WDFC - WD-40 Company: Driving Future Growth Through Premiumization E-Commerce And Volume Recovery

2023-11-29 06:46:26 ET

Summary

- Strong recovery in sales volume from 1H23's decline caused by announcement in price increase demonstrates a continuing strong demand.

- WDFC's strategic initiatives, including product premiumization and e-commerce, are expected to drive future growth and margin expansion.

- 2024's guided net sales are expected to grow at 2 -3X of 2023's reported growth rate.

- Relative to its peers under household brand category, it has outperformed in context of margin and growth outlook.

Editor's note: Seeking Alpha is proud to welcome RL Insights as a new contributor. It's easy to become a Seeking Alpha contributor and earn money for your best investment ideas. Active contributors also get free access to SA Premium. Click here to find out more »

Synopsis

In this post, I will discuss my analysis, views, and recommendations for WD-40 Company (WDFC), a proud American manufacturer of household and multi-purpose products, primarily known for its signature blue-yellow penetrating oil product, WD-40. WDFC's historical performance has shown its strong ability to protect and maintain its net margins despite fluctuating revenues, and this is a testament to its expense management ability.

For its 4Q23 results, it shows robustness and strength as net sales grew and gross margin expanded due to higher pricing and a strong recovery in its sale volume, which was negatively impacted when they introduced price increases last year. This strong recovery in volume demonstrates its products' strong branding. With higher pricing and a strong recovery in volume, it is expected to bolster its growth outlook.

In addition to pricing and volume recovery, its product premiumization and e-commerce strategic initiatives are expected to further bolster its growth outlook. In 2024, net sales are expected to grow by 6 to 12%, more than double the 2023 reported results. With these factors, I am recommending a buy rating for WDFC.

An In-Depth Look At WD-40 Company And Its Financial History

WDFC is an American company that produces and sells household products, which includes it most popular brand, the WD-40 penetrating oil. In addition to WD-40, it also sells a diverse range of products, such as 3 in 1, X-14, and many more. It sells its products in multiple locations across the globe, such as the Americas, EMEA, and Asia-Pacific.

From 2020 to 2023, WDFC's revenue year-on-year growth is quite evidently cyclical in nature. In 2020, due to the COVID-19 pandemic, revenue suffered and reported a decline of 3.51%. In 2021, when COVID-19 started to settle down and economies were recovering, it reported a robust growth of 19.49%. In 2022 and 2023, rising inflation negatively impacted WDFC again, it reported 6.29% and 3.55%, respectively.

Its 5 years revenue compound annual growth rate is ~4.8%. For 2024 and 2025, the market is expecting WDFC to grow above its 5 years CAGR, signaling the market's confidence in its growth outlook and strength. Although its revenue is full of peaks and troughs, its net income margin is remarkably consistent, and its 5 years' median is ~13%. This is clear evidence of robust and effective expense management. When revenue is declining, WDFC is able to respond to it effectively and keep its costs in line with revenue.

Author's Chart

Moving into its balance sheet, WDFC has kept its debt level relatively stable. Its 5 year's median debt/equity ratio is ~62%. For 2023, its debt/equity ratio is ~61%, in line with its historical average. As a result of its prudent debt management, it is able to keep its interest expense low. It only accounts for ~1% of its total revenue, hence supporting its stable net margins even when interest rates are rising. In terms of free cash flows, WDFC has been growing them consistently. In 2019, free cash flow per share was $3.59, and by 2022, it had grown to $6.74 per share, which represents a growth of ~87%.

Author's Chart

Making The Case For My Optimistic Outlook

WDFC reported robust 4Q23 financial results. Net sales reported were $140.5 million, 8% growth from 4Q22's $130.4 million. The growth in net sales was mainly driven by Americas and EMEA markets. In Americas, total segment sales grew 10% year-on-year, and it accounts for 53% of net sales. In EMEA, total segment sales grew 16% year-on-year, and it accounts for 36% of net sales. For both of these markets, the growth was mainly driven by the price increase implemented last year and strong demand recovery from the price increase impact. In addition, these two markets, which have strong growth of more than 10%, form the lion's share of WDFC's net sales, ~89% combined.

For its last segment, Asia Pacific, total segment sales declined 20% year-on-year, but it only accounts for 11% of net sales, hence, its overall impact has been offset by the strong growth seen in Americas and EMEA. The main driver for the 20% decline was due to the tough comparison period for the Asia pacific distributor market, not really a demand issue. In 2022, as the COVID-19 lockdown was lifted, it resulted in strong sales for 4Q22 due to pandemic induced demand, thus creating a tough comparison period. Moving forward, as Asia Pacific sales numbers start to normalize and create a better comparison period, I expect Asia Pacific to report better figures for the upcoming period.

In terms of gross margin, it improved to 51.4%, a 4% increase from 4Q22's 47.4%. The improvement was driven by WDFC's decision to increase the price of its products for all markets in 4Q22. In the first two quarters of 2023, volume and sales were negatively impacted by its decision to increase prices, which resulted in net sales decreasing by 7% year-on-year for 1Q23 and flat for 2Q23 . However, for the last 2 quarters of 2023, management has stated that volume has recovered, and this is evident in the 3Q23 and 4Q23 net sales growth of 15% and 8%, respectively. With the new higher pricing and recovery in its sales volume, I expect these two combinations to drive WDFC's revenue growth outlook upward. In addition, I expect its higher pricing to contribute positively to its gross margin. At its current 51.4%, I believe management's long-term target of 55% is well within reach.

WDFC Q4 FY23 Press Release WDFC Q4 FY23 Press Release

WDFC's Strategic Initiatives

I believe WDFC has positioned itself well to capitalize on its current higher pricing level and strong recovery in demand to drive its growth and margin outlook. One of the strategies it employed was premiumization, such as the introduction of WD-40 smart straw and EZ-Reach delivery system. These innovations have proved to be popular among users, which allows WDFC to charge a premium for its products.

In my opinion, I believe WDFC's premiumization effort is an effective way to boost its revenue and margins. With WDFC's smart straw and EZ-Reach delivery system, it is effectively selling the original product, but the innovation allows WDFC to charge consumers at a premium. As discussed above, pricing is important to WDFC as it drives revenue growth and margin expansion, as witnessed in the 4Q23 results. In addition, its premium products' last 5 years' net sales growth has been very robust, with a CAGR of 7.3%. Therefore, in 2024, I expect its premiumization efforts will continue to drive its growth outlook as well as margin expansion.

The next strategy employed by WDFC to capture growth is e-commerce. E-commerce is a very powerful tool, as it not only drives sales but also drives brand awareness, as digital advertisements also allow WDFC to showcase their products ease of use and effectiveness. This is evident in its 2023 e-commerce sales, which grew 35% year-on-year.

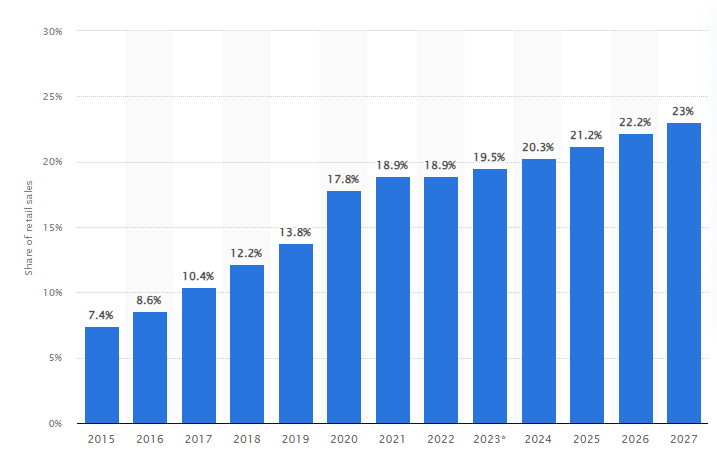

Global e-commerce sales, as a percentage of total sales, have been growing rapidly. In 2015, it only accounted for 7.4%, but by 2027, it is expected to account for about 23% of all sales. With the rapid growth of e-commerce, I believe WDFC's foray into e-commerce is an excellent strategic decision. Based on WDFC's e-commerce growth strength and the rapid global e-commerce growth outlook, I believe this strategic decision will contribute positively to WDFC's growth outlook.

{kind=link}

Revenue Guidance

With these strengths and tailwinds in mind, let's move on to the 2024 guidance. Management guided sales growth of 6-12%. This is in stark contrast to the 2023 growth of ~4%. In my opinion, this is extremely positive, and it shows management's confidence in WDFC's growth outlook. This optimism further bolstered my confidence in the strength of WDFC I discussed earlier.

In addition, 2024 gross margin is guided to 51% to 53% vs 2023's 51%, showing a potential improvement of 2%. In my opinion, WDFC's premiumization effort, which I have discussed above, is likely to be the main driver of its gross margin improvement. Overall, management's 2024 guidance is very strong, and it exudes management's confidence in WDFC's growth outlook.

{kind=link}

Comparative Analysis

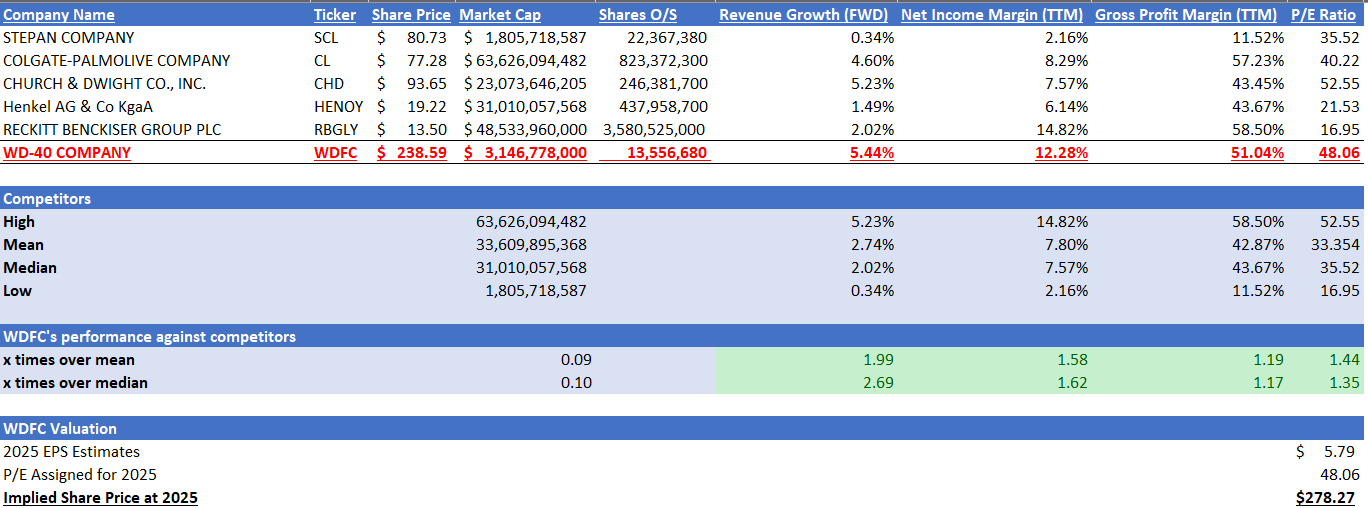

WDFC operates in the household products industry, and the competitors I have gathered in the table below are based on this, and I believe this group is a good representation of this industry. Due to the presence of outliers, median serves as a better representation than mean. Thus, I will be comparing WDFC against competitors' median.

Competitors' median market cap is ~$31 billion, while WDFC is ~$3.1 billion. Thus, in terms of company size, WDFC is only ~10% of its competitors. Despite its smaller size, WDFC outperforms its competitors in all areas. Its revenue growth FWD is 2.69x over competitors median, its net income margin TTM is 1.62x over competitors' median, and its net income is 1.17x over competitors median. Looking at my table, WDFC's P/E is 1.35x over competitors' median.

Given its superior financial performance and revenue growth outlook against its competitors, and its current P/E is in line with its 5-year average, my stance is that its current P/E given by the general market is fair.

Author's Multiple Valuation Table Seeking Alpha

{kind=link}

{kind=link}

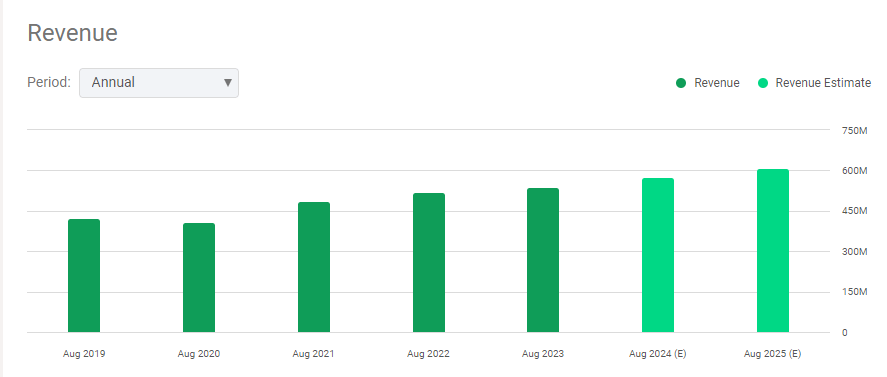

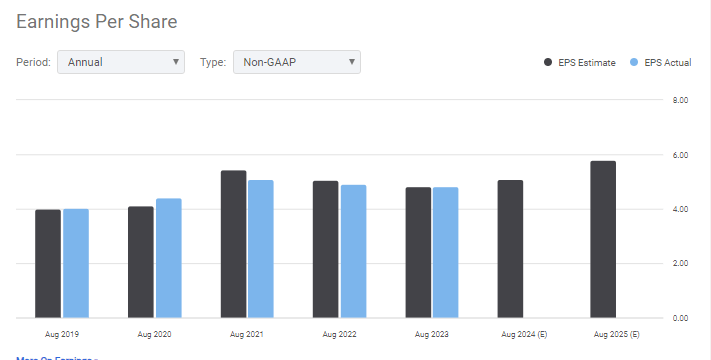

Market revenue estimate for WDFC is expected to reach $574.77 million in 2024 and $608.1 million in 2025. The market estimate for WDFC's 2025 EPS is $5.79. I believe these estimates to be reliable, as they are in line with management's guidance. In addition, my discussion on its strengths and growth catalysts above also supports this outlook. By applying its current P/E, which I have discussed above, to its 2025 EPS estimates, my 2025 price target is $278.27, and this represents an upside potential of ~16%.

Seeking Alpha Seeking Alpha Seeking Alpha

{kind=link}

{kind=link}

{kind=link}

The Risk Associated With WDFC

The first downside risk lies in WDFC's reliance on pricing and premiumization strategies to drive future growth. These growth strategies could backfire if consumers are sensitive to price increases, particularly in an economic downturn, or if competitors offer similar products at lower prices. In the current high inflation landscape, there is a higher possibility that consumers might switch to cheaper alternatives.

In addition, as WDFC's PE is trading at a premium when compared to competitors' medians, the premium indicates that the general market has higher expectations for it. This can be evident in its revenue growth FWD, which is more than double its competitors' median. In the event that WDFC underperforms this expectation, its P/E will definitely contract lower towards competitors' medians, which will cause its share price to drop.

Conclusion & Recommendation

WDFC's historical performance has shown its ability to protect margins against market uncertainties. Its most recent 4Q23 result has shown robust growth in net sales as well as gross margin expansion. These improvements were mainly driven by its higher pricing strategy and a strong recovery in sales volume, which was negatively impacted in the first two quarters of 2023. The strong volume recovery shows its products' strong branding.

While Asia Pacific has reported a decline, it was mainly due to tough comparisons with 4Q22 due to pandemic induced demand. In order to ride the wave of volume recovery and better pricing, WDFC has implemented two strategic initiatives, which are product premiumization and e-commerce. Together, I expect its strategic initiatives, better pricing, and volume recovery to bolster its growth outlook. This expectation of mine is further supported by management's 2024 guidance, which projects sales growth and margin improvements. With all of these in mind and an upside potential of ~16% by 2025, I recommend a buy rating for the stock.

For further details see:

WD-40 Company: Driving Future Growth Through Premiumization, E-Commerce, And Volume Recovery