WDI - WDI And PAI: Attractively Discounted And Delivering Investors Income

2023-07-17 16:29:39 ET

Summary

- WDI and PAI are two funds that can deliver regular income to investors with a monthly distribution, though they pay out substantially different levels of yield.

- These are two quite different funds in terms of strategy and being leveraged vs. non-leveraged, but together could be considered quite complementary, weighing the positions depending on one's risk tolerance.

- Despite their different strategies, both funds are delivering income to investors on a monthly basis, and their distributions are covered by net investment income.

Written by Nick Ackerman, co-produced by Stanford Chemist.

Western Asset Management Company might not be as popular as PIMCO, but they are a big player in the fixed-income space. They were founded in 1971 and then acquired by Legg Mason in 1986. Later, Franklin Templeton Investments (Franklin Resources ( BEN )) acquired Legg Mason in 2020. Western Asset still operates pretty independently as an indirect wholly owned subsidiary, retaining its branding on its funds.

Two of these funds, I believe, represent attractive choices for different reasons in the current environment. That includes Western Asset Diversified Income Fund ( WDI ) and Western Asset Investment Grade Income Fund ( PAI ).

WDI is a leveraged multi-sector fixed-income fund, while PAI is a non-leveraged fixed-income fund focused on investment-grade securities. This clearly sets them apart with significant differences. Both are delivering income to investors on a monthly schedule. Perhaps more importantly, these distributions are being covered by net investment income being generated on these funds. That's unlike several other fixed-income closed-end funds these days.

WDI Basics

- 1-Year Z-score: 0.36

- Discount: -10.79%

- Distribution Yield: 12.03%

- Expense Ratio: 1.65%

- Leverage: 32.87%

- Managed Assets: $1.15 billion

- Structure: Term (anticipated liquidation date, June 24, 2033)

WDI's objective is "to seek high current income. As a secondary investment objective, the fund will seek capital appreciation." They will bring a "flexible and dynamic" approach. They anticipate doing this by rotating sectors and securities in response to market conditions, focusing on what we believe are undervalued securities with attractive fundamentals.

WDI is the newest fund of these two, with inception in mid-2021. We touched on this with previous updates that it was one of the worst times to launch a fixed-income fund. It resulted in some significant declines for investors who bought in too early. I first turned bullish on WDI in July 2021, and that was too early. It still resulted in positive total returns of 5.16% since that time. With hindsight, though, we can see had I waited until the fall, it would've presented a much better opportunity.

{kind=link}

In reality, almost any fund launched in 2021 was met with a big downturn in 2022. It was one of the worst markets experienced in decades for both equities and fixed-income. With rates stabilizing now and the potential for only a couple more increases before some cuts, the future is looking much brighter.

WDI's expense ratio comes to 1.65%. In isolation, that could appear high, but it really isn't anything outlandish for a multi-sector fixed-income fund. When including leverage expenses, it climbs to 2.98%. Higher interest rates have negatively impacted them, leading to higher borrowing costs.

However, their portfolio can defend against this as they are also exposed to their floating rate investments. That's what has ultimately driven their NII to increase during this period, despite these rising borrowing costs. WDI is also the more exciting of the two, with a significantly higher distribution rate in the first place, but the trade-off is that it is due to the higher risks.

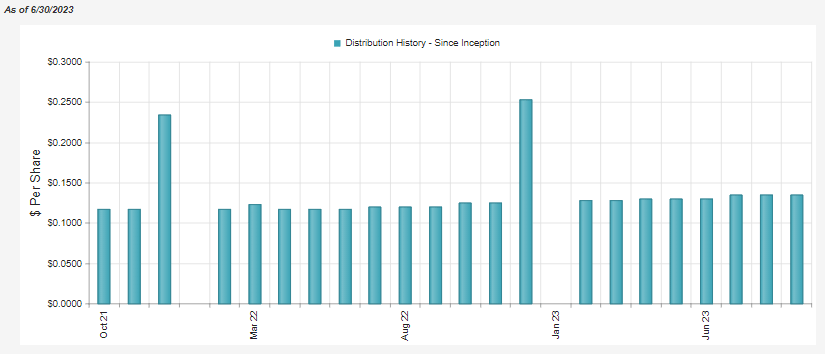

Those increases in NII have resulted in the fund being able to raise its distribution several times since its relatively recent launch. Taking the payout from $0.117 per month to the latest $0.135 per month.

{kind=link}

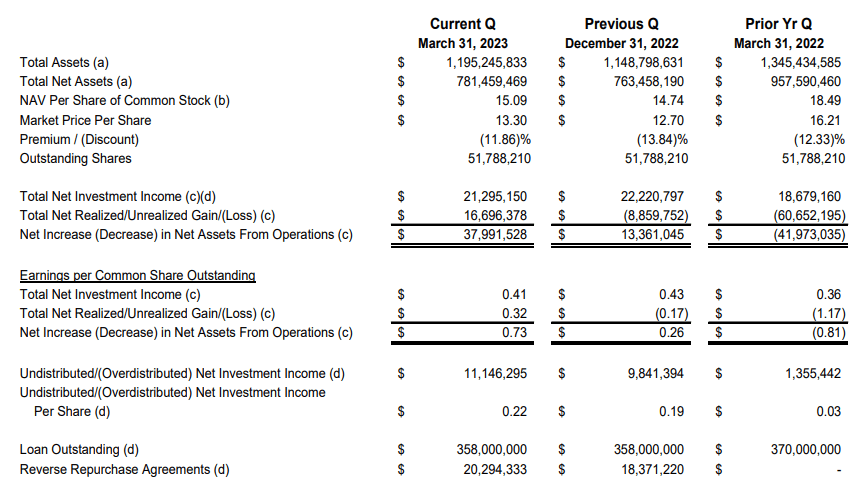

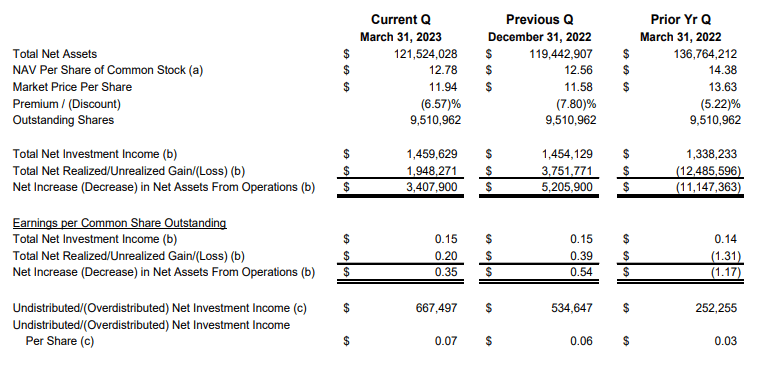

Their latest quarter showed a declining quarter over quarter, but year-over-year can be a better representation of coverage due to the timing of payments. For the year-over-year NII, we've seen a nearly 14% increase. The undistributed NII balance has also grown because even though they've been increasing their payout, it's remained over 100% coverage.

{kind=link}

Coverage in the first quarter was 101.23% based on the now increased distribution, or what was nearly 107% coverage based on the amount paid during that quarter at the time.

Despite the fund's growing NII and translating into distribution growth for investors, the market has still been giving WDI the cold shoulder. The fund remains at an attractive discount for investors to consider today.

Slap "PIMCO" on the front of this fund and cut distribution coverage to a precarious level, and we could possibly be trading at a premium.

Ycharts

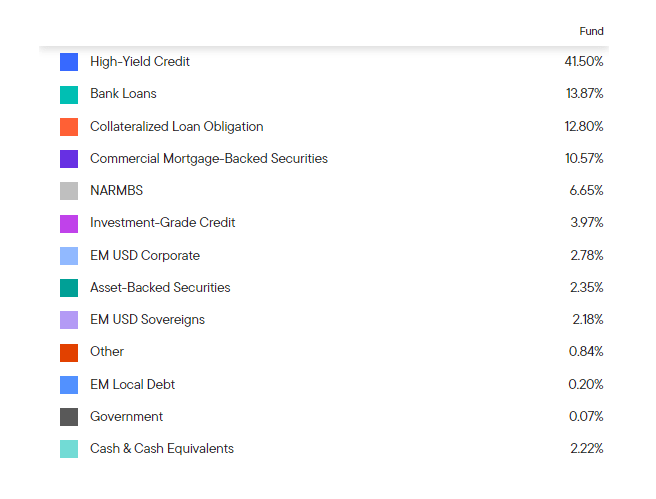

Of course, the 12.03% distribution rate on the share price and the NAV rate of 10.73% indicate this yield doesn't come for free. The portfolio is dominated by 'junk,' representing ~91.4% of the fund's assets. With higher junk and floating rate exposure, the fund's duration is relatively limited, coming in at 4.81 years.

{kind=link}

PAI Basics

- 1-Year Z-score: -1.19

- Discount: -8.06%

- Distribution Yield: 4.80%

- Expense Ratio: 0.77%

- Leverage: N/A

- Managed Assets: $119.95 million

- Structure: Perpetual

PAI's investment objective is "a high level of current income, along with capital appreciation." To achieve this, the fund "provides a portfolio of primarily investment grade debt, including government securities, bank debt, commercial paper, and cash/cash equivalents." They "emphasize team management and extensive credit research expertise to identify attractively priced securities."

PAI is the more boring of the two, but that can be precisely what some investors are looking for. It's also much older, with a history going back to its launch in 1972. Personally, PAI is one of the newest funds I've begun to cover, and it was when I was on the hunt for non-leveraged funds with higher-quality bonds.

With no leverage expenses, we don't have to worry about rising costs of borrowings or the greater volatility that comes with it. For a CEF, it also sports a fairly low expense ratio of 0.77%.

In reverse to how WDI is positioned, ~93.4% of PAI's portfolio is BBB rated or higher.

PAI Portfolio Credit Quality (Western Asset)

The 4.80% distribution yield currently is fairly comparable to money market funds but with more risk. So I'm not looking for it solely as a yield play. With a higher quality portfolio, the fund comes with a higher duration of 7.34 years. That means it's relatively more interest rate sensitive when compared to WDI. That's also one of the primary characteristics that I'm hoping to exploit with this fund going forward when interest rates are cut.

When rate cuts occur, we should expect the fund's underlying portfolio to rise in value - reversing some of the damage that it went through in 2022 when interest rates were rising rapidly.

Ycharts

During this time, the fund also experienced a widening discount. Getting some of that discount to narrow or if the fund went back to trading at a premium could really be a kicker to the end result.

Ycharts

At the same time, the yield itself can still provide regular income while waiting for that to happen. Just like WDI, it is well-supported. Based on the latest quarterly financials, NII coverage comes to 107.5%. That leads to an argument that could be made that we could see an increase as the UNII balance has been rising a bit.

{kind=link}

Year-over-year, they also saw NII increase a touch. It was to a much smaller degree than WDI, but a rising trend could be seen going forward due to higher yields available these days. However, it isn't necessarily completely in the clear if we hit a recession. The 2020 Covid pandemic actually saw the fund reduce its distribution twice during that year.

{kind=link}

The main questions then become how long until potential rate cuts, and what damage has to happen to the overall economy for the Fed to cut? The Fed expects to cut next year and the following year based on their last projections . It's based primarily on inflation cooperating and heading lower.

Fed Interest Rate Forecast (FOMC)

Those expectations had increased from the March projections, too. It's a good reminder that it's only a guess, and anything can happen depending on the future. It makes these main questions impossible to answer.

Conclusion

Ultimately, my viewpoint on PAI is this; it's a bond fund with an investment-grade focus. It offers potential catalysts for outsized returns if interest rates are cut and if we get some discount contraction in the fund. If not, I'm left with a portfolio that should still be fairly safe - even if it provides only a meager yield - that I don't mind holding for the long term.

For WDI, rate cuts could also benefit this fund. However, it's important to consider that if rates are cut, the fund's NII could actually sink. So the offsetting appreciation that should be experienced on the underlying portfolio could offset that. In general, the current play is more for the covered distribution yield that the fund is paying out right now. An investor can do fairly well if they can keep that yield up and covered. Being leveraged and in a lower credit quality portfolio means greater risks, of course, which means there will most definitely be losses in the underlying portfolio. It's keeping them limited compared to what works – that is the important part.

For further details see:

WDI And PAI: Attractively Discounted And Delivering Investors Income