EYE - Warby Parker: Growth Should Accelerate As Trends Seem To Have Turned Positive

2023-09-25 10:30:08 ET

Summary

- Positive trend reversal and confident management outlook support a buy rating for Warby Parker.

- Warby Parker's growth prospects are expected to improve with the expansion of stores and increased insurance coverage.

- Slow growth in active customer counts in 1H23 is a potential risk that needs to be monitored.

Summary

I am recommending a buy rating for Warby Parker ( WRBY ), as I believe the trends have turned positive since the low of 1H23, especially with management sounding confident in the recent conference (held in September). Growth should gradually accelerate from here, and the stock should continue to trade at a premium to peers given its higher growth rate.

Business

WRBY is a lifestyle brand that designs products and develops technologies that help people see, from prescription glasses and contacts to eye exams and vision tests, through Warby Parker retail stores and its e-commerce platform. Warby Parker serves customers in the United States and Canada. WRBY competes in the eyewear space, which is experiencing a secular uptrend due to the increasing penetration of myopia , which I expect to worsen over time as more people rely on digital tools (computers, smartphones, laptops, etc.) to facilitate their lifestyle.

Financials / Valuation

WRBY has certainly benefited from the secular uptrends since its net sales performance, which more than doubled from $272 million in 18 to near $600 million in FY22. However, the business is still in the growth stage; hence, it is not generating any meaningful profits at the moment. Since 2018, the business has reported worsened GAAP EBIT from -$24 million in FY18 to -$111 million in FY22. However, based on the WRBY definition of adj EBITDA (which includes stock-based compensation), the company has reported improving adj EBITDA from FY18 of $8.6 million to FY22 of $27.2 million. As for the most recent quarter (2Q23), WRBY reported 2Q23 adjusted EBITDA of $14.2 million, ahead of consensus at $12.2 million. Net sales of $166 million grew 11%, above the consensus of 8.6%. GAAP gross margin of 54.6% contracted to 314 bps, but adj EBITDA margin improved by 450 bps to 8.5%.

Based on author's own math

Based on my view of the business, WRBY should see growth recover from the lows of 2023 (growing 12% in FY24 and 14% in FY25), as the trend seems to have recovered and management is confident that they can continue opening new stores at the same rate as in FY22 (~40 a year). While active customer counts have slowed in the recent quarter, I believe they might be due to stores not being mature yet (i.e., new stores take some time for customer traffic to flow in). The maturity of these stores, along with the new upcoming 40 stores, should improve overall active customer counts, thereby improving sales. When compared to the next best competitor (National Vision Holdings ( EYE )), I believe WRBY deserves a premium given its growth profile (EYE is expected to see weak growth in the near term based on my view ). EYE is trading at 1x forward revenue today and WRBY is trading at ~2x, and I expect WRBY to continue trading at this valuation. With my assumptions, my price target of $14.10.

Below are my thoughts and forward outlook on EYE. I recommend readers to refer to the post for more details as this post is to cover WRBY and not EYE.

"B ased on my view on the business, EYE will experience a 3% decline in growth in FY24. This projection is primarily attributed to the subdued revenue growth observed in 2Q and the company's decision to terminate its long-standing partnership with WMT. The growth rate aligns with market consensus.

My model uses a margin of 56% for FY24. This estimate is underpinned by a positive outlook, as there is optimism surrounding the gradual improvement of optometrist capacity. This improvement is expected to materialize through ongoing recruitment and retention initiatives, as well as the implementation of EYE's remote medicine program. It's worth noting that while the company is currently facing some pressure in this quarter, it is anticipated that these challenges will ease in the near future, therefore driving margins to expand." Normad Capital

Comments

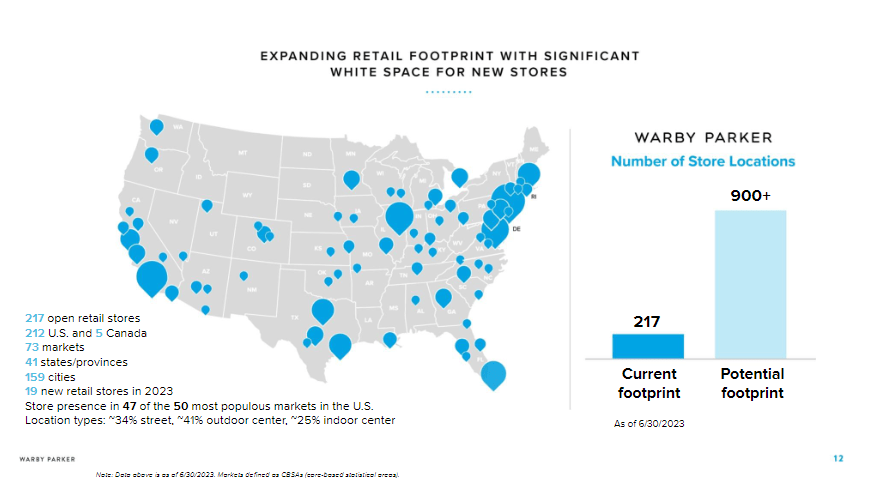

WRBY reported strong adjusted EBITDA growth in 2Q23 and increased its full-year outlook. The quarter ended with me feeling somewhat more optimistic about WRBY's underlying business trends, as evidenced by the y/y number of stores opened and my optimistic commentary on 3Q23. Most notably, consumer traffic trends are normalizing, which is particularly encouraging given the strong early back-to-school exam bookings and other indicators that a turnaround trend may be ongoing. I believe the trend has continued to 3Q23 as management struck the same tone during the 30th Annual Global Retailing Conference by GS. The same positive tone was struck in terms of forward-looking comments. I believe this indicates that 3Q23 is likely going to see the same momentum throughout (given that half of the quarter is positive, it is likely that the remaining half is positive). Specifically, management has been very upbeat about the future of the visioncare market as a whole, despite the fact that demand was restrained in 2022 and the first half of 2023. Management has pointed out that WRBY has a history of gaining market share regardless of the overall economic climate and that this trend should continue into next year thanks to cyclical tailwinds from both smaller and larger competitors in the industry.

The optimistic tone was further supplemented by the store opening guidance. Managers have assured employees that 40 annual store expansions with optometry services are still in the works. Keep in mind that this is in keeping with FY22 opening levels, which were already an improvement over the 30+ stores opened in the previous fiscal year. Since eye exams are known to attract customers, it stands to reason that stores equipped to perform them will have better unit economics. According to management during the conference, an eye exam results in consumers spending 2.2x more than those who just purchase glasses. Importantly, they emphasized that this penetration of comprehensive vision care is still in its infancy; hence, I believe there is plenty of room for expansion. The pushback from this strategy is that there is an ongoing optometrist shortage in the US, which means costs are going to go up because of wages. However, management has stressed that the store's experience, tools, and emphasis on assisting with administrative tasks are what have helped the company keep and expand its optometrist workforce.

{kind=link}

WRBY

I also believe that WRBY's investments in its insurance coverage will serve as a growth driver that will help the company attract new customers. By increasing its in-network coverage to over 18 million lives, WRBY has taken a positive step toward easing the pain points that many customers experience when making purchases with the company (lower out-of-pocket payment). WRBY has also recently introduced online universal eligibility checks as part of their consumer-facing technology investment to further reduce purchase friction. To further improve the insurance process for customers, management plans to continue testing and implementing new tools in the near future.

"as we look at vision insurance in America, the average out-of-pocket spend is over $250. So, as we're thinking about our pricing and the value that we're providing, we're looking not only at what sort of our competitors are charging and making sure that we're a fraction of that, we're also looking at what customers are spending that happen to have insurance and go in-network as well to make sure that we're competitive with what they're paying out-of-pocket as well. " Source: GS Retailing conference

While WRBY has a short history as a listed company, I believe management words have high creditability when we look its historical guidance vs actual results. For FY21/22 management guided for $539.5 million to $542 million and $595 million to $596 million, respectively, and actual results were both ahead at the mid-point. Notably, FY22 guidance was revised upwards in 3Q23. The same could be said for management EBITDA guidance in FY22 as well, where the actual results come in $1.2 million above the mid-point of $26 million.

Risk & Conclusion

Despite these positive developments, WRBY's active customer count has grown slowly (from the high single digits to the low single digits in 1H23), despite its expanding store count and geographic reach. This might indicate that the new stores are doing as well as I had hoped. We need to keep an eye on this going forward. The complexity of the vision care market, with its many rules and regulations meant to protect consumers and their health information, is another risk to expansion. As a result, expanding stores and managing patient records can become more complicated in order to pass muster with regulators on both the state and federal levels.

Overall, I recommend a buy rating for WRBY due to the positive trend reversal witnessed since 1H23 and the company's confidence in its growth prospects, as demonstrated in the recent conference. The expansion of stores with optometry services and increased insurance coverage are strategic moves that should attract more customers and enhance profitability. Management's upbeat outlook and commitment to market share growth reinforce my positive stance. However, the slow growth in active customer counts in 1H23 is a potential risk, necessitating continued monitoring.

For further details see:

Warby Parker: Growth Should Accelerate As Trends Seem To Have Turned Positive