WDI - WDI And PDO: Pumping Out 11%+ Distribution Yields

2023-05-24 12:31:04 ET

Summary

- PDO and WDI both invest in below-investment-grade debt and are leveraged.

- That can make them riskier, so they might not be for everyone, but income investors often find them compelling for the higher distribution yields they can provide.

- Coverage at WDI is strong, and PDO coverage has been under pressure, but both pay over 11% distribution yields.

Written by Nick Ackerman, co-produced by Stanford Chemist. A version of this article was originally published to members of the CEF/ETF Income Laboratory on May 9th, 2023.

PIMCO Dynamic Income Opportunities Fund ( PDO ) is one of PIMCO's newer closed-end funds that was launched in early 2021. Western Asset Diversified Income Fund ( WDI ) was launched in mid-2021, so both of these funds are fairly new. While PDO experienced a deep discount initially, more recently, the fund has sported a small premium. WDI still trades at a deep discount and remains a more compelling option, but both funds can be fairly attractive if you are looking to diversify.

They are leveraged funds and invest in mostly below-investment-grade fixed-income. That raises risks and makes them more volatile, and they may not be for all investors. That being said, it also means these funds can both offer investors relatively higher monthly distributions.

Overall, fixed-income funds can be a compelling place to put capital to work compared to equity funds. That's because coverage of the distribution can be more predictable due to underlying portfolio holdings paying predictable yields. For equity funds, you are more at the mercy of a volatile asset class that requires capital gains for funding distributions.

Additionally, yields have been rising due to depreciation in the underlying portfolios due to the Fed raising interest rates. At some point, this should stabilize as we near the end of rate hikes. This can provide a potential boost in the future when rates are cut, but that shouldn't be something that is necessarily relied upon for results.

WDI 11.79% Distribution Yield

- 1-Year Z-score: -0.44

- Discount: 12.56%

- Distribution Yield: 11.79%

- Expense Ratio: 1.65%

- Leverage: 32.62%

- Managed Assets: $1.16 billion

- Structure: Term (anticipated liquidation date, Jun. 24, 2033)

WDI's objective is "to seek high current income. As a secondary investment objective, the fund will seek capital appreciation." They will bring a "flexible and dynamic" approach. They anticipate doing this by rotating sectors and securities in response to market conditions, focusing on what we believe are undervalued securities with attractive fundamentals.

The fund's expense ratio comes to 1.65%. In isolation, that could appear high, but it really isn't anything outlandish for a multi-sector fixed-income fund. When including leverage expenses, it climbs to 2.98%. Higher interest rates have negatively impacted them, leading to higher borrowing costs. However, their portfolio can defend against this as they are also exposed to their floating rate investments.

For greater flexibility, they have no restrictions on investing in investment grade or below investment grade. Meaning that they will span the credit quality spectrum, leading to a truly multi-sector bond fund with limited constraints. This can be a positive if they can successfully manage it. It leaves investors a bit more in the dark and more reliant on the management team to operate the fund. That can also include various derivatives that they implement in their portfolio.

The highest allocation for WDI is allocated to high-yield credit. Additionally, bank loans and CLOs come in as the second and third largest weightings.

WDI Sector Breakdown (Western Asset)

Bank loans and CLOs are particularly helpful for the fund when rates are rising. These are the investments that see their yields climb as rates rise, and that helps offset the rising leverage costs for WDI itself. They also show floating rates in most of their MBS exposure and other asset-backed securities. To further help minimize the higher expenses for the fund due to leverage is the fund's interest rate swaps that they had in place.

This has all been helpful enough during this rising rate environment to see the fund's distribution raised four different times in its short life. These have been small increases, but an increase when something is already yielding double-digits is quite a feat. Junk loans are really the only place that you'll tend to see that happen. The last annual report showed a net investment income coverage of nearly 110%, which provides evidence of why they were able to raise their distribution.

In fact, they've recently upped the distribution once again to $0.135 per month. NII came in at $0.41 for Q1 2023 , which provides for 101.2% NII coverage based on the now-upped payout.

{kind=link}

The latest distribution yield works out to an attractive 11.79%, while the fund's NAV rate is a more moderate 10.31%. This has been the result of the fund trading down to a wide discount.

New funds trading at a large discount shortly after launching isn't anything new, but being a term fund means that, eventually, this discount should be realized. That's far enough off at this point, where it isn't a main selling point of the fund, but it is something to keep in the back of your mind before investing in WDI.

The latest discount is below its average, which is admittedly only a short period of time. However, it's also approaching some previous trough levels. I believe that makes it an interesting choice at this time for this fund.

Ycharts

PDO 11.64% Distribution Yield

- 1-Year Z-score: 1.04

- Premium: 1.15%

- Distribution Yield: 11.64%

- Expense Ratio: 2.12%

- Leverage: 47.09%

- Managed Assets: $2.711 billion

- Structure: Term (anticipated term date Jan. 27, 2033)

PDO is designed to provide "current income as a primary objective and capital appreciation as a secondary objective." This is pretty standard for the PIMCO funds and most CEFs. They go on to mention how they will attempt to achieve this;

The fund will normally invest at least 25% of its total assets in mortgage-related assets issued by government agencies or other governmental entities or by private originators or issuers. The fund may invest up to 30% of its total assets in securities and instruments that are economically tied to “emerging market” countries; however, the fund may invest without limitation in short-term investment grade sovereign debt issued by emerging market issuers. The fund may normally invest up to 40% of its total assets in bank loans (including, among others, senior loans, delayed funding loans, covenant-lite obligations, revolving credit facilities and loan participations and assignments). It is expected that the fund normally will have a short to intermediate average portfolio duration (i.e., within a zero to eight year range), although it may be shorter or longer at any time depending on market conditions and other factors.

Including the leverage expenses, the fund's total expense ratio comes to a fairly lofty 2.79%. That being said, that's about where the whole PIMCO suite comes in, with higher expenses. They've traditionally outperformed despite this, too, historically. This helps highlight why I feel that WDI's expense ratio, while high in isolation, seems competitive compared to the PIMCO funds.

Additionally worth noting is that PDO carries a meaningfully higher amount of leverage compared to WDI, and PDO also trades at a slight premium after bouncing from their discount. Worth noting is that PDO is also a term structure fund, but if it trades at a premium near the termination date, that could see a better chance that it becomes a perpetually trading fund. However, similar to WDI, we have a while to worry about that event.

Ycharts

On top of this, PDO's latest coverage wasn't as impressive as WDI's. At one point, PDO's coverage was incredibly strong - interestingly, it was strong when it was at a deep discount. So now, with coverage lacking, the fund is trading at a premium.

{kind=link}

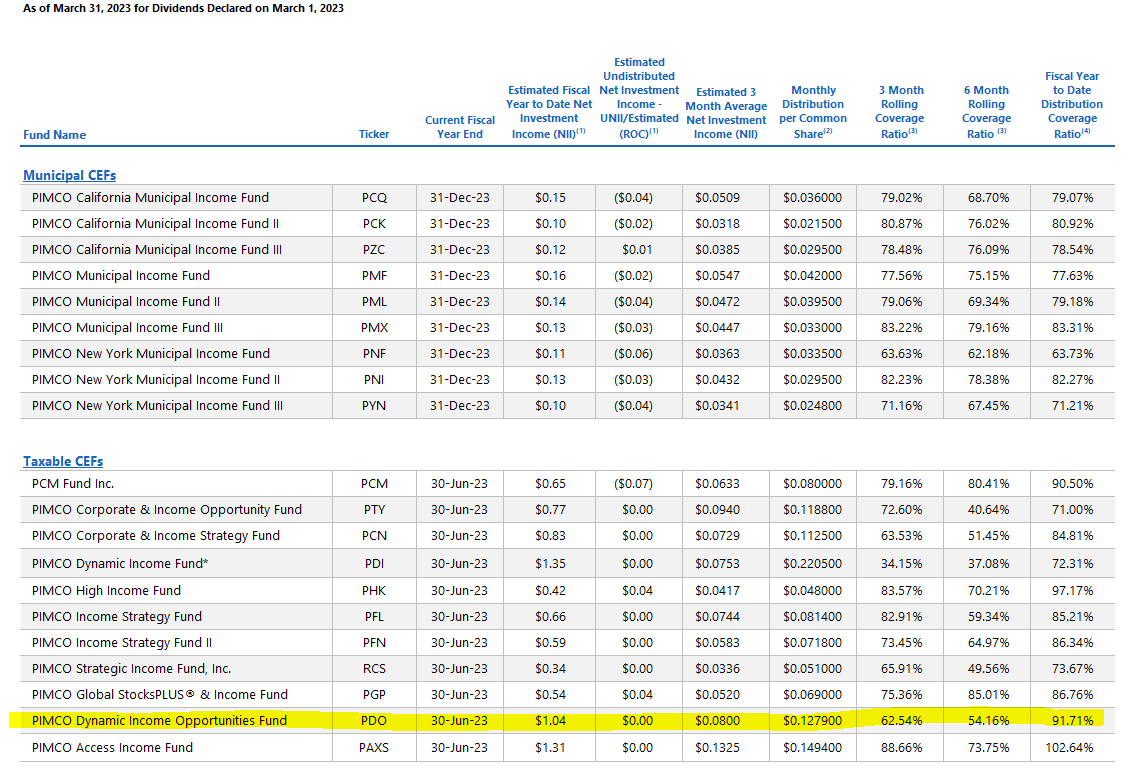

To be fair, though, this was as of the end of Mar. 31, 2023. The nearly 110% coverage we saw from WDI was for the year ending December 2022. Coverage for PDO in their last semi-annual report, which also is for the period ending December 2022 but is only a six-month report, was also stronger. In that report, the coverage stood at around 109% if you exclude the $0.96 special. They earned $0.84 NII per share and paid a total of nearly $0.77 after subtracting the $0.96 year-end special.

The coverage seems to be under pressure due to rising leverage costs and due to having to deleverage. WDI has been able to avoid deleveraging because they aren't maxing out their leverage in the first place. To highlight this, PDO's reverse repurchase agreements stood at $1.382 billion at the end of 2022. As of the end of March 2023, they are at $1.276 billion. To go back to their fiscal year-end on June 30, 2022, they reported reverse repurchase agreements of $1.52 billion. Reduced leverage means less income generation.

With costs rising for reverse repurchase agreements, it pinches the spread between what they can earn on the leverage that is left over. In their annual report, they listed these costing them anywhere from around 1% to 3%. By the end of 2022, we have seen these costs explode, going anywhere from nearly 2% to pushing nearly 6%.

While PDO isn't more compelling to me than WDI at this time, retaining the position in PDO can still make sense. First, you don't want to count out PIMCO, as they've proven historically that they can deliver results. That is, as long as you don't buy their funds at extreme premiums. PDO's premium is hardly "extreme" at this time. Even if there was a distribution cut, it would likely see relatively limited fallout.

Secondly, it can still provide more diversification through different holdings.

PDO Sector Allocation (PIMCO)

Not only diversification of different holdings but also diversification of a different management team. That's why I'm happy to hold both PDO and WDI as complements to each other over the long term. Both of these funds can provide attractive distribution yields for investors paid monthly. While WDI's coverage is significantly stronger based on our current information, that might not always be the case. In the future, it could be PDO that carries the better coverage. The market is constantly changing, and both funds are offered by fund sponsors with a history in the fixed-income space.

For further details see:

WDI And PDO: Pumping Out 11%+ Distribution Yields