WAT - Waters Corporation: High Quality Niche Company In Mass Spectrometry

2023-12-28 13:25:53 ET

Summary

- Waters is a niche player in the liquid chromatography, mass spectrometry, and thermal analysis markets, with a simple and profitable business model.

- The company's focus on product innovation and acquisitions contributes to its growth and competitive advantage.

- However, Waters faces headwinds in the Chinese market, which may impact its growth in the near term.

Waters ( WAT ) is the market innovator for liquid chromatography, mass spectrometry, and thermal analysis products. They serve the pharmaceutical, industrial, and Academic & Government end-markets. Although their exposure to the Chinese market presents a notable growth headwind for the company in the near term, it is a highly profitable and niche player. I recommend a 'Buy' rating with a fair value of $350 per share.

Niche and Simple Business Model

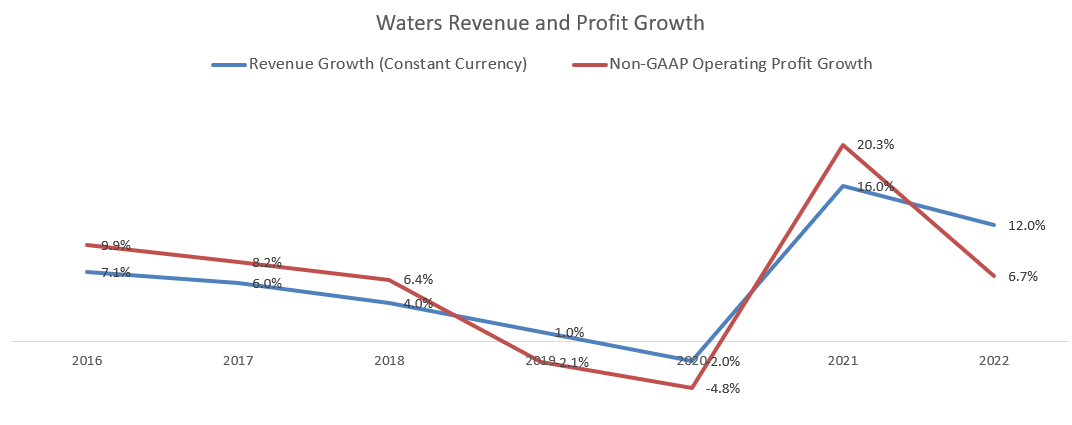

Waters has been offering liquid chromatography, mass spectrometry, and thermal analysis products for decades, and their business model is both simple and unique: they sell equipment and provide services to their customers. With a global installed base exceeding 150,000 units, the replacement cycle is a key driver of their revenue growth. Additionally, they are actively launching new products and gaining market share to fuel further expansion. Prior to the COVID-19 pandemic, their top-line and bottom-line growth consistently reached high-single digits.

{kind=link}

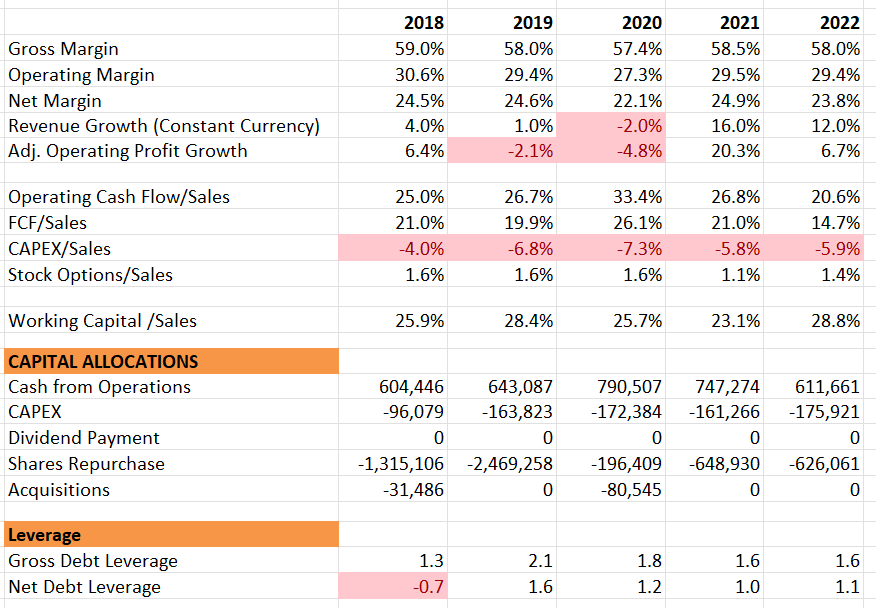

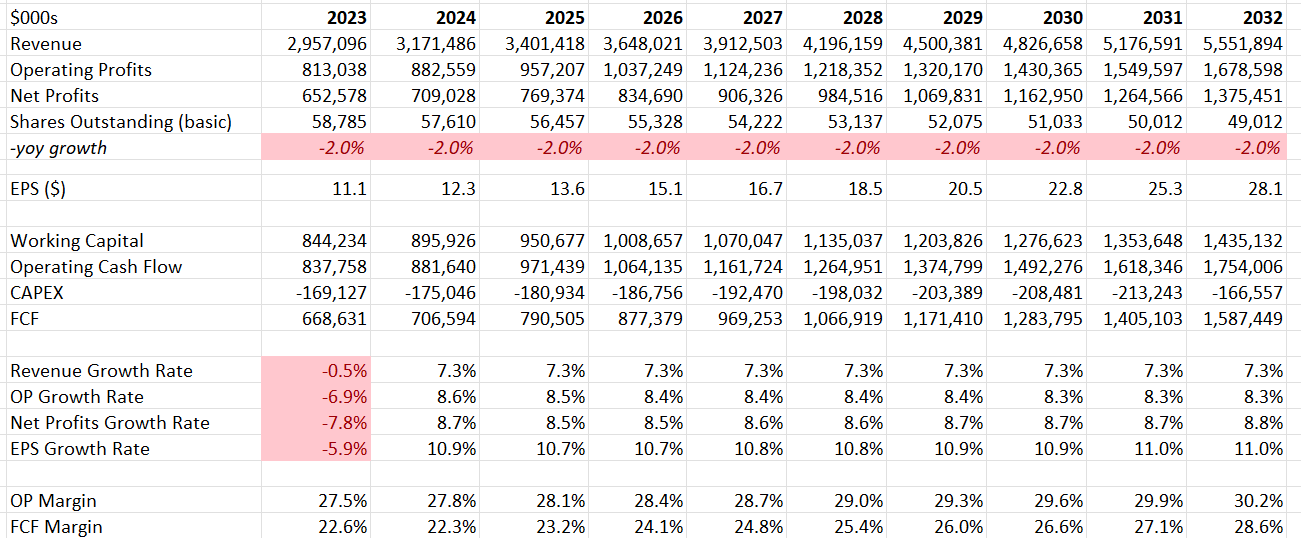

Due to their specialization, they earn high margins, with an adjusted operating margin exceeding 30%. The table below provides an overview of their historical financials. Notably, their free cash flow margin is substantial, surpassing 20%, and a significant portion of their cash from operations is allocated to share repurchases. Additionally, their balance sheet is robust, boasting a net debt leverage of only 1.1x.

{kind=link}

Their products compete with Agilent (A), Danaher (DHR), and Thermo Fisher (TMO), with Waters being the sole pure player in this market. I believe their business is inherently recurring for the following reasons.

Firstly, mass spectrometry and liquid chromatography-mass spectrometry are essential tools used to identify unknown compounds, quantify known materials, and elucidate the structural and chemical properties of molecules. They play a mission-critical role in pharmaceutical and industrial markets, particularly in drug discovery and development, as well as environmental, clinical, and nutritional safety testing. Given the crucial functionality, customers in the pharmaceutical and industrial sectors are reluctant to purchase low-quality and inexpensive mass spectrometry products.

Secondly, once customers have selected a specific mass spectrometry product, they are unlikely to switch to another brand due to the need for consistency in testing results.

Lastly, services account for over 33% of total revenue, and the service business is more sticky and recurring than equipment sales.

Product Innovation and Acquisition

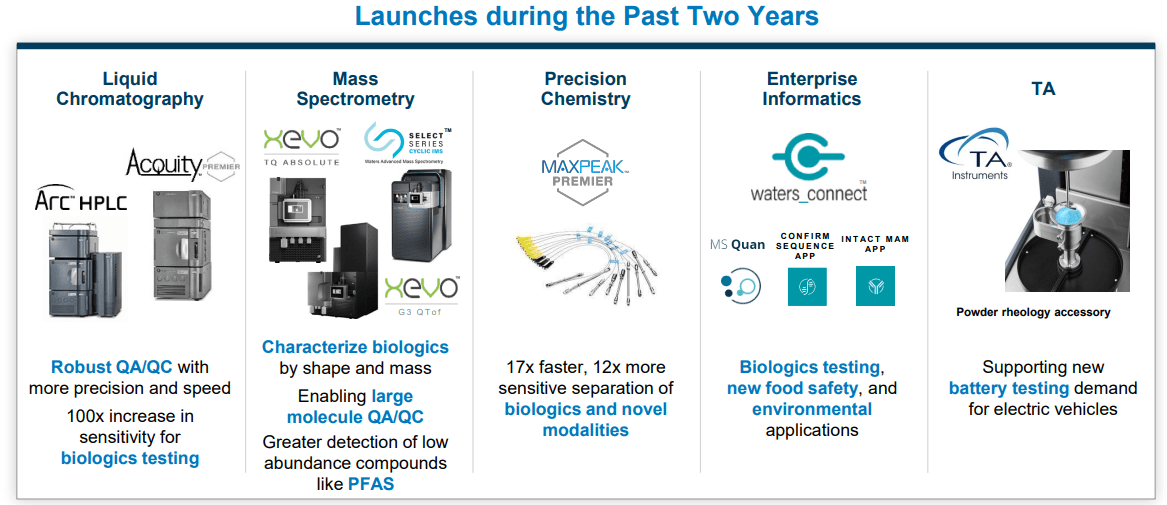

To sustain their competitive advantage, Waters must continue to prioritize innovation in new products. They allocate 7% of their revenue to R&Ds, a figure slightly higher than their peers' average of 6%. In 2023, they successfully launched crucial new products, such as the next-generation Alliance is high-performance liquid chromatography system.

{kind=link}

I believe that their commitment to new product innovation is pivotal for future growth. These innovations are centered around their core technology and contribute to the expansion of their service offerings. With these new products, the sales team can capitalize on their existing customer base, facilitating cross-selling of multiple products and services. Moreover, these innovations empower Waters to broaden their gross margin. While raising prices on existing products might be challenging, the introduction of new products allows for a starting point with higher prices and improved margins.

M&A serves as a crucial vehicle for their new product innovation strategy. In 2023, Waters made a significant move by acquiring Wyatt Technology , a pioneer in laser light scattering, for $1.36 billion. Wyatt, initially a family business, boasted approximately $110 million in revenue, experiencing a robust growth rate exceeding 20%. They were the first to commercialize on-line multi-angle laser light scattering instruments over 40 years ago. While the deal price appears high, I believe the acquisition of Wyatt holds substantial potential for contributing to Waters' future growth.

With its global footprint, Waters has the opportunity to expand Wyatt's business into other major regions, including Asia and Europe. Moreover, considering that Wyatt's primary end-market is the large-molecule pharmaceutical market, Waters can leverage its extensive sales force to effectively cross-sell Wyatt’s instruments.

China Exposure Creates Headwinds

At the beginning of this fiscal year, China represented approximately 20% of group revenue, and the region is anticipated to decline by 25% this year according to their guidance. Following this significant decrease, China is expected to account for around 12-13% of group revenue by the end of the year. The substantial decline in China poses considerable growth headwinds for Waters, affecting not only the pharmaceutical industry but also the industrial and academic end-markets. It appears that China's slow growth is inevitable and unlikely to reverse in the near term. Factors contributing to this slowdown include weak exports due to the global economy and subdued domestic consumption resulting from previous extensive COVID-19 lockdowns. It is speculated that several years may be required for China to experience a genuine economic recovery, indicating that Waters will likely continue to face growth challenges in this important region.

Recent Results and Outlook

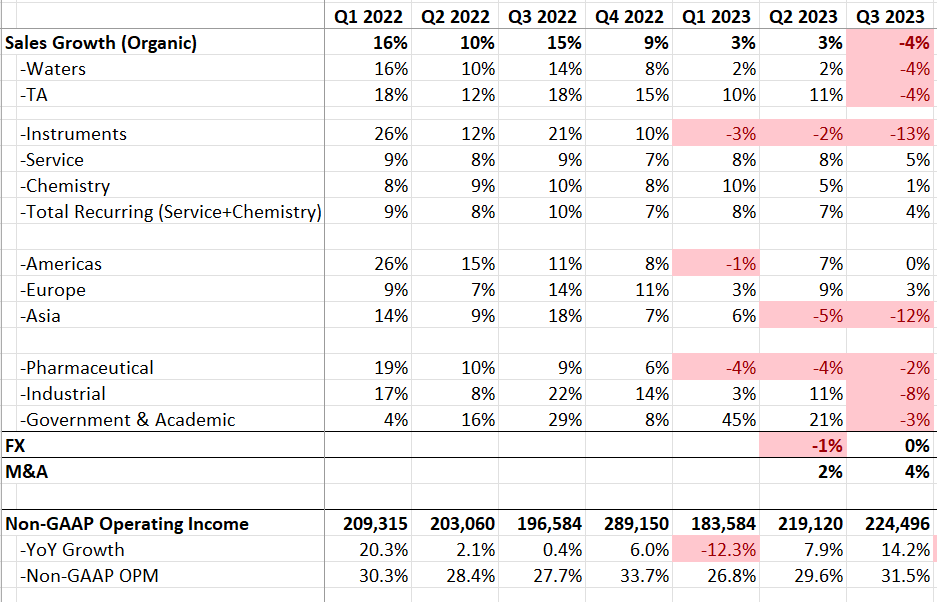

During Q3 FY23 , Waters reported a -4% organic revenue growth, primarily attributed to the sluggish economic conditions in China. However, the acquisition of Wyatt contributed positively, adding 4% to overall sales with robust growth. The adjusted EPS increased by 8% year over year, propelled by a notable 380 basis points operating margin expansion.

{kind=link}

As for the full-year guidance, they anticipate organic revenue growth in the range of -2% to -1% and non-GAAP EPS to be within $11.65 to $11.75. The upcoming Q4 FY23 results may not hold any surprises, as the company has already factored in the impact of weak China growth, projecting a further decline in the region. The market's sensitivity is likely to shift towards their FY24 guidance. With a full-year decline expected in their China operations, the FY24 guidance may exhibit less downside risk. By the end of the next quarter, China's business would constitute just above 11% of group sales. Even if China continues to decline by another 10%, it would only cause a 1% growth headwind for the group. Waters is proactively managing costs and implementing price increases. Their unique product proposition allows them to raise product and service prices with minimal pushback from customers. As mentioned by their management in the earnings call, Waters typically achieves 50-75 basis points of price growth each year. These pricing and cost management initiatives position Waters to guide a robust margin expansion in FY24.

Valuation

The assumptions for FY23 align with the company’s guidance, suggesting a notably weak year-over-year growth in China. For normalized revenue growth, the model assumes 6% of organic revenue growth and 1.3% of acquisition growth. These growth assumptions mirror the company's historical average, comprising around 5.3% volume growth and 0.7% price growth.

{kind=link}

Waters possesses the capability to enhance its margin over time, with primary drivers including new product launches, pricing increases, cost reduction initiatives, and operating leverage. The model employs a 10% discount rate, a 4% terminal growth rate, and a 15.5% tax rate. The calculated fair value is $350 per share.

Key Risks

Industrial Market : Waters has approximately 30% of total revenue exposure in the industrial market. Historically, the industrial market has shown more volatility compared to their pharmaceutical end-market. The business grew by 1% in FY18, declined by -2% in FY19, and further decreased by -3% in FY20. Notably, segments such as material characterization, food, environmental, and chemical markets contribute to the increased cyclicality in Waters’s performance.

Competition From Big Players : Among competitors, Danaher and Thermo Fisher emerge as formidable players in the pharmaceutical end-market. Boasting robust balance sheets and extensive acquisition experience within their focused market and technology domains, Danaher and Thermo Fisher stand out as industry leaders. In contrast, Waters positions itself as a smaller niche player. Consequently, Waters must persist in investing in research and development to continually launch innovative products, a crucial strategy for maintaining its competitive edge against these industry giants.

Conclusion

Waters is a unique and niche player in the markets of liquid chromatography, mass spectrometry, and thermal analysis. I assign a 'Buy' rating with a fair value of $350 per share.

For further details see:

Waters Corporation: High Quality Niche Company In Mass Spectrometry