HCC - Warrior Met Coal: Still Attractive After Its 200% Run

2024-01-09 10:28:00 ET

Summary

- Warrior Met Coal has outperformed the S&P 500 by more than 200% in the past 36 months.

- The company has been generating strong cash flows and reported a net profit of more than $85.4 million in Q3 2023.

- The development of the Blue Creek coal mine is expected to significantly increase Warrior Met Coal's free cash flow and support its current valuation.

Introduction

Back in 2020, I was very bullish on Warrior Met Coal ( HCC ) as I was expecting the metallurgical coal price to rebound once the fallout of the COVID pandemic had been digested. I anticipated the share price to increase by 100-200% within 24 months. We're now 36 months later, and the total return of this idea has jumped to in excess of 240%. An outperformance of the S&P 500 ( SPY ) by in excess of 200% in the same period.

Seeking Alpha

While I'm definitely very happy to have identified this opportunity, it now appears I sold the majority of my position too early . While I was speculating on a rebounding coking coal price, I had not anticipated the price of metallurgical coal would be "higher for longer." The image below shows the price history for coking coal (Australian-sourced, which still provides "the" benchmark price) for delivery in June of this year. And sure, the price has been bouncing around dropping from $600 to just $200 during 2022, but it has since averaged around $300/t.

barchart.com

And that's why I wanted to revisit Warrior Met Coal to see if I should perhaps get back in.

The company has been printing cash lately

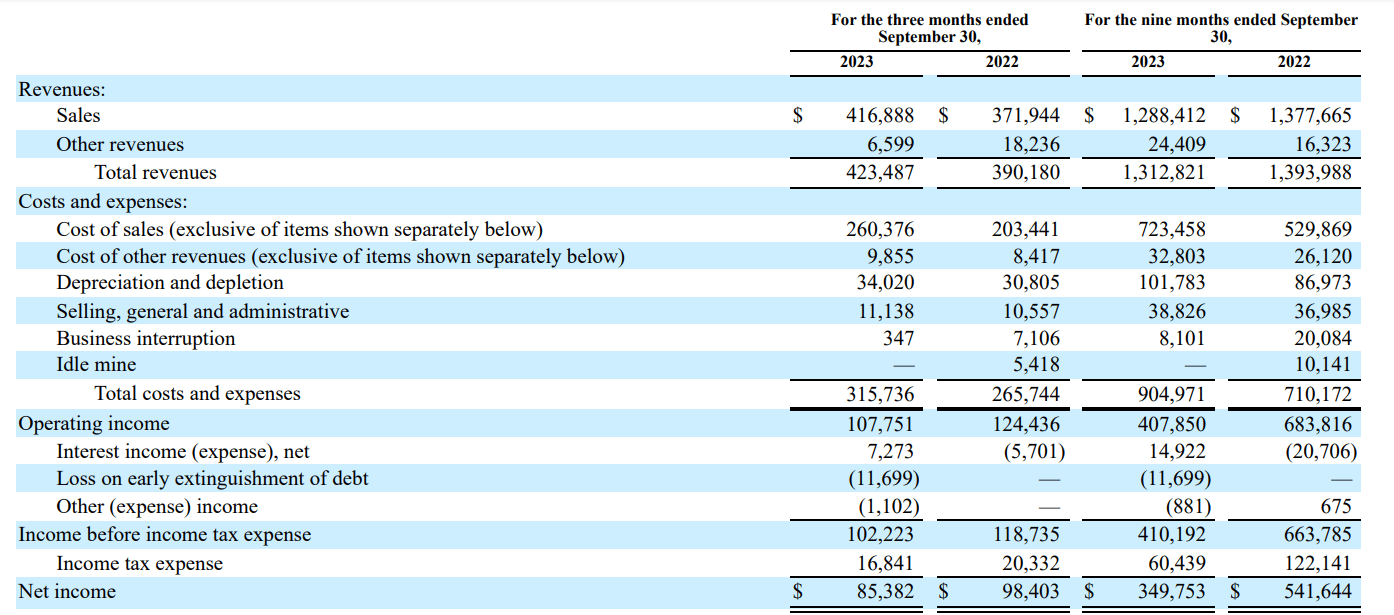

During the third quarter of this year, the company sold approximately 2.3 million short tons, which is a very substantial year-over-year increase thanks to better rail and terminal availability. That's great but keep in mind that the company sold more than it produced as its output was just 2 million tonnes and the additional 260,000 tonnes were drawn from the existing inventory levels. With an average net selling price of almost $185 per short ton, Warrior Met Coal was able to convert the 260,000 tonnes of inventory into almost $50M of cash.

This resulted in a total quarterly revenue of $417M from the sale of coal, resulting in total revenue of just more than $423M. As the total operating expenses came in at almost $316M, the total operating income was almost $108M, which is just slightly below the Q3 2022 operating income.

{kind=link}

The company also recorded a net interest income and the sole reason why its net finance expenses came in negative was related to the early extinguishment of debt. With a pre-tax income of $102M, the net profit of in excess of $85.4M for an EPS of $1.64 per share was very robust.

Looking at the 9M 2023 results, the company reported a total operating income of $408M and a net profit of $350M, resulting in an EPS of $6.73 per share.

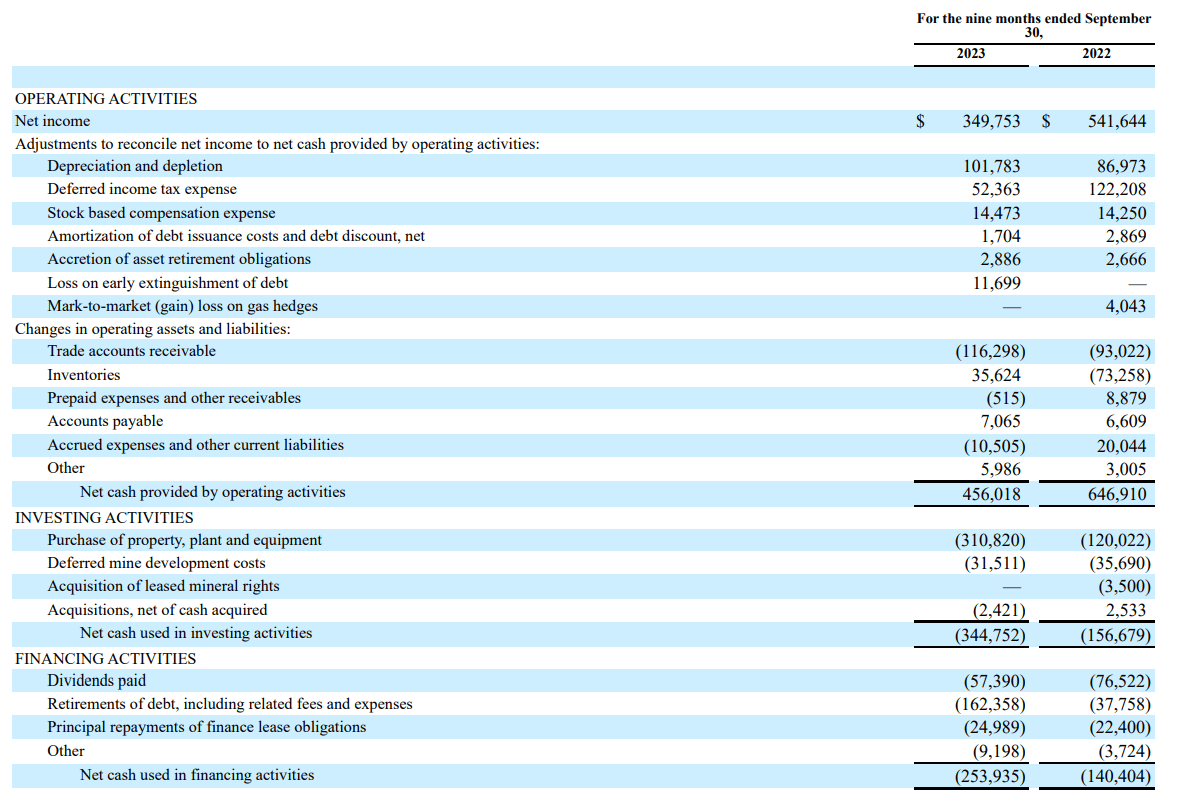

This also translated into very strong cash flows. As you can see below, Warrior Met Coal generated approximately $456M in operating cash flow, but this includes a relatively high net investment in the working capital position, mainly because the total amount of receivables increased. I expect those receivables to be converted into cash in the near future.

{kind=link}

Adjusted for those changes in the working capital position and the lease payments, the operating cash flow was $509M.

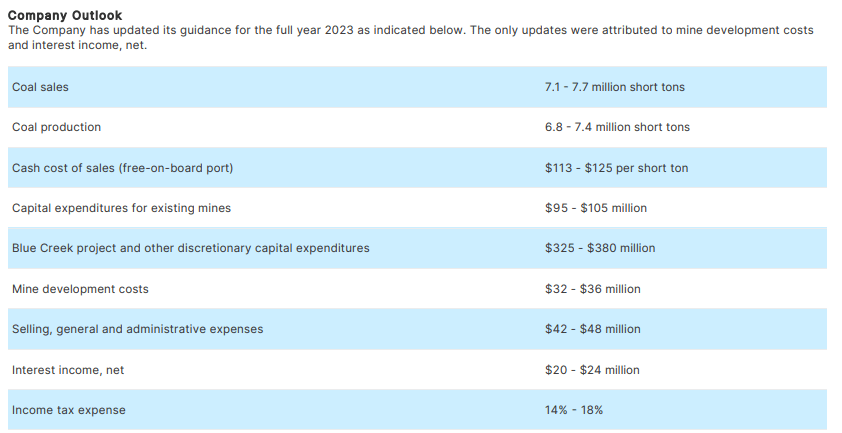

We see the total capex was approximately $342M, but this includes a tremendous amount of growth capex. As you can see below, last year's total capex guidance for the existing mines was just around $100M. If we add $35M in mine development costs, we end up with just under $140M in sustaining capex for the year. This means the normalized 9M 2023 sustaining capex would be around $105M, resulting in an underlying free cash flow result of approximately $404M or $7.8/share.

{kind=link}

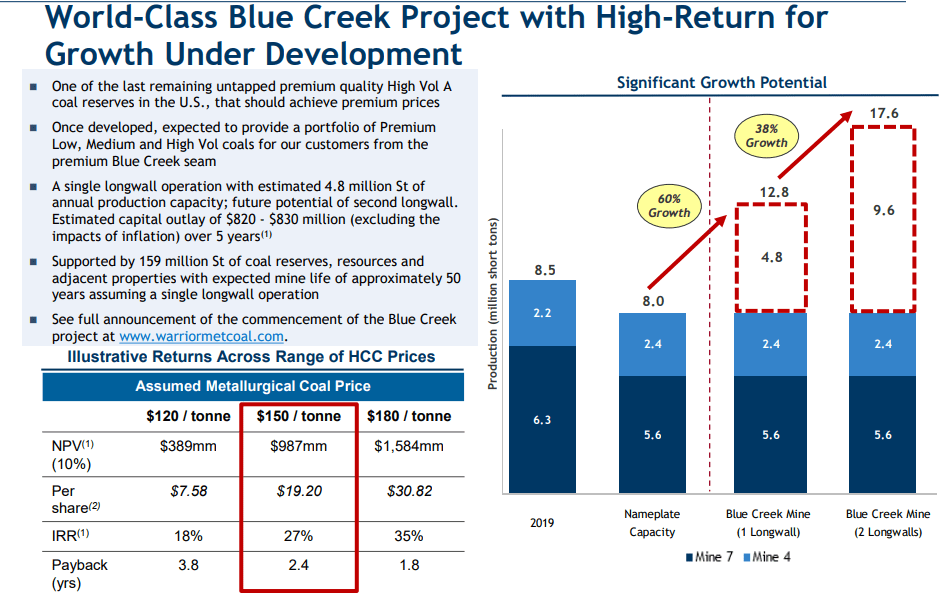

As explained in a previous article, it makes a lot of sense for Warrior Met Coal to invest its "excess" cash flow in the development of the Blue Creek coal mine. The anticipated $350M capex to be spent on Blue Creek this year should be fully covered by the company's sustaining free cash flow. At an average realized coking coal price of $150 per metric tonne (which is about 25% lower than the average realized price during the third quarter), Blue Creek will add approximately $245M in free cash flow per year to Warrior Met Coal's result. At $180 per metric tonne, Blue Creek will even add $339M in annual free cash flow , which means Blue Creek alone could support Warrior's current valuation.

Warrior Met Coal Investor Relations

According to Warrior Met Coal, the NPV10% of Blue Creek is just under $31/share using a coal price of $180 per tonne.

{kind=link}

By the end of this year, Warrior Met Coal will have spent close to $500M on the development of Blue Creek, which will put it on track for initial production by the end of this year . The total capex guidance has been increased to $820-830M, including the development of the longwall section which will accelerate the production rate to 9.6 million short tons per year, which should be reached by the end of 2026.

Investment thesis

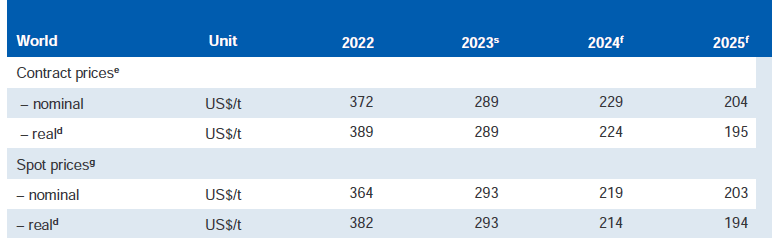

While I was happy taking profits, it now looks like I may have sold my position in Warrior Met Coal too early. The coking coal price is still trading higher than I had expected and even the outlook for the next few years is better than I had anticipated. In its recently published quarterly report issued by the Office of the Chief Economist, the Australian Department of Industry, Science and Resources anticipates the average coking coal price to exceed US$200/t for the next two years. That would be great news for Warrior Met Coal as the initial revenue and cash flow from the first longwall section of the mine could fund the development of the second longwall.

{kind=link}

I currently have no position anymore in Warrior Met Coal, but the company's future looks pretty bright. Using Q3 2023 prices, adding the first phase of the Blue Creek Longwall development would likely result in a sustaining free cash flow result of $10-12/share. Adding the second longwall to the combined production would catapult the free cash flow at $180/st to in excess of $16/share.

Even if the coal price decreases to $150/st on a net selling price basis, I anticipate the FCF per share to exceed $5.5. And with in excess of $10/share in net cash on the balance sheet and a positive working capital position of almost $1B, the balance sheet likely has never been this strong.

Based on all these elements, Warrior Met Coal still appears to be a "buy" and it looks like I sold out too soon.

For further details see:

Warrior Met Coal: Still Attractive After Its 200% Run