HCC - Warrior Met Coal: A Cheap Coal Mining Company With Excellent Growth Prospects

2024-01-18 12:40:48 ET

Summary

- Warrior Met Coal is a leading metallurgical coal producer in the US, with two active mines and a strong focus on export sales.

- The company's Blue Creek development project is expected to significantly increase production and lower operating costs in 2026.

- Warrior has a strong balance sheet with substantial cash reserves, allowing for potential debt repayment, funding of Blue Creek, and good shareholder distributions.

Overview

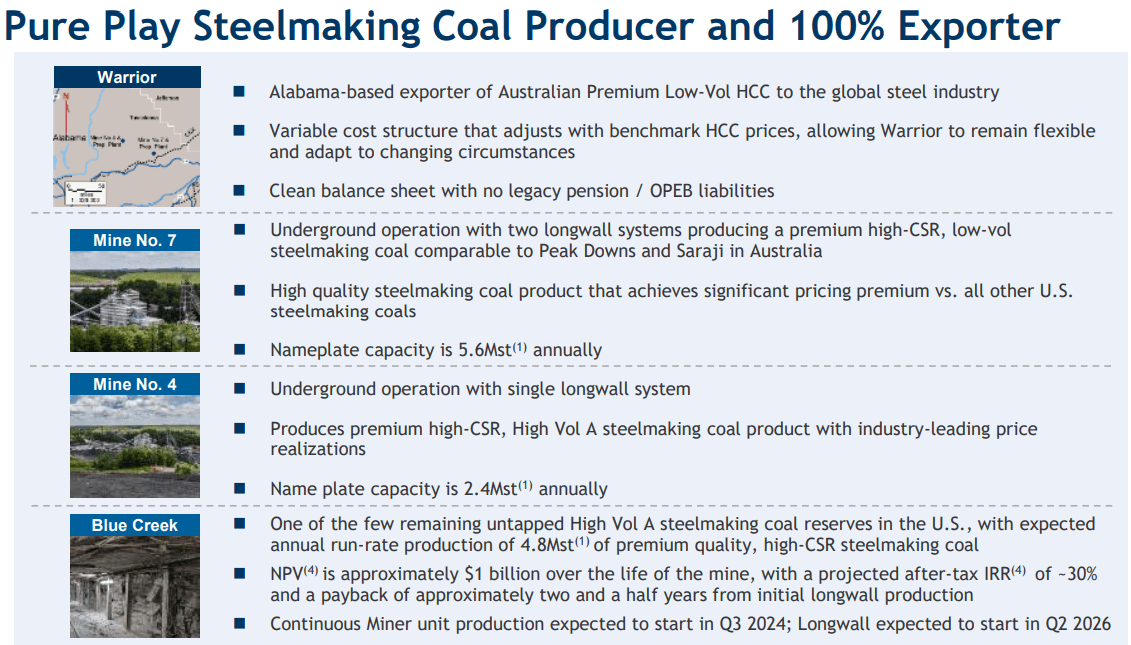

Warrior Met Coal ( HCC ) is a metallurgical ("met") coal producer in the United States. The company has two active mines in Alabama, Mine No. 4 and Mine No. 7, with a combined name plate capacity of 8M short tons of met coal production per year. The two mines have very healthy reserves, with a combined mine life of more than 20 years . Please note that any reference to tons in this article, whether in text or in the charts, refers to short tons.

The two active mines produce premium Low-Vol and High-Vol A coal, and exports 100% of its production. The combination of premium quality coal, efficient transportation to an export terminal, and the focus on export sales is why the company has an industry leading sales price and a great margin.

{kind=link}

Figure 1 - Source: Warrior Corporate Presentation

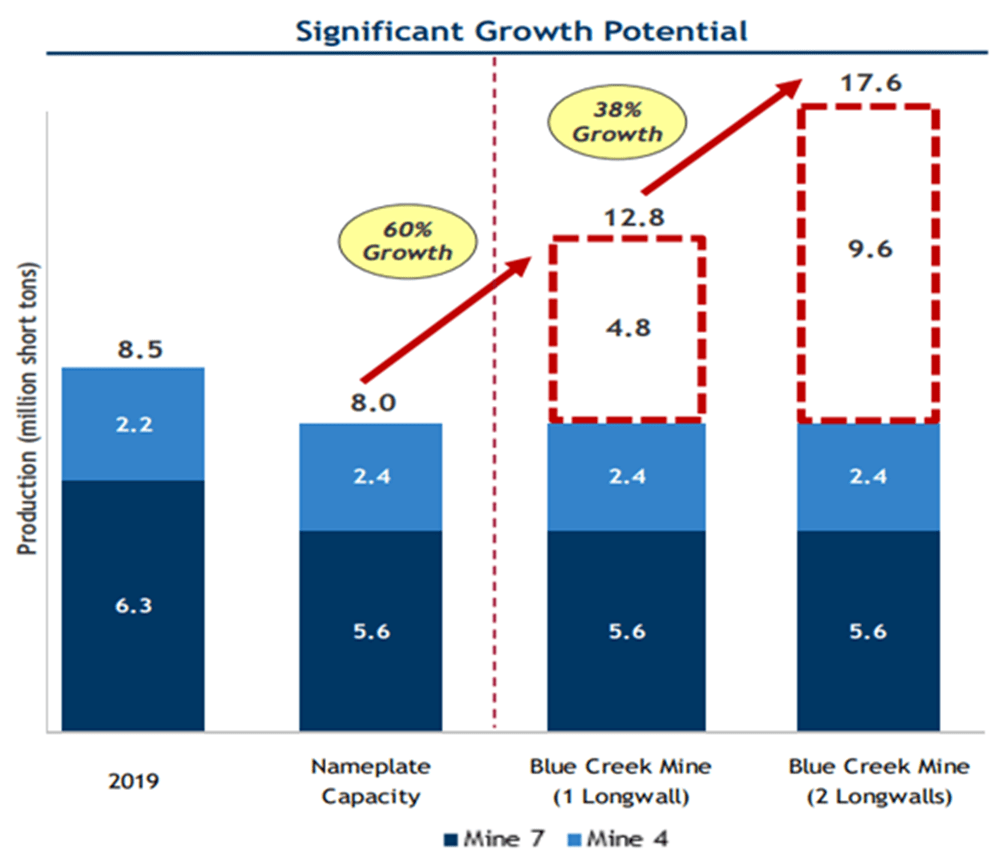

Warrior also has the Blue Creek development project, which has an estimated total project cost of around $825M, where $238.4M has been spent as of Q3-23. The project is expected to substantially boost production in 2026 when the first longwall of the mine goes into production and lower the operating cost for the company. The mine also has a lot of reserves, so it could be producing for several decades to come.

{kind=link}

Figure 2 - Source: Warrior Corporate Presentation

Warrior is already a highly profitable met coal producer, but the Blue Creek mine will be a major catalyst for the company in the coming years. However, in the short term, the project cost is naturally eating up a portion of the cash flow, which is why shareholder distributions have recently been lower than for some of the peers.

Balance Sheet & Capital Allocation

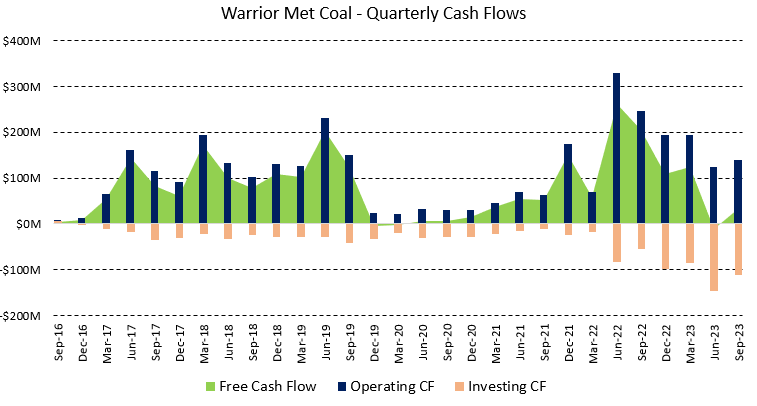

The balance sheet of Warrior is extremely strong, which is a result of some very impressive cash flows over the last few years.

{kind=link}

Figure 3 - Source: Data from Koyfin

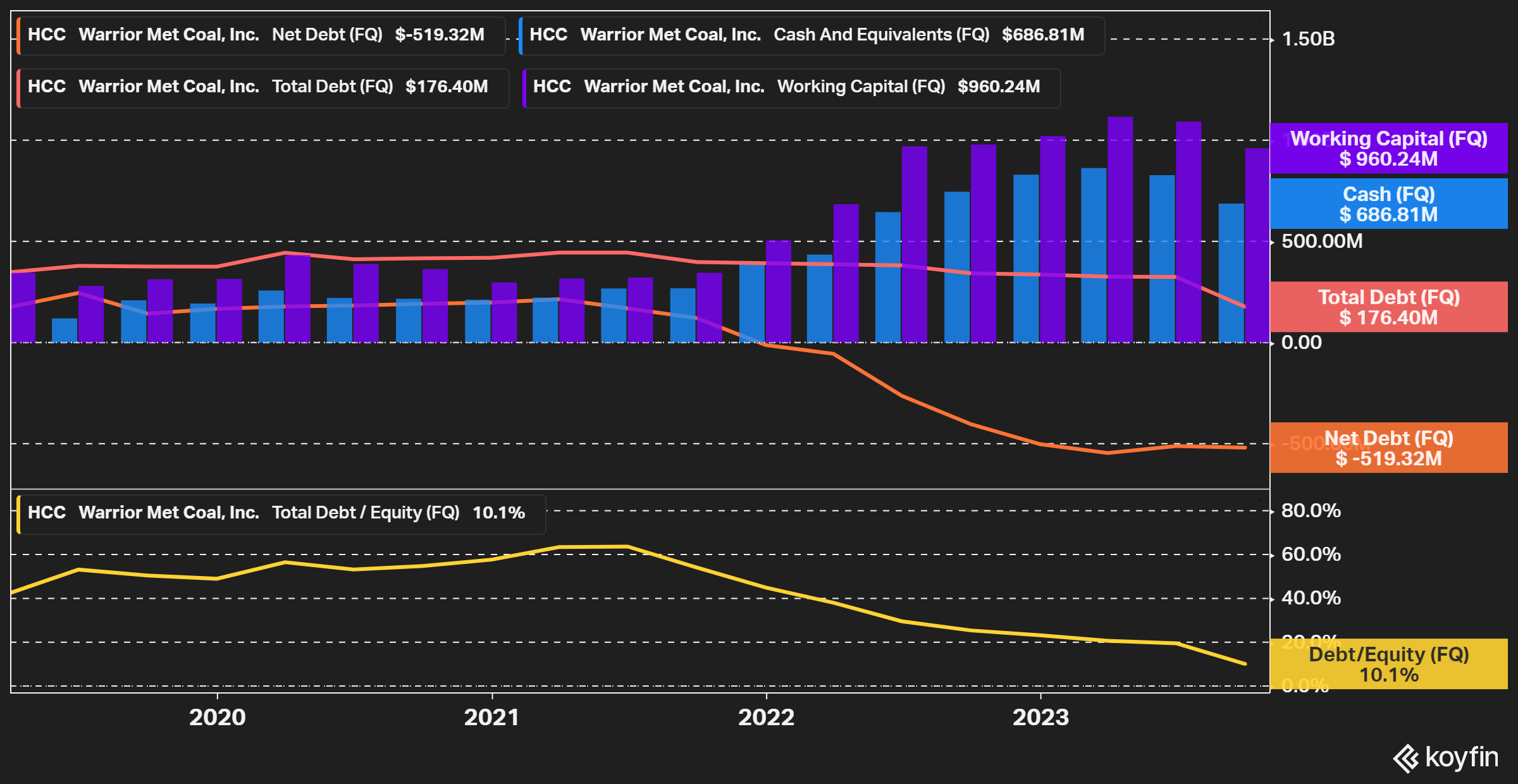

The strong cash flow has allowed Warrior to build up a substantial cash position of $687M and the working capital is as high as $960M in Q3-23. The company has $176M in total debt, following an early repayment of $146M during the third quarter of 2023.

{kind=link}

Figure 4 - Source: Data from Koyfin

So, even if the company has somewhere around $600M left to spend on Blue Creek, not counting any potential inflationary impact, there are no liquidity concerns for Warrior. If current accommodative met coal prices persist, the company can likely buy back its remaining senior secured notes, fund Blue Creek, and provide relatively good shareholder distributions over the next few years.

The regular quarterly dividend is very low at $0.07 per share, which comes to a dividend yield of less than 1%, there have also been special dividends on occasion. The company hasn't relied on buybacks recently like many of its peers, but that is understandable given the priority of funding Blue Creek.

Valuation

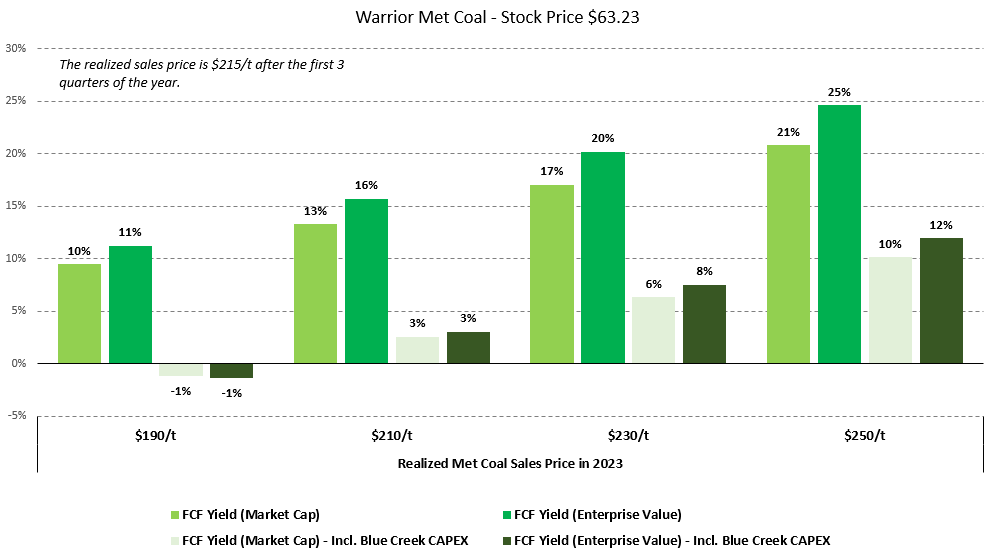

The below 2023 figure is based on the shares and financials as of Q3-23 together with the latest guidance from the company. During the first three quarters of the year, the company achieved a realized sales price of $215/t, which is likely to increase slightly for the full year, as Q4 will see a higher realized sales price, based on recent met coal price trends.

{kind=link}

Figure 5 - Source: My Estimates

If we only consider the capex for the existing mines, the 2023 free cash flow yield is likely to be close to 20%, but that drops to a single digit free cash flow yield when all the capex is considered.

The company hasn't provided official guidance for 2024 yet, but if close to current met coal prices persist, the numbers are likely to improve in 2024, somewhat depending on how much of the remaining Blue Creek capital spending ends up in this year. It is worth reiterating that unless the project capex changes, much of the Blue Creek capex can also be taken from the working capital.

Conclusion

If we primarily focus on the near-term cash flows and shareholder distributions, Warrior is attractive compared to the overall market. However, the near-term cash flow yield and shareholder distributions are less impressive than for some other U.S. met coal producers, which were discussed here recently.

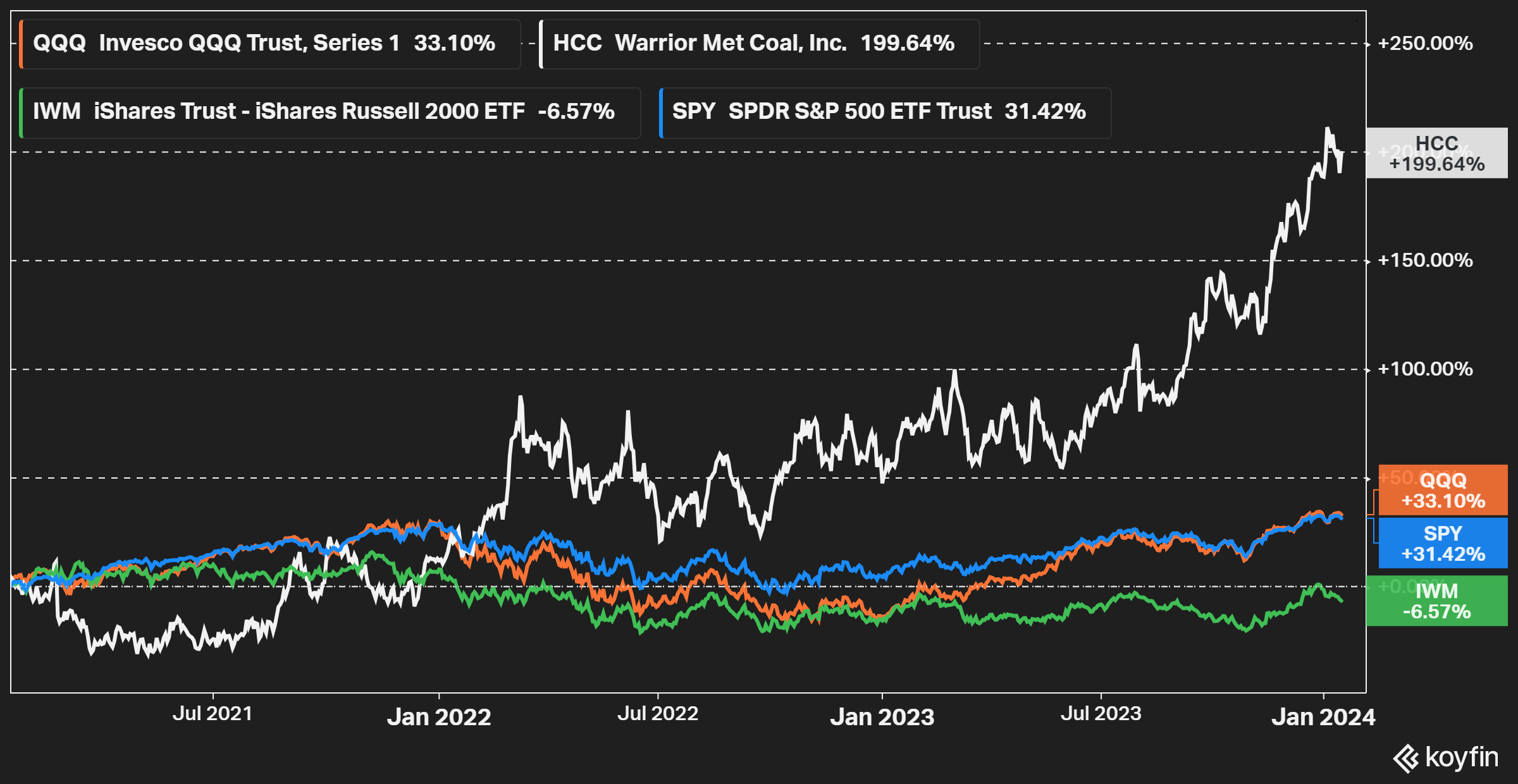

Anyone making an investment in Warrior should be aware of the lower near-term free cash flow, but if Blue Creek comes online on budget and on time, the current share price still feels very attractive. That is despite the strong stock price performance we have seen over the last few years.

{kind=link}

Figure 6 - Source: Koyfin

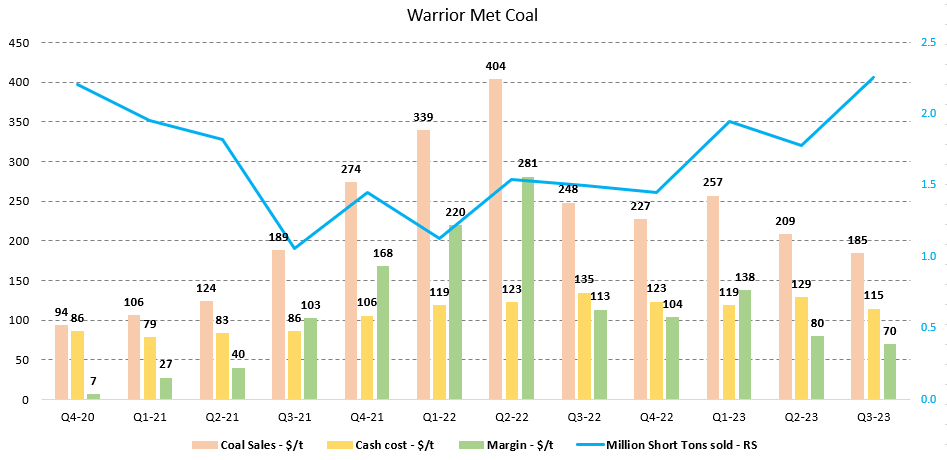

Warrior Met Coal has some of the better margins in the business, which will improve further once Blue Creek starts producing material quantities. This will naturally transform the production, cash flows, valuation, and capital distributions to shareholders. So, in the medium term, Warrior is just as attractive, possibly more, than some of its peers.

{kind=link}

Figure 7 - Source: Warrior Quarterly Reports

Large construction projects are not without risk though, which one should consider. Cost overruns and delays for a multi-year project with a budget of almost $1B are relatively common. However, I do think investors are well compensated for that risk at the current share price. There are no significant leverage or liquidity risks, which means delays are at least much more manageable if they were to materialize.

There is of course commodity price risk as well. It is important to remember that coal prices are cyclical, so while I like the risk-reward here for a multi-year investment, waiting for a smaller correction might be prudent before buying or adding to Warrior Met Coal.

For further details see:

Warrior Met Coal: A Cheap Coal Mining Company With Excellent Growth Prospects