WCN - Waste Connections Stock: Highly Attractive Business But Not So Much For The Valuation

2023-08-08 12:22:25 ET

Summary

- Waste Connections is a high quality business underpinned my multiple competitive advantages.

- The company's business model focuses on secondary rural markets, allowing them to capture more market share and have pricing power.

- Waste Connections has a resilient business with consistent revenue growth and impressive cash flow generation.

- Despite the attractive business, I assign a hold because the company seems fairly valued at the current price.

Investment Thesis

Waste Connections (WCN) is the third-largest waste services company in North America. The company's strategy to focus on secondary and rural areas has allowed them to expand market share, have higher margins than competitors, and create competitive advantages such as landfill ownership and pricing power.

WCN's industry itself is protected by high barriers to entry like regulations and capital intensity. I like to believe the company's business model to be resilient due to strong demand and very low risk. Despite all the pros, I assign a hold because the stock seems fairly valued. Now let me explain my thesis's main point in more detail.

Competitive Advantages

WCN operates in Waste collection and Waste Disposal. I will be discussing the waste disposal industry. I believe the waste disposal industry is protected by two high barriers to entry. The first one is Capital intensity. WCN has spent an average of 11.34% of revenue on capital expenditures in the past 10 years and more than $5 billion on acquisitions in the past five years. These investments have helped the company expand its footprint and strengthen its cost advantage against peers, resulting in higher margins. Same scenario with its peers: On average, Republic Services spent 10.74% of revenue on CapEx in the past 10 years and Waste Management spent 10.52%.

The second barrier is regulations. According to Statista , in 1990, there were 6326 municipal waste landfills, and as of 2018, there were 1269. The tight government regulations and "not in my backyard" movements or activism have made it very difficult to open or receive approval for new landfills. Landfills are expected to keep decreasing, which will make them even more scarce and a precious asset. In order for a waste disposal company to succeed they need access to the right Landfills and transfer stations. WCN has 100 landfills, Waste Management +250, and Republic Services +180.

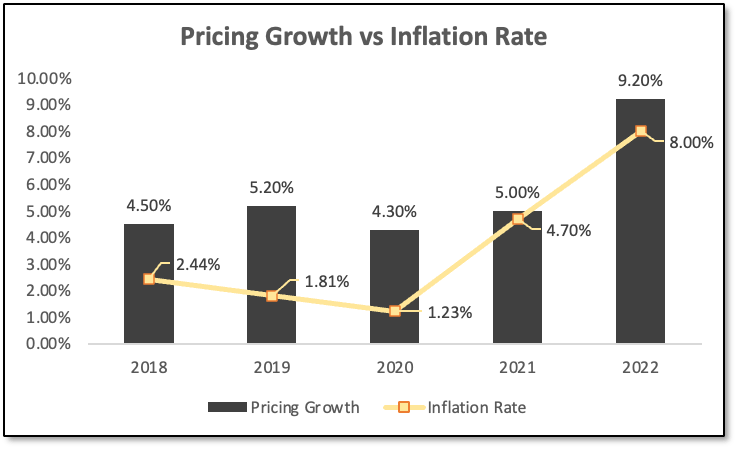

Despite having fewer landfills than its two other peers, I believe the company has stronger pricing power than them. How, you might ask? My belief is as follows: rather than competing with the mega-companies in urban areas, WCN focuses on establishing its footprint in markets that competitors don't find attractive such as secondary and rural areas. As a result, companies in those markets have no other choice but to contract with WCN, Thus providing the company with pricing power. Below is a graph chart comparing WCN's pricing growth with CPI.

Created by the author using company filings

{kind=link}

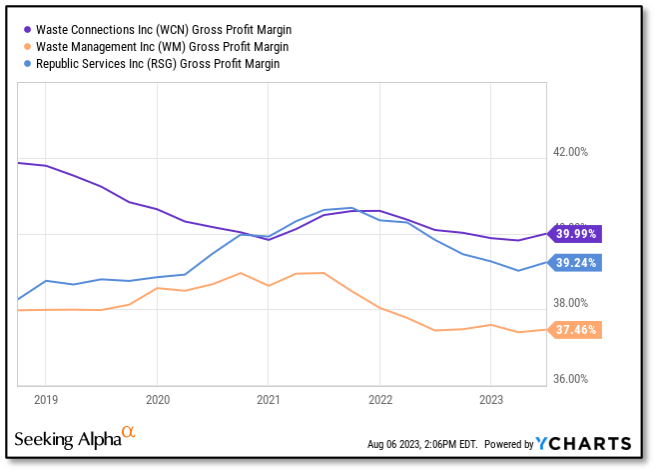

As you can see due to the company's strong pricing power, they have been able to increase prices at a rate that is higher than inflation. Pricing power can also be reflected in the company's gross margin. Below is a graph of WCN's gross margin vs. peers over the years. As you can see, the firm has outpaced its competitors for years.

{kind=link}

Business Model

I like to believe that WCN is a resilient and safe business because it benefits from recurring revenue due to the long tenure of its contracts and the simple fact that we as human beings will always produce waste and I believe that as the population grows so does waste volume. Personally, I love businesses with recurring revenue because it enables predictable cash flow.

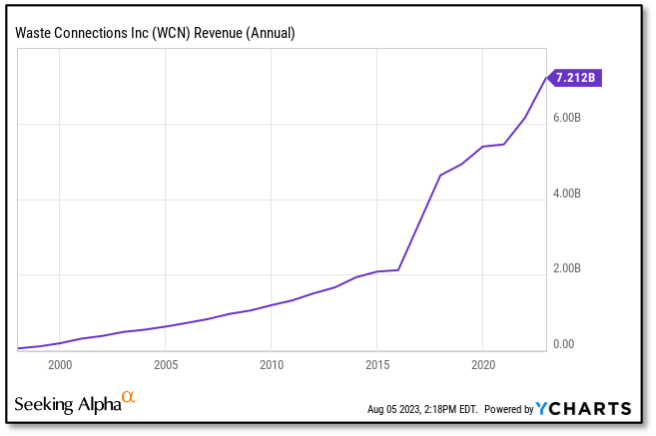

Waste services companies tend to have very little risk because they are not exposed to many macroeconomic conditions. Whether we are in a good or bad economy, there will still be demand for waste services. That puts WCN in a good position. Below is a graph that further proves the resiliency of WCN's business. Revenue has not experienced a decline for over 15 years. During the financial crisis, revenue grew by 10%, and during the COVID lockdown, it grew by 1.06%. Of course, all of this revenue wasn't organic, the company has made a few acquisitions to extend its footprint. Over the past five years, The firm has spent more than $5 billion on acquisitions.

{kind=link}

Another thing I want to point out is that despite spending an average of 11.34% of revenue on capital expenditures in the past 10 years, Free cash flow has grown at an annual rate of 17% in the same period. WCN's free cash flow generation is truly impressive, with it only declining in 2020 over the past 10 years and quickly recovering to above the pre-covid level in 2021. I believe that the company's strong cash generation has to do with its landfill ownership and pricing power. This will enable it to keep generating free cash flow in the future.

Company Overview

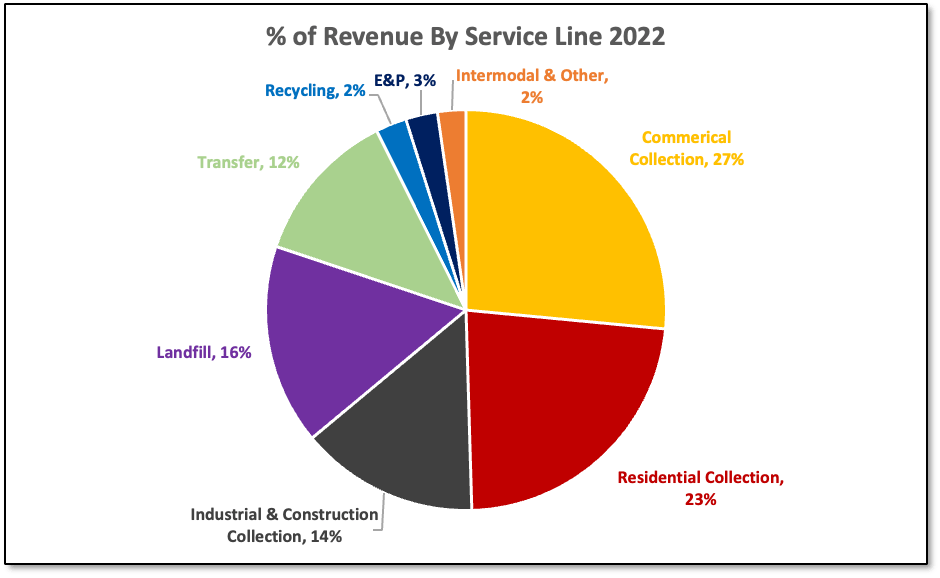

Waste Connections, along with Waste Management (WM) and Republic Services ( RSG ), is the third-largest waste services company in North America. The firm has 100 active landfills, 157 transfer stations, and 79 recycling operations. The company operates in Canada and the United States. The firm is very diversified in terms of revenue, Deriving revenue from eight different sources: Its collection business has three units: Residential, Commercial, and Industrial & Construction. The other sources are Landfills, Transfer, Recycling, E&P, and Intermodal.

{kind=link}

The waste collection business involves the collection of waste from residential, commercial, and industrial customers for transport to transfer stations, or directly to landfills or recycling centers.

Landfill revenue is generated by charging tipping fees on a per-ton and/or per-yard basis to third parties based on the volume disposed of and the nature of the waste. Transfer station revenue is primarily derived from charging tipping or disposal fees on a per-ton and/or per-yard basis. The fees charged to third parties are based primarily on the market, type, and volume.

I think everyone knows what recycling is. As for E&P revenue, it is revenue primarily generated through the treatment, recovery, and disposal of non-hazardous exploration. Intermodal revenue is primarily generated through providing intermodal services for the rail haul movement of cargo and solid waste containers in the Pacific Northwest.

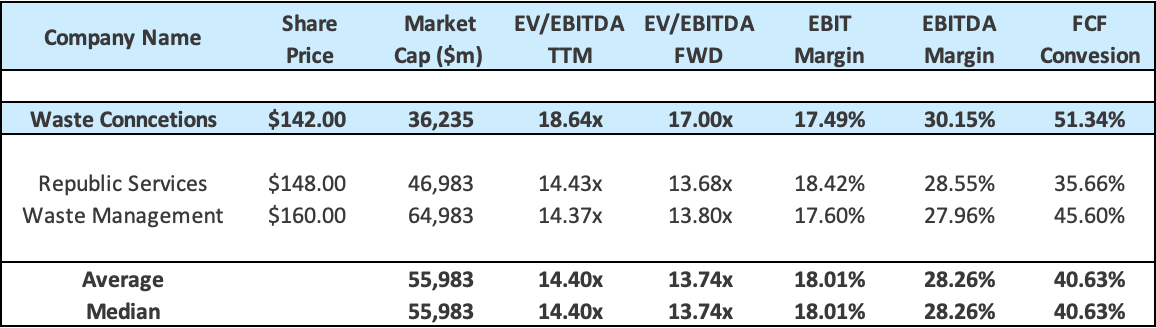

Competitors

WCN only really completes against two other companies. Waste Management and Republic Services. Below is a table I constructed comparing the three companies in terms of multiples and margins.

{kind=link}

As you can see the company is trading at a higher EV/EBITDA multiple when compared to its peers, but the firm does have a higher EBITDA margin and free cash flow conversion than its comps. I think this is possible due to the firm's focus on landfill ownership in rural areas which enables them to have strong pricing power.

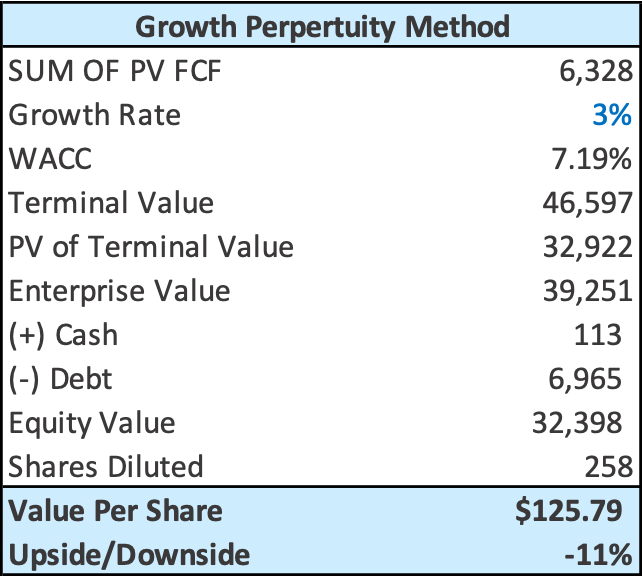

Valuation

I used the discounted cash flow analysis to value WCN. My fair value of the company is $124 per share, which equates to a 12% downside from the current price. I project revenue to increase by 8.60% annually for the next five years. My main revenue drivers are pricing power and market growth.

In its recent guidance, the company revised its adjusted EBITDA by $25 million to $2,525 million and its margin by +40 bps to 31.5%. They expect to finish the year at 32.5%, with the potential for more expansion in 2024. The company said that it could have exited at 33% if commodity prices normalized. This was said in the press release .

we look forward to driving outsized margin expansion in the second half of 2023 and into 2024."

In my model, I have gross margins expanding by 140 bps from 2023 to 2027. This assumption is attributed to commodity prices normalizing and pricing growth. My calculated WACC was 7.22%; I used that to discount the future cash flows, which amounted to $6.4 billion, and the terminal value. I arrived at an equity value of $32.7 billion. I used a 3% terminal growth rate aligned with the GDP. I project CapEx spending to average 12% of revenue from 2023 to 2027. This projection is based on a historical averages.

{kind=link}

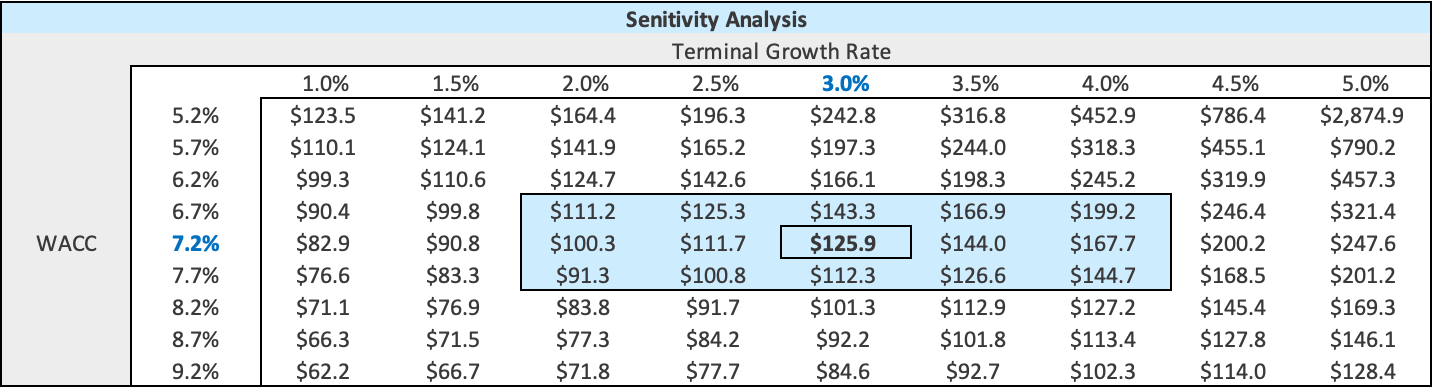

In one of my last article, a reader pointed out that it would be better if I provided a sensitivity table in my valuation, So I will start doing that from now on. Below is a sensitivity table that shows how a different growth rate and WACC can impact the share price.

{kind=link}

Risks

1) Competition is a risk that will probably keep haunting WCN for years or even decades to come. Companies such as WM and RSG are both larger than WCN. Competing with such firms can make it harder for the firm to acquire other companies and win contracts.

2) WCN is also a big spender on acquisitions. So far most of the acquisitions have been sound, but if miscalculations were to happen in the future such as overpaying, it could hurt shareholder value and the business. Plus the current high interest rates make it more difficult for M&A.

3) Regulation can serve as a double-edged sword for WCN. Just as regulations protect them from newcomers, it can also hurt them if new laws are passed to shut down landfills in certain areas in which WCN operates or maybe they increase taxes on landfill ownership.

4) Volatile commodity prices can make life hard for the company's margins. In the last earnings call the company highlighted that it would have improved margins if it weren't for high commodity prices.

Conclusion

The bottom line is that WCN is a high-quality business that I believe to be resilient, has strong demand, very little risk, and is underpinned by multiple competitive advantages. I believe the company's strategy to focus on secondary and rural markets has helped minimize competition and develop strong pricing power. This pricing power has helped the firm have better margins than its two biggest peers, Waste Management and Republic Services. My valuation suggests that the company is currently trading at a fair valuation. However, I will be keeping an eye on the company. If the stock price drops in the near future and nothing bad happens to the business, I may change my rating.

For further details see:

Waste Connections Stock: Highly Attractive Business But Not So Much For The Valuation