WLBMF - Wallbridge Mining: High Risk Potentially High Reward

2023-04-04 16:08:36 ET

Summary

- Wallbridge has declined 90% from the peak a few years ago and has only recovered a small amount, despite the strong gold price.

- So, the risk-reward is now relatively attractive for this high-risk investment.

- The company is due to release a PEA in Q2-23, which has the potential to be an important catalyst for the very depressed share price.

Overview

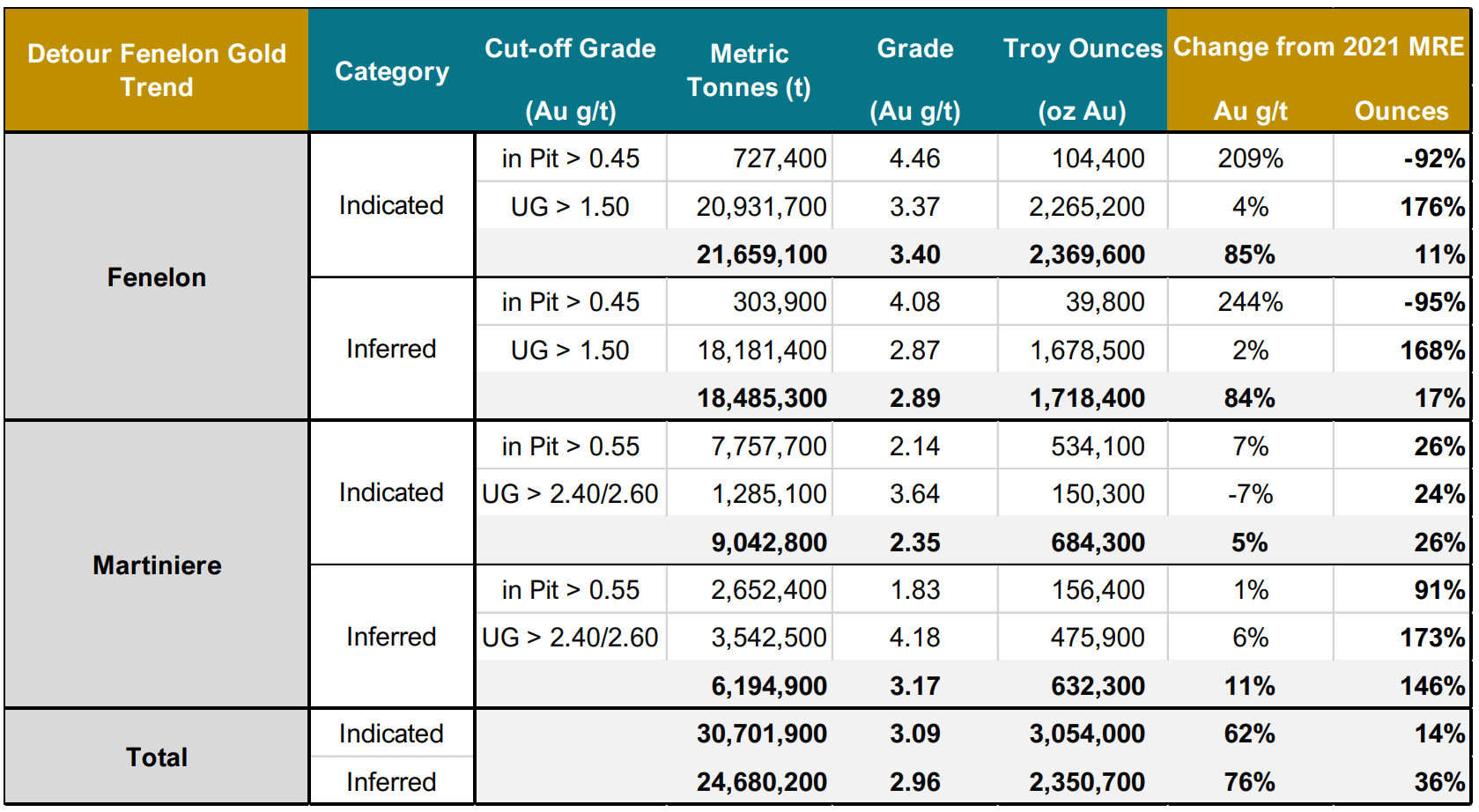

Wallbridge Mining ( WLBMF ) is a Canadian precious metals development and exploration company with assets in Quebec. The company gets most of its value from the Fenelon deposit, which as of the latest 2023 resource update had 4.1Moz of gold resources, much of it in the indicated category. Martiniere is another gold deposit close by, which currently has 1.3Moz of gold resources. The company has a few other minor exploration interests, but in this article, I will focus on the key Fenelon and Martiniere projects.

There is a PEA due to be released during the second quarter of 2023, which will be focused on Fenelon, as Martiniere is probably a year or two behind Fenelon in the development phase.

{kind=link}

Figure 1 - Source: Wallbridge Presentation

Wallbridge has over the last few years underperformed the price of gold and precious metals miners by quite a lot, despite growing the resource ounces. The economic estimates are now due to be released in the next few months with a PEA, which has the potential to be a good catalyst for the company.

This is an early exploration and development company, which means there are substantial risks involved in an investment. However, the core assets are in a very favorable mining jurisdiction, have over 5Moz of gold resources already, and a fairly good chance of becoming a mine. So, given the weak stock price lately, I like the risk-reward at this level.

Figure 2 - Source: YCharts

Stock Price & Potential Risks

The stock price of Wallbridge has gotten severely punished since the peak in September of 2020. It has declined by a massive 90% from the top and has not recovered much from the low. The stock likely got ahead of itself during the run up, but the decline has been extraordinary.

The chart below is a good illustration of how poor the sentiment has been over the last few years for some of the smaller development companies in the precious metals industry. Even if we have seen the price of gold recover lately, that has not trickled down to some of the smaller companies in the industry.

{kind=link}

Figure 3 - Source: Koyfin

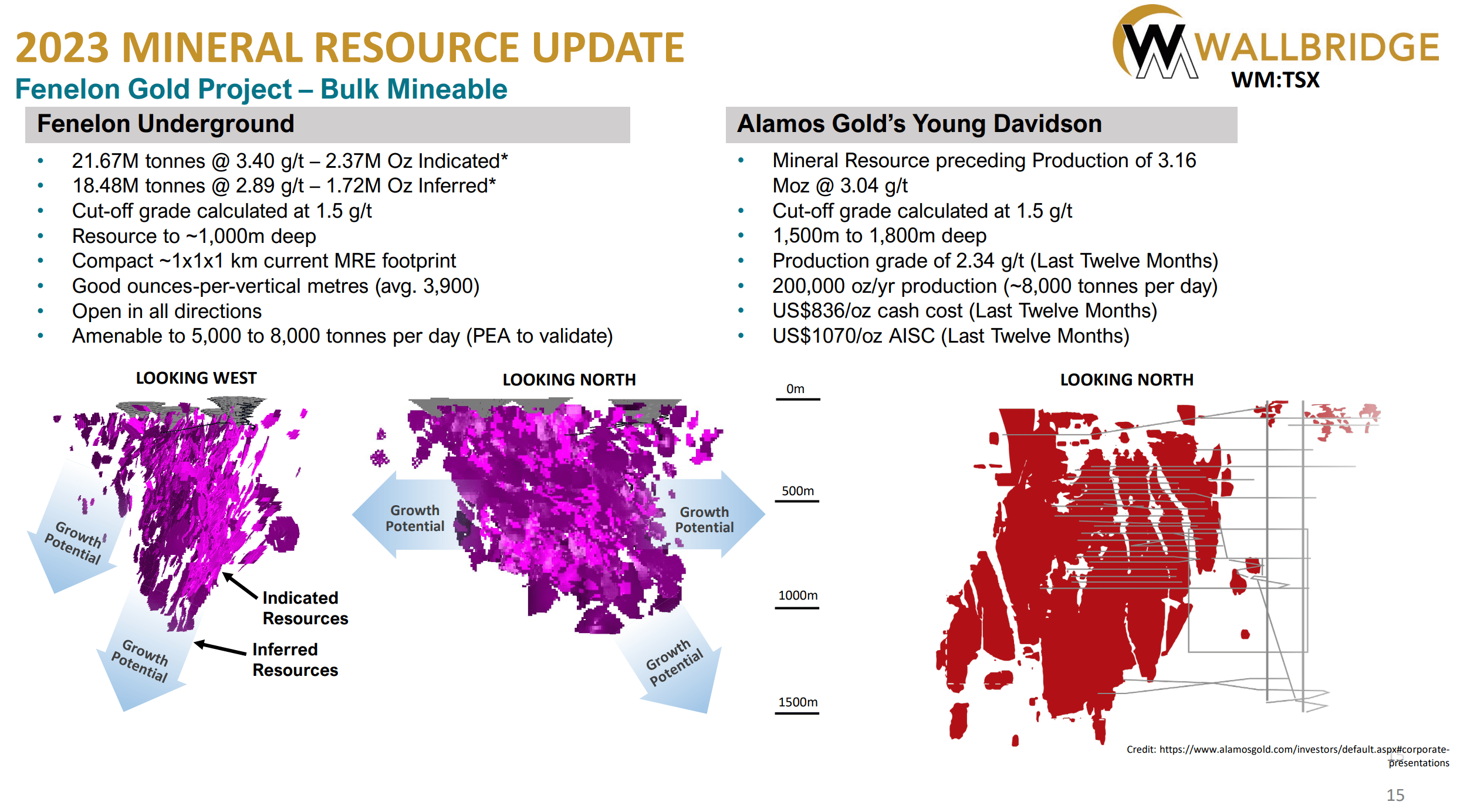

Wallbridge did historically indicate that Fenelon might be suitable for a reasonably large open pit project together with underground mining at depth. Given how expensive it has become for building large scale operations like that lately, the market increased its skepticism about the project. The company consequently pivoted Fenelon more towards an underground project, which should simplify the permitting process, and lower the initial capital cost.

Some would argue underground mining might be a challenge given somewhat lower underground grades. However, we are talking about bulk underground mining with a healthy thickness of the mineralization, where other similar assets with comparable grades can profitably operate. So, I do think Fenelon has a good chance of becoming a mine when one considers the size, grade, and tier 1 location.

{kind=link}

Figure 4 - Source: Wallbridge Presentation

When the 2023 resource update was released, there were some concerns about the lack of growth in the number of ounces from the 2021 resource update. However, that is perfectly natural given the pivot to more underground mining with a higher cut-off, where the improvements will be seen more so in the average grade, as is illustrated in the chart below, where the average grade has now increased to about 3 g/t gold.

{kind=link}

Figure 5 - Source: Wallbridge Presentation

Without a PEA, we can only speculate on all the economic numbers, but I do think it is fair to say the initial capital cost will be a massive challenge for Wallbridge, unless the sentiment turns around from these levels. However, that is true for almost all development companies today, except for companies with plenty of cash, lower initial capital costs, and a larger market cap. So, that is a risk one has to accept for earlier stage development companies.

Another risk to be aware of is the share dilution. Wallbridge is an earlier stage development company without revenues. That means the company will continue to fund itself in the equity market. So, some share dilution is to be expected each year. One positive aspect about drilling in Quebec are the tax credits the company gets on all exploration, where the company presently has C$18.2M in accounts receivable. This allows Wallbridge to stretch the value of the money raised each year.

{kind=link}

Figure 6 - Source: Q4-22 Financial Statement

Market Value

Wallbridge presently has 934M shares outstanding, a few million share units, and a small amount of in-the-money options. The 0.5M warrants that remain and most of the options have anti-dilutive exercise prices, they are consequently not included. So, the fully diluted share count is 939M, which includes the February/March 2023 private placements.

{kind=link}

Figure 7 - Source: TradingView & Q4-22 Financial Statement

That gives us a market cap of $111.9M. The company has $24.5M in cash, mostly held in Canadian Dollars, and no debt. So, the enterprise value is $87.3M

Value & Conclusion

{kind=link}

Figure 8 - Source: Wallbridge Presentation

Fenelon and Martiniere now contains 5.4M resource ounces of gold with a grade around 3 g/t. The company has up until Q4-22 spent C$227M on the two key exploration and development projects.

{kind=link}

Figure 9 - Source: Q4-22 Financial Statement

Given that Wallbridge does not yet have a technical report with economic estimates, with the PEA due in the next few months, there is a very large degree of uncertainty in the economic value of the assets. Having said that, I would roughly estimate the NPV for Fenelon and Martiniere to be somewhere in the $400M to $1,000M range.

The company presently has a market cap of only $112M together with a decent amount of liquidity. So, even if the economic value turns out to be in the lower end of that range, Wallbridge looks like a good risk-reward at this level.

I view Wallbridge as a high-risk investment. While I think it has relatively good chance of eventually becoming a mine. There is also a substantial chance of an almost total loss of capital if the industry sentiment continues to be poor and there are no larger mining companies interested in the project. I have consequently used a smaller position size in this investment that reflects the larger risk.

It should be noted that Agnico Eagle did spend about C$1M in March of 2023 to maintain its 9.9% ownership interest in Wallbridge. So, the company is not completely without institutional interest today.

For further details see:

Wallbridge Mining: High Risk, Potentially High Reward