WKME - WalkMe: Teed Up For Government Contracts

2023-06-13 07:48:56 ET

Summary

- WalkMe's software focuses on tracking user behavior and providing UI elements for product adoption, primarily targeting large customers.

- WalkMe's Q1 report showed slowing revenue growth amid cautious enterprise spending.

- With its FedRAMP-ready status, WalkMe has set up the public sector as its next growth lever.

Thesis

Despite being hit hard by reduced enterprise spending, WalkMe ( WKME ) should benefit from its strategic investments in the public sector. I would wait for Q3/Q4 earnings in case we get positive surprises.

What is WalkMe

WalkMe, founded in 2011, is a Digital Adoption Platform (DAP) that helps employees and customers to learn and use the abundant collection of home-grown and third-party software applications. Its functionalities allow workflow owners to create in-app content, nudging and validations to increase users' engagement and adoption. The DAP category has proven valuable given the abundance of applications in a company's tech stack these days (and therefore the number of applications each employee has to be get accustomed to). This leads to an impressive roster of companies adopting the WalkMe technology.

{kind=link}

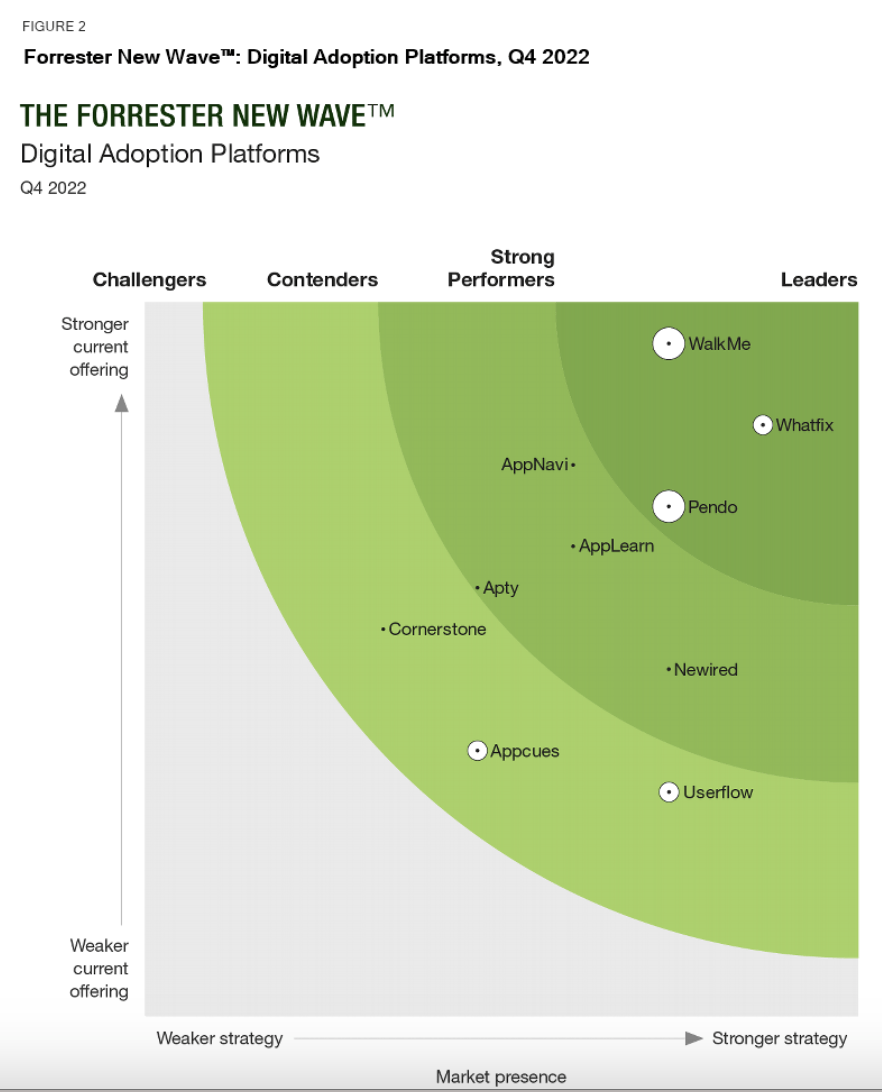

Competition and Moat

Digital Adoption Platform is a new rising product category. As you can see below in Forrester's overview of the landscape, competitions are mostly made up of small and medium sized companies. WalkMe is a market leader and the only publicly traded firm among them.

{kind=link}

The company has made an early strategic decision to focus on larger enterprise customers. In my opinion, this is a good strategy that takes advantage of the competitive landscape. Selling software to enterprise takes a different level of scrutiny. For example, it involves far more stringent security review, and also requires significant GTM maturity. By accustoming themselves to the process early, they not only gain a first-mover advantage with the large customers, they also create a moat for themselves against smaller rivals.

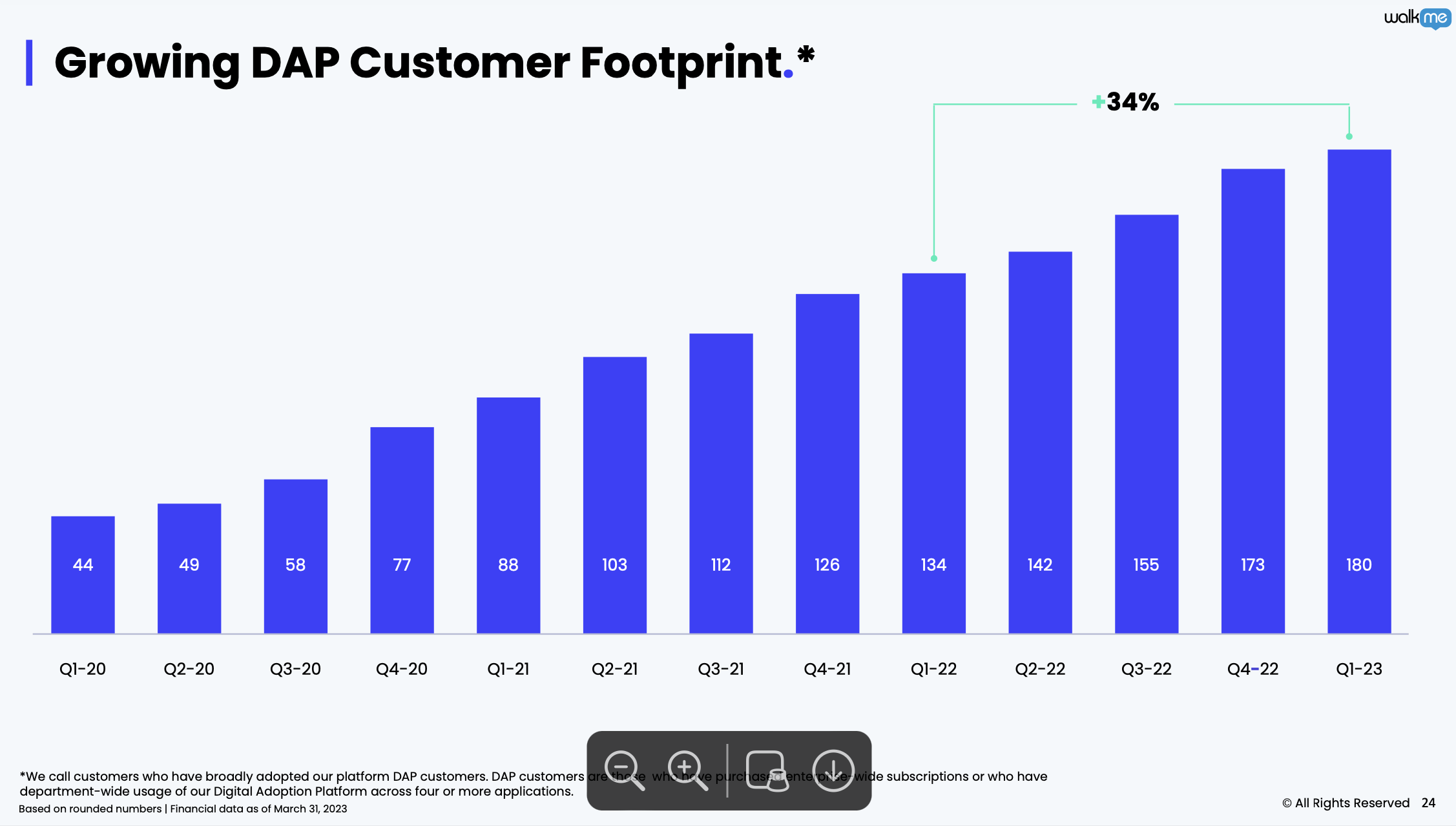

WalkMe, to its merit, has proven that they can sell big. As of today, the company boasts 31% of Fortune 500 as their customers. Between Q4 2021 and Q4 2022, the number of customers with >$1M ARR has increased from 31 to 39 . They also report healthy DAP customer growth , which is defined as customers "who have purchased enterprise-wide subscriptions or who have department-wide usage of our Digital Adoption Platform across four or more applications".

DAP customer counts (walkme.com)

{kind=link}

Recent Development

WalkMe's momentum has stalled amid the macro-economic backdrop. Q1's earnings were below expectation:

- QoQ revenue growth slowed to 1.6%, from ~5% a few quarters ago.

- Ending NRR of companies with 500 or more employees is 105% (and is likely at least three percentage points lower for smaller companies).

- Number of customers with >$1M ARR decreases from 39 to 36.

Turning to the Government Software Needs

Corporate market is likely to remain sluggish, but a positive development is WalkMe's announcement of their FedRAMP Ready status. Now fully certified, the company can go after more deals with the federal government. Government agencies, just like business corporations, run on multitudes of software today. Federal employees face the same problem of needing to get accustomed to the many customized or third-party software for their jobs. This create a significant opportunity for WalkMe's product.

Before fully certified, WalkMe has already helped the State of Georgia with their My Voter Page, the Department of Veterans Affairs with their HR modernization among others . This has proved the demand from the public sector, and the certification now opens up more GTM channels for the company. Management mentioned in the earning call that the public sector segment can contribute as much as 35%-40% of revenue when it is fully developed. The certification essentially turns into another competitive differentiator for them.

As fiscal year ends in September for government agencies, we should receive updates on the progress in the Q3 earning. As I mentioned before, the WalkMe team has demonstrated that they can execute, and I am willing to be patient with them.

Valuations

We can quantify the public segment potential using DCF valuations. We will set a base case where business grows with the current revenue mix, and a scenario where eventually 35% of revenue is from public segment, as management predicted.

We will make the following assumptions for both scenarios:

Cost of Equity

Cost of equity is calculated using the CAPM, i.e., risk-free rate + beta x equity risk premium.

- Risk-free rate = 3.79%, the rate of 10-year T-bill as of the date of writing

- Beta = unlevered beta of software industry x [1 + (1- marginal tax rate) x (debt/equity)] = 1.37 x [1 + (1-25%) x (192M/248M)] = 2.17, where unlevered beta and marginal tax rate come from Prof. Aswath Damodaran's estimation .

- Equity risk premium = 6%, the equity risk premiums again from Prof. Damodaran's estimations .

This gives us a cost of equity of 16.7%

Starting Numbers and Assumptions

Summing the numbers from the most recent 4 quarters :

- Starting revenue is $254M and net loss is $102M, resulting in a starting net margin of -36%.

- Management has guided for a revenue growth of 11% at midpoint for full year 2023.

- Net CapEx is assumed to be 2% of revenue and Change in WC is -7% of revenue based on averages from 2021 and 2022. Note that I do not add back stock-based compensation since I believe this is a real ongoing expense.

- Terminal Revenue growth = 4%

- Net Margin = 40%, similar to that of mature SaaS company

Denominator of the number of shares

- Current total shares outstanding = 87M

- Number of unvested RSUs = 6.6M

- Number of options outstanding = 279K at weighted average exercise price of $8.96.

Number of shares used as denominator = 87M + 6.6M + 0.28M * (9.34-8.96)/9.34 = 94M. RSUs and options are as of December 31, 2022 since they are not provided in the quarterly filing.

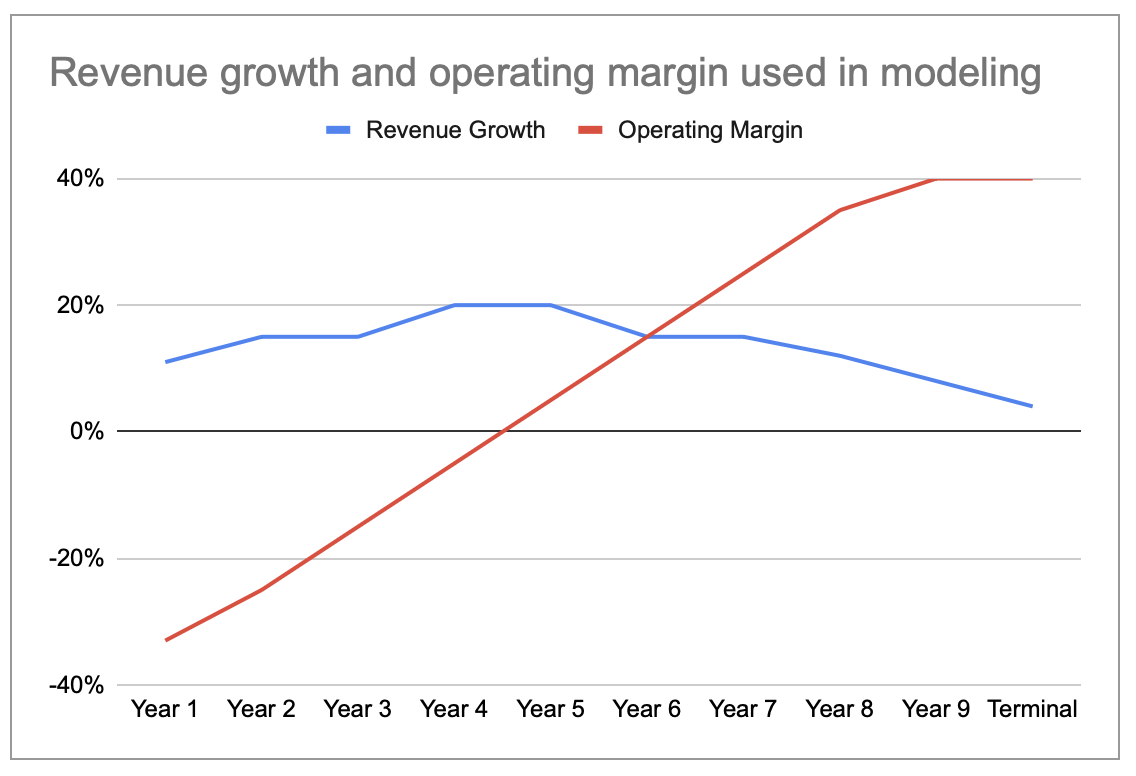

Revenue Growth & Net Margin

Since WalkMe still has negative earnings, I estimated 10-year cash flows to adjust the revenue growth and net margin each year to arrive at the terminal assumptions. The trajectory is as follows:

Revenue growth and net margin projections used in modeling (Author's assumptions)

{kind=link}

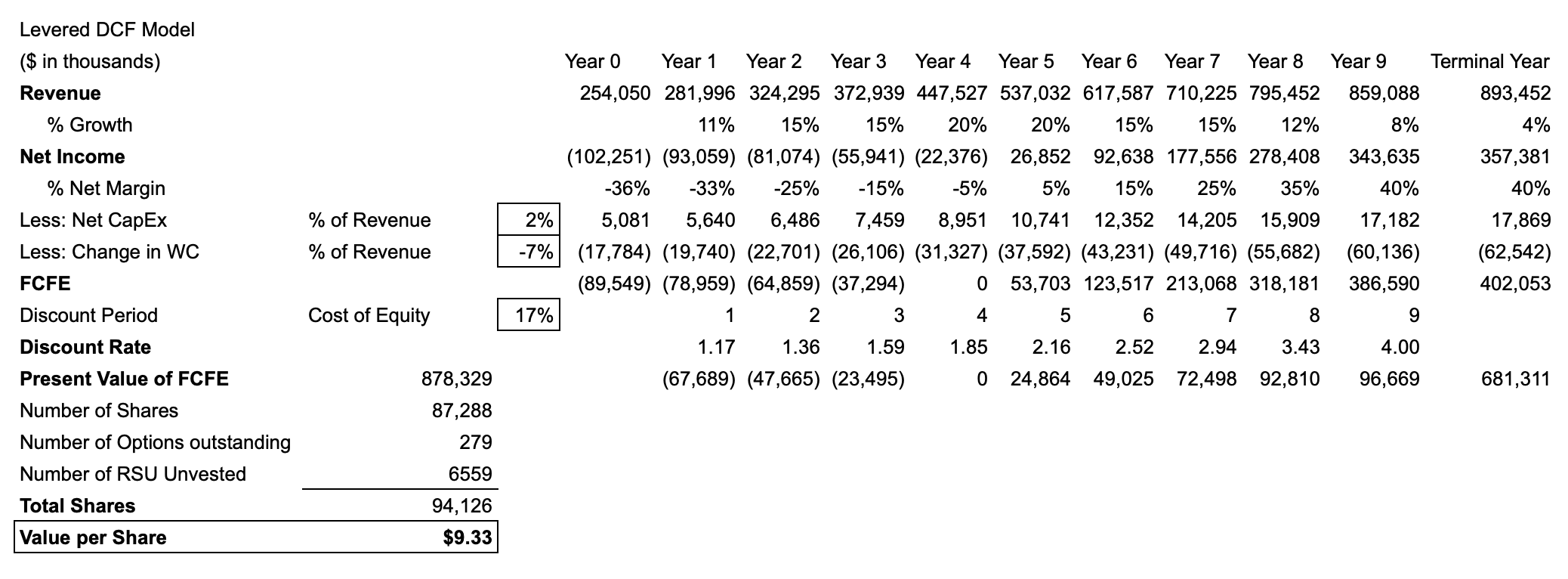

Base Case Valuation

Using the above assumptions, the base case valuation turns out as $9.33/share.

DCF valuation (base case) (Author's calculations)

{kind=link}

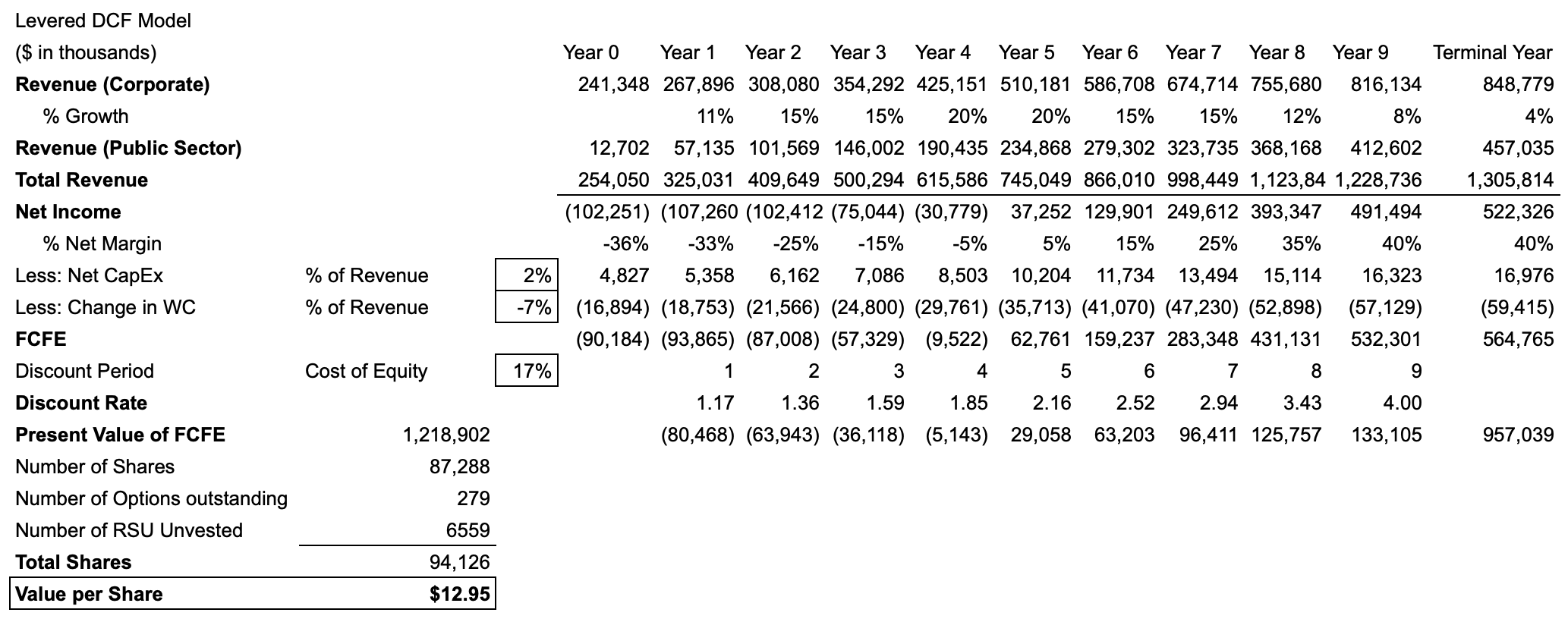

Valuation with Public Segment At Scale

To factor in the public segment growth, we add the assumptions that the contribution to revenue from the public segment is 35% at terminal (per management's commentary), and the public segment contribution is currently 5%. We further assume that public segment revenue grows linearly across the years to arrive at the terminal value.

This results in a valuation of $12.95/share, a 39% upside to today's price of $9.32/share.

DCF valuation for scenario where revenue contribution from public segment turns out as management has commented. (Author's calculation)

{kind=link}

Risks

Even though WalkMe seems to be on a solid path, there are several visible risks.

One concern is their NRR. Despite a large customer base, WalkMe suffers equally deterioration in NRR as its peers. The ending NRR for this quarter is 105%. It might be that its product is not as sticky as it seems. This can create a long-term weakness for WalkMe and the DAP category. It can become an easy target when companies are looking to cut costs and reduce software bloat.

Relatedly, since WalkMe mostly courts larger customers, churn of one customer will have a higher impact on its financials.

Lastly, affected by the macro-economic conditions, both governments and corporates may choose to delay their purchases and causes deal cycle to lengthen further. This gives smaller rivals valuable time to catch up and compete with WalkMe.

The Bottom Line

Enterprise demand is slowing. This impacts WalkMe's corporate business and I don't expect any material improvement before the end of the year. However, the company remains solid and continues to execute on its long term strategy. While the stock is at fair price, it has presented clear growth levers in the public segment.

For further details see:

WalkMe: Teed Up For Government Contracts