T - Warner Bros. Discovery Stock Is A Pass For Me For Now

2024-01-10 17:48:01 ET

Summary

- Warner Bros. Discovery, Inc. shares are cheap compared to similar firms, but there are risks involved.

- The company's recent financial data shows some improvements, but there are still concerns such as a drop in subscriber numbers and high debt.

- Despite the potential for upside, the current weaknesses and risks make Warner Bros. Discovery, Inc. stock a hold for now.

One of the things that investors really appreciate about entertainment conglomerate Warner Bros. Discovery, Inc. ( WBD ) is the fact that shares of the enterprise are quite cheap. This is true not only on an absolute basis, but also relative to similar firms. As a value investor myself, I find buying shares of cheap stocks to be highly rewarding when it is done right. But it also brings with it certain risks like buying shares of companies that deserve to trade at a discount. In the past, I have been rather neutral on Warner Bros. Discovery.

When the management team at AT&T ( T ) ended up splitting WarnerMedia from its operations and merging them into Discovery to create the Warner Bros. Discovery entity that we know today, I almost immediately sold off my shares of the new enterprise. Based on my own assessment at the time, Warner Bros. Discovery was not exactly a bad prospect. But it was far from being a great one. As I saw it, all of the true value was in AT&T. Since that time, I believe that my thesis on the matter has proven to be true.

In the last article that I wrote about Warner Bros. Discovery, which was published in October of 2022, I mentioned that there was a lot of uncertainty regarding the company's streaming operations at that time. Overall, the company was looking better than it was prior to that point. But I still said that the company was not good enough to warrant an investment.

Since then, shares have fallen a further 11.6% while the S&P 500 (SP500) has jumped 21.2%. And fundamentally speaking, at least in some respects, the picture continues to look better. But when you add in some of the negatives like its recent drop in subscriber numbers and the massive amount of debt the company has on hand, I do not yet believe that it is worthy of an optimistic assessment. Because of that, I am keeping the company rated a "hold" for now.

The picture is improving… and worsening

{kind=link}

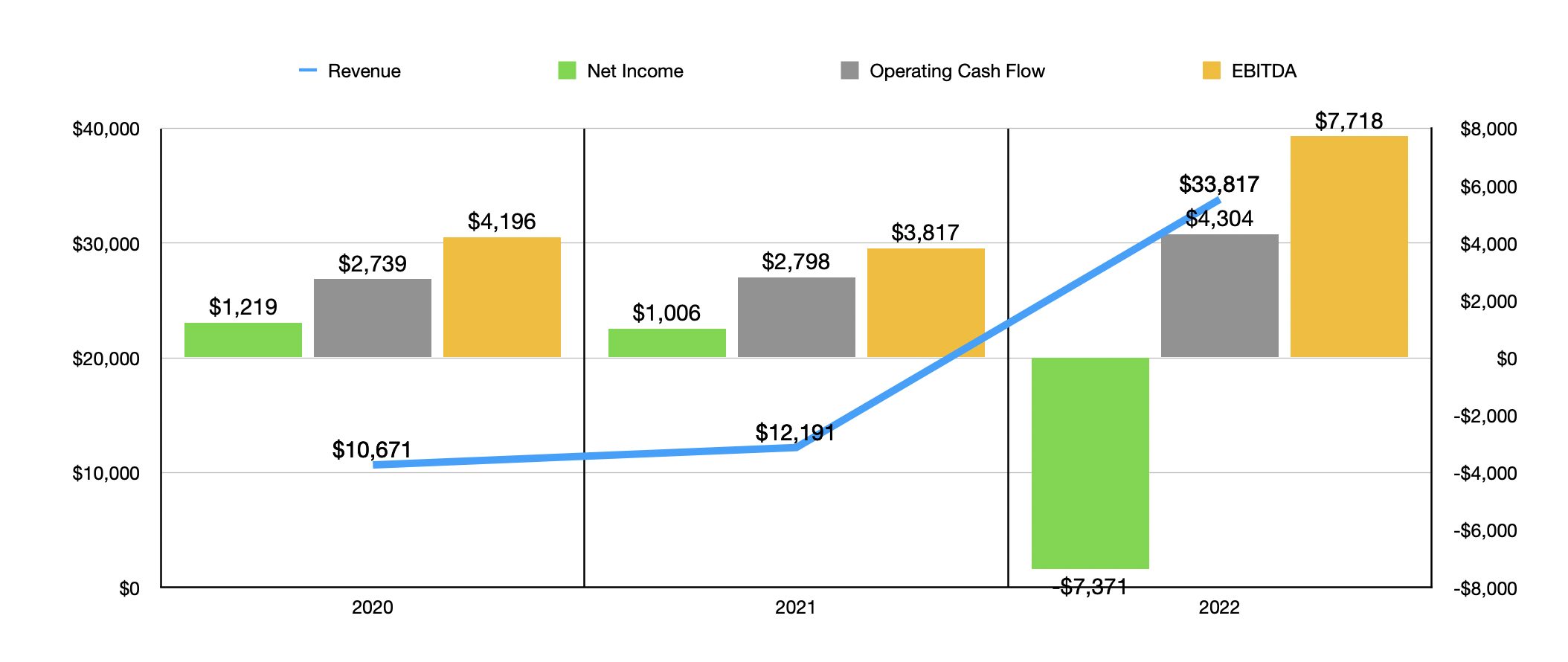

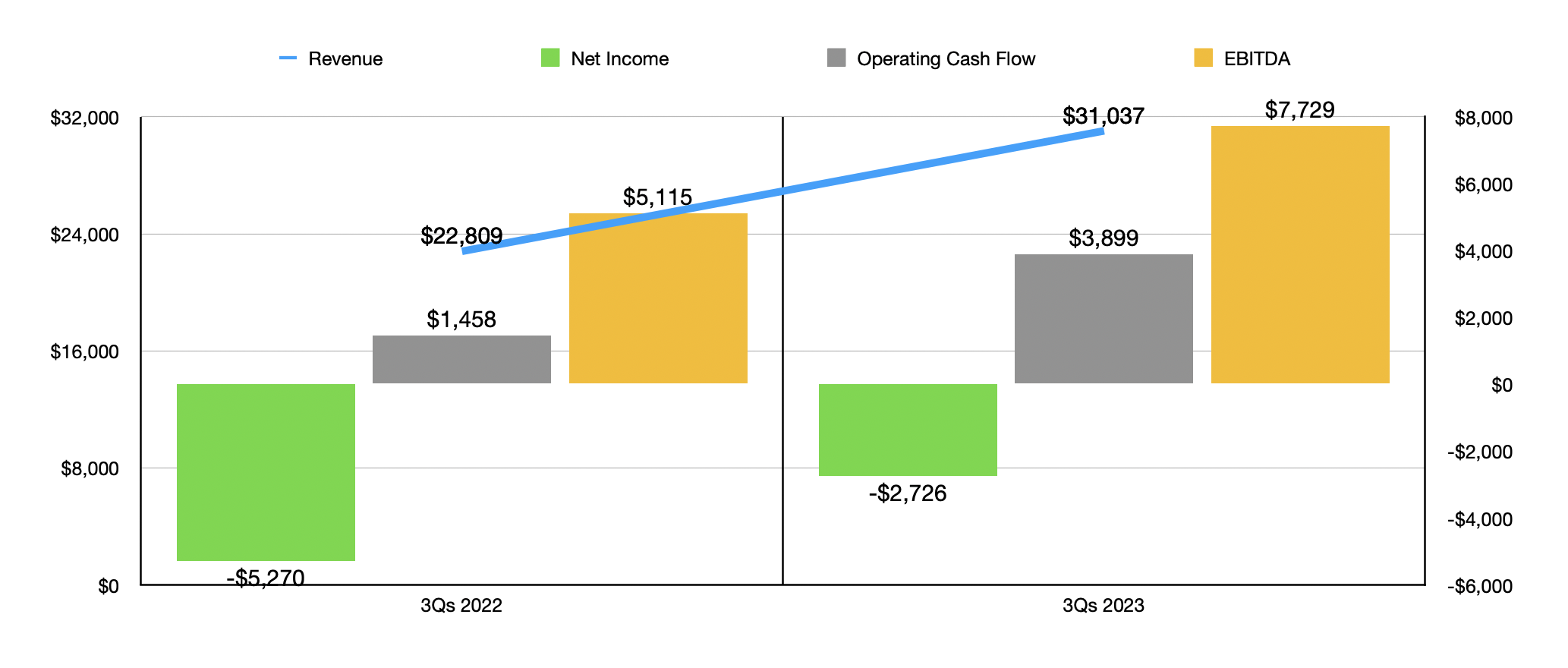

The most recent fundamental data that we have regarding Warner Bros. Discovery covers the third quarter of the company's 2023 fiscal year. If you look at the surface level data, the firm is, in many respects, performing quite well. In the chart above, for instance, you can see revenue, earnings, and cash flows, covering 2020 through 2022 . And in the chart below, you can see data covering the first nine months of 2023 relative to the first nine months of the year prior. The first thing you will notice is that sales skyrocketed from 2021 to 2022. However, it's important to dig a bit deeper in order to understand all that is going on.

{kind=link}

The good news for shareholders is that, to make things easier, the management team at the company provides data that shows what the fundamental picture would look like for the business had the merger between WarnerMedia and Discovery taken place at the beginning of the firm's fiscal year. This is necessary because the merger did not, in fact, occur in that manner.

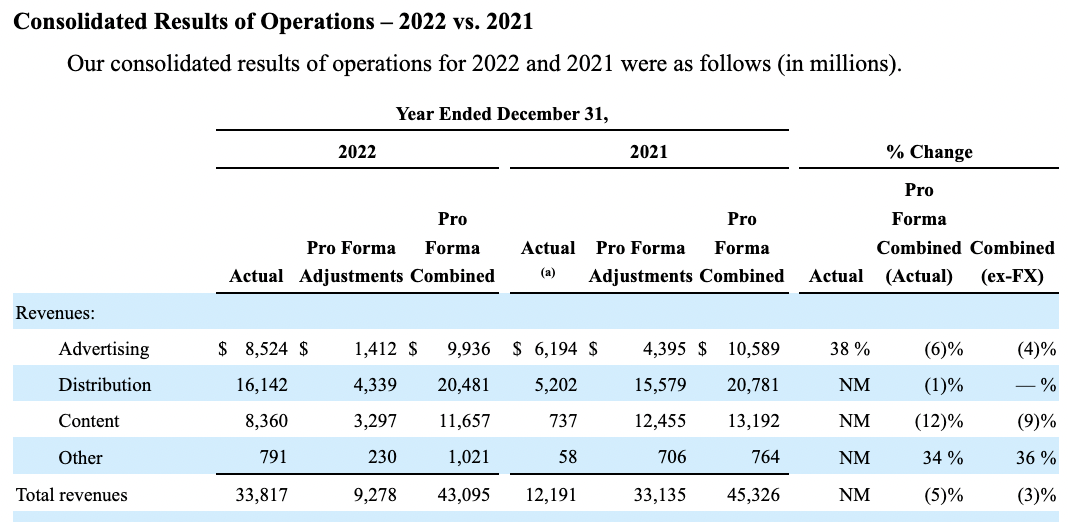

For the time prior to 2023, I won't cover all of the data since our primary focus should be on more recent results. But in the image below, you can see the revenue picture for the company as it was compared to what it would have been had the transaction been completed at the beginning of any given fiscal year. Instead of seeing revenue jump from $12.19 billion in 2021 to $33.82 billion in 2022, pro forma results would have shown a decline from $45.33 billion to $43.10 billion.

{kind=link}

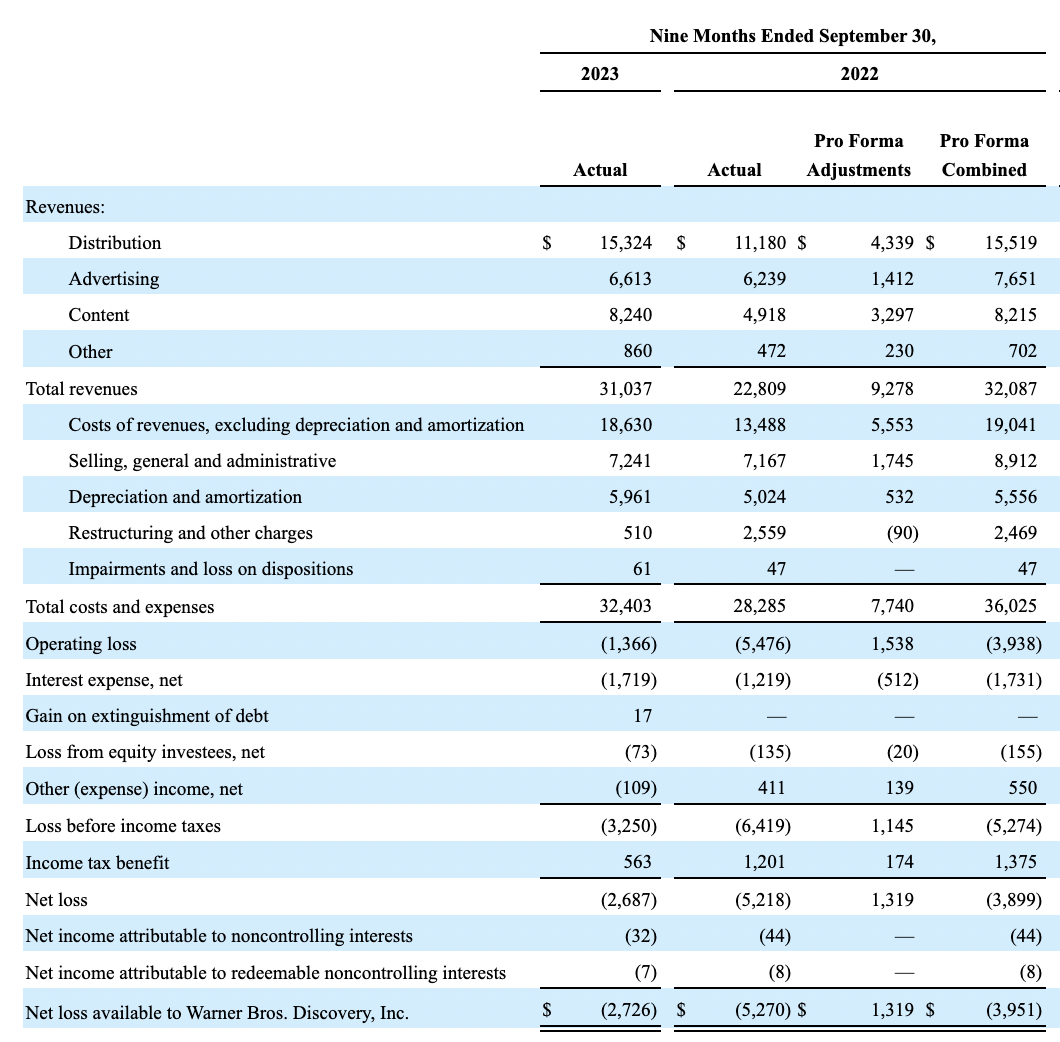

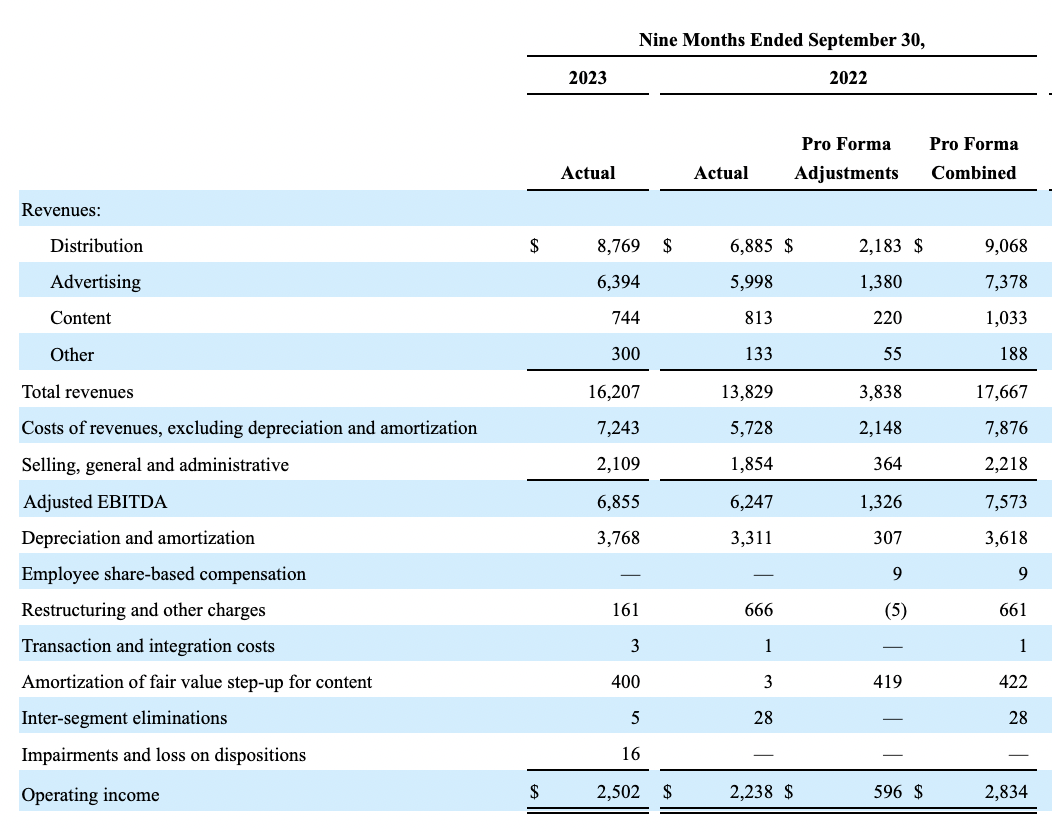

In the next image below, you can see comprehensive data covering the first nine months of 2023 relative to the first nine months of 2022. Instead of seeing revenue climb from $22.81 billion to $31.04 billion, an increase that would be impressive no matter what, we would actually see revenue drop slightly from $32.09 billion to $31.04 billion. On the bottom line, instead of seeing the firm's net loss improve from $5.27 billion to $2.73 billion, the improvement was less substantive from a loss of $3.95 billion to $2.73 billion. Admittedly, that's still an improvement, just not of the magnitude that the official GAAP results demonstrate.

{kind=link}

This does not change the fact that shares of Warner Bros. Discovery are fundamentally cheap. According to management, guidance for the 2023 fiscal year should result in EBITDA of between $10.5 billion and $11 billion. This compares to the $7.72 billion generated in 2022. This is a massive improvement and it is thanks to cost cutting initiatives that have allowed the company to capture synergies in excess of $5 billion. Though this has come at a cost that is estimated to be toward the higher end of the $1 billion to $1.5 billion range that management previously forecasted. Given the magnitude of the savings, this is a small price to pay that investors should be very happy with.

No estimates were provided when it comes to operating cash flow. But assuming it is expected to increase at the same rate that EBITDA at its midpoint should, investors should anticipate a reading of just under $6 billion.

{kind=link}

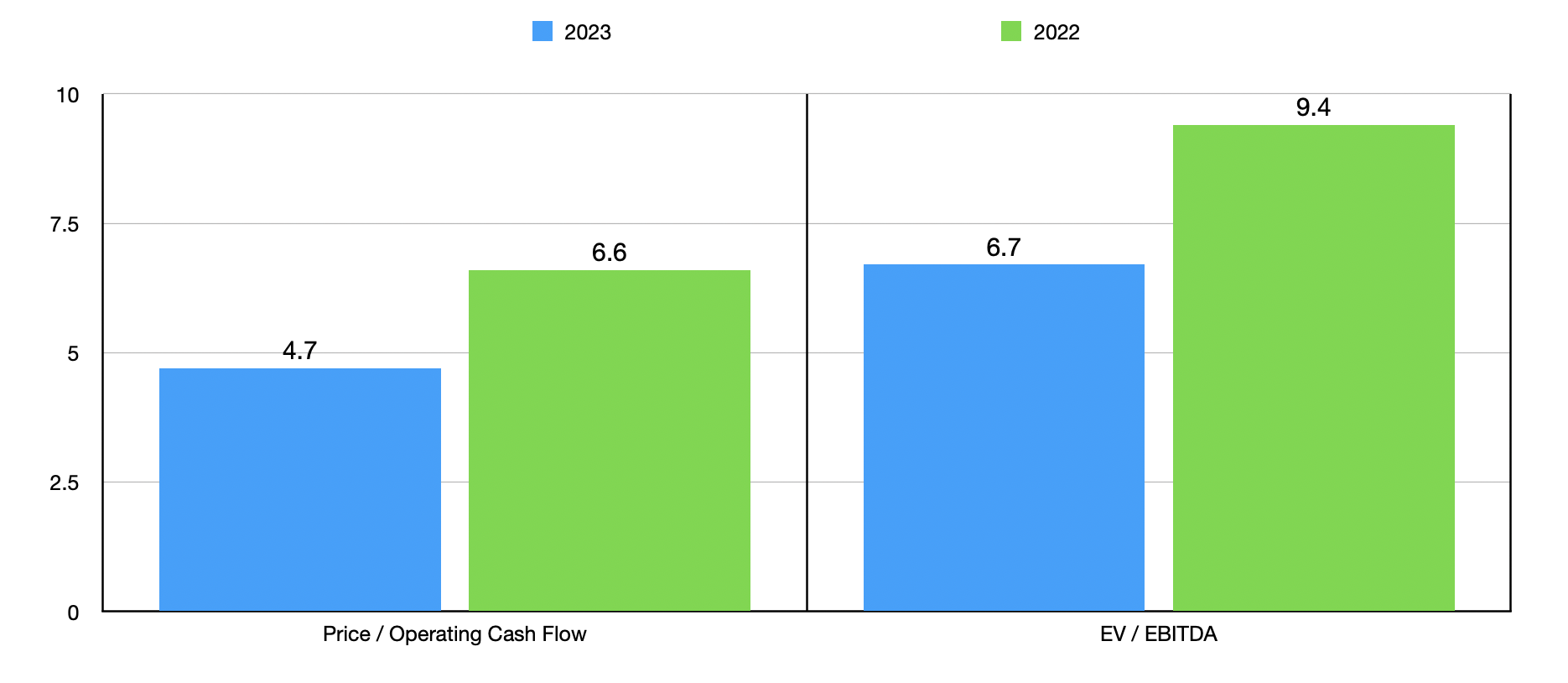

In the chart above, you can see what this does to the pricing of the stock for 2023 relative to 2022. The price to operating cash flow multiple should drop from 6.6 to 4.7. Meanwhile, the EV to EBITDA multiple of the company is expected to fall from 9.4 to 6.7. Often, when multiples are in the single digit range like this, it should be construed as a bullish sign.

But shares aren't just cheap on an absolute basis. In the table below, I compared the enterprise to two similar firms. It is quite a bit cheaper than either one. As a note, I was tempted to compare it to The Walt Disney Company ( DIS ) as well, given its massive streaming and theatrical production divisions. But given how many other operations exist under the Disney umbrella, I felt it wouldn't be comparable enough.

| Company |

| Price / Operating Cash Flow |

| EV / EBITDA |

| Warner Bros. Discovery |

| 4.7 |

| 6.7 |

| Netflix ( NFLX ) |

| 35.1 |

| 10.3 |

| Paramount Global ( PARA ) |

| 64.5 |

| 37.4 |

Based on the data seen so far, Warner Bros. Discovery looks to be an interesting turnaround prospect. However, there are parts of the company that I remain uncomfortable with. First and foremost, I don't like the massive amount of debt that the enterprise has on its books. Net debt as of the end of the most recent quarter was $42.42 billion. Granted, the recent surge in EBITDA should bring the net leverage ratio of the enterprise down to about 3.95. That's a nice improvement over the 5.50 reading that we get using EBITDA from 2022. That is likely to continue dropping from this point on so long as profitability remains elevated.

This alone would not be enough to cause me to take a bearish stance on the business, especially the big improvement that we have seen from 2022 to 2023. But it is a piece of the pie that investors need to take into consideration.

{kind=link}

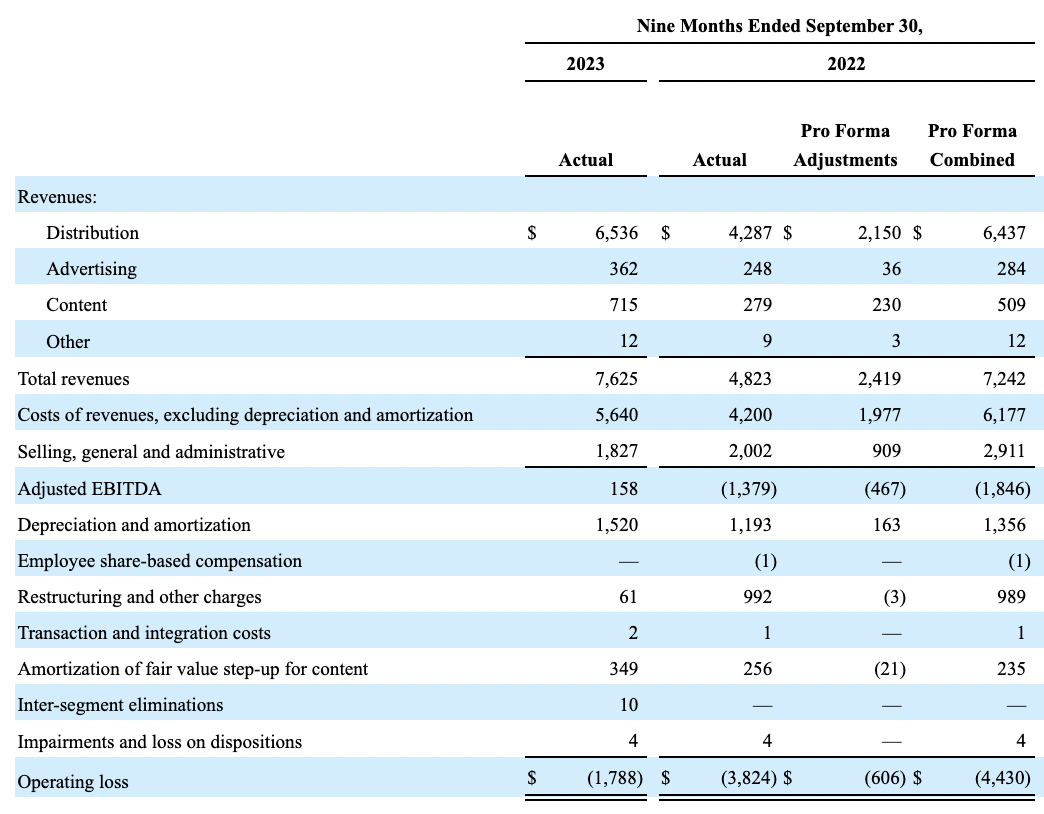

Another thing that bothers me is that a large portion of the company's revenue and profits comes from its Networks division. As of the end of the 2022 fiscal year, this included 30 U.S. general entertainment, lifestyle, and news networks, as well as international networks and regional sports networks, that the company made available to various domestic and international television networks. While revenue managed to grow from $13.83 billion in the first nine months of 2022 to $16.21 billion at the same time for 2023, actual pro forma revenue for the first nine months of 2022 was higher at $17.67 billion. Instead of seeing profits rise from $2.24 billion to $2.50 billion, profits would have actually fallen from $2.83 billion on a pro forma basis.

This weakness has come even at a time when management has been able to get higher contractual affiliate rates here at home. Advertising revenue has dropped by 13% year over year because of audience declines in both domestic general entertainment and news networks, as well as overall weakness that management claims exists in the U.S. market. Some international markets have also proven to be a pain when it comes to advertising, though not to the extent that the U.S. has.

Even worse was the content side of things, with revenue plunging 26% because of the timing of third-party content licensing deals here at home and a reduction in international sports sub licensing revenue. In general, this is an area that seems to be in trouble, largely thanks to a shift away from traditional networks and toward online content.

{kind=link}

Meanwhile, direct to consumer content that includes streaming operations has managed to grow, even on a pro forma basis. Sales on a pro forma basis have grown from $7.24 billion to $7.63 billion. On top of this, the bottom line for the enterprise is also improving nicely. In fact, management is forecasting EBITDA of $1 billion or more associated with these operations in 2025. For the first nine months of 2023, the improvements on the revenue side were largely driven by growth associated with the company’s U.S. ad-lite subscriber offering, higher engagement, and higher pricing.

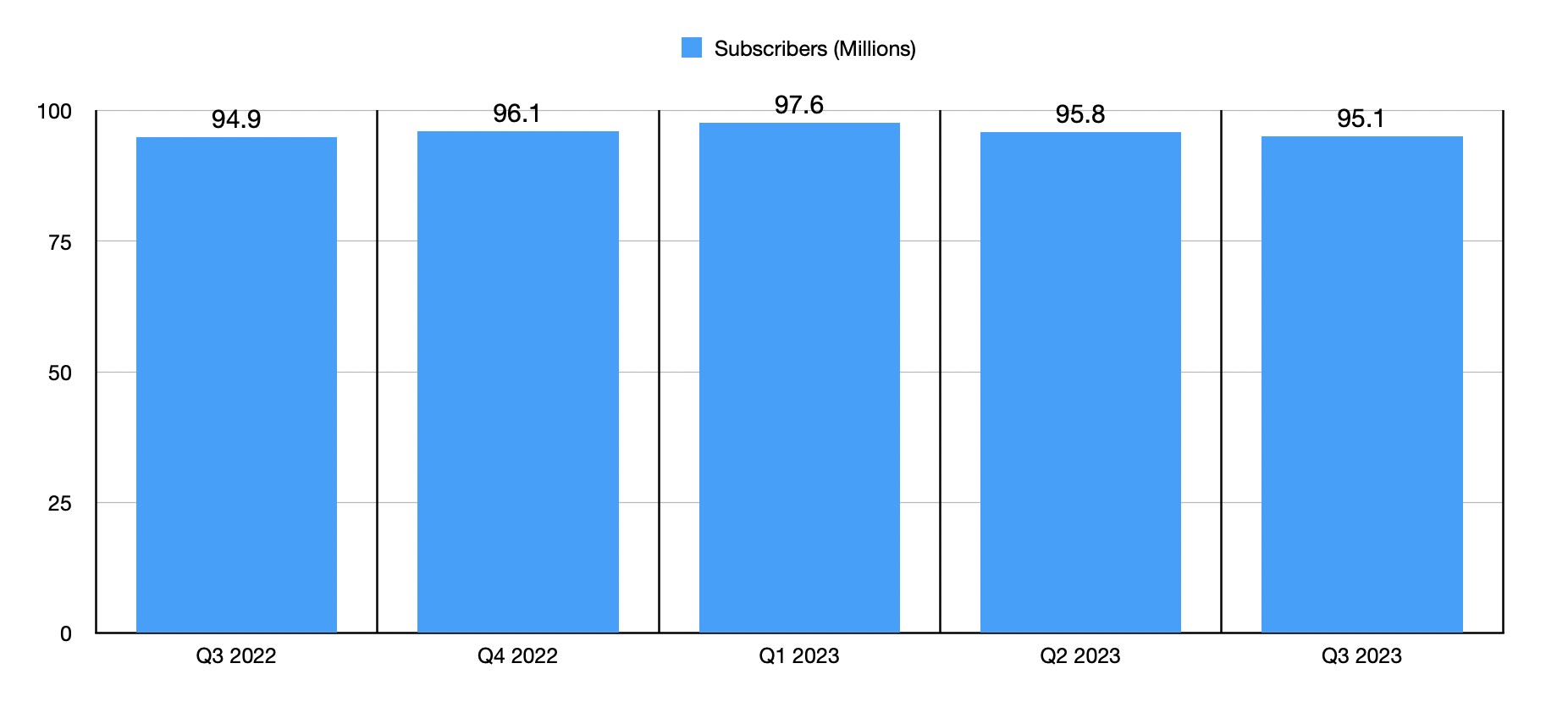

Here at home, the launch of the Ultimate tier of subscription also played a role that helped the enterprise. What bothers me, however, is the fact that, after peaking at 97.6 million subscribers in the first quarter of 2023, we have seen only declines in subscriber count since. By the end of the third quarter, that number had fallen to 95.1 million. A drop in subscriber numbers at a time when other competitors are growing is disconcerting.

{kind=link}

Takeaway

In my opinion, Warner Bros. Discovery is an interesting prospect that very well could go on to generate significant upside for shareholders. But it's not a prospect that is without a good amount of risk. When you look at the current areas of weakness for Warner Bros. Discovery, Inc. and what that might mean for the long haul, I am not yet comfortable turning bullish on the business.

If shares continue to drop and/or if we see meaningful improvements in some of these weak areas, my mindset could change. But relative to the upside that's on the table, I believe that the risk is too high for someone like me. Because of that, I have decided to keep Warner Bros. Discovery, Inc. shares rated a "hold" for now.

For further details see:

Warner Bros. Discovery Stock Is A Pass For Me For Now