INBKZ - Want To Buy A Beaten Down Bank Stock? Here's A List And Analysis

2023-05-08 00:48:23 ET

Summary

- Thirteen badly beaten-up bank stocks are reviewed and compared to those that were recently taken over.

- Items reviewed include uninsured deposits, risky activities, unrealized investment losses, capital ratios, ROE, performance in the last recession, and loan growth.

- A chart comparing all the banks and a paragraph on each bank is included.

- This is a cursory review or starting point, if you wish to invest more due diligence would be needed.

Background

In the past two months, three large banks (Silicon Valley Bank, Signature and First Republic) have been taken over by the FDIC due to liquidity problems. I have been involved in banking my entire career starting as a government Bank Examiner. Over a thousand banks and S&Ls have failed in that time and I do not recall one that was taken over due to illiquidity. I also don't recall one that was taken over when having more than adequate capital on their last financial statement. In most cases, when a bank is taken over it's due to a high level of bad loans combined with insufficient capital. There are a number of reasons why illiquidity suddenly became an issue. These include a large amount of uninsured deposits at a few banks. This is an age of electronic banking where massive shifts in deposits can occur with a few keystrokes. Also, there are also more banks involved in non-traditional banking activities such as crypto, venture capital, and fin-tech. Signature was involved in the first and Silicon Valley the second.

The takeover of these three banks caused a panic in the other bank stocks. The SPDR S&P Regional Banking ETF ( KRE ) is down a whopping 34.2% year to date. I strongly believe that the FDIC is at fault for much of this decline. The takeovers of Signature and First Republic were unnecessary as both were adequately capitalized and had access to, or could have been given access to, the necessary liquidity. Bank stocks were hit hard after each takeover. I actually said in my recent article on banks dated March 20 that if the FDIC took over First Republic all hell would break loose. It certainly did, though things stabilized the next day after the SEC indicated it would go after market manipulators of bank stocks. They actually did that in 2008, so it was not an idle threat. The amount of rebound indicates market manipulation was also a major factor.

Most banks in the KRE index are not down as much as it is. The KRE is skewed by almost 100% losses in the 3 banks that were taken over. But there are a number down more than the KRE and are now trading well below book value. This article looks at 13 of the most distressed bank stocks. I included only midsized and larger banks that have significant stock liquidity.

The banks that are beaten down the most tend to have one of the following characteristics:

- a large amount of uninsured deposits

- a large amount of unrealized losses on investments

- significant non-traditional banking activities or rapid loan growth

If you look at the chart below, the 3 that were recently taken over all had huge ratios of uninsured deposits and unusually rapid loan growth the past 3 years. Rapid loan growth was also a big factor in determining which banks went under in 2008-2012 when 465 banks and S&Ls went under.

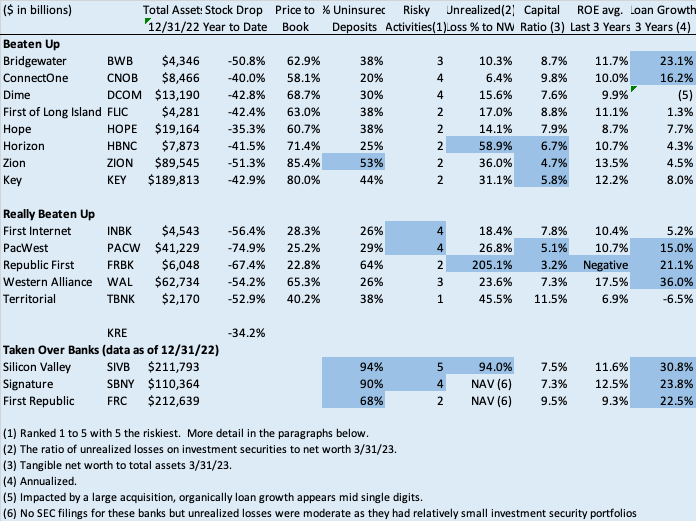

Distressed Bank Stocks

The chart below has three categories; beaten down stocks, really beaten down stocks and the 3 that were recently taken over. All but one is down over 40% this year and most are trading 1/3 or more below book value. The highlighted areas are those that are particularly problematic.

FDIC, Value Line, Yahoo Finance and SEC filings

{kind=link}

A paragraph on each bank is provided below. Please be advised this is only a cursory review of these banks. If you are interested in buying any, more due diligence would be required.

Bridgewater ( BWB )

Bridgewater is a newer rapidly growing bank located in the Twin Cities area of Minnesota. It has benefitted from several local mergers resulting in rapid growth. However, I believe it's that rapid growth the market is holding against it. Bridgewater is a traditional bank with higher than normal levels of loans in multifamily real estate and construction and land development. The latter is a higher risk loan type. I actually owned this stock last year but sold when I started to expect a recession as rapid growth banks have a well below average track record in recession. This is because of an unseasoned loan portfolio.

ConnectOne ( CNOB )

ConnectOne is a traditional New Jersey based bank. It has a small investment portfolio, so much lower than peer unrealized losses. The capital ratio is normal. It recently significantly reduced its uninsured deposits to a normal level. The biggest issue appears to be recent rapid loan growth. There is also a heavy concentration of commercial real estate. Many experts are expecting a lot of losses there in a recession. The largest portion is multi-family real estate. More due diligence is needed to find out how much is office and retail space. If it's a lot then that may be a big problem. ConnectOne did relatively well in the 2007-2009 recession.

Dime ( DCOM )

Dime is quite similar to ConnectOne as it is also a NYC area based bank with heavy commercial real estate exposure. Like ConnectOne, a lot of that is multi-family real estate and more due diligence is needed to see how much is office and retail real estate. It also has few unrealized investment security losses and adequate capital. Dime had a major acquisition two years ago that doubled its size. Organically, it has not been the rapid grower ConnectOne has been. Dime FKA Bridge Bancorp did well in the 2007-2009 recession.

First of Long Island ( FLIC )

First of Long Island is a traditional bank with low growth, low unrealized investment securities losses, a normal level of higher risk activities, and adequate capital. The issue appears to be its earnings and margins are getting heavily squeezed by interest rates. Earnings last month were cut in half from a year ago. They have a large portfolio of residential loans, which are low credit risk but high interest rate risk. But that doesn't mean the bank is in any jeopardy. First of Long Island struggled in the 2007-2009 recession.

Hope ( HOPE )

Hope is a traditional bank based in Los Angeles primarily serving the Korean community. It is quite similar to FLIC in that it has moderate growth, low unrealized investment securities losses, a normal level of higher risk activities, and adequate capital. Its margins are also getting squeezed, but not as much as FLIC. I really don't understand why it's on this list but I'm sure more due diligence will turn up the reasons. Hope struggled in the 2007-2009 recession.

Horizon ( HBNC )

Horizon is the bank I retired early from 10 years ago. I can personally attest the credit quality is quite good. The Chief Lending Officer I reported to was relatively conservative. He retired about two years ago, so his imprint is still there. The CEO is also conservative. Horizon has grown by acquisition mostly, though often in second tier markets. The problem is their large investment security portfolio. It has a large amount of unrealized losses. Combined with a relatively low tangible net worth ratio, it leaves little capital after unrealized losses. As of December 31, 2022, tangible net worth after unrealized losses was 2.2% of total assets. This of course is a problem that goes away when interest rates come down. In the meantime, the high level of fixed rate investments is also squeezing the profit margin. Uninsured deposits are normal versus the peer and they have not been losing deposits. Horizon did well in the 2007-2009 recession.

KeyCorp ( KEY )

Key is a traditional bank with all the offerings of a large regional such as wealth management and capital markets activity. The loan portfolio is below average risk as it is over half commercial loans and a relatively low amount of commercial real estate. Uninsured deposits are somewhat high versus the peer. The biggest issue appears to be a low tangible net worth ratio of 5.8%. However, that ratio would be 8.6% if unrealized losses on held for sale investments is excluded. That is a normal level. Key has been a solid performer with an above average ROE and steady growth. The analysts expect earnings to decline this year by 20% for a variety of reasons such as; higher wages, lower capital markets income, less overdraft fees and higher loan loss provisions. Key struggled in the 2007-2009 recession.

Zions ( ZION )

This Utah based regional is a traditional regional bank which like Key has significant wealth management and also some capital markets activity. The loan portfolio is traditional and not riskier than peer. It used to have a large oil & gas exposure but that is more normal now. There are several issues though. The first is a tangible net worth of only 4.7%, which is very low. However, this number is after $2.9 billion of deductions for unrealized losses. Otherwise, it would be around 8%. Zion moved half of its investments in held for maturity in the fourth quarter of 2022, and that impacted net worth at that time. Zion did poorly in the 2007-2009 recession. It also has a high level of uninsured deposits.

Republic First ( FRBK )

This Philadelphia based bank has been one of the poorest performing banks in the U.S. for quite some time. Tangible net worth has now dropped to only 3.2% of total assets, an inadequate and alarming level. It is not involved in much higher risk activities at this point other than a higher level of construction and land development loans. Their interest margin was heavily squeezed in the most recent quarter indicating more problems ahead. This is the riskiest bank on this list. Republic First was a bigger FDIC takeover candidate than First Republic.

First Internet ( INBK )

First Internet is a non-traditional bank based in Indiana. It operates mostly online and only has one office for deposits plus a loan production office. It has other non-traditional activities such as a large franchise finance operation and a very large single tenant commercial real estate loan operation. Single tenant loans tend to be to stronger tenants but could be to anyone. It has a solid track record in recent years but a relatively low net worth ratio versus the peer. Loan growth has been moderate. The bank lost money last quarter due to an elevated loan loss provision and a squeezed net interest margin. First Internet did poorly in the 2007-2009 recession.

PacWest ( PACW )

PacWest has had the most attention since the FDIC takeover of First Republic. It's stock already down considerably, was cut in half on May 4th, after rumors it was trying to sell itself. It gained almost all that back the next day when they announced they have not put the bank up for sale but have received offers for specific assets and the bank. They also announced that deposits have been stable since quarter end. PacWest has two fundamental issues. The first is a low tangible net worth ratio. The second is a lot of loan and deposit activity with venture capital. This is the same industry that fled Silicon Valley Bank causing its collapse, though PacWest's exposure is much less. Unlike Silicon Valley Bank, PacWest has an industry normal level of uninsured deposits. It has been quite profitable but above average loan growth is a concern. PacWest did poorly in the 2007-2009 recession.

Western Alliance ( WAL )

Western Alliance has been one of the fastest growing most profitable banks out there over the past three years. It is generally not involved in unusual activities, other than a relatively small amount of equity investments. The capital ratio is moderately low. The culprit here appears to be the growth. The bank did poorly in the 2007-2009 recession after growing rapidly into that. The market apparently fears a repeat. The loan portfolio has grown so rapidly that it is not seasoned like most other banks.

Territorial ( TBNK )

At first blush everything looks fine with this Hawaii based bank. There is plenty of capital, uninsured deposits are normal, and it is as plain vanilla as it gets. But underneath lies a problem. Almost every loan is a single family mortgage. These are usually long term fixed rate loans. They had an average yield of 3.47% on December 31, 2022, well below what it costs to borrow these days. If Territorial had to sell these loans, they would take a huge loss. On top of that there is a large underwater investment security portfolio. Sounds bad huh? This is actually the old savings and loan business model most remaining S&Ls have moved away from. Back in 1981, almost every S&L was insolvent if you measured the fair market value of their assets, but most ended up surviving. Meanwhile, their margins are getting squeezed hard and they will likely start losing money soon if interest rates don't come down. Territorial sailed right through the 2007-2009 recession.

A Window of Opportunity

As noted earlier, most banks that fail historically did so due to a high level of bad loans. Bad loans not only create losses, they also pile up costs such as legal, real estate holding costs, loss of interest income and more staffing. Very few if any banks right now have a high level of bad loans. In fact, I believe that 2022 witnessed the lowest level of bad loans in banking history. The level of bad loans industrywide is increasing but only to a more normal historical level. Recessions, if more than mild or short, almost always result in a much higher level of bad loans. The thing is, it takes 9-15 months after the start of a recession for it to become evident which banks are going to get hit. That is because most larger borrowers (corporate or individuals) have reserves they can tap before being unable to pay. It also takes a while to foreclose on collateral, especially real estate. Banks usually start increasing their loss reserves before that, so earnings may still be significantly impacted this year.

I do expect a decline in bank industry earnings this year. In addition to higher loss reserves, many banks are getting squeezed by interest rates (though some actually benefit). Bank profits were juiced the last 2 years by all the stimulus pumped into the economy. Just a return to normal will reduce earnings. Loan growth is likely to stall or decline in a recession as underwriting standards get tightened. Regulatory activity may get tighter. Even if a recession doesn't happen, bank earnings are likely to decline for most of the reasons noted above.

There is likely to be a window between the current liquidity induced bank panic and when the bank industry starts to see declining earnings and a big increase in problem loans. If you expect the current bank panic to die down, it is a window of opportunity to invest in beaten up bank stocks.

Risks to Look For in a Bank

If you are looking to invest in bank stocks here are some risks to look at, that are particularly important in a recession.

1. Level of risky assets - The riskiest primary loan types for banks in a recession are usually unsecured consumer loans including credit cards and construction and development loans. In this case I would add office and retail real estate, especially office. Look for concentrations in these areas.

2. Track record - Many of the largest banks were hit hard in the 2007-2009 recession, especially Citicorp, Bank of America, and Ally. Regional and community banks on average fared a little better but 465 did go under from 2008-2012. I provided a list of how 102 community banks did in the 2007-2009 recession in this article.

3. Concentrations by industry - Banks that have a large amount of loans to a riskier industry such as oil and gas, venture capital (SIVB is an example there), and newer technology companies should be avoided. In real estate I recommend avoiding those with high concentrations to office and retail buildings which both face large secular headwinds.

4. Current level of delinquencies - We have had a strong economic expansion for years, and most banks have few bad loans. Those that currently have a higher than average level indicate they are likely to be harder hit due to looser underwriting standards or riskier loan types.

5. Rapid Growth - This is a big one. Historically those banks growing the fastest are most at risk in a recession. They tend to take more risk or underprice to take loans away from competitors. Also, their loan portfolio has less seasoning to it. Loans do better as they age. The three banks that were taken over (SIVB, SBNY FRC) and Silvergate were all growing well in excess of the industry norm.

6. Capital level - Most banks have a significantly higher level of capital to assets than they did going into the 2007-2009 recession. This gives them a bigger cushion to absorb losses. An average level for banks is currently around 9% capital to assets. Be careful with those significantly below that. Deduct intangible assets when looking at capital.

7. High Interest Rates on Assets - As of December 31, 2022, the average yield on banks earning assets was 4.54%. These assets include lower yielding investment securities. If the bank you are looking at had an average asset yield of over 5.50% at that time, they are probably making riskier loans. A higher rate is needed to compensate for higher risk.

8. Search FDIC Enforcement Actions - You can actually see what the FDIC and other regulatory agencies are doing at their websites. The FDIC's is here. If you type the bank's name into the search bar past FDIC activity comes up.

If You Invest

A few caveats if you decide to invest now. Avoid the stubs of those recently taken over. They have little to no assets remaining. If there are shareholder lawsuits against the FDIC, officers or D&O insurance, you won't benefit if you purchased the stock after the takeover.

I recommend keeping any investments with these higher risk banks relatively short as I expect bank earnings to decline this year and probably more next year for reasons given earlier. This may be somewhat offset by less unrealized losses once the Fed starts lowering rates.

Investing in the most beaten down bank stocks means taking higher than normal risk. Higher risk for me means a smaller position.

You are betting on things settling down. FDIC needs to stop taking over solvent banks as it has created a lot of the panic. Most survivors have increased liquidity or access to liquidity so that should help. Also, you would think they have learned their lesson at this point.

Takeaway

I have taken 2 positions in the last 2 trading days, both at the bottom end of my usual position size. I bought PacWest as it was the most beaten down, and I did not believe it was in immediate danger of an FDIC takeover on Friday morning (May 5) before the market opened based on this 8-K filing. It indicated that deposits were stable and that some parties have contacted them about investment and that efforts to maximize shareholder value continue along normal lines. Liquidity is well in excess of uninsured deposits, which are down to 25% of total deposits. Since liquidity appears fine and deposits are stable, the risk of an FDIC takeover is significantly reduced. I bought as soon as I saw the statement before the market opened.

I also purchased the SPDR S&P Regional Bank ETF ( KRE ) to have a more diversified exposure.

I may also buy KeyCorp. They have none of the issues that the banks taken over did and are very diversified.

These are all short term positions for me.

Most of the others are worthy of a look if your investment is short term. Avoid Republic First as it is most in danger of being taken over on the list.

I am not necessarily making recommendations as this is not a detailed review just a starter for your own due diligence. What I cannot analyze is sentiment and FDIC actions that are driving that sentiment. That's why my positions are relatively small.

For further details see:

Want To Buy A Beaten Down Bank Stock? Here's A List And Analysis