SCHQ - Wall Street Desperately Begs For The Pause - But More Rate Hikes Are Likely Coming

2023-05-05 12:05:59 ET

Summary

- Wall Street expects the Fed to pause in June and subsequently to cut.

- However, the Fed will likely hike in June and July.

- The S&P 500 is very likely to sell off sharply in this environment.

Let's all call for a recession now

Everybody on Wall Street is now united in calling for a recession. Why? Because it's convenient, they want the Fed to pause and cut. But Powell says, sorry no recession, meaning more hikes are likely coming.

Here is what Bloomberg reports as the immediate reaction to the Fed's May decision to hike by 25bpt:

DoubleLine Capital's Jeffrey Gundlach told CNBC that "recessionary odds are pretty darn high right now" and "the Fed likely won't lift interest rates again following its latest increase". Meanwhile, over at the Milken Institute Global Conference, talk among the panelists suggested a consensus view that a contraction is inevitable.

The recession is imminent, but the Fed will likely continue to hike into the recession, which is the worst-case scenario for the markets. Wall Street is aware this could lead to a much deeper and longer recession, with widespread bankruptcies and defaults, but this is possibly what it takes to bring inflation down to 2%.

The Fed is now data dependent

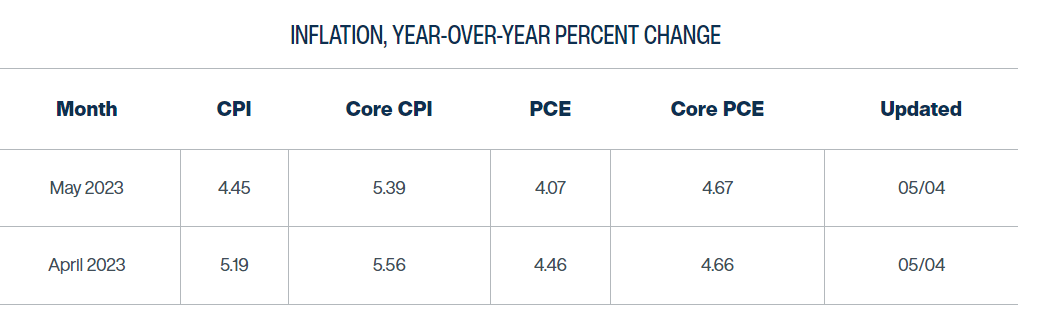

These are the targets for 2023 in the Fed's Summary of Economic Projections (SEP):

- 5.1% Federal Funds rate (current 5.07%)

- 4.5% unemployment rate (current 3.4% for April)

- 3.6% core PCE (current 4.6%)

The Fed has reached the 5.1% target for the Federal Funds rate with the hike at the May meeting. Based on the SEP projections, the Fed will now pause for the rest of 2023.

However, the unemployment rate at 3.4% is still way too low, and the inflation rate at 4.6% is still way too high. Thus, Powell acknowledged that the Fed will be data-dependent from this point on.

The Fed will also update the SEP projections at the June meeting, and it is likely that it will upgrade the expectations for the Federal Funds rate - and hike by 25bpt.

Inflation still very high, unemployment still very low

Here is the stunning fact that Powell "dropped" at the (May) post FOMC press conference - the current unemployment rate at 3.4% is well below the 3.8% unemployment rate in February 2022 - despite the 5% increase in the Federal Funds rate since March 2022. This fact is truly stunning.

Powell was very clear that "labor market is very tight" and "inflation is well above the target". Let's emphasize the wording: "very tight" and "well above". The Fed has a dual mandate, price stability (currently defined as 2% inflation), and full employment. Obviously, the Fed's primary focus is still inflation.

Here is the actual Powell statement from the post FOMC meeting press conference:

The labor market remains very tight. Over the first three months of the year, job gains averaged 345 thousand jobs per month. The unemployment rate remained very low in March, at 3.5 percent. Even so, there are some signs that supply and demand in the labor market are coming back into better balance. The labor force participation rate has moved up in recent months, particularly for individuals aged 25 to 54 years. Nominal wage growth has shown some signs of easing, and job vacancies have declined so far this year. But overall, labor demand still substantially exceeds the supply of available workers.

Inflation remains well above our longer-run goal of 2 percent. Over the 12 months ending in March, total PCE prices rose 4.2 percent; excluding the volatile food and energy categories, core PCE prices rose 4.6 percent. Inflation has moderated somewhat since the middle of last year. Nonetheless, inflation pressures continue to run high and the process of getting inflation back down to 2 percent has a long way to go.

The unemployment rate is a lagging indicator, and it's likely not reflecting the slowing economy. Thus, Wall Street hopes that the Fed would cut preemptively - before the unemployment rate spikes. But Powell explains that" labor demand still substantially exceeds the supply of available workers".

Obviously, there is a labor shortage. This is keeping the unemployment rate low despite the aggressive monetary policy tightening and complicating the Fed's job.

Thus, the Fed might be forced to drastically reduce the demand for labor to bring the labor market in balance - and this suggests further hikes (into the recession) to engineer the hard landing, which is what the Wall Street fears.

The Fed to hike in June and July

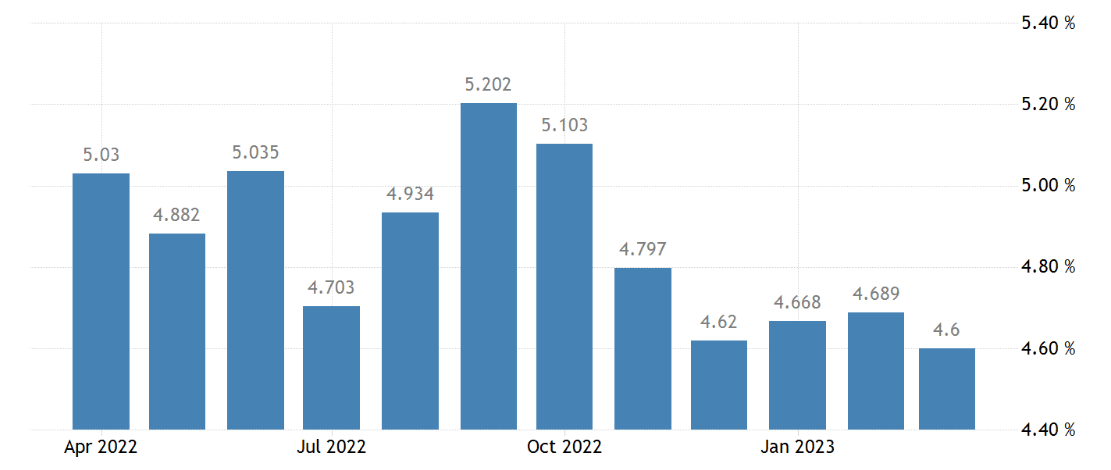

The Cleveland Fed publishes Inflation Nowcast, which has been back-tested and proven to be fairly accurate. So, these are the current projections for April and May:

{kind=link}

The Fed will meet on June 14th, and look at the 4.66% core PCE number for April, which is above the 4.6% print for March. Hey, inflation is actually rising! Obviously, if the 4.66% projection for April proves accurate, the Fed will have no choice but to hike.

The Fed will meet again on July 26th, and stare at 4.67% core PCE number for May, which is projected to equal, if not exceed, the April's print. And then, the Fed will look at the recent core PCE data and observe that core PCE has been at the 4.6% level since Dec 2022. Inflation has plateaued at a very high level, well above the 2% target! The Fed will have no choice but to hike again in July.

{kind=link}

What about the recession?

Currently, the real GDP is projected to be around 0% for Q2 2023, and then to contract in Q3 and Q4 2023. Essentially, we could be in a recession already. For example, this is the current ING GDP forecast for the US:

{kind=link}

The banking crisis is expected to produce credit tightening, which is expected to result in lower consumption and an increase in the unemployment rate. But, the data is not going to show this over the next 2-3 months, and the Fed is data dependent. Powell was clear that the Fed needs to see "months of data" to conclude that inflation is falling towards the 2% target over time.

Thus, the Fed will likely be forced to hike into the recession, which is likely to deepen and prolong the expected recession, which is what Wall Street fears the most.

Implications

The Fed could pause and cut, as the Wall Street currently expects, under only one condition - the stock market sells off sharply well below the October lows. For S&P 500 ( SP500 ), this would be the selloff to the 3200 level.

The selloff of such magnitude would "kill" the sentiment and accelerate the disinflationary process. I think that the probability of such a stock market "crash" is very high. Wall Street is begging for the pause and the cuts, but the Fed will likely continue hiking.

Once the Wall Street bulls give up with the counter-Fed liquidity-boosting speculative bets, the Fed would be able to accommodate the markets and cut.

For further details see:

Wall Street Desperately Begs For The Pause - But More Rate Hikes Are Likely Coming