KHC - Wall Street Lunch: No Refills

2023-08-02 13:55:00 ET

Summary

- U.S. scraps offer to buy 6M barrels for SPR; ADP jobs report exceeds expectations in July.

- Arm eyes for $60B IPO next month; CVS launches company-wide restructuring.

- Morgan Stanley bear Wilson says monetary policy to drive late-cycle rally for 2023.

Listen below or on the go on Apple Podcasts and Spotify

U.S. scraps offer to buy 6 million barrels of crude for the SPR (0:15). ADP jobs report exceeds expectations in July. (1:57) Arm eyes $60 billion IPO next month. (3:52)

This is an abridged transcript of the podcast.

Our top story in today’s session –

The U.S. government has withdrawn its offer to buy 6 million barrels of oil for the Strategic Petroleum Reserve as crude prices continue to rise.

The Energy Department made the purchase offer on July 7, saying it would "pursue additional repurchase opportunities as market conditions allow." After the offer was withdrawn, a spokesperson said the department "remains committed to its replenishment strategy."

The government released a record 180 million barrels from the SPR in 2022 to rein in gas prices that surged after Russia's invasion of Ukraine. It later said it would replenish the reserve once prices were at or below $67 to $72 per barrel, with 6.3 million barrels reportedly bought back in recent months.

Energy Secretary Jennifer Granholm previously said it is "definitely possible" that the government will ramp up SPR buying, but warned that a complete refill is unlikely any time soon.

Crude prices just saw their best monthly gain in more than a year, with benchmark WTI (CL1:COM) trading above $80 per barrel.

Now a look at today’s trading –

Stocks are lower, with growth struggling as longer-term rates rise.

The Nasdaq (COMP.IND) is down nearly 2%, while the S&P (SP500) is off about 1% and the Dow (DJI) off more than 0.5%.

The megacap sectors are performing the worst, with Info Tech (XLK) the weakest. Healthcare (XLV) is the only gainer, slightly in the green.

The 10-year Treasury yield (US10Y) is up as it bumps against 4.1%.

The Treasury outlined its plans to raise $103 billion with new Treasury issuance this month, which, along with sales, will raise $19 billion in new cash. Based on projected intermediate- to long-term borrowing needs, the Treasury says it "intends to gradually increase coupon auction sizes beginning with the August to October 2023 quarter."

Before the bell, ADP reported a much bigger jump in hiring for July than expected. Private payrolls rose by 324,000, well ahead of the consensus of 185,000.

But Pantheon Macro says that ADP is "utterly useless" in predicting the official nonfarm payroll figures. ADP reported a rise of nearly 500,000 for June, with the BLS print just 149,000.

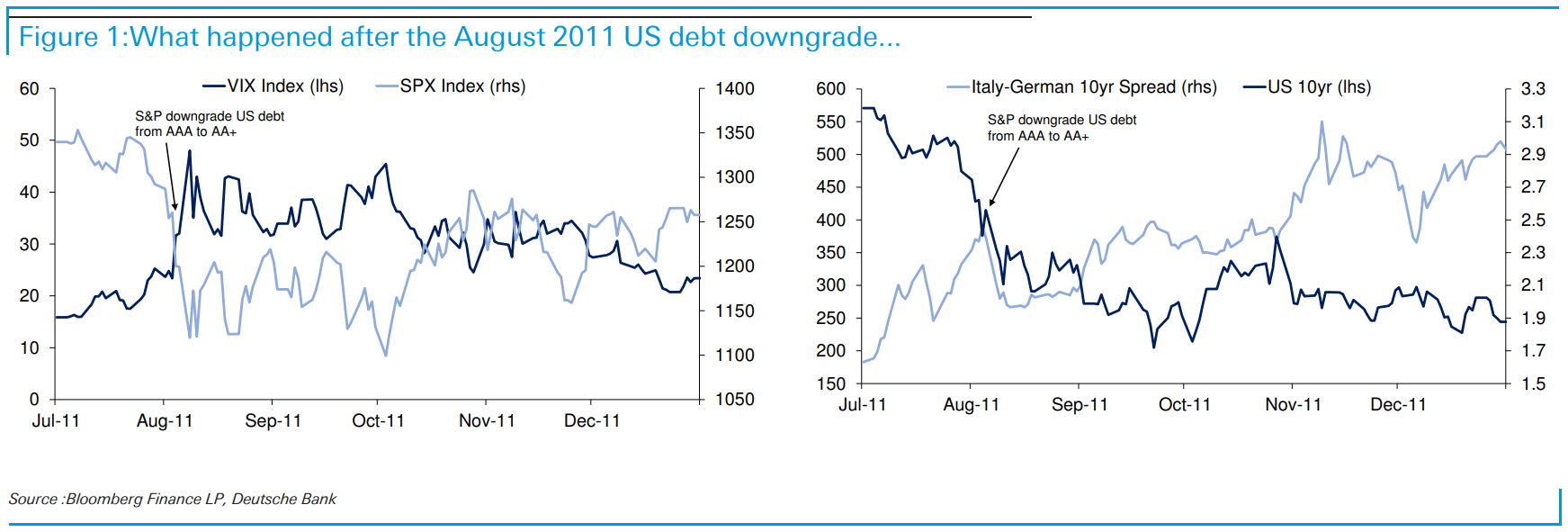

Traders are also still digesting the Fitch decision to downgrade U.S. long-term debt.

You can check out a chart that shows what happened to the market and the VIX (VIX) following the last downgrade by Standard & Poor’s in 2011.

{kind=link}

Among active stocks –

Yum Brands (YUM) reported a 9% increase in same-store sales in Q2 to top the consensus expectation of a 7.1% gain – with a helping hand from The Colonel. System sales rose 19% at KFC, Taco Bell posted 7% growth, and Pizza Hut was up 7%.

Pinterest (PINS) slipped even as Rosenblatt upgraded the social network after second-quarter results. Analyst Barton Crockett raised his rating to Buy from Neutral and boosted his price target to $35 from $27. He says, unlike its peers, the company is building better ad tools and using better AI engines.

Kraft Heinz (KHC) reported that organic sales rose 4% in Q2, with an 11% rise in pricing offsetting a sharp 7% decline in volume. The organic sales tally was short of the consensus estimate of +4.6%. Organic sales were up 1.3% for the North America business and rose 13.2% for the international.

CVS Health (NYSE) announced a company-wide restructuring initiative after reporting a sharp drop in its quarterly net income. CVS faced rising costs in its pharmacy and insurance units.

Among other stories of note -

Arm, the British chip design firm owned by SoftBank (SFTBY), is reportedly targeting an IPO worth some $60 billion that could happen as soon as next month.

The offering could raise as much as $10 billion, and the roadshow is slated to occur the first week of September, with pricing set for the following week. That’s according to Bloomberg, who cited people familiar with the matter.

While the $60 billion valuation on Arm is underscored by appetite for AI, executives for the company could try to press for an $80 billion valuation.

It was previously reported that the valuation for the firm had ranged between $30 billion and $70 billion.

Last month, it was reported that Arm had spoken to Nvidia (NVDA) about being an anchor investor in the offering. Arm has also spoken to a number of tech companies about participating, including Intel (INTC), Alphabet (GOOGL), Apple (AAPL), Microsoft (MSFT), Taiwan Semiconductor (TSM), and Samsung (SSNLF).

In the Wall Street Research Corner –

Noted bear Mike Wilson is spying a late-cycle rally driven by policy right now.

Morgan Stanley strategist Wilson, who has been bearish on equities through the 2023 rally, says current conditions look similar to 2019, when the S&P 500 rose 29%. That was the best performance since 2013.

Wilson says "the positive policy impact has been supported by a very strong fiscal impulse, a still supportive global liquidity backdrop and optimism that the Fed can now transition to easier monetary policy given the falling inflation data."

"The latest example of such a period occurred in 2019, but for somewhat different reasons - the Fed definitively paused and then cut rates and the Fed's balance sheet began to expand toward the end of the year."

He adds that in 2019 and now, megacap tech has led and growth has outperformed value as equity market internals process a path to easier monetary policy."

"The 2019 analogy, in and of itself, suggests more index level upside from here."

But J.P. Morgan’s global strategy team still isn’t buying the soft landing scenario.

They are "anticipating the inflation decline to prove incomplete," which would leave restrictive central bank policies in place that should "increase private sector vulnerabilities and end the global expansion."

They add that equity multiples remain too high and that rate cuts in developed economies look unlikely in the near term.

In contrast, BofA is now revising its outlook to call for a soft landing "where growth falls below trend in 2024, but remains positive."

It predicts "U.S. GDP growth of 2% (4Q/4Q) this year."

"Growth in economic activity over the past three quarters has averaged 2.3%, the unemployment rate has remained near all-time lows, and wage and price pressures are moving in the right direction, albeit gradually," BofA added.

For further details see:

Wall Street Lunch: No Refills