WDFC - WD-40 Company: Long-Term Growth Potential Is Still Not Enough To Make Me Bullish

2023-03-18 01:15:46 ET

Summary

- WD-40 Company has faced a bit of pain lately, with sales, profits, and cash flows pulling back some.

- Despite this, management remains optimistic for 2023 as a whole, and the company offers attractive growth potential overseas.

- The business is a quality operator, but the stock is not cheap enough to make me bullish on it.

As a value-oriented investor, I often find myself passing up on opportunities solely based on the pricing of the firm in question. But one of the most important traits of being an investor is flexibility. Over the years, I have found that companies that I might otherwise be bearish on deserve a more neutral stance, while those that I might be neutral on, deserve a more bullish stance. This can be because of some attractive catalyst that the company has, or because it is a high-quality business that offers long-term stability. In those cases, a premium is not necessarily out of the question. One company where this is the case, in my opinion, is WD-40 Company ( WDFC ), an enterprise responsible for the production of WD-40 and similar related products. Most recently, the firm has faced a bit of downward pressure on its bottom line. Sales have also experienced a bit of a pullback. But if management's guidance for the year turns out to be accurate, then the business is not in that bad of shape. The stock does look a bit lofty on an absolute basis. But considering how high quality the company is, and factoring in a really great growth opportunity for it, I do think a ‘hold’ rating is appropriate for WDFC stock, as opposed to something more bearish, at this time.

Where future growth lies

Back in the middle of September of last year, I decided to revisit my prior investment thesis on WD-40 Company. Leading up to that point, the company had experienced a bit of pain, with both revenue and profits taking a hit. Despite these troubles, management remained optimistic about the future. Long before writing that article on the company, I knew that shares were rather pricey. But I have also known that this is the kind of business that you could likely go into a 20-year coma owning stock in and wake up knowing that your money is not likely to have disappeared. Because of these reasons, even though the stock was expensive enough for me to normally rate the business bearishly, I ended up keeping it as a ‘hold’ prospect. Since then, the firm has experienced a bit of downside. While the S&P 500 is up 1.1%, shares of WD-40 Company have dropped by 6.1%.

{kind=link}

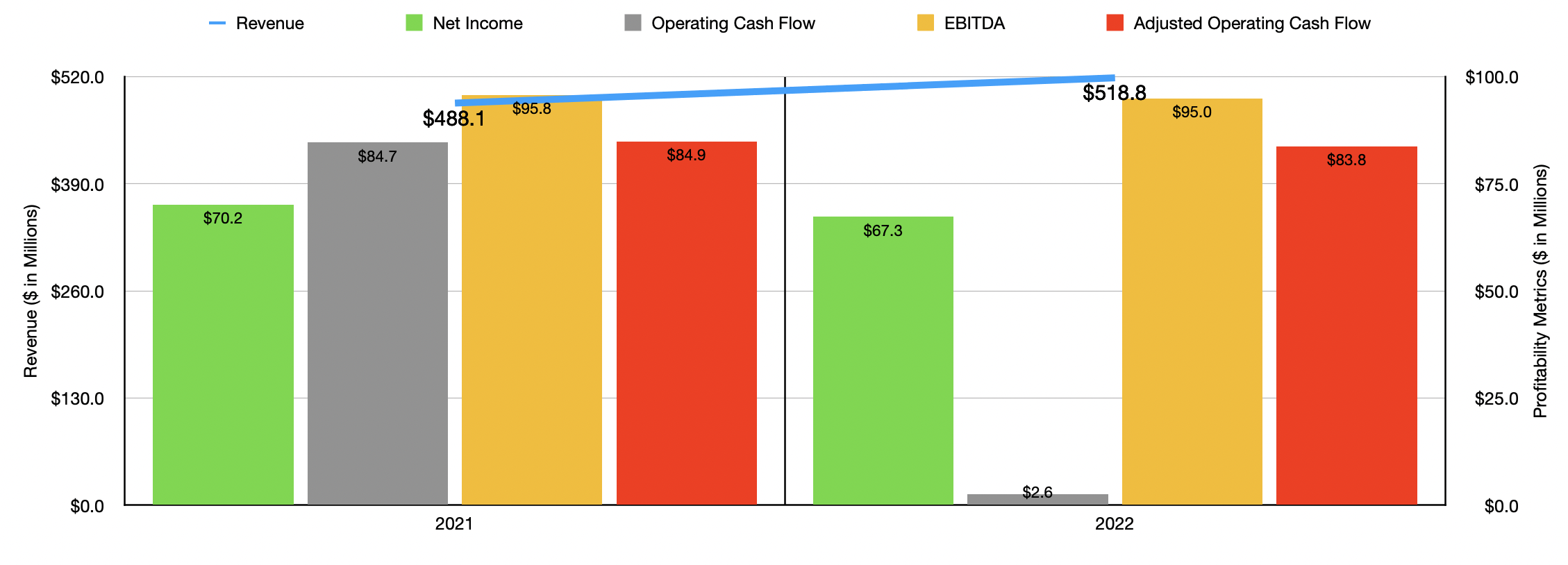

In my opinion, the weakness that WD-40 Company has seen was not driven by the fact that shares are a bit lofty. Rather, it had to do with some mixed financial performance. Consider the company's results for the 2022 fiscal year . Revenue during this window of time totaled $518.8 million. That's 6.3% higher than the $488.1 million reported for the 2021 fiscal year. Based on the data provided, this sales increase came even as the home care and cleaning products that the company produces reported a drop in revenue of about 15%. By comparison, the maintenance products it's responsible for saw a roughly 8% surge in revenue.

The greatest strength of the company during this window of time came from a mixture of its operations in the Americas, and its growth in the Asia Pacific region. In the Americas region, revenue jumped 12% The greatest portion of this increase in the US specifically involved the company’s WD-40 Specialist product. Revenue here spiked about 51% thanks to a combination of factors. This involved higher prices on the offering, combined with the fact that the company was negatively impacted the prior year from supply chain issues. Sales in Latin America jumped by 35% thanks to higher prices and greater product availability, while sales in Canada grew 16% because of greater demand in the industrial channel in Western Canada, with that demand improvement attributable to greater activity levels of end users in the oil space. In the Asia Pacific region, sales grew by 13% because of promotional programs and the continued easing of COVID-19 restrictions. The only significant weakness that the company experienced globally involved the EMEA (Europe, Middle East, and Africa) regions. Sales here dipped by about 2% Because of lower demand, as well as foreign currency fluctuations.

Although revenue for the company increased during this window of time, profits took a slight step back. Net income, for instance, shrank from $70.2 million to $67.3 million. Operating cash flow fared even worse, plunging from $84.7 million down to $2.6 million. But if we adjust for changes in working capital, we would have seen it fall from $84.9 million to $83.8 million. Meanwhile, EBITDA for the company inched down from $95.8 million to $95 million.

{kind=link}

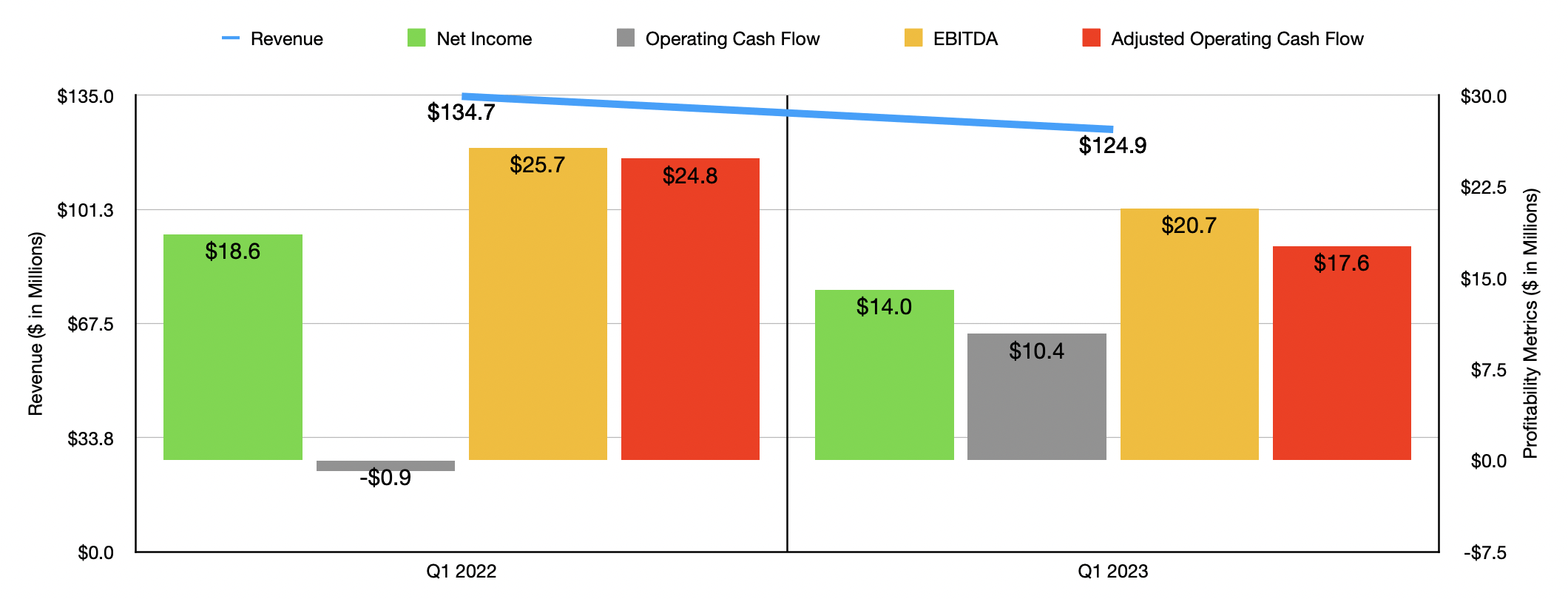

Heading into the 2023 fiscal year, we saw some of the picture worsen. In the first quarter of the year, revenue of $124.9 million came in lower than the $134.7 million reported the same time one year earlier. Just as was the case for the 2022 fiscal year as a whole, the first quarter of the year involved weakness from the EMEA regions. Revenue there plunged about 29% year over year. This, management said, came in spite of higher selling prices on these products. A decline in sales volume impacted revenue here negatively to the tune of $18.3 million, with $5 million of the sales decline related to the suspension of activities within Russia. Foreign currency fluctuations also hit the company here to the tune of $8 million. This decline in revenue also brought with it bottom line results that were worse than they were a year earlier. Net income, as an example, fell from $18.6 million down to $14 million. In the chart above, you can see that its other profitability metrics largely fell as well.

Despite the troubles in the first quarter of the year, management remains optimistic about 2023 as a whole. They currently anticipate revenue of between $545 million and $570 million. That would represent year-over-year growth of between 5% and 10%. In addition to this, they said the net income should be between $69 million and $71 million. No guidance was given when it came to other profitability metrics. But if we assume that they will change to the same rate that net income is forecasted to, we would get adjusted operating cash flow of $87.2 million and EBITDA of $98.8 million.

{kind=link}

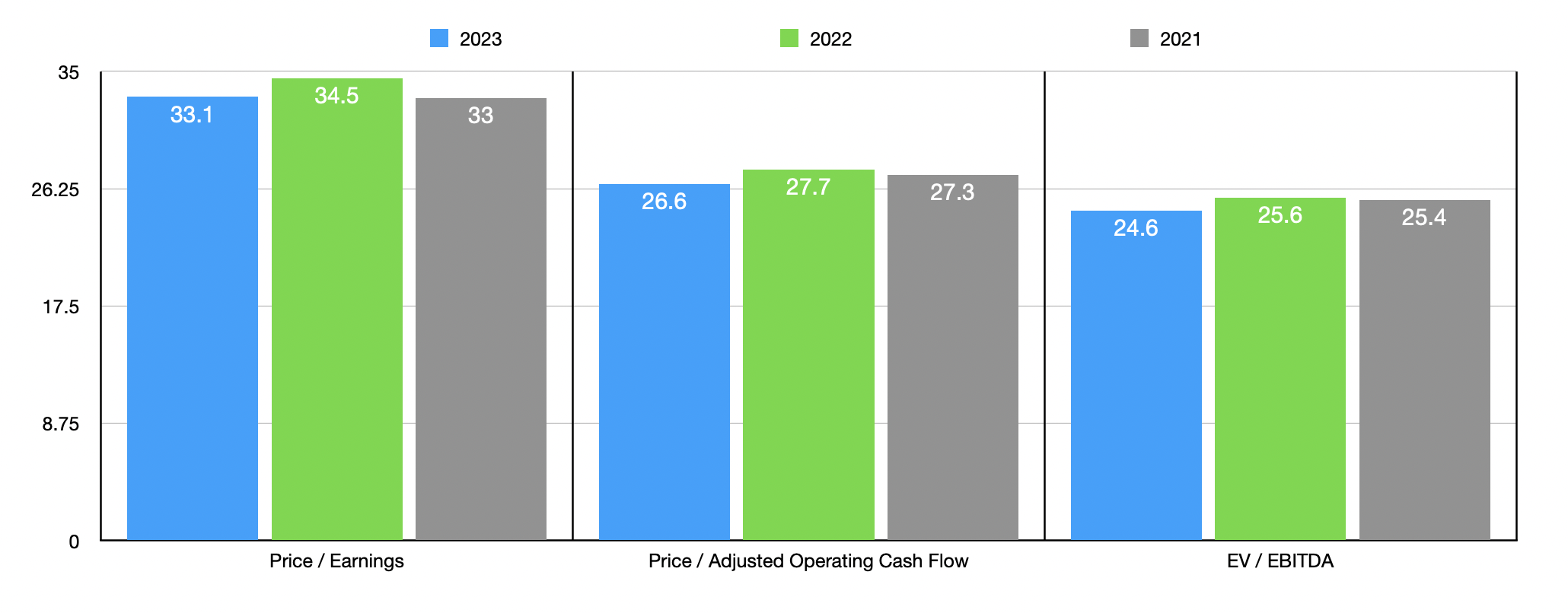

As part of my analysis, I calculated out what the company would look like using data from not only 2021 and 2022, but also using the estimated figures for 2023. The results can be seen in the chart above. On an absolute basis, the stock definitely looks expensive. But relative to similar consumer product businesses, the stock is only a bit lofty. On a price-to-earnings basis, the five companies that I compared it to had multiples of between 8.5 and 56.6. Three of the five firms were cheaper than WD-40 Company. Using the price to operating cash flow approach, the range was from 10.9 to 25.7. In this case, our prospect was the most expensive of the group. And finally, using the EV to EBITDA approach, we get a range of between 10.2 and 49.9. In this scenario, four of the five companies were cheaper than our target.

| Company |

| Price / Earnings |

| Price / Operating Cash Flow |

| EV / EBITDA |

| WD-40 Company |

| 34.5 |

| 27.7 |

| 25.6 |

| Energizer Holdings ( ENR ) |

| 8.5 |

| 10.9 |

| 10.5 |

| Spectrum Brands Holdings ( SPB ) |

| 56.6 |

| 15.7 |

| 49.9 |

| Central Garden & Pet Company ( CENT ) |

| 15.9 |

| 22.9 |

| 10.2 |

| Reynolds Consumer Products Inc. ( REYN ) |

| 21.7 |

| 25.7 |

| 14.2 |

| The Clorox Company ( CLX ) |

| 44.7 |

| 20.4 |

| 23.9 |

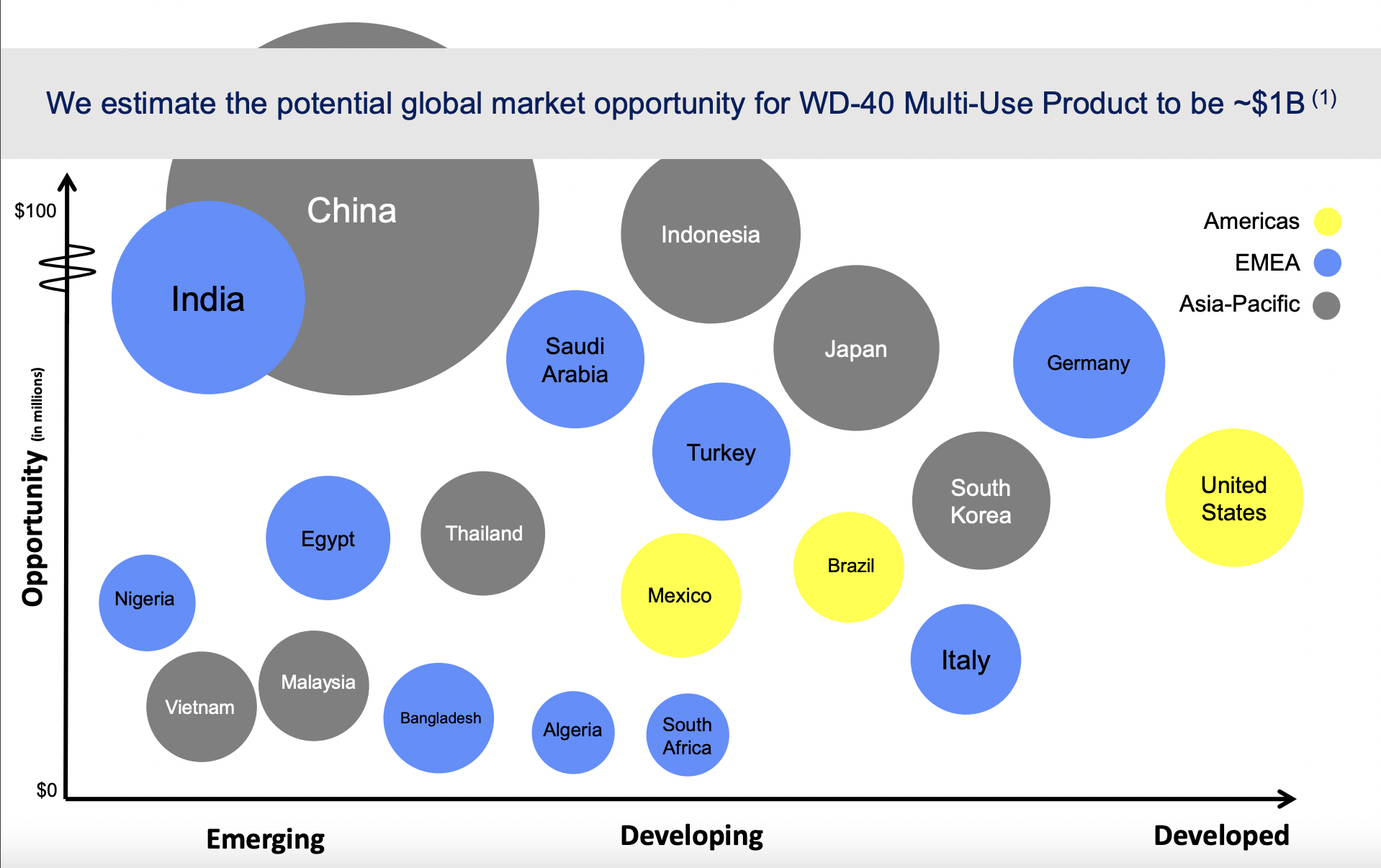

Truth be told, WD-40 Company is not growing at a particularly fast rate. However, the firm does have a rather attractive growth catalyst to propel it further. This is the fact that the Americas accounts for 46% of the company's revenue while the markets in this regional collection comprise only a very small and developed portion of the firm's overall market opportunity. For just its WD-40 Multi-Use Product alone, management believes that there exists an opportunity worth around $1 billion. The greatest exposure for the business should come from China, followed by a variety of other countries like India, Indonesia, and Japan. In addition to investing in ways to further expand its product availability in these markets, the company is also focusing on things like its ‘premiumized’ products. These are basically reimagined, upgraded versions of its original product line. One example is the introduction of a ‘smart straw’ on the cans of its products that make using said product easier. 47% of revenue associated with the WD-40 Multi-Use Product falls under this category. And management expects this number to exceed 60% in the not-too-distant future.

{kind=link}

When it comes to competitive analysis, it's important to note that there aren't any real major publicly traded companies that compete with the core products that WD-40 Company offers. Even the comparable firms listed above focus on general consumer goods items that don't have a great deal of overlap with what WD-40 Company sells. This is not to say that there aren't other products on the market that compete with WD-40 Company. Examples include PB Blaster, 3-In-One, and Liquid Wrench. But none of these are major products of a publicly traded firm. In truth, there's probably a good reason for this. It's not that the product that WD-40 Company makes is vastly superior to what else is out there. Rather, it's how the company sees itself. Management describes the firm as a ‘global marketing organization dedicated to creating positive lasting memories’. They don't describe it as a provider of water displacement products.

The company has essentially taken what could normally be considered a commoditized offering, and made it a household name through creative and robust marketing efforts. Along these lines, the firm has even documented over 2,000 distinct uses for its hallmark WD-40 product. Over decades, this has paid off nicely. As far back as 1993, the company estimated that at least one of its products was in about 80% of all households in America. As recently as 2018 (no newer data has been released), the company even boasted a WD-40 Fan Club that consisted of roughly 100,000 members. At the end of the day, its economic mode has been the product of how management has nurtured the brand and promoted the brand’s recognition in the markets in which it operates. As I mentioned already, the company's greatest opportunities moving forward lie abroad. It already has a good start on that, with operations spread across 176 different countries.

Assessing balance sheet strength

When I mention that WD-40 Company is a high-quality company, that means more than saying that sales, profits, and cash flows are stable, and that cash flow margins are robust. It also means that the company's overall financial health is strong. We can validate this in a number of ways, but the fact that management has made some changes over the years requires us to dig deeper than just the surface-level numbers to see it.

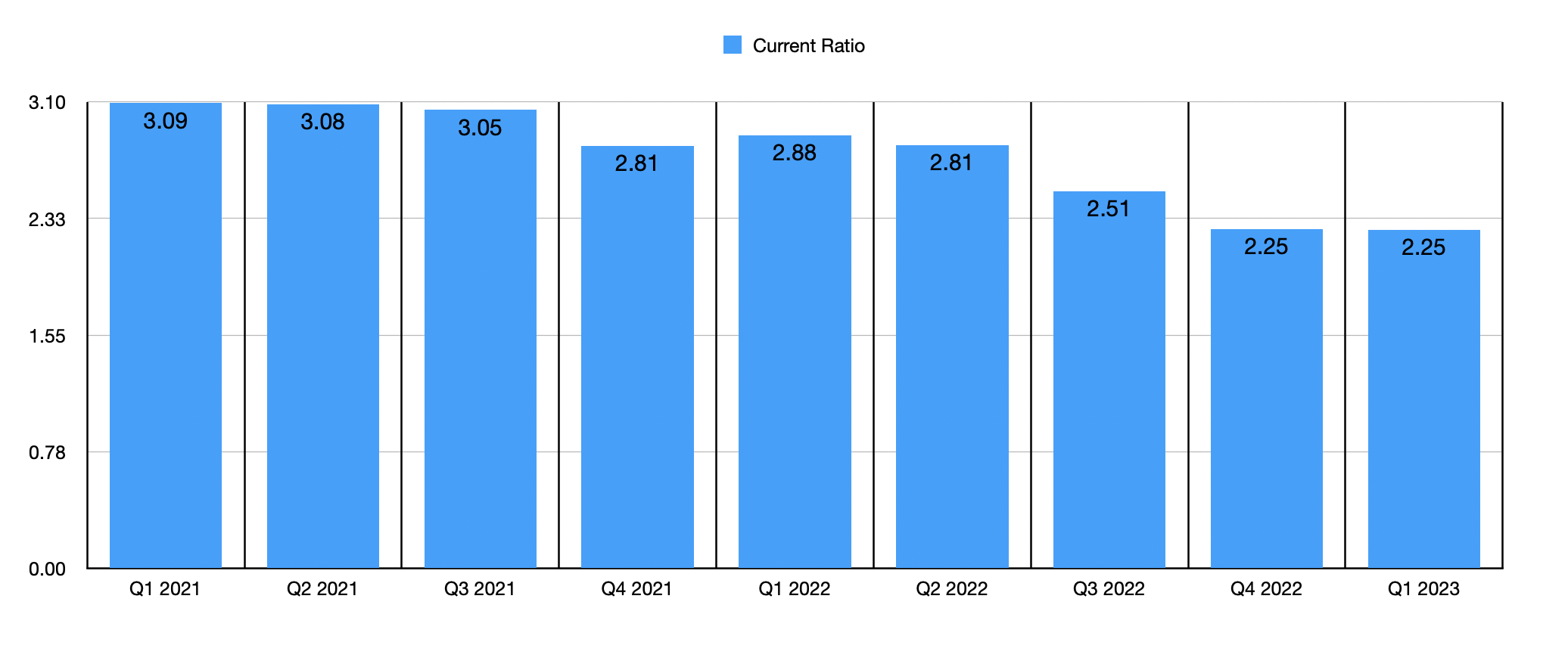

A vital part of a company's financial health is determined by the strength of its balance sheet. When it comes to this, there are a few choice metrics that I like to look at. The first of these is the current ratio. This is the value of current assets divided by the value of current liabilities. And it serves as a measure of how liquid the company is. In short, over the next 12 months, can it be expected to pay its bills without needing to tap into debt? In the case of WD-40 Company, the answer is a resounding yes. However, when looking at the data over the past several quarters, investors might initially be alarmed by a significant trend that has emerged.

{kind=link}

As you can see in the chart above, the current ratio of the company back in the first quarter of 2021 was 3.09. This means that the company had about $3 in liquid assets or assets that would become liquid over the next 12 months for every $1 in liabilities that would be coming due. Since then, the overall trend in this has been negative, with the most recent reading coming in at 2.25. This means that the company has become less liquid over time. Although disconcerting, I don't see much of an issue here. Generally, a reading of 2 or higher is considered highly liquid. So a case could be made that management was trying to reduce excess capital on its books in order to become more financially efficient. Frankly, I think the current ratio could fall below the 2 handle given how stable the company's cash flow history has been. But the bottom line is that this reading on its own is still robust.

{kind=link}

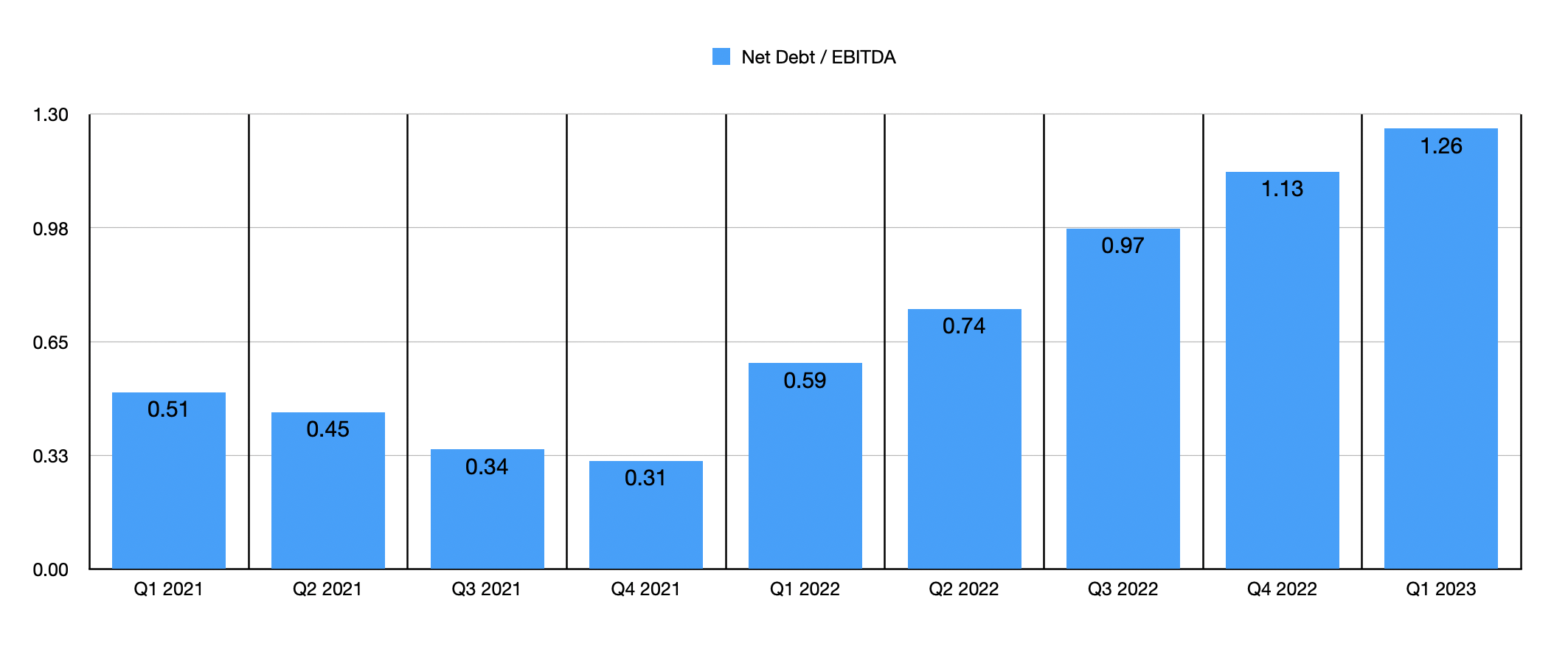

Moving on, it's important to discuss overall leverage for the business. High amounts of debt can have a significant negative impact on the health of a business. In the case of WD-40 Company, we would have actually seen the amount of net debt increase from the first quarter of 2021 through the first quarter of 2023. This number grew from $49.7 million to $113.5 million. And as a result of this, the net leverage ratio expanded from 0.51 to 1.26. Those who are critical of the company would point out that this is normally the opposite direction of what the business should want to be heading.

{kind=link}

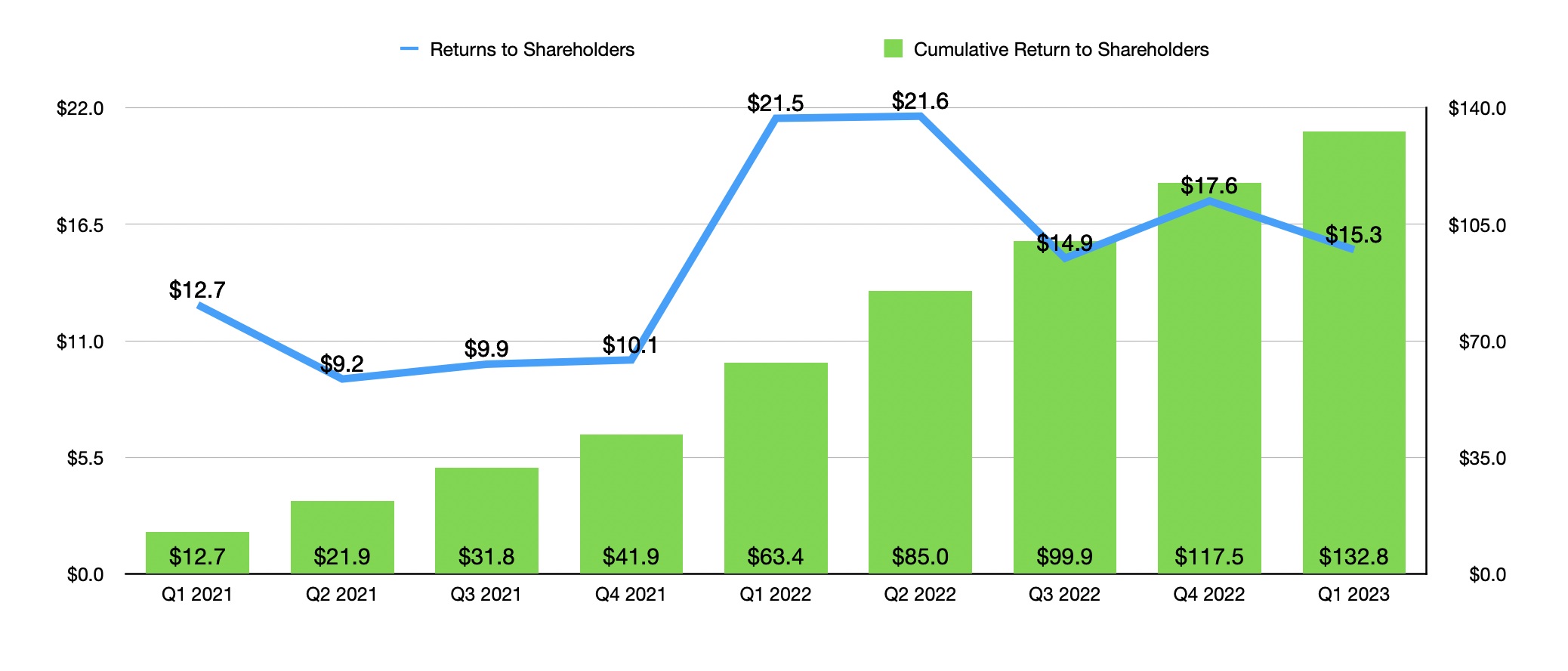

On this point, I do agree. But I also think significant context is needed. A couple of years ago, we had a company that had more liquidity than it needed. In order to operate more efficiently, the firm decided to make some rather bold moves. In the timeframe covered, this involved significant returns that management made to shareholders. Between dividends and share buybacks, the company returned $132.8 million to its investors from the first quarter of 2021 through the first quarter of 2023. In the latest quarter alone, this involved $10.6 million for dividends and $4.7 million in stock buybacks. Not only was this a use of cash, it also involved the company taking on additional debt to fuel these changes. Gross debt at the end of the first quarter of 2021 was $115.5 million. Today, it stands at $150.4 million. You can actually see, in the chart below, what the adjusted net debt of the company would have been had management never bought back any stock or paid out any distributions.

{kind=link}

Given the current interest rate environment that we are dealing with, it would be entirely appropriate for investors to wonder what impact this might have on the business moving forward. In my opinion, I believe the impact will be minimal. Yes, the company does have some debt that is interest-rate sensitive. As of the end of the latest quarter, that number stood at $82.4 million. A 1% rise in interest rates on this debt would increase interest expense on an annual run rate basis by $0.82 million. But of course, this ignores the tax shield that the company enjoys. If we assume a 21% effective tax rate, the after-tax impact would be $0.65 million. The rest of the debt is fixed. This includes $16 million at a 3.39% rate per annum. Until maturity, the firm has to repay $0.4 million in principal every six months On this. The company also has another $52 million in fixed debt with a weighted average interest rate of about 2.6%. Half of this comes due in 2027, while the other half comes due in 2030.

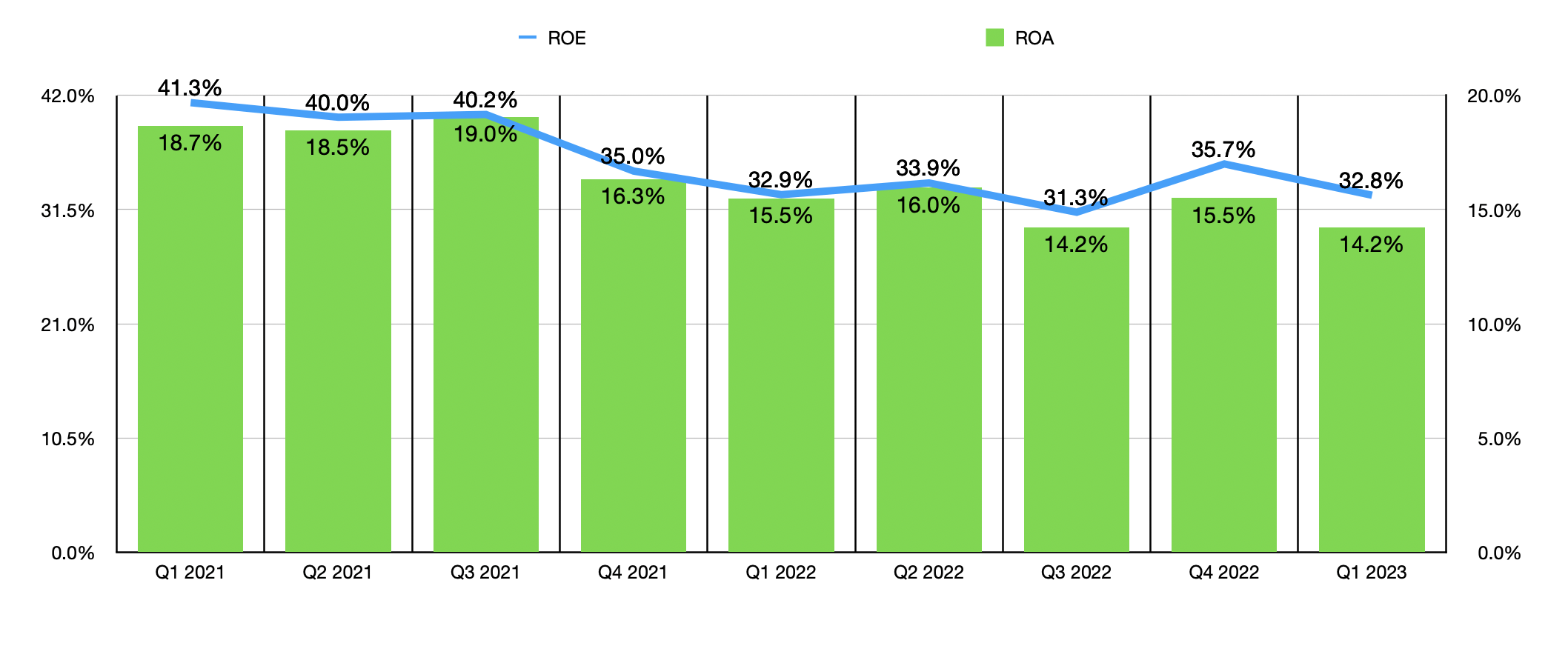

The changes made by management, combined with just operational changes in general, have resulted in some of its most important profitability margins worsening. As you can see in the chart below, the return on equity for the business has fallen from 41.3% to 32.8%, while the return on assets has declined from 18.7% to 14.2%. Again, in a vacuum, this looks bad. But be mindful of the fact that, historically speaking, value investors like Warren Buffett have praised companies that have consistently generated a return on equity of 20% or higher.

{kind=link}

Takeaway

From the data that I can see, WD-40 Company is hitting a bit of a rough patch. But that doesn't change the fact that management currently has a rosy outlook for the enterprise. Shares are not exactly the cheapest. But for a high-quality company with a solid history of stability, I don't think this stock is necessarily overvalued. This is especially true when you consider that the business continues to grow both here at home and overseas. And based on management's own expectations, the overall opportunity there could be significant. For these reasons, I do still believe that the company warrants a ‘hold’ rating at this time.

For further details see:

WD-40 Company: Long-Term Growth Potential Is Still Not Enough To Make Me Bullish