WDFC - WD-40: Defying Expectations With Bullish Q3 2023 Earnings

2023-07-11 12:50:43 ET

Summary

- WD-40 Company reported strong fiscal Q3 2023 earnings with net sales growth of 14.60% YoY, surpassing expectations and resulting in a 15% surge in stock price.

- The company's growth is attributed to its diverse product portfolio, expansive distribution network, and focus on geographic expansion and digital commerce.

- Despite challenges such as currency fluctuations and operational cost hikes, WD-40 maintains a "buy" rating due to its robust financial performance and promising growth strategies.

Thesis

WD-40 Company ( WDFC ), a global mainstay in the homecare and maintenance sector, has just reported a bullish fiscal Q3 2023 earnings performance, surmounting previous flat quarters and recording impressive net sales growth and a significant increase in net income. The company's EPS of $1.38 beat estimates by $0.16, and its revenue of $141.72 million marked a 14.60% year-over-year increase, surpassing expectations by $3.32 million and the market, at the time of this analysis, appears to be loving it with +15% surge in its price.

This remarkable financial turnaround, fueled by a diverse product portfolio and expansive distribution network, signals the firm's resilience in the face of headwinds such as currency fluctuations and operational cost hikes. The article that follows will dive into WD-40's financial report, dissecting the potent strategies underpinning its strong earnings and global footprint, and examining future growth prospects, while also highlighting potential areas of concern.

Company Overview

Since 1953, WD-40 Company , a name that resonates across continents, is standing tall as a key player in the arenas of maintenance, homecare, and cleaning products under the WD-40 Multi-Use brand that offers versatile maintenance products in different forms, including aerosol sprays, non-aerosol trigger sprays, and liquid-bulk products.

Its footprint is substantially broad - the Americas, Europe, Middle East, Africa, Asia Pacific, and even down under in Australia. Their robust distribution network extends from warehouse club stores, hardware stores, and automotive parts outlets. Not to mention a veritable army of industrial distributors and suppliers, mass retail and home center stores, value retailers, and grocery stores.

WD-40 Company's Bullish Fiscal Q3 2023 Earnings Highlights

The WD-40 Company exhibited a powerfully robust performance in the third fiscal quarter of 2023 , having muscled past a pair of flat quarters. It is a story of remarkable top and bottom line growth, with net sales clocking a 15% surge year-over-year, thereby setting a new record of $141.7 million. Meanwhile, net income took a giant 30% leap to $18.9 million. However, the tailwind of these positive strides was slightly curbed by the bitter gusts of currency headwinds.

Despite the harsh storms of pricing surges which have haunted the past year, the company managed to hold its sails firm with growth in sales volume. The decline in sales volume in the Americas and EMEA regions was overshadowed by a healthy injection of $5.5 million in growth from the Asia Pacific region. With this, the company's net sales to date for the year scaled a 2% incline compared to the prior year, reaching a respectable $396.8 million.

Breaking it down regionally, the Americas witnessed a hearty 16% growth in sales. This was primarily fueled by a powerful response to WD-40 multi-use products and a surge in sales of 3-IN-ONE and WD-40 Specialist, underpinned by price increases, expansion in production capabilities, and notable supply chain enhancements.

Meanwhile, the EMEA region exhibited signs of a comeback with a modest 6% quarter-over-quarter growth in sales, bouncing back from an unsteady beginning brought on by pricing actions and the impact of lost sales in Russia and Belarus. When observed on a constant currency basis, the rise would have been a more noticeable 13%.

On the other hand, the Asia Pacific region stole the spotlight with a phenomenal 42% increase. This growth was orchestrated by a positive shift in supply chain conditions and price elevations compared to the prior year. However, Australia had to weather a 14% sales reduction, a result of dwindling volumes and an unfavorable currency environment.

Eyes set on global expansion and premiumization, the company revisited its aspirations for growth. Anticipated annual sales growth for the Americas, EMEA, and the Asia Pacific are projected at 5%-8%, 8%-11%, and 10%-13% respectively. Amid the whirlwinds of geopolitical instability, foreign currency fluctuations, and the potential deemphasis of homecare and cleaning brands, the company is reevaluating its 2025 revenue objectives.

In the face of such obstacles, the company remains unfazed, and steadfastly focused on their essential strategic battles, which encompass geographic expansion and premiumization of the WD-40 Multi-Use Product, growth of WD-40 Specialist, and an increased concentration on digital commerce. Global sales of WD-40 Multi-Use products have resumed growth so far this year, with the United States, China, and Mexico leading the way. E-commerce sales too have seen a significant over 35% surge in the third quarter and year-to-date, predominantly stimulated by growth in the Americas.

Expectations

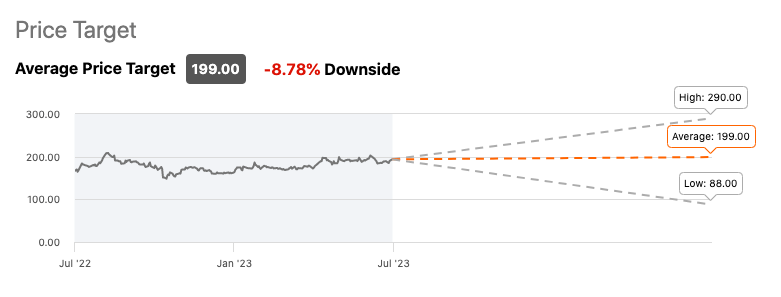

At the time of my analysis, WD40 is covered by 4 Wall Street analysts who have an average "Buy" rating on the company with some fairly wide predictions on its price target that translate to a -8.78% performance.

{kind=link}

Performance

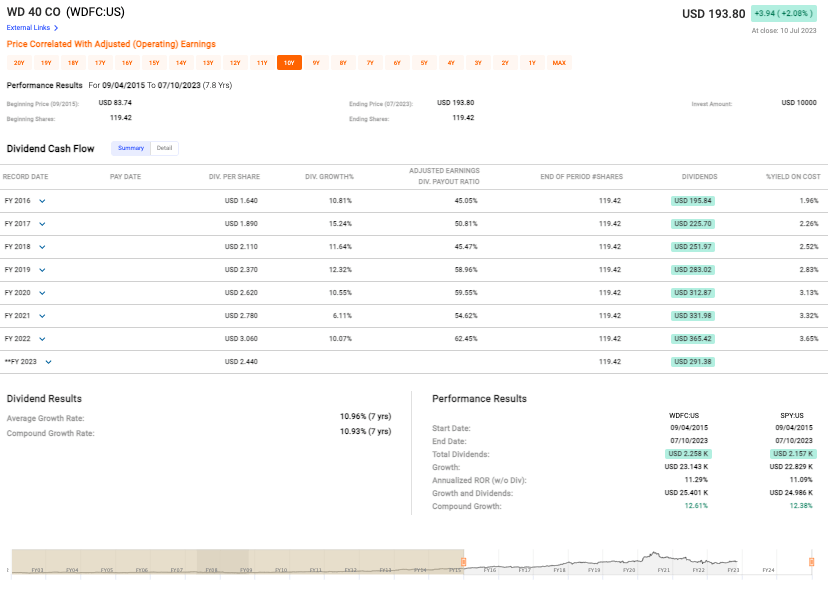

Over the medium-term (7.8 years), WD-40 showed a high degree of financial robustness and savvy growth strategy by more than doubling from USD83.74 in September 2015 to a whopping USD193.80 as of July 10, 2023 (please keep in mind that the data had not caught up with the post-earnings morning surge of +15%); therefore, we're seeing a compounded annual growth rate ((CAGR)) of 12.61% including dividends, that ever-so-slightly outpaces the broader market as represented by the S&P 500 Index (SP500) with a CAGR of 12.38%.

{kind=link}

In seven consecutive years (see data above), WD-40 has seen an average dividend growth rate of 10.96%; an initial investment of USD10,000 would have grown significantly during that timeframe. Looking at the data, the growth including dividends for WDFC was USD25.401K versus USD24.986K for the S&P. And, on an annualized basis, WDFC delivered a rate of return of 11.29%, compared to S&P's 11.09%, without considering dividends.

Valuation

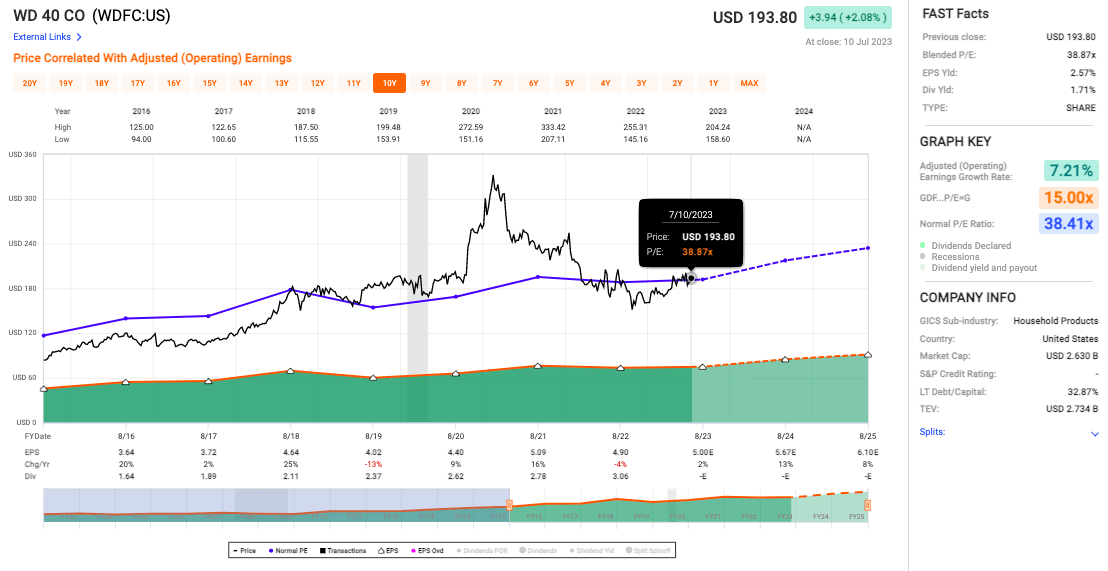

At the time of my analysis, the Blended Price-to-Earnings (P/E) ratio is a meaty 38.87x (see chart below). The market, it seems, is expecting a lot from WD-40. This optimism is further highlighted by the firm's Normal P/E Ratio of 38.41x, indicating that this high valuation isn't a sudden fluke.

{kind=link}

The Adjusted Earnings Growth Rate at 7.21% seems reasonable, but doesn't exactly match the frothy P/E ratios we're seeing.

Finally, the dividend yield of 1.71%, suggests that WD-40 is rewarding its shareholders reasonably well. At 2.57%, however, I find WD-40's EPS yield somewhat disappointing given its high P/E multiples and relatively high multiple of earnings reinvestment into the business.

Risks & Headwinds

At 50.6% , gross margin falls short of its long-term goal of 55% and EBITDA stands at 20% - five percentage points below the desired 25%. While these numbers may seem inconsequential at first glance, their underperformance indicates areas of inefficiency or systemic underperformance that need addressing in future quarters.

Additionally, the increase in the cost of doing business from 31% to 32% warrants careful consideration. In an environment where employee-related expenses, professional services fees, and the costs tied to cloud-based systems are escalating, margin management becomes increasingly critical. Rising costs can easily eat into profitability, even in the face of strong revenues.

Now, it's essential to factor in the role of foreign currency in the financial performance. The company has felt the pinch due to fluctuations in foreign currency exchange rates, and this trend has been adverse to its net income. Currency headwinds can be unpredictable and can have a material impact on earnings, so any further volatility could continue to suppress the company's bottom line.

This brings me to my final point about potential earnings pressure. The projected earnings per share, in the range of $4.80 to $5, reflect a decline from last year's figure of $5.5, so it is imperative for the company to find ways to bolster earnings per share as investors may become concerned over this decrease in growth potential.

Final Takeaway

WD-40 Company's latest fiscal Q3 financial report has me leaning firmly into a "buy" rating for its stock. Undeterred by the swirling maelstrom of currency fluctuations and operational cost hikes, WD-40 emerges with Q3 2023 earnings radiating robust vitality, painting a canvas of burgeoning net sales and income. A host of strategic elements - a powerful distribution network, successful product suites, and a hawkish focus on geographical and digital expansion - converge into strong momentum for WD-40 Company within the Americas, EMEA, and Asia Pacific regions. The result? A company leaving broad footprints across the global landscape, its growth strategies not just resonating, but resounding triumphantly.

For further details see:

WD-40: Defying Expectations With Bullish Q3 2023 Earnings