WM - Waste Management: Renewable Energy And Recycling Investments Look Promising But Valuation Poses Risks

2023-10-24 04:29:35 ET

Summary

- WM is investing in renewable energy and recycling to achieve $4 billion in free cash flow by 2027.

- WM is capitalizing on RNG demand, diversifying sales, and targeting $500 million in EBITDA by 2026.

- WM's recycling strategy targets growth, efficiency, and $240 million in EBITDA by 2026.

- WM's potential stock price CAGR is 11.5% over the next 5 years, but multiple compression is a risk.

Investment Thesis

Waste Management ( WM ) stock is a hold. Waste Management is investing in renewable energy and recycling to reach $4 billion in free cash flow by 2027. Responding to demand for Renewable Natural Gas, WM is diversifying sales and aiming for an EBITDA of $500 million by 2026. At the same time, their recycling plans aim for $240 million EBITDA by 2026. As WM moves into the renewable sector, its stock shows potential. The expected Compound Annual Growth Rate for the stock is 11.5% over the next five years. Yet, there's a risk of multiple compression which could affect returns, highlighting the importance of a cautious investment approach.

Company Overview

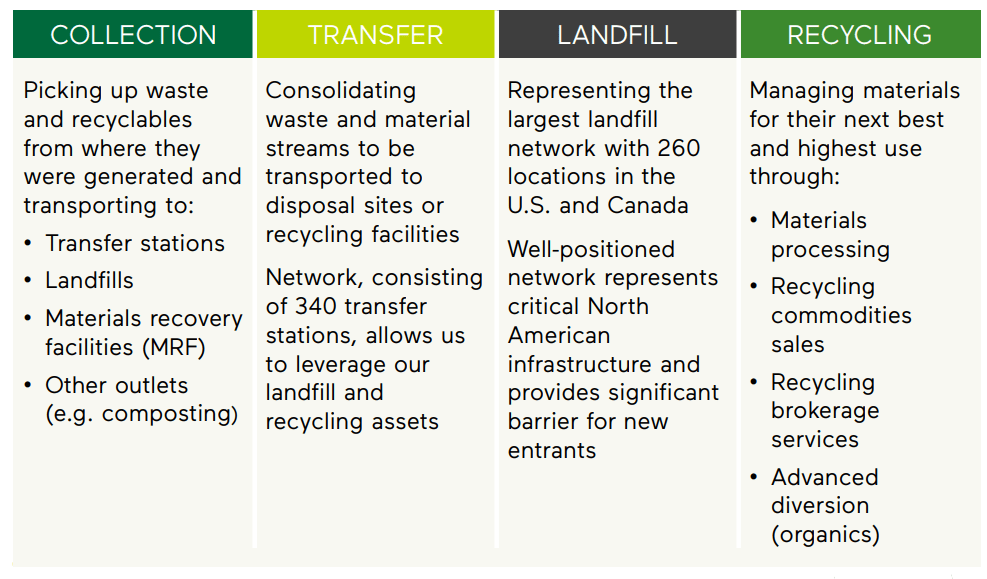

Waste Management provides environmental solutions services in North America, serving over 21 million customers in the U.S. and Canada. The structure of the company is divided into various business segments being Solid Waste, which deals with collection, transfer, disposal, and recycling services; Hazardous Waste, dedicated to managing and treating toxic materials; Environmental and Maintenance Services, which focus on a myriad of remediation and other service operations; and Recycling Operations, emphasizing the processing and selling of recyclable materials.

{kind=link}

Waste Management Investor Day 2022

In the competitive landscape, Waste Management faces competition from other players in the sector such as Republic Services ( RSG )??, Waste Connections ( WCN )??, and Advanced Disposal Services ( ADSW ). These companies, along with Waste Management, contribute to the competitive dynamics of the waste management and environmental solutions industry in North America.

Sustainability Growth Investment Program

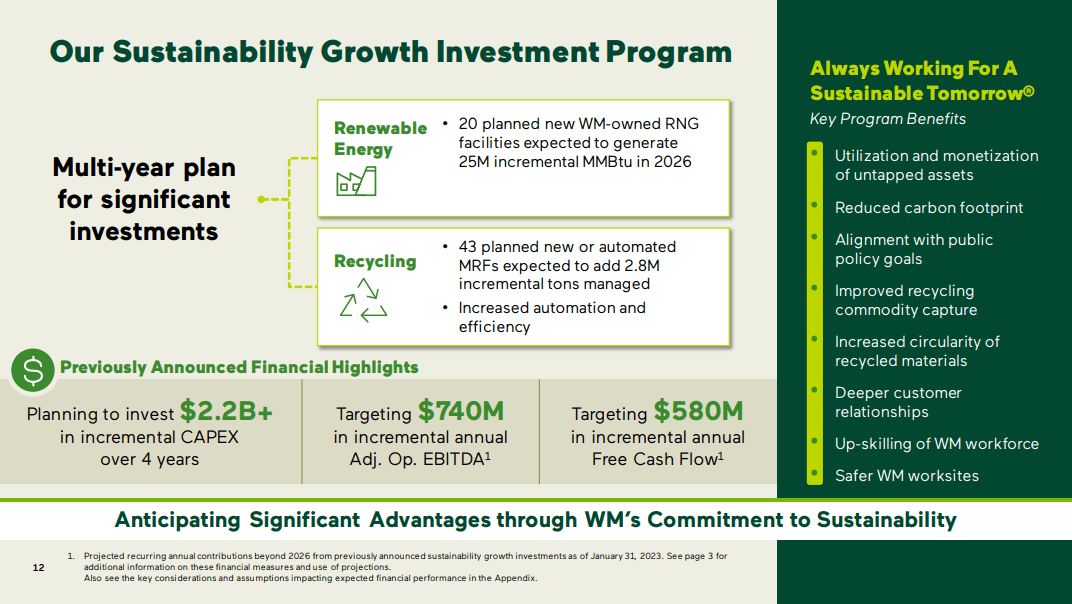

In my opinion, Waste Management is taking a significant step with its Sustainability Growth Investment Program . They are focusing on Renewable Energy and Recycling over several years. By 2026, WM plans to operate 20 new RNG facilities, aiming to produce an added 25M MMBtu. They're also looking to introduce or automate 43 MRFs, which, I believe, will handle about 2.8 million tons more material. A big part of this strategy seems to be about increasing automation in their facilities. On the financial side, it seems that WM plans to spend around $2.2 billion in CAPEX over four years. In return, they expect an annual adjusted EBITDA of $740 million and an annual free cash flow of $580 million. To me, the main goal appears to be making the most of available resources, reducing environmental impact, building customer relationships, and ensuring safety at work sites.

{kind=link}

Waste Management Investor Day 2023

RNG Opportunity for Waste Management

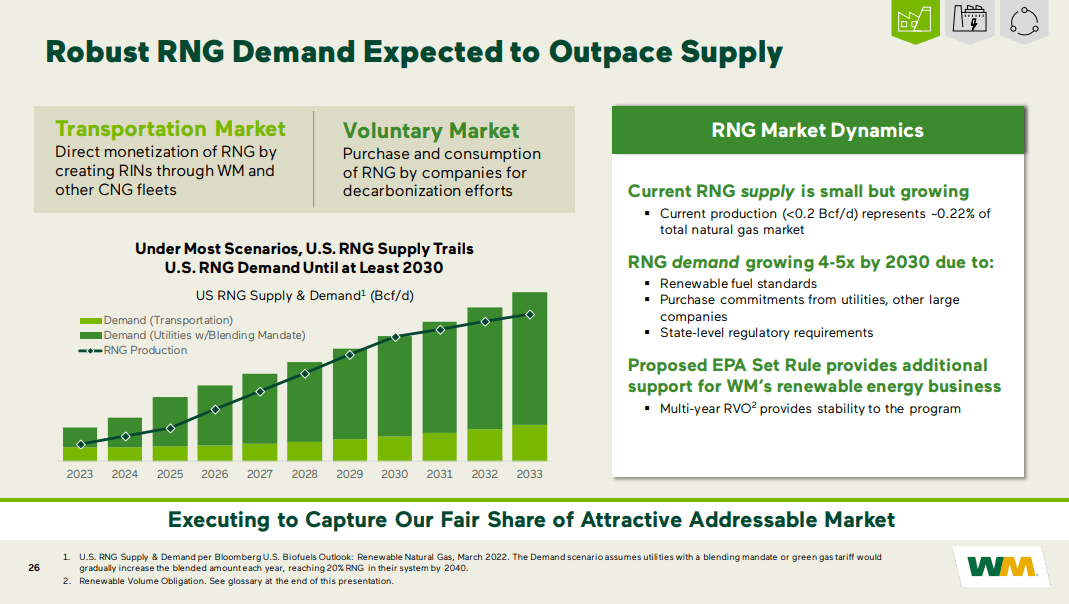

I believe Waste Management is strategically positioning itself within the Renewable Natural Gas ((RNG)) market. The data implies that, until 2030, there's a likelihood that RNG demand might surpass supply. This presents a valuable opportunity for WM.

{kind=link}

Waste Management Investor Day 2023

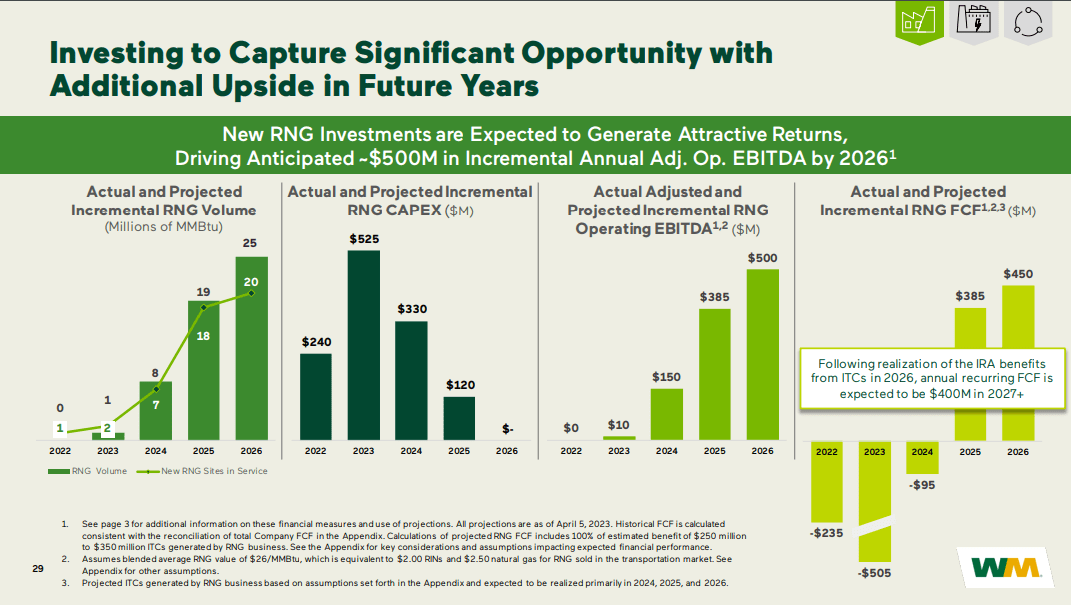

By 2026, WM has plans to operate 24 RNG facilities, aiming to elevate their RNG capture from 120 MMBtu in 2021 to about 135 MMBtu. Furthermore, WM is making efforts to ensure RNG is available for beneficial use, actively collaborating with third-party facilities, and extending their supply to industrial customers. WM also emphasizes a balanced approach to risk by engaging with reliable buyers in both voluntary and transportation markets, diversifying their buyer base, and adopting varied contract lengths. Pricing strategies combine fixed and indexed pricing for RINs and RNG, alongside leveraging a "dollar cost averaging" method. Notably, WM aims to stabilize earnings by executing forward, fixed-price sales across a rolling 36-month period. This strategic method seeks to lessen earnings volatility, enhancing the value as RNG's significance in WM's overall earnings grows.

Financially, the projections are promising, with an expected operating EBITDA of $500 million and a free cash flow ((FCF)) of $450 million in 2026. In my view, the RNG market is not just a potential avenue for financial growth for WM, but it also resonates with their environmental sustainability objectives.

{kind=link}

Waste Management Investor Day 2023

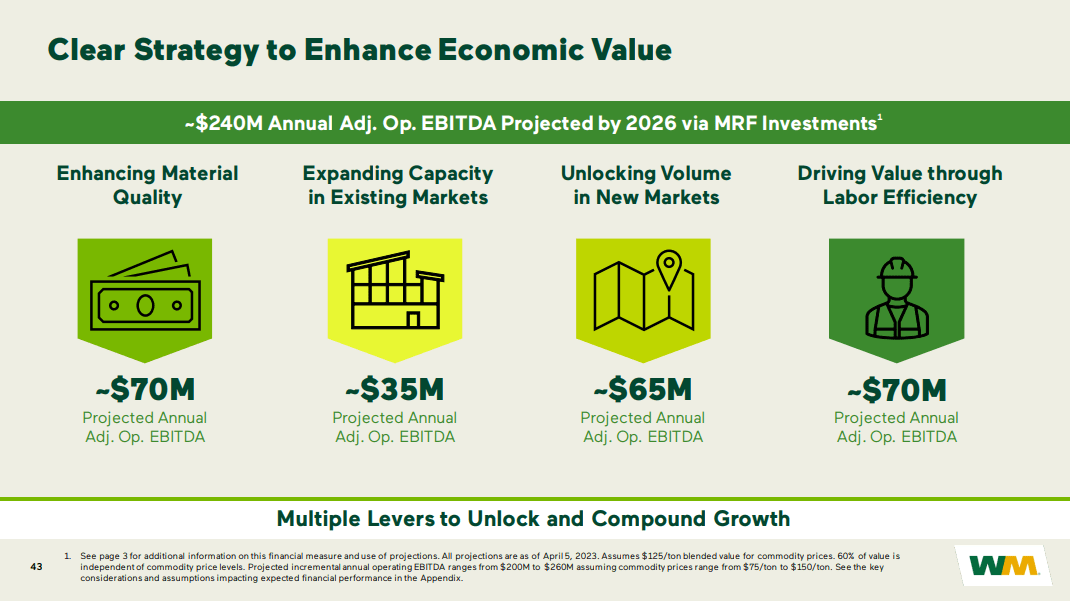

Recycling Opportunity for Waste Management

WM's recycling investments present a clear strategy for future growth and efficiency. The data indicates a significant emphasis on labor efficiency, with projected annual adjusted operational EBITDA increasing by $70 million by 2026. This is further complemented by the benefits of automation, which show a 30% improvement in labor costs per ton for 2022 and a 43% boost in safety, evidenced by the decrease in the total reported incident rate.

{kind=link}

Waste Management Investor Day 2023

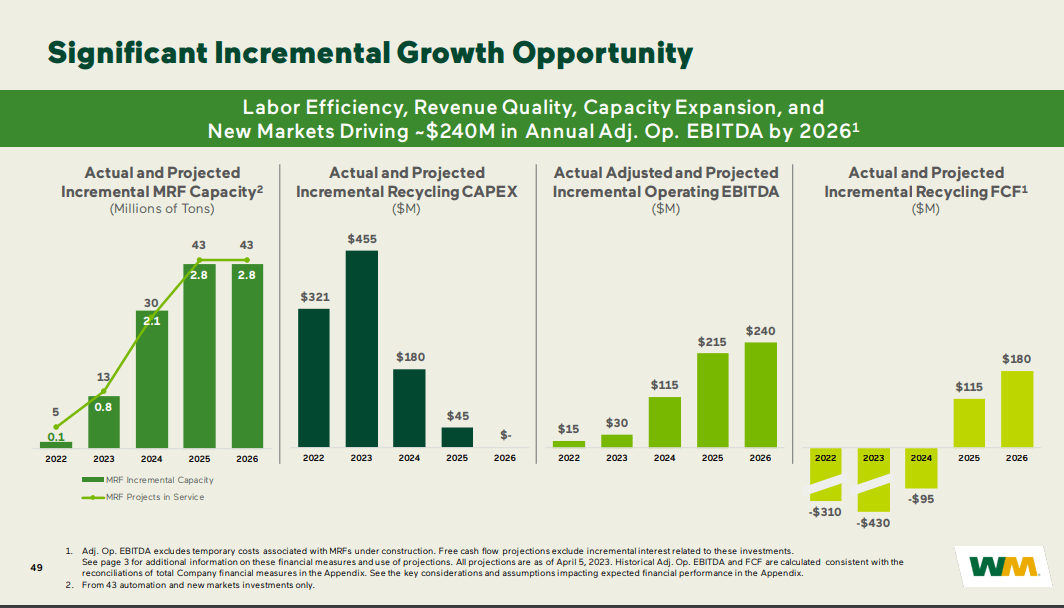

In addition, WM projects substantial growth in recycling, anticipating about $240 million in annual adjusted operational EBITDA by 2026. These projections span various strategies, including improving material quality, expanding capacity in current markets, and tapping into new markets. Notably, WM also forecasts $180 million in recycling FCF by 2026. In my opinion, by strategically distributing their investments across these domains, WM is positioning itself for robust growth in the coming years. The emphasis on enhancing operations and increasing automation further signals WM's commitment to both economic value and sustainability.

{kind=link}

Waste Management Investor Day 2023

Financial Analysis

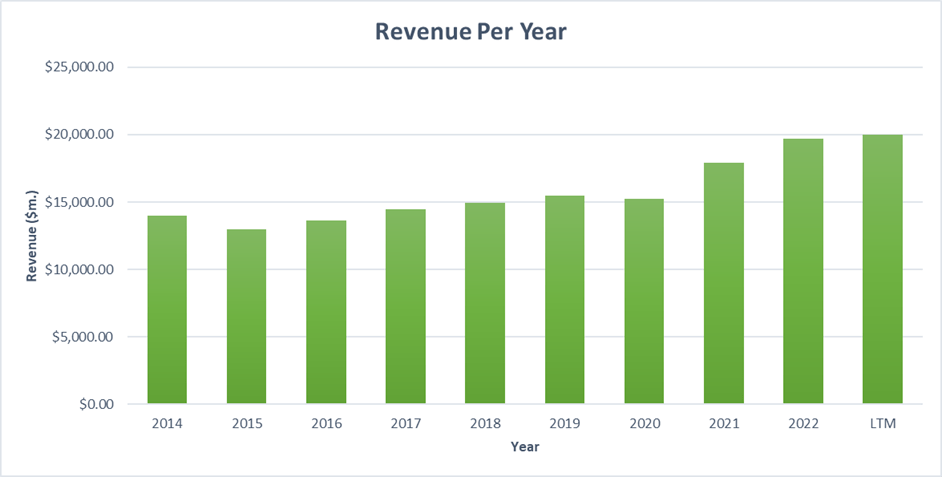

As of 2023, Waste Management has shown solid and consistent financial performance. In my opinion, the rise in revenue from $14,914.00 million in 2018 to $20,021.00 million over the past year is noteworthy. This corresponds to a CAGR of 6% over the previous 5 years.

{kind=link}

Author

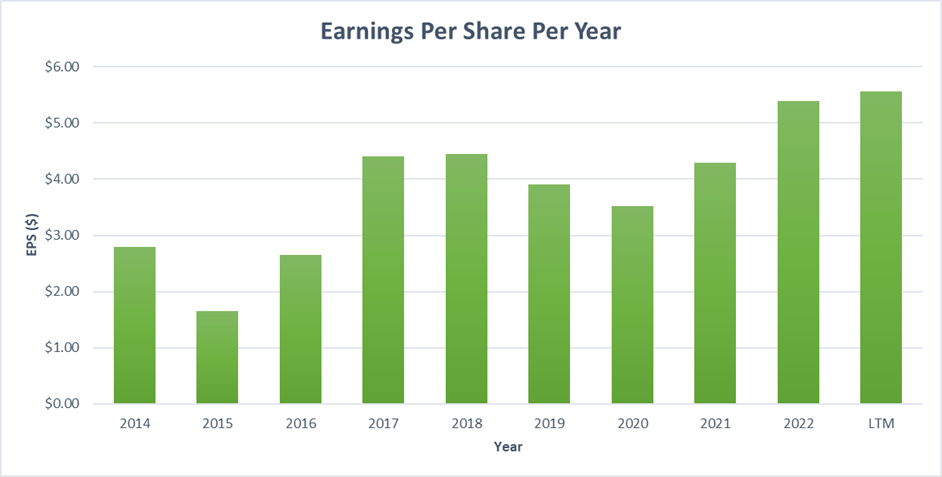

The Earnings Per Share ((EPS)) has been growing steadily, going from $4.45 in 2018 to $5.56 in the last twelve months, this is a CAGR of 5%. The management team has shown financial responsibility, especially in their approach to managing debt. The company's total debt net of cash and cash equivalents is $14,000 million, which on the surface may seem high compared to their LTM net income of $2,286 million it is important to consider that WM should be able to expand their margins over the next few years as a result of automation and the completion of sustainably investments. As it stands it will take approximately 6 years’ worth of net income to pay off the total long-term debt. Given the recurring revenue nature of this business, I believe this level of debt is manageable.

{kind=link}

Author

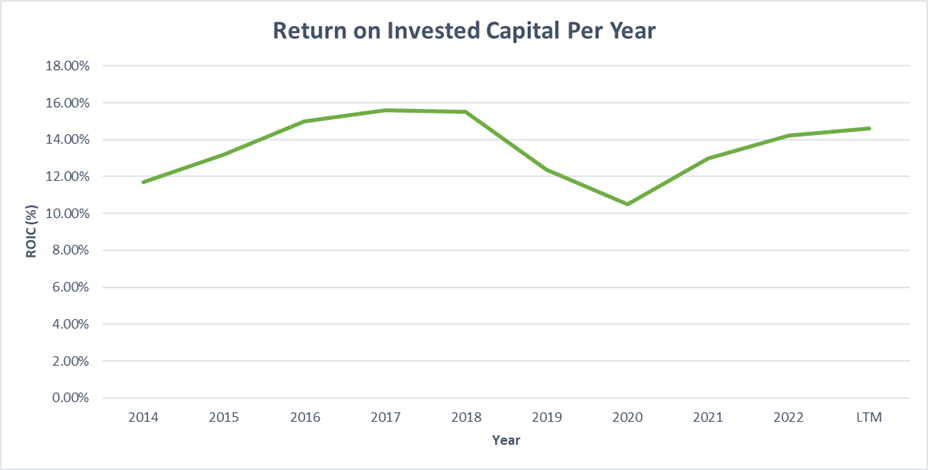

Waste Management's Return on Invested Capital has remained above 10% for the past decade, showcasing resilience even during the pandemic. With a 10-year average of approximately 13%, it's evident that the management is adept at reinvesting into the business, thus delivering substantial returns to shareholders.

{kind=link}

Author

Overall, I'm optimistic about Waste Management's growth prospects, particularly given their push towards automation, capacity expansion in existing markets, expansion into new markets, the recession resistant business model and the growth investments into renewable energy and recycling, I am confident that the business can reach their long-term target of achieving $3.8 to $4.2 billion in free cash flow by the end of 2027.

Valuation

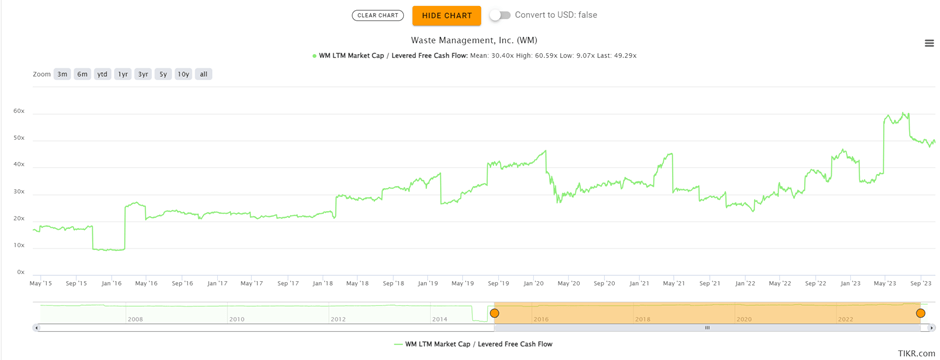

Based on WM’s long-term target of achieving $3.8 to $4.2 billion in free cash flow by the end of 2027. Since May of 2015, WM has traded at a price to free cash flow ratio of anywhere between 9.07 and 60.59, with a mean of 30.40. In my opinion, a mean price to free cash flow ratio of 30.40 is quite high and would be risky to use in the valuation. While I acknowledge that WM is a high-quality business with recurring revenue and prospects for sustainable growth, I believe it is prudent to use a price to free cash flow ratio of 25 or below for this business to manage risk.

{kind=link}

Tikr Terminal

If we assume a price to free cash flow ratio of 25 at the end of 2027, and assume WM reach the mid-point of their 2027 free cash flow guidance of $4 billion, this will result in a market capitalization of $100 billion ($4 billion in free cash flow multiplied by a price to free cash flow ratio of 25 equals a market cap of $100 billion). I believe the assumption of $4 billion in free cash flow, is likely due to the investments into renewable energy and recycling as discussed earlier in the article. Given that the current market capitalization is $63 billion, this would result in a CAGR of the expected Compound Annual Growth Rate would be 11.5% over the next four years and three months, based on these calculations (a market cap of $63 billion which grows to $100 billion over a period of 4 years and 3 months results in a 11.5% CAGR). I arrive at a market capitalization of $100 billion due to the expected $4 billion in free cash flow by 2027, as a result of free cash flow growth from the areas of renewable energy and recycling, and when you account for a price to free cash flow ratio of 25 based off would I believe is reasonable for WM, I arrive at a $100 billion market cap in 2027. While, this may seem attractive, I believe multiple compression is a risk if we were to enter a prolonged economic downturn or a recession. For instance, in a recessionary period, it would be likely for the price to free cash flow multiple to drop to 20, hence this would result in a market cap of $80 billion resulting in a CAGR of less than 6% and if the multiple was to fall to 15, this would result in a negative return on investment at the current share price.

Conclusion

Waste Management is making strategic investments in renewable energy and recycling with a clear vision to achieve $4 billion in free cash flow by 2027. Recognizing the rising demand for Renewable Natural Gas, WM is actively diversifying its sales and formulating strategies to target an impressive EBITDA of $500M by 2026. Parallelly, their recycling initiatives are intricately designed to ensure growth and efficiency, with a projection to reach $240M EBITDA within the same timeframe. As WM shapes its future in the renewable sector, its stock offers potential promise. The anticipated Compound Annual Growth Rate for the stock price is 11.5% over the next half-decade. However, investors should be circumspect as there is an inherent risk of multiple compression. This could significantly impact returns, emphasizing the need for a balanced and well-informed investment approach.

For further details see:

Waste Management: Renewable Energy And Recycling Investments Look Promising But Valuation Poses Risks