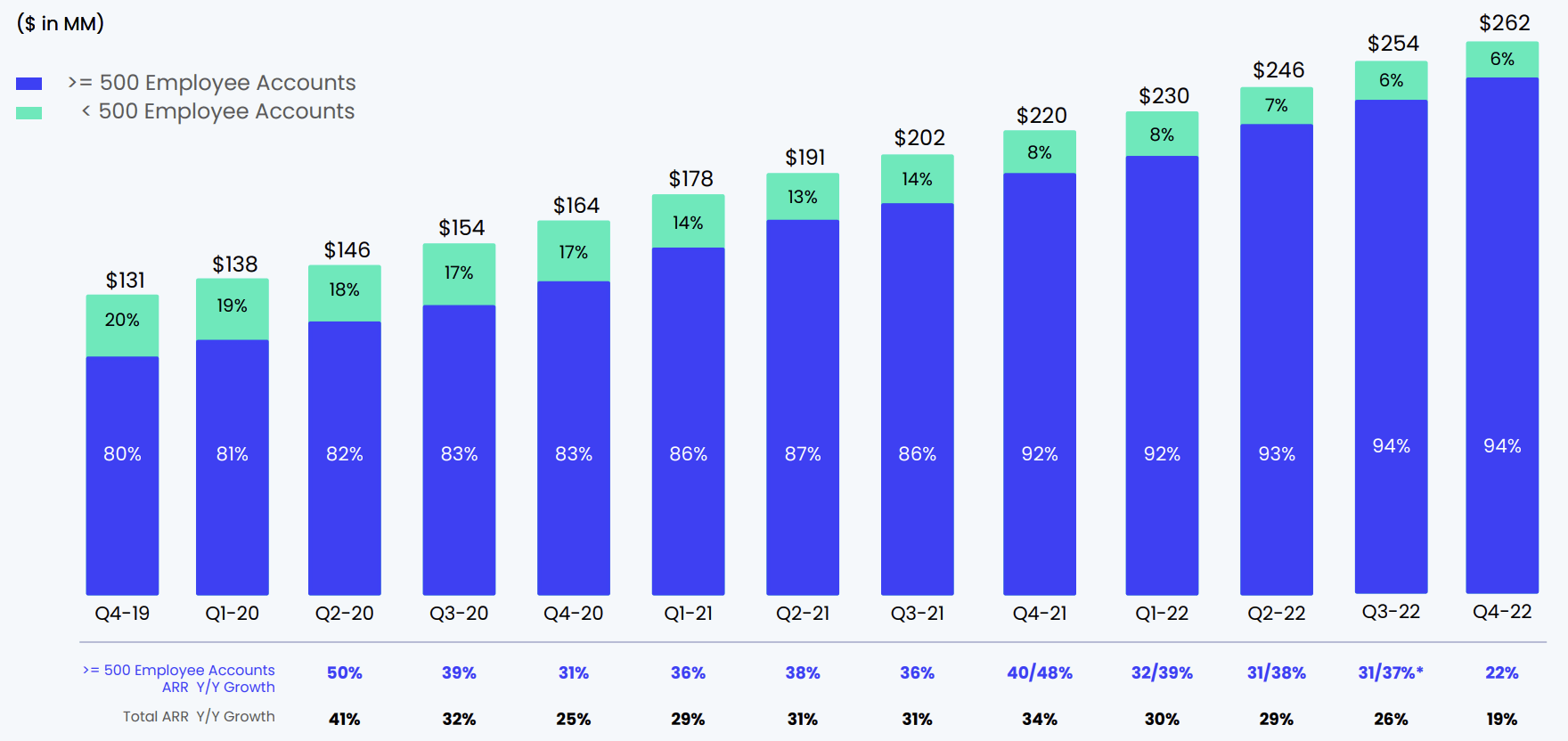

WalkMe was impacted during COVID related headwinds with slowing expansion and weaker net customer additions. It also paused hiring in 2020 which impacted growth amidst a dip in S&M spends, however, accelerated soon thereafter in 2021 with an above 30% ARR growth along with a growing share of larger accounts with employees of more than 500 (contributing 92% in Q4 2021 vs 80% in Q4 2019). However, growth decelerated again in 2022 as a result of challenging macro environment leading to slowing pace of new customer additions and dollar churn.

{kind=link}

Retention Rate

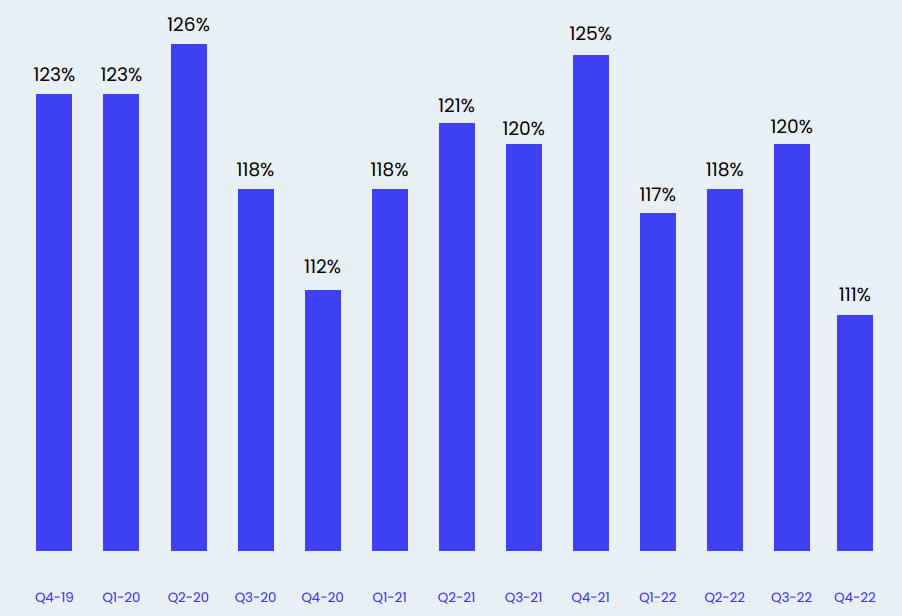

Net retention ratio trended above 120% generally driven by its strong product portfolio enabling upselling and cross-selling of its products. However, net retention rates dropped in the latter half of 2020 due to COVID related challenges before re-accelerating again soon thereafter, declining further in 2022 due to macro headwinds.

{kind=link}

Customer Additions

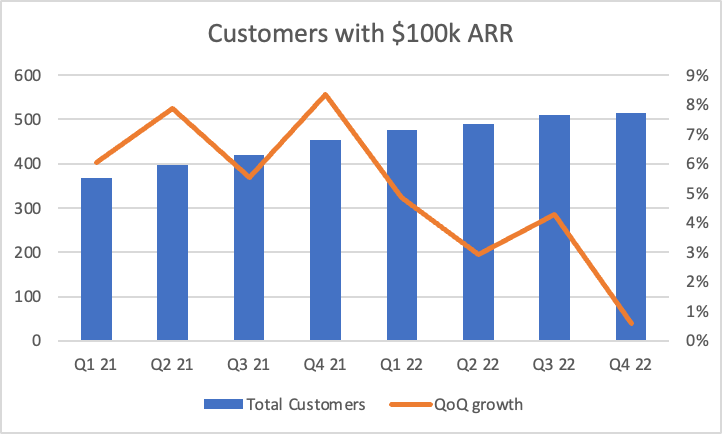

Net Customer additions had been strong historically with an average 6-8% growth in net customer additions, however, the growth decelerated significantly during 2022 amidst higher dollar churn and slowing sales and marketing spends amidst challenging macro environment.

{kind=link}

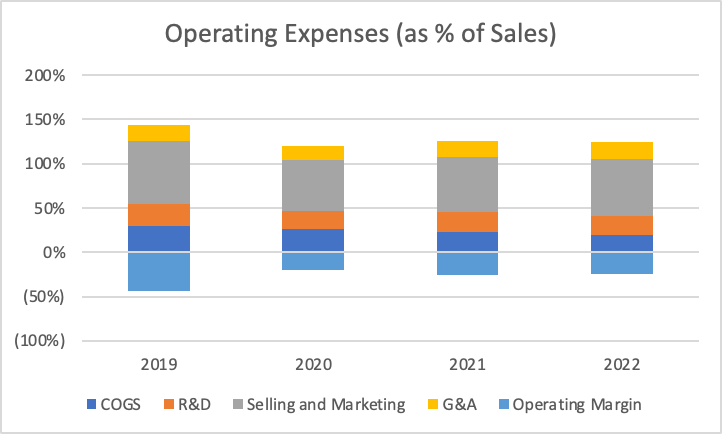

Operating Loss Margins

Gross product margins improved from 71% in 2019 to 80% in 2022 driven by improving utilization, cross selling and upselling initiatives and growing number of customer additions with higher ARR spends and larger employee accounts. R&D expenses as % of sales declined slightly from 25% in 2019 to 21% in 2022 as a result of operating leverage while selling and marketing expenses continue to be elevated at 64% in 2022, although slightly lower than 71% in 2019, typical of SaaS based tech players. G&A expenses continue to be flattish at 19% with the company still not being able to fully leverage its growth. Operating loss margin remains at (24%) in 2022, largely in line in recent quarters, although down from (44%) in 2019.

{kind=link}

Mixed Q3 Results

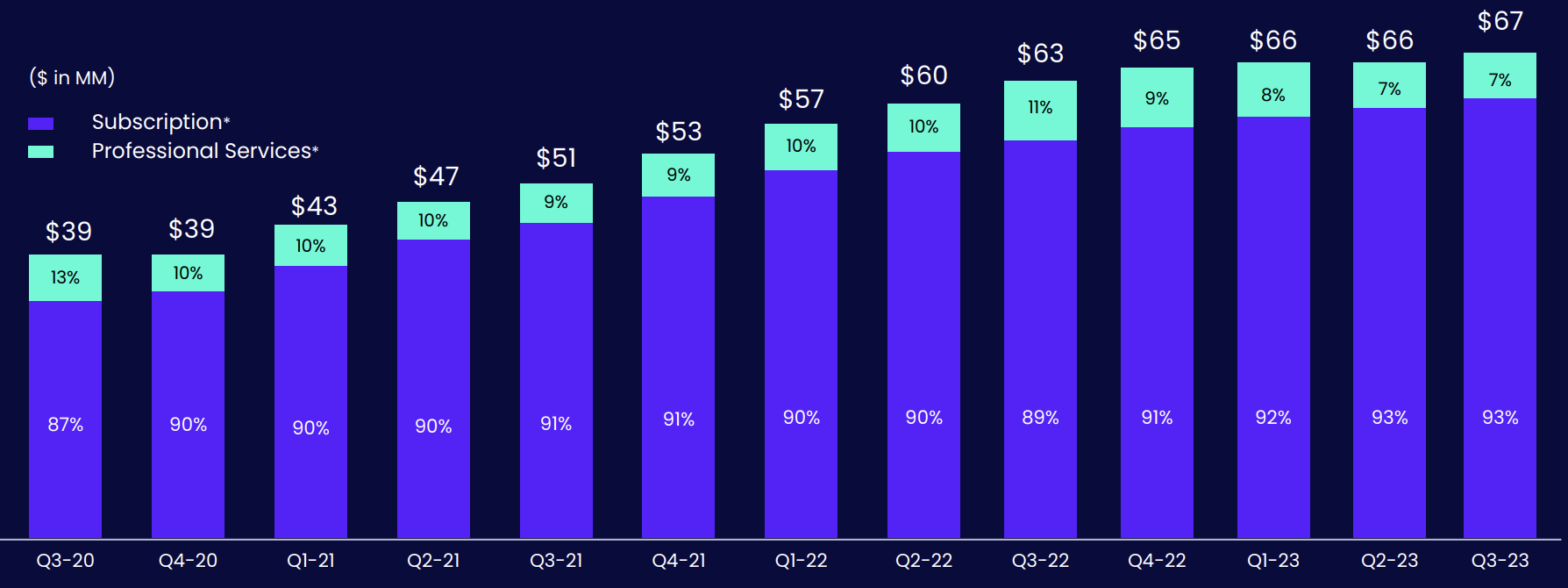

The company reported mixed Q3 results with revenues growing by 6% YoY, its slowest growth in a quarter throughout its history and below the company's 16% growth in Q1 and 10% growth in Q2. The revenue growth was driven by a 10% growth in subscription revenue while professional services segment continue to be a dampener, down 30% YoY and flat sequentially. On sequential basis, revenue has largely been flat over the past several quarters reflecting plateauing growth.

{kind=link}

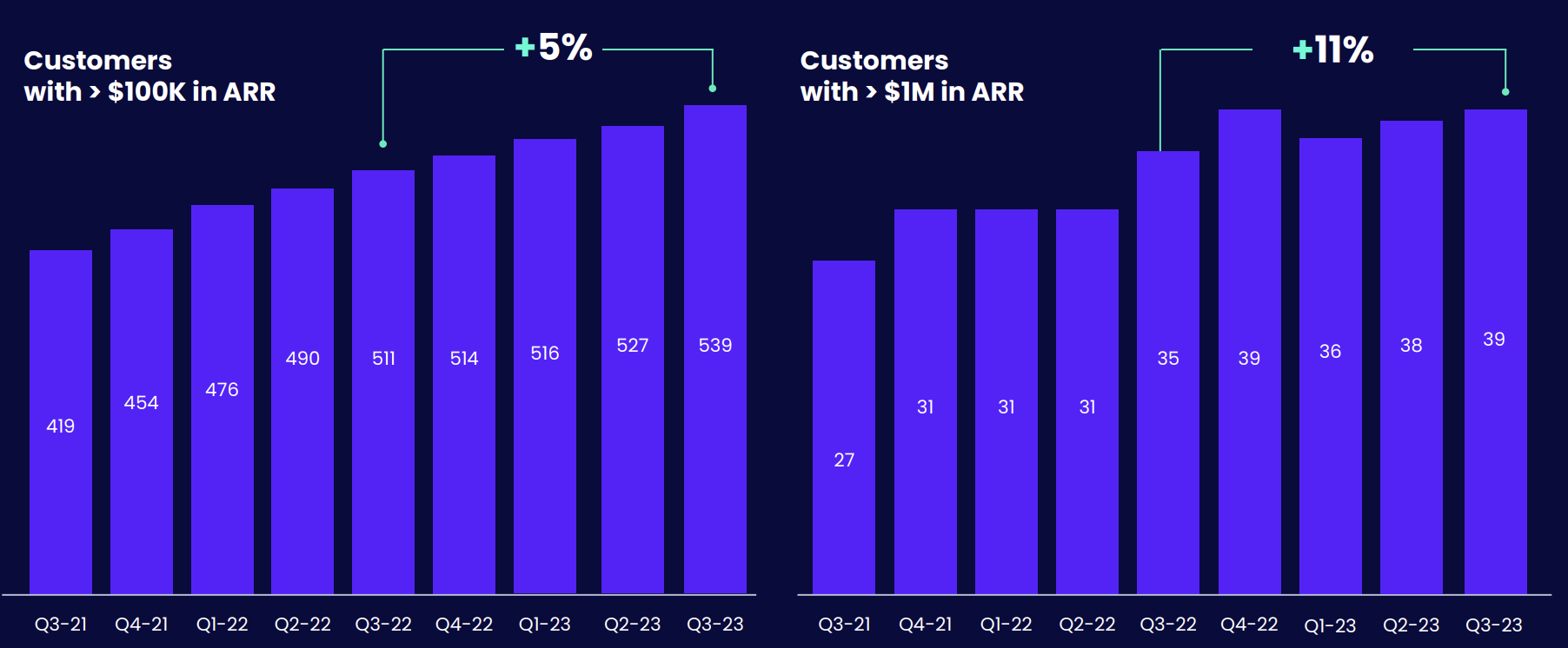

However, public sector showed strength in addition to higher quality ARR with 11 new DAP customers (vs. 10 net adds during H1) reaching a total of 194 total DAP customers and also gaining an additional $1M+ ARR customer during the quarter reaching a high of 39.

{kind=link}

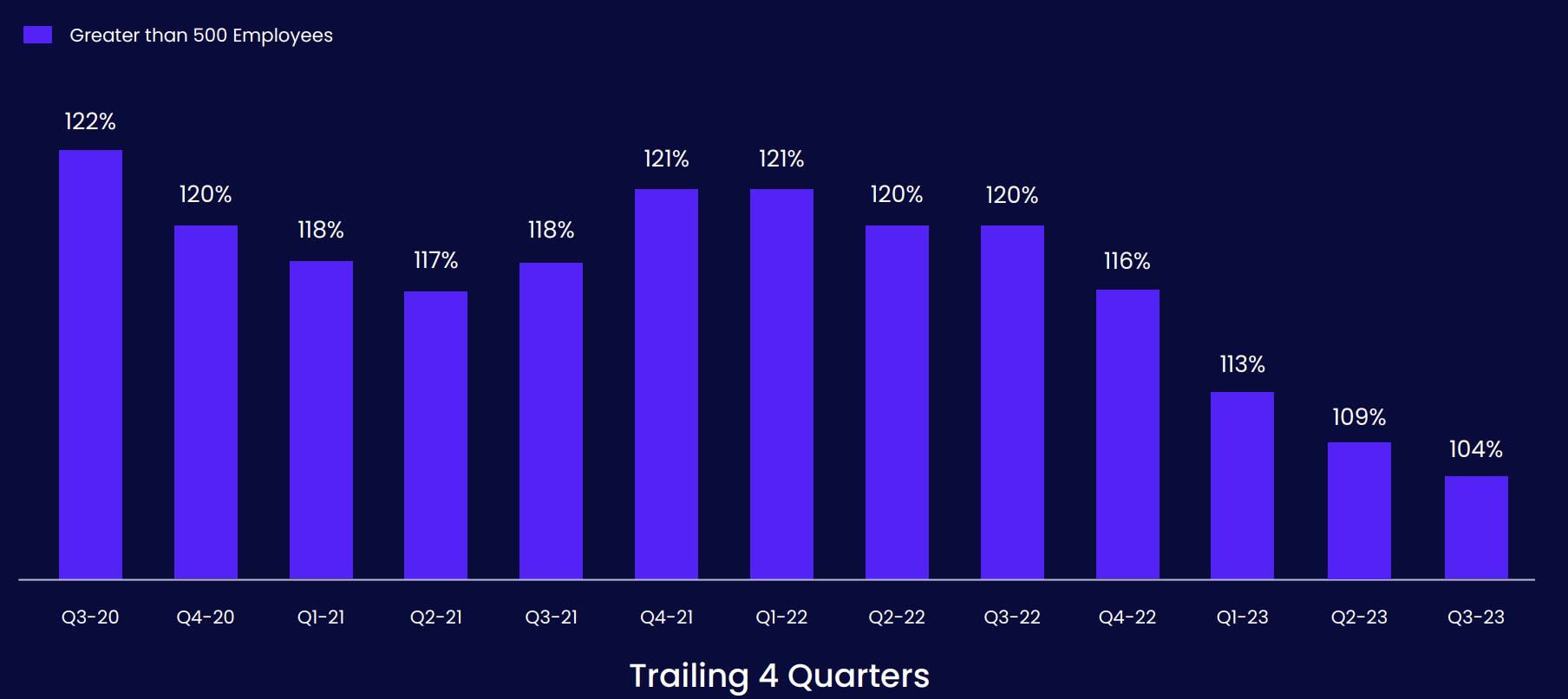

Management discontinued its provision of net retention ratio data for each quarter since it faced a significant churn during Q1 2023 and have been rather cryptic, providing trailing 4 quarter data in aggregate. The retention rates have been on the downward trend as it continues to face significant dollar churn, however, management noted that the trends have been positive through the year with Q3 retention being better than Q2 and Q2 retention being better than Q1. The improvement was driven by execution and easing macro headwinds with several projects brought back in action as part of the customer budgeting processes.

{kind=link}

Gross margin improved by about 5 percentage points to 85% with subscription gross margin of about 91%, up about ~200 bps as a result of improving utilization while professional services gross margins came in at 16% driven by better workforce utilization. Sales and marketing expenses leveraged by 12 percentage points, a massive improvement, driven by headcount reduction, better optimization of marketing channels, and improved GTM efficiencies. G&A also leveraged by 100 bps as a result of tight cost control. This helped the company to post a positive non-GAAP operating margin of 2.4%, significantly ahead of the estimates and a couple of quarters ahead of management plan. This also drove positive free cash flow of about $6 mn.

However, despite the robust improvement in profitability metrics, management guidance for Q4 remained lacklustre with revenues expected to be $67 - $68 mn, a 4% growth at mid point, further decelerating from the 6% growth it recorded in Q3. It guided for an non-GAAP operating profit margin of ~2-3%, in part helped by strong gross margin and cost control, however, near term challenging macro environment continue to weigh on the demand scenario and cripple growth.

Valuation

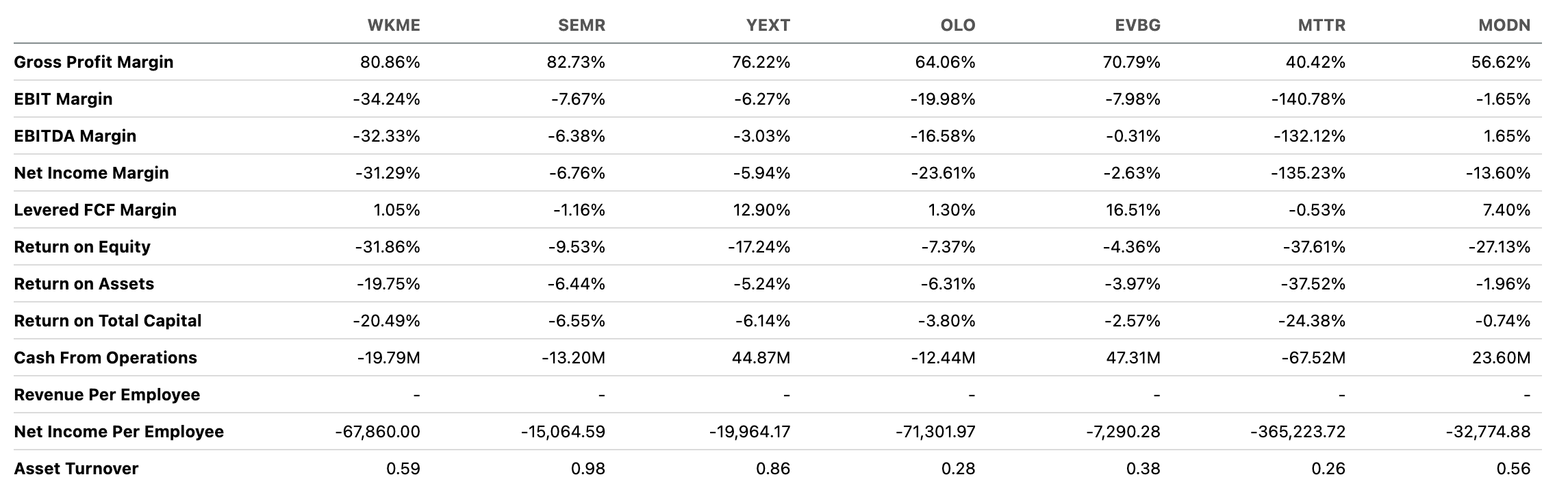

Considering the company's growth profile and lack of operating leverage building up to operating losses, we value WKME on an EV/ Sales approach, as is typical of a SaaS based growth company. The company trades at 2.3x EV/ Fwd Sales largely in line compared to the peer average of 2.6x.

In addition, despite its gross margin being at the top of the quartile compared to its peers, its operating margins remain relatively weak and rank among the bottom tier compared to its peer set. We believe a slight discount is warranted given WKME's scale, weak operating margin profile relatively and lower cash generation along with limited track record of execution as a listed entity compared to its peers. Given the near term uncertainties as a result of tough macro backdrop along with limited margin of safety, we initiate at Neutral.

{kind=link}

Risks to Rating

Risks to rating include

1) Selling and marketing expenses can increase as a result of competitive intensity and its bid to attract customers to drive growth

2) Adverse macro backdrop can result in further slowdown in technology spends which can dampen recovery and impact its operating margins

3) Upside risks include stronger than expected macro recovery leading to growing technology spends, shareholder activities such as dividends and share repurchases and operating leverage to drive higher margins

Final Thoughts

WalkMe had a tumultuous debut with shares down 65% since listing as COVID-19 pandemic jolted its recovery while the challenging macro backdrop and slowing technology spends lead to decelerating growth. We allude to the progress made in 2023 by WKME which was likely a transformational year wherein the company lowered its costs, drove positive operating margins and generated free cash flows.

However, the current valuation and persisting near term uncertainty provide limited margin of safety. Initiate at Neutral.

For further details see:

WalkMe: Demand Headwinds Weigh In On Profitability Improvements