WDH - Waterdrop: Turnaround Story Supported By An Outsized Net Cash Balance

Summary

- The Waterdrop turnaround is taking shape.

- In addition to its P&L strength, the growing net cash position provides downside protection.

- There are regulatory risks here, but the cheap valuation makes the overall risk/reward very compelling.

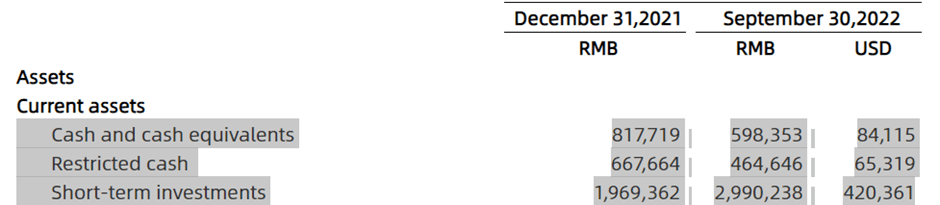

Integrated Chinese insurtech platform Waterdrop ( WDH ) continues to enjoy strong brand recognition through its medical crowdfunding and insurance marketplace platforms, delivering another strong beat-and-raise quarter in Q3. Beyond the P&L improvement, WDH’s growing cash position has largely been ignored by the market and now stands at ~RMB3.6bn (>RMB4bn, including restricted cash), providing ample valuation support. While the stock has rallied in the last month or so, the cash balance remains >50% of the market cap despite WDH remaining on track to generate cash through the coming years. Further traction in the multi-year pivot toward long-term policy sales will be a key catalyst – as of Q3, first-year premiums here have already grown in the high-single-digits % QoQ. As WDH continues to prove the viability of its strategic pivot and FCF generation potential, I see a clear path to the stock re-rating much higher.

Lots of Positives from the Beat-and-Raise Quarter

As the QoQ growth in first-year premiums showed in Q3, sales are likely moving higher despite the on/off COVID lockdowns during the period. Of note, the balance of non-current contract assets was up again by >RMB20m (a similar pace to Q1 and Q2), pointing toward further momentum in the sales of long-term policies. I expect the FY22 disclosures next year to support this view. The key uncertainty heading into Q4 will be the impact of lockdown measures through late November, as well as the impact of the latest COVID wave after restrictions were lifted in China. Given the traction in recent quarters through the lockdowns, I suspect premium growth will continue to improve, reinforcing the case for a sustained top-line turnaround.

{kind=link}

Also impressive is that WDH’s revenue strength has come without sacrificing profitability. Q3 saw a net profit of RMB170m, which was down QoQ, but broadly in line with prior quarters’ results, excluding the impact of tax credits. A key reason for the well-controlled cost base has been WDH’s plan to focus on existing user conversion over more expensive external customer acquisition. With the success of this growth strategy clearly being reflected in the P&L, the upward revision to the FY22 guidance seems prudent. The extent of the revision points to some conservatism, though – given the YTD net profit is already at ~RMB480m, WDH should easily clear the FY22 net profit target of RMB500m, paving the way for another beat-and-raise quarter ahead.

Long-Term Strategic Pivot on Track

Amid the higher competitive intensity, WDH has protected margins by transitioning away from expensive customer acquisition through third-party channels. Instead, it is now focused on converting existing non-paying users to paying insurance customers. As seen in the Q3 results, this strategy has already driven significant opex savings, allowing for consecutive quarters of net profits for the first time in its history as a listed company. The profits have been translating into cash flow as well, driving a sizeable net cash position.

{kind=link}

In reaction to the tighter regulatory backdrop on short-term products, management has also prudently transitioned its product mix toward long-term insurance products. The regulatory focus on increasing insurance affordability has already resulted in a 35% commission cap on short-term insurance products, along with the implementation of a >50% claim ratio requirement for accident insurance. Given WDH’s outsized exposure to short-term medical product commissions, diversifying away from this revenue stream makes sense. Early signs have been positive, but given this is a 3–5-year goal, progress here will be worth monitoring, as well as any further tightening on industry regulation.

Insulating Against Regulation

As with all investments in China, regulatory developments are key. While the China Banking and Insurance Regulatory Commission (CBIRC) has not signaled any new policy implementations for now, the government’s increasingly populist rhetoric is a concern. In recent weeks, for instance, the Beijing Medical Security Bureau announced the cancellation of the upper limit of outpatient reimbursement for employees in the region from 2023. Post-implementation, this means the reimbursement ratio for expenses over RMB20k will now be ~60% for current employees and ~80% for retirees.

While bears will point to the developments in Beijing as a negative sign of things to come, WDH’s competitive positioning in lower-tier cities and with a younger, tech-savvy customer base gives it some leeway. The platform also tends to serve people with existing health conditions via short-term medical insurance, an underserved segment with limited overlap with traditional insurers. Importantly, WDH’s role in serving segments that traditional insurers do not serve gives it more insulation against any adverse regulatory shifts. Plus, it allows for a more cooperative relationship with the big insurers, which WDH could leverage to alleviate competitive pressures from other tech platforms.

Turnaround Story Supported by an Outsized Net Cash Balance

The recent quarterly outperformance offers yet another confirmation of the WDH turnaround strategy as it looks to further monetize its internal user base and pivot toward a greater mix of long-term policy sales. Betting on turnarounds is usually risky, but the risk-reward is particularly attractive here, given the large cash balance (including short-term investments). The current net cash position makes up >50% of the market cap and is on track to continue growing from here, providing ample downside support. Key catalysts include further traction in premium growth and long-term policy sales; as WDH continues to prove the viability of its turnaround, expect the stock to re-rate accordingly.

For further details see:

Waterdrop: Turnaround Story Supported By An Outsized Net Cash Balance