HCC - Warrior Met Coal: Expected Production Increase Makes It Look Undervalued

2023-11-29 17:11:42 ET

Summary

- Warrior Met Coal recently reported better than expected earnings and announced appealing decisions such as dividend increases and note repurchases.

- The Blue Creek project is expected to significantly increase free cash flow to around $647 million, indicating significant undervaluation.

- Recent earnings were overall better than expected, with EPS GAAP close to $1.64 and revenue of $423 million. However, I will be studying Warrior mainly because its valuation appears low.

Warrior Met Coal, Inc. ( HCC ) recently delivered better than expected EPS, and announced many other appealing decisions like dividend increases and the repurchase of notes. With that, the most interesting appears to be the Blue Creek project, which is expected to push FCF to close to $647 million. Given the current market capitalization, I believe that the undervaluation is significant. There are obvious risks from changes in the price of coal, crude oil price, or the price of steel. Besides, changes in the mining regulation, accidents, or changes in the labor law could affect production or the FCF margin growth. With that, HCC does look like a must-follow stock.

Business Model

The company is a U.S.-based supplier to the global steel industry, offering the possibility of 13 million short tons of coal capacity production for steel manufacturers in Europe, South America, and Asia. The company reported two operating mines and a mine under development called Blue Creek.

Source: Quarterly Report

Recent earnings were overall better than expected, with EPS GAAP close to $1.64 and revenue of $423 million. However, I will be studying Warrior mainly because its valuation appears too low.

Source: SA

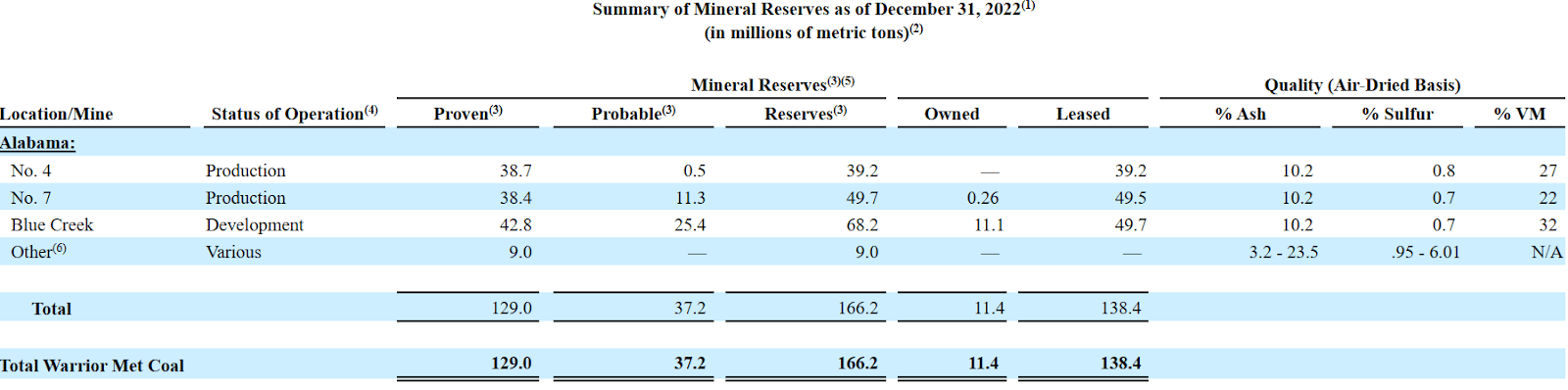

With three mines, I believe that the most interesting thing about Warrior Met is the total amount of reserves and the expected mine life. The company expects to improve production from 8 million short tons to close to 13 million short tons.

Source: Warrior Met Coal

According to the last annual report, Warrior reported proven reserves of close to 129 million metric tons. If we assume 8 million tons sold per year, future production would last for about 15-16 years. Including total reserves of 166 million metric tons and 8 million tons per year, I would say that Warrior could operate for about almost 21 years.

{kind=link}

With the information from the recent quarterly release, we can make an approximate valuation of the company. In the last quarter, the company reported an adjusted EBITDA of $145 million, close to 2 million tons sold, and an average per ton of $203k.

Source: 10-Q

Source: Quarterly Report

If we multiply the average selling price per ton by the total amount of reserves, we may obtain a valuation that appears elevated given the current market capitalization. It is worth taking into account that Warrior may deliver lower production than expected, or the total amount of proven reserves may not be correct.

With that, I believe that Warrior is quite undervalued. Assuming annual adjusted EBITDA of $580 million for 16 years, I do think that the total market capitalization of $2.9 billion sounds too small. I executed a DCF model to understand what could be the fair price, but there are some analysts who believe that this looks like a buy.

Source: SA

Balance Sheet

As of September 30, 2023, the company reported cash and cash equivalents worth $686 million, short-term investments of about $8 million, trade accounts receivable close to $268 million, and total current assets worth $1104 million. The current ratio is larger than 1x, so I believe that liquidity does not seem an issue here. Additionally, with mineral interests of $82 million and property, plant, and equipment worth $1006 million, total assets stood at about $2.219 billion. The asset/liability ratio is larger than 5x, so I believe that the balance sheet appears quite healthy.

Source: 10-Q

I am really not concerned about the total amount of liabilities or the debt outstanding. Accrued expenses stood at $72 million, with short-term financing lease liabilities close to $13 million and total current liabilities of about $143 million. Besides, with long-term debt of about $152 million, asset retirement obligations worth $64 million, and long-term financing lease liabilities close to $9 million, total liabilities were equal to $474 million.

Source: 10-Q

The New Project Could Bring Significant IRR Increase, And Warrior Could Be Trading At 4x-5x FCF

I believe that anybody interested in Warrior needs to study carefully the numbers of the new project. They include a maximum net present value of about $1.58 billion, payback of 3.8 to 1.8 years, and IRR between 18% and 35%.

Source: Quarterly Report

With the Blue Creek project, the company is expecting to deliver an Adjusted EBITDA of close to $784 million and FCF of about $647 million. If we assume a market capitalization of about $2.9 billion, with the Blue Creek project, the company would be trading at close to 4x-5x FCF.

Source: Quarterly Report

Significant Logistical Cost Advantages, Which May Bring FCF Margin Growth

I also believe that it is worth noting the fact that customers are not that far from the facilities of Warrior Met. With most clients located in North America or Europe, Warrior does not have to pay a lot in transportation, which may enhance future FCF margins in the coming years. In a recent presentation, management offered further explanation with respect to the logistics of its operations.

Source: Quarterly Report

Given The Current Amount Of Liquidity And Recent Acquisitions, I Believe That We May See New M&A Operations

The recent acquisition of Black Warrior Methane and Black Warrior Transmission as well as ownership interest in gas wells were not very significant. However, given the state of the balance sheet and the total amount of cash in hand, I believe that management may try to acquire new interests, which may accelerate production, reserves, and FCF growth potential.

We acquired the remaining 50% interest in Black Warrior Methane and Black Warrior Transmission for $0.3 million. The purchase consideration has been allocated to the assets acquired and liabilities assumed based upon their estimated fair values at the date of acquisition. The acquisition is not deemed to be material to the condensed financial statements. Source: 10-QOn March 31, 2023, we acquired the remaining ownership interest in gas wells owned by an independent third party for $2.4 million. Source: 10-Q

Recent Increase In Dividends Reported In 2023 May Bring Demand For The Stock

I also believe that further announcement with regards to quarterly cash dividend increases could bring more demand for the stock. In 2023, we saw once again an increase in the dividend per share. In the last 5 years, the company reported a growth rate of close to 6.96%.

We announced that the Board approved an increase in the regular quarterly cash dividend by 17%, from $0.06 per share to $0.07 per share. Our strategy continues to be focused on optimizing our capital structure to improve returns to stockholders, through special cash dividends, while allowing flexibility for us to develop our strategic growth project Blue Creek. Source: 10-Q

Source: SA

The Tender Offer And Lowering Leverage Could Bring New Investors, And Enhance The Demand For The Stock

The recent tender offer for the 8.00% senior secured notes due 2024 and other transactions recently reported indicate that management intends to lower its cost of debt and leverage. Successful reductions in the total amount of debt or decline in the total amount of interest paid will most likely bring the interest of new investors. Besides, I believe that Warrior could trade at better EV/FCF and EV/EBITDA multiples. As a result, we could see an increase in the stock price. The following lines include information about recent debt transactions.

We used the net proceeds of the offering of the Notes, together with cash on hand, to fund the redemption of all of our outstanding 8.00% senior secured notes due 2024 (the “Existing Notes”), including payment of the redemption premium in connection with such redemption.

The Notes will accrue interest at a rate of 7.875% per year from December 6, 2021. Interest on the Notes will be payable on June 1 and December 1 of each year, commencing on June 1, 2022. The Notes will mature on December 1, 2028.

On August 9, 2023, we commenced an offer to purchase (the “Restricted Payment Offer”), in cash, up to $150,000,000 principal amount of its outstanding Notes, at a repurchase price of 103% of the aggregate principal amount of such Notes, plus accrued and unpaid interest with respect to such Notes to, but not including, the date of repurchase (the “Restricted Payment Repurchase Price”). Source: 10-Q

Valuation Considering The Coal Sales Guidance, Previous Financial Figures, And The Expectations Of Other Analysts

For the assessment of the incoming income statements and cash flow statements, I took a look at the expectations of management and the expectations of other market analysts. The company expects coal sales close to 7.1-7.2 Mst and capital expenditures of about $95-$105 million. Note that I did not include the capital expenditures reported for the Blue Creek project.

Source: Quarterly Report

In the past, Warrior reported quarterly net sales growth as large as 150%-100% y/y, but also negative net sales growth. With these figures, I believe that assuming net sales growth close to 7% appears conservative.

Source: Ycharts

I also took a look at the previous financial figures like the EBIT margin, changes in working capital/sales, and capex/sales of D&A/sales to design my DCF model.

Source: YCharts

My assumptions included short tons sold close to 10.457 Mst, growth rate of 7%, EBIT margin of about 27%, and conservative tax rate of 25%. Additionally, with working capital/sales of 8% and capex/sales of 9.5%, I also included cost of capital close to 7.8% and depreciation/sales of 9.54%.

Source: My DCF

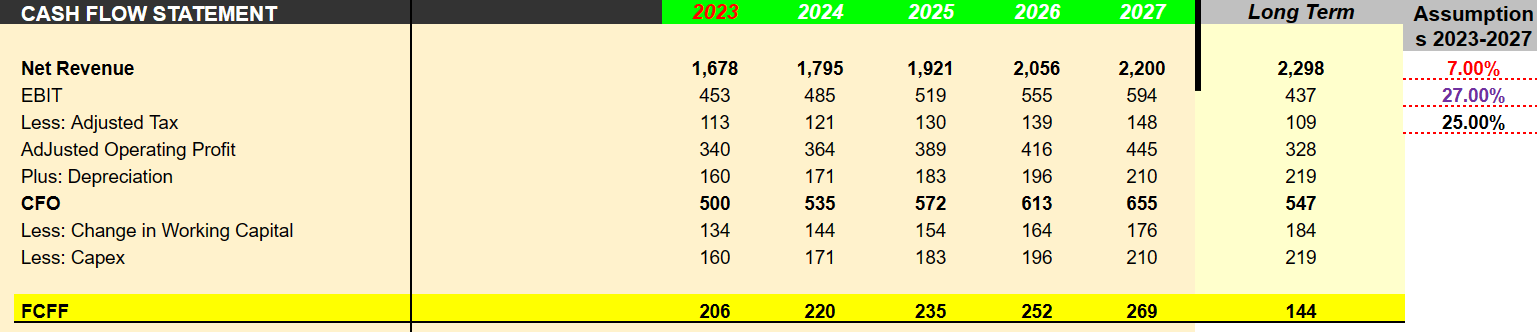

For the calculation of the net debt, I included short-term investments, but also the asset retirement obligations, long-term financing lease liabilities, and long term debt. The results are shown in the image below.

Source: My DCF

With the previous assumptions, I obtained 2027 net revenue close to $2.199 billion, with EBIT of $593 million, adjusted operating profit of about $445 million, and depreciation of about $210 million. The implied results would be 2027 CFO of $655 million, with change in working capital of $175 million and FCFF close to $269 million.

{kind=link}

Using the Gordon-Growth model for the valuation of the exit multiple, the implied equity forecast would be close to $71 per share. Given the current market capitalization, I would say that there exists certain undervaluation.

Source: My DCF Model

Competitors, And Risks

According to Seeking Alpha, competitors are trading at EV/EBIT, EV/EBITDA, and PE ratio larger than that of Warrior Met. Trading multiples of companies in the same sector indicate that Warrior could be undervalued by close to 51%. The following table appears quite relevant.

Source: SA

I see risks with regards to changes in the price of crude oil, which may lower the FCF margins of Warrior, and lower the implied valuation of the company. Even if clients are not far, logistics could become quite expensive if the oil price reaches $100 per share.

The company may also suffer significantly if final reserves or production is lower than expected. Note that proven, provable, and indicated reserves are an approximate estimate of what the company may produce. If engineers and geologists fail to assess the total amount of reserves, production estimates may decrease, which may also lead to lower net sales growth estimates and FCF growth estimates.

Changes in the labor conditions, accidents, strikes, or even changes in the mining regulations could also affect the business model. As a result, Warrior could suffer production decreases, lower FCF margins, or lower EPS expectations. In the worst case scenario, if dividends decrease, I believe that many investors could sell shares, which could lead to lower stock prices.

It is also worth noting that Warrior delivers net sales from the production of coal. There is little diversification in terms of mineral properties. Lower coal pricing or the emergence of new mineral substitutes for manufacturing could lower the net sales expectations delivered by investment analysts.

Substantially all of our revenues are derived from the sale of met coal and our business may suffer from a substantial or extended decline in met coal pricing and demand or other factors beyond our control. This lack of diversification of our business could adversely affect our financial condition, results of operations and cash flows. Source: 10-k

Increases in price of steel, copper, and rubber products could also bring lower FCF margins and lower EPS expectations. Keep in mind that Warrior uses a significant amount of equipment made of these minerals. If mining equipment becomes more expensive, capital expenditures may need to increase, which may lower profitability.

Met coal mining consumes large quantities of commodities including steel, copper, rubber products, diesel and other liquid fuels, and requires the use of capital equipment. Some commodities, such as steel, are needed to comply with roof control plans required by regulation. The cost of roof bolts we use in our mining operations depends on the price of scrap steel. The prices we pay for commodities and capital equipment are strongly impacted by the global market. A rapid or significant increase in the costs of commodities or capital equipment we use in our operations could impact our mining operations costs because we may have a limited ability to negotiate lower prices and, in some cases, may not have a ready substitute. Source: 10-k

Conclusion

Warrior recently delivered better than expected quarterly earnings reports, but I believe that the company is a must-follow because of its Blue Creek project. The new project is expected to enhance production, and help deliver an adjusted EBITDA of close to $784 million and FCF of about $647 million. Also, taking into account recent dividend increases, the repurchase of notes, and acquisitions, there are many attractive things about Warrior. There are risks from lower production than expected, higher crude price, or commodity inflation, however I believe that future FCF growth expectations could imply significant undervaluation.

For further details see:

Warrior Met Coal: Expected Production Increase Makes It Look Undervalued