WRBY - Warby Parker Q3: Thriving In A Niche Market With A Compact Brand

2023-11-14 10:57:00 ET

Summary

- Warby Parker's stock price has declined by 30% and 8% since reporting its Q3 earnings results.

- The company has shown improvements in profit margins and average customer spending, indicating a resilient brand.

- Warby Parker's potential for growth is limited to less than 20% annually due to its reliance on physical retail store expansion.

Warby Parker's Q3 Earnings Report and Stock Decline

On November 8, 2023, Warby Parker (WRBY) reported its financial results for the third quarter of 2023. Since reporting these third-quarter results, Warby Parker's stock price has decreased by 30% and 8% after our previous coverage of Warby Parker in April 2023.

Investment Thesis

We believe that Warby Parker is a company worth continuing to monitor because it has identified a specific market niche that allows it to compete with larger players in the industry and establish its own distinctive brand. The fact that Warby Parker has shown improvements in profit margins and the average amount spent by each of its customers is evidence that its brand has strength and resonance with consumers.

However, we anticipate that Warby Parker's potential for growth is restricted to an annual rate of less than 20% because its strategy for growth depends heavily on expanding its physical retail store footprint.

Given both the strengths of its competitive positioning and branding, along with the limited upside for rapid growth, we are maintaining our neutral rating on Warby Parker at this time. We believe the strengths and limitations of the company balance each other out, justifying our neutral perspective.

Financial Review

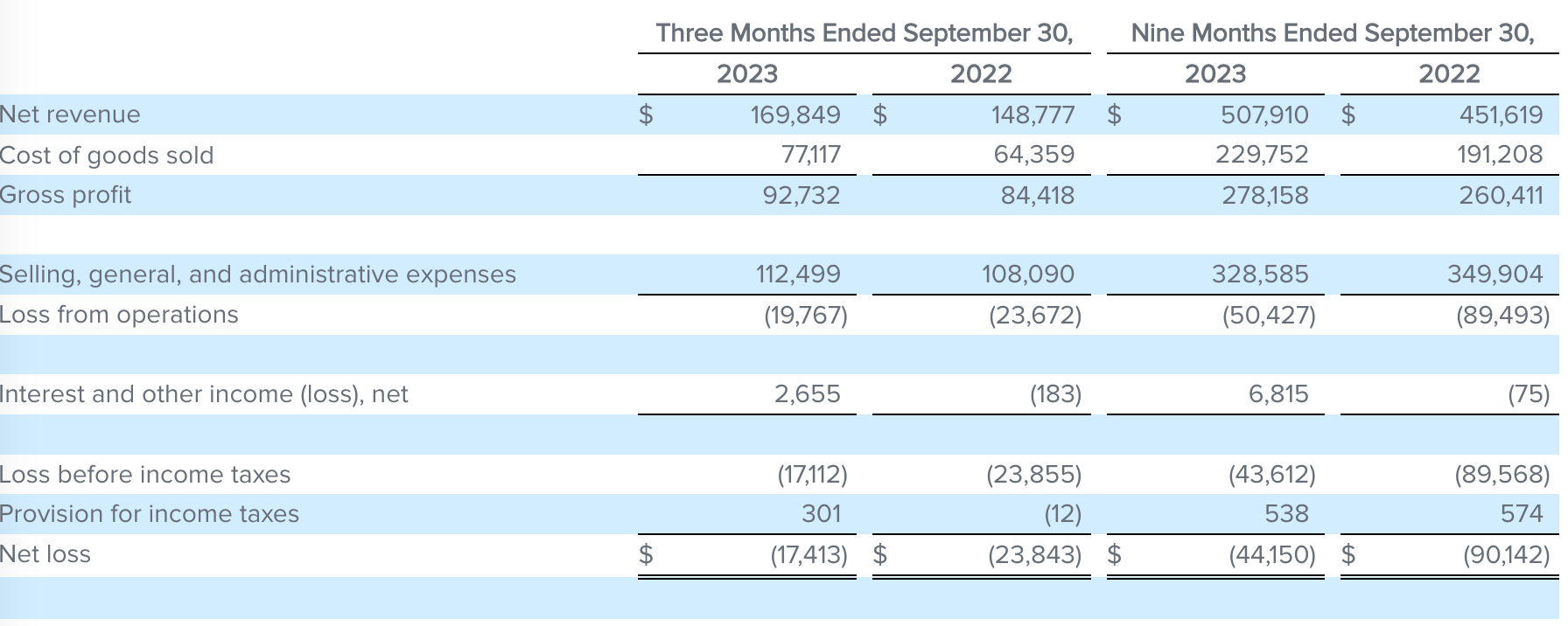

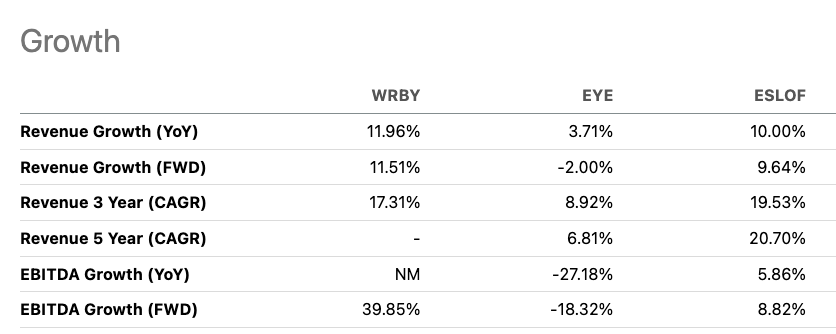

In its third quarter ( Q3 ) earnings report, Warby Parker announced that its revenue grew by 14% compared to the same quarter last year. This 14% growth rate is an acceleration from the 11% year-over-year revenue growth the company saw in the second quarter (Q2). Based on the Q3 results, Warby Parker raised its full-year revenue guidance to predict 11.5% revenue growth for the full year, which is higher than its previous estimate of 9.5%-11% growth. However, the increased full-year guidance suggests Warby Parker's revenue growth will slow to 9.5% in the fourth quarter (Q4) of the year.

{kind=link}

Warby Parker was able to narrow its losses in Q3 as the company further leveraged occupancy expenses through higher revenue numbers and increases in average revenue per customer. The company's SG&A as a percentage of revenue decreased to 66% in Q3, down from 73% in the prior year's Q3. Additionally, average revenue per customer increased by 10% to $284 and Warby Parker's total customer count increased by 1.8% to 2.3 million customers. These metrics indicate Warby Parker is seeing improved customer engagement despite facing inflationary headwinds.

Compared to the same time last year, Warby Parker has reduced its total inventory levels by 10%. The company currently has a cash balance of $215 million. Over the last nine months, Warby Parker generated $7 million in free cash flow. Despite the fact that the company is still operating at a net loss, these metrics around inventory, cash balances, and free cash flow suggest that Warby Parker has been able to maintain a healthy balance sheet and halt its cash burn rate. The steps taken to cut inventory and generate free cash flow indicate that Warby Parker has made progress in operating efficiently and conservatively to stop bleeding cash, even as it continues to operate at a loss on the bottom line.

Competition Risk

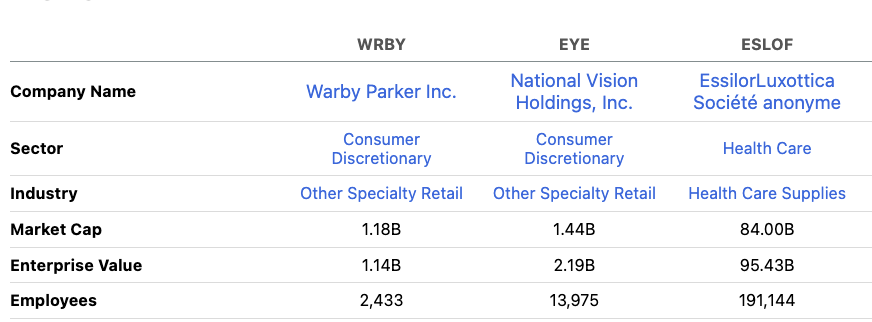

There are 3 major public companies that operate in the eyeglasses industry that we have identified. National Vision ( EYE ) and EssilorLuxottica ( ESLOF ) both operate using a traditional retailer business model.

{kind=link}

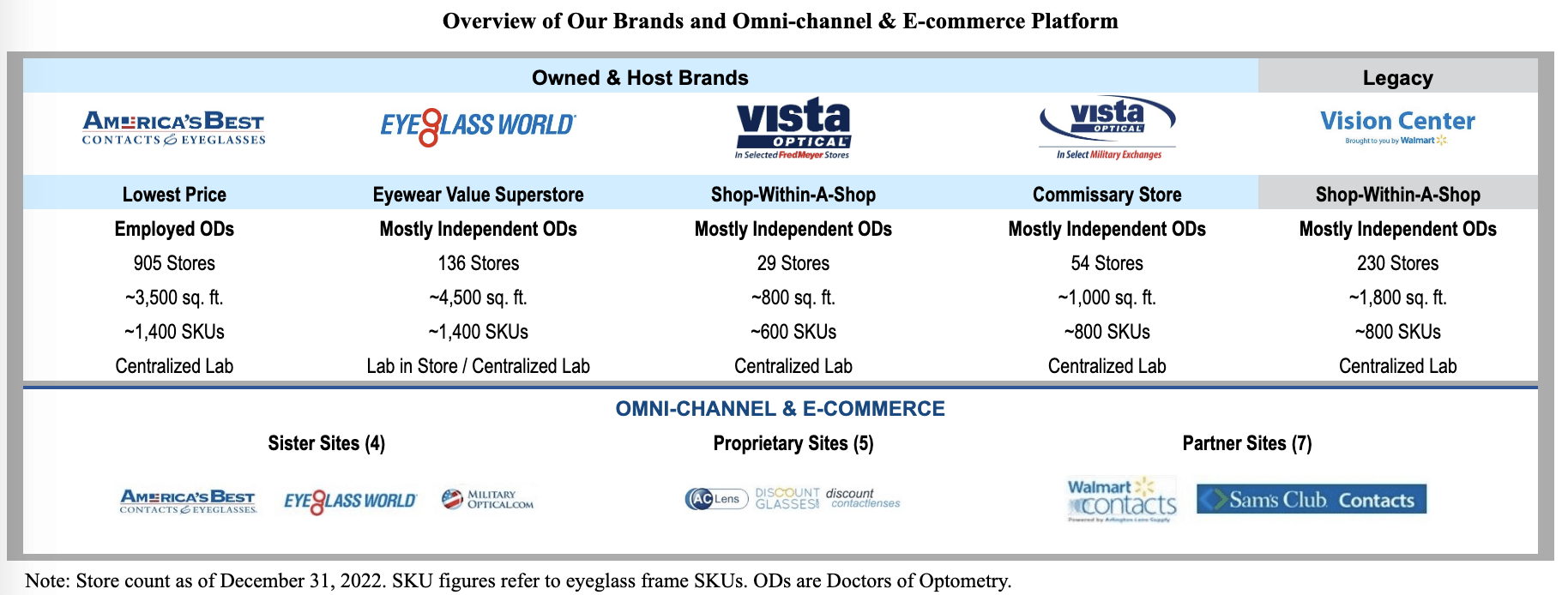

To give an example, National Vision owns and operates its own stores for selling eyeglasses, contact lenses, and eye exams directly to customers. Additionally, National Vision partners with independent optometrists and other distributors such as Walmart ( WMT ) to sell its products and services. Through these company-owned locations, partnerships with optometrists, and distribution of products in other major retail stores, National Vision covers multiple channels within the traditional eyeglasses retail industry.

{kind=link}

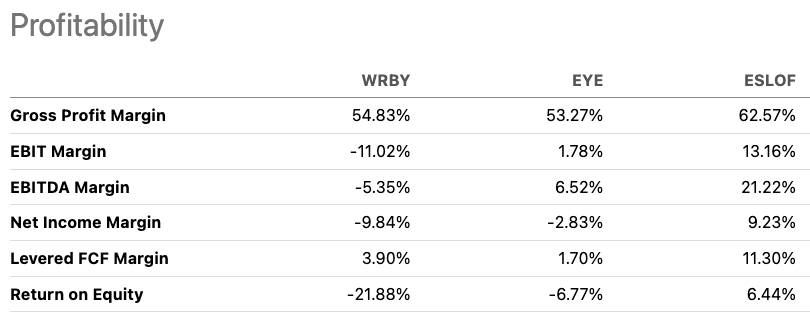

National Vision has an extensive physical retail store presence. Due to state laws that require eyeglass prescriptions to expire after a certain period of time, eye exam services play a crucial role in the traditional retail model. The eye exam helps retain customers within the retailer's network of stores since customers need to get updated prescriptions. This retail network acts as a moat for traditional companies on a regional basis. The eye exam service allows traditional retailers to charge premium prices on eyeglasses. For example, in 2022 National Vision had a much higher gross margin on its eyewear products compared to its eye exam services.

Companies report

The old-school retail approach that companies like National Vision use is solid. They partner with luxury brands to sell high-end glasses but just compete on price for cheaper frames. That left an opening for an upstart like Warby Parker to shake things up through cool, affordable designs.

By focusing on product design, Warby Parker built up a loyal customer base who loved the style and price. Once the company had penetrated the budget-conscious young consumers, it leveraged its reputation for quality and innovation to start offering higher-end options too. The fact that Warby Parker makes a higher gross margin than National Vision shows this strategy is working.

Rather than just fighting over bargain basement prices, Warby Parker found a niche selling great specs at reasonable prices. That allowed them to grow a loyal following incrementally, and expand into pricier products as they went. National Vision's lack of imagination and reliance on partnerships and discounts left them vulnerable to a challenger with creative flair. Warby Parker's success proves the power of innovation and branding, even in a traditionally commodity-driven business.

However, there are two key challenges with Warby Parker's strategy. First, the transaction cycle is long in the eyewear market, so it takes significant time for a new brand to stand out and be recognized. Warby Parker's current consumer base is still small and not yet large enough to support building out an extensive national physical store network. As a result, Warby Parker still operates with higher costs overall. In addition, Warby Parker's e-commerce channel growth seems to be plateauing, as its percentage of revenue from online sales is decreasing and e-commerce sales are stagnating. Without a strong e-commerce channel to accelerate growing its customer base, Warby Parker may see slow progress in overall revenue growth and path to profitability.

{kind=link}

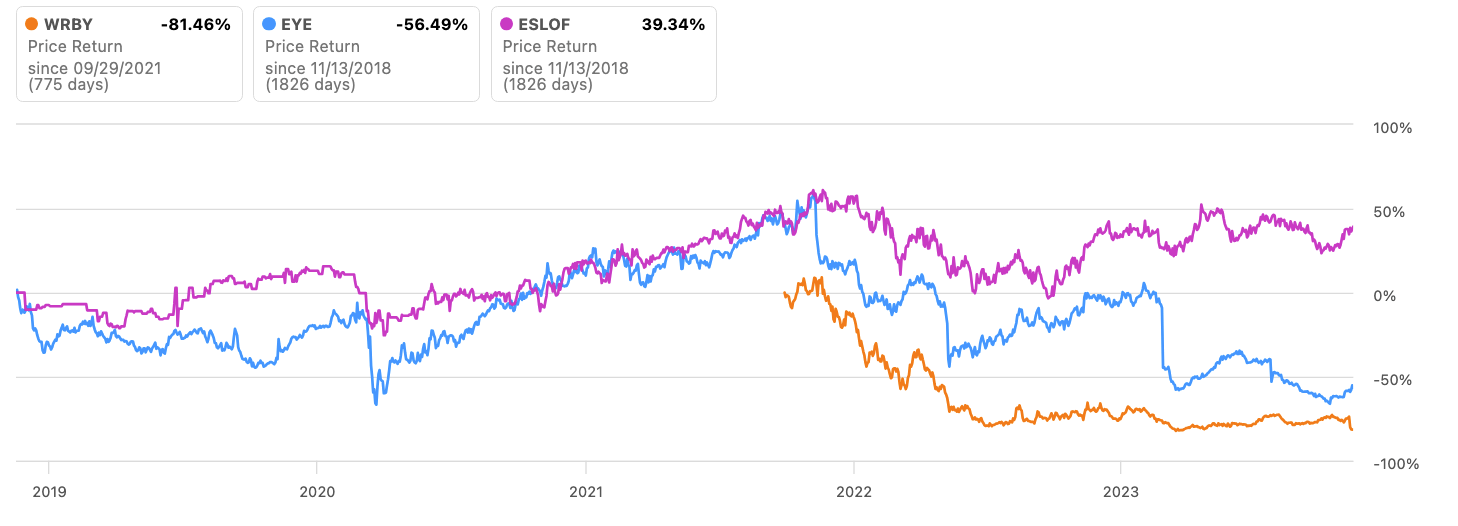

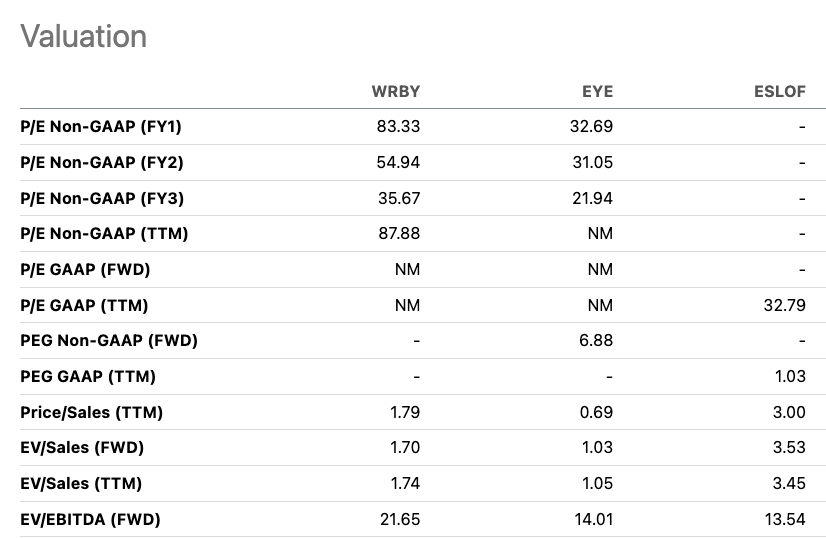

Stock Performance and Valuation

Among its 3 major public company peers, Warby Parker's stock performance is lagging. Its omni-channel strategy with both physical stores and e-commerce does not seem to be significantly helping Warby Parker accelerate its revenue growth. While Warby Parker's current gross margin is better than National Vision, it remains behind larger competitors like EssilorLuxottica, which has 80 times more employees than Warby Parker and thus a much more extensive retail network and scale.

{kind=link}

Looking at valuation, Warby Parker trades at a P/S ratio of 1.79x, which is lower than EssilorLuxottica but higher than National Vision.

{kind=link}

Warby Parker's growth trajectory and profitability levels rank in the middle compared to these peers. Therefore, we believe Warby Parker's current valuation properly matches its competitive profile. Unless Warby Parker can find new ways to meaningfully accelerate its revenue growth, we don't foresee any short-term catalysts that will drive the stock higher. The company's growth and profitability remain middling versus peers, warranting a neutral view.

{kind=link}

{kind=link}

Looking longer-term, even though Warby Parker currently has less than 1% market share, the competitive landscape in the eyeglasses industry is fierce. Independent optometrists are increasingly joining larger networks like National Vision. Meanwhile, EssilorLuxottica has been very active in acquiring eyewear brands to expand its market presence. Despite our view that Warby Parker has a niche value proposition, these competitive dynamics lead us to believe the company's revenue growth rate will likely remain below 20% annually. The moves by National Vision and EssilorLuxottica to consolidate market share along with independent optometrists will make it challenging for Warby Parker to significantly expand from its small current market position. Given the competitive industry conditions, we expect Warby Parker to maintain its niche positioning but foresee growth being limited to less than 20% per year.

Conclusion

In our view, Warby Parker has succeeded in establishing a strong brand and brand identity in the eyewear market. However, when looking at the company's growth strategy, it appears to rely heavily on expanding Warby Parker's physical retail store footprint. Given the dependence on opening new stores to drive growth, we believe Warby Parker's revenue growth rate will likely remain below 20% annually going forward. There is a lack of other significant growth drivers for Warby Parker in the near term. With store expansion being the primary way the company can grow, there are limitations to how fast growth can accelerate. As a result, we believe Warby Parker's current valuation fairly reflects its growth prospects and competitive positioning. Without a compelling case that growth is poised to inflect higher, the stock appears appropriately valued at current levels. We maintain our neutral rating on Warby Parker.

For further details see:

Warby Parker Q3: Thriving In A Niche Market With A Compact Brand