WDI - WDI: Attractive Discount ~12% Distribution Yield And Solid Coverage

2023-09-18 07:16:38 ET

Summary

- If you're looking for a sustainable high-yield fund, Western Asset Diversified Income Fund could be it.

- WDI offers a high distribution yield, growing monthly distribution, and strong distribution coverage, which could mean even more increases in the distribution.

- WDI is trading at a deep discount, making it an attractive investment option in the high-yield leveraged CEF space.

Written by Nick Ackerman, co-produced by Stanford Chemist.

As we've seen several closed-end funds cut their distributions this year, Duff & Phelps Utility and Infrastructure Fund ( DPG ), John Hancock Premium Dividend Fund ( PDT ), Brookfield Real Assets Income Fund ( RA ) and now the latest Virtus Total Return Fund ( ZTR ), it might be time to look for a higher yield that is actually sustainable in the current environment.

That brings us to Western Asset Diversified Income Fund ( WDI ), one of my favorites in the high-yield leveraged CEF space currently. The fund sports a high distribution yield, a growing payout and strong distribution coverage. In fact, since our last coverage just in mid-July, we've seen another distribution increase . These aren't massive increases, but they are seriously starting to add up. Despite this, it is also trading at a deep discount, which makes it an even better deal.

WDI Basics

- 1-Year Z-score: 0.33

- Discount: -10.83%

- Distribution Yield: 11.92%

- Expense Ratio: 1.65%

- Leverage: 32.21%

- Managed Assets: $1.17 billion

- Structure: Term (anticipated liquidation date, June 24, 2033)

WDI's objective is "to seek high current income. As a secondary investment objective, the fund will seek capital appreciation." They will bring a "flexible and dynamic" approach. They anticipate doing this by rotating sectors and securities in response to market conditions, focusing on what we believe are undervalued securities with attractive fundamentals.

The fund is leveraged primarily through a loan, but it also incorporates some reverse repurchase agreements. They've had to deal with rising leverage costs just as any other CEF currently, and the latest semi-annual report shows a total expense ratio rising to 4.55% from 2.98%.

However, despite the rising costs, the portfolio is invested in floating rate investments that have been enough to offset these rising costs and produce increasing income. Additionally, the fund incorporates futures contracts and interest rate swaps to hedge these rising costs as well. This has all translated into rising interest rates positively contributing to WDI.

Still, leverage carries its own risks, as volatility and the risk of deeper losses is there. If we get a black swan event, they could be forced to deleverage their portfolio at a disadvantageous time and cause permanent damage. That's always a key risk when considering leveraged funds. Being a newer fund, this could be one of the main concerns investors have in how it would perform going through such a period.

Performance - Attractive Discount

Since our last update, the fund hasn't really done anything too exciting in either direction. Though it has been a relatively short period of time, the reason for updating coverage on this fund is more so due to the new semi-annual report and distribution coverage that's worth going over.

Ycharts

During this time, the fund's total share price return has lagged the total NAV returns. That resulted in the discount widening out just a touch further, though it hasn't been anything too material as that's been relatively unexciting since our last update too. It still remains one of the most attractive multi-sector bond fund discounts in the entire CEF universe.

Ycharts

As I jested in the last update, " Slap "PIMCO" on the front of this fund and cut distribution coverage to a precarious level, and we could possibly be trading at a premium. "

But again, a new fund, so everyone ignores it, and to be fair, we are still in an uncertain interest rate environment. Higher rates leading to higher yields have helped this fund in terms of producing income, but it also can lead to a tougher economic environment, and it still hurts the underlying portfolio. The effective duration for this portfolio comes in at 5 years.

That means for every 1% change in interest rates - lower or higher - WDI's underlying portfolio should move roughly 5%. Every 25 basis points could shift the underlying portfolio by roughly 1.25%, which is why we saw the fund's share and NAV collapse through 2022 - just as all other fixed-income did. In fact, it was higher quality and longer maturity portfolios that carried higher interest rate sensitivity that did even worse.

Ycharts

Factoring in the distribution in total returns would have dampened the damage from the January 1, 2022, to date performance materially.

Ycharts

I initially turned bullish on WDI in July 2022 - which proved to be too early. If I had waited for October lows, a better deal would have resulted.

WDI Performance Since Prior Update (Seeking Alpha)

The fund noted in the latest report that they were able to outperform their benchmark through this six-month period as well.

For the six months ended June 30, 2023, Western Asset Diversified Income Fund returned 7.85% based on its net asset value ("NAV") i and 12.28% based on its New York Stock Exchange ("NYSE") market price per share. The Fund's unmanaged benchmark, the Bloomberg U.S. Corporate High Yield - 2% Issuer Cap Index ((USD)) ii , returned 5.38% for the same period.

High Distribution Yield With Solid Coverage

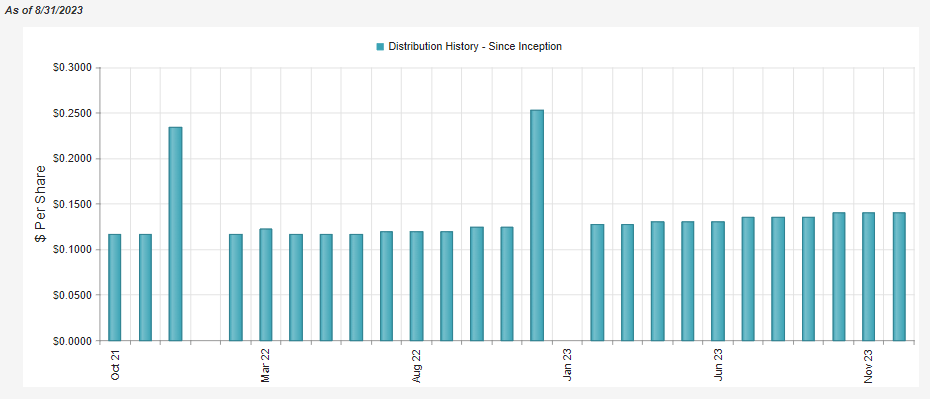

The latest distribution announcement gave us another increase to $0.14 per month from $0.135. This is now the sixth increase for the fund since it launched.

WDI Distribution History (CEFConnect)

{kind=link}

These increases have been supported by an increasing net investment income that the fund is able to generate from its underlying portfolio.

WDI Semi-Annual Report (Western Asset)

On a per-share basis, the NII went from $1.59 in fiscal 2022 to $0.86 in the latest six-month report. If we annualize that out, we'd come to $1.72. However, the trajectory would actually mean we should be higher than this annualized amount.

What this latest report shows us is that NII came in at $0.86 for the six-month period. Western Asset also provided a quarterly financial report previously that showed NII was at $0.41 for the first quarter of the year. That means the latest quarter gave us NII of $0.45, resulting in an increase of 9.76% over the last quarter. Last year NII came in at $0.77 for the same corresponding six-month period, which means we saw a 9.09% increase year-over-year.

We could still be looking at another increase from the Fed, and since this report, we also had another 25 basis point bump in July. That should all bode well for coverage and earnings climbing further going forward.

Given this report shows us that NII was $0.86, that would put distribution coverage at 102.38% based on the new distribution rate. If we use the $0.45 of the latest quarter, we would see distribution coverage of 107.14%. This could mean even further increases in the future. However, we are starting to get to the point where peak rates may be in. So, I certainly don't expect another six distribution increases going forward, as we saw in the past period.

The fund sports some strong distribution coverage even as its distribution is increased, which is precisely why we've been seeing an increase in the distribution. However, the fund's derivatives have also been mostly positive contributors to the fund's performance, negating some of the realized losses the portfolio experienced. During this report, NAV increased due to unrealized gains that completely offset the realized losses.

WDI Realized/Unrealized Gains/Losses (Western Asset)

{kind=link}

We discussed the tax breakdown in a prior update but will reiterate it for those who may have missed it:

For tax purposes, WDI's distributions were classified as ordinary income in both 2022 and 2021. Since it's a fixed-income fund, this is naturally the case, and it would suggest holding in a tax-sheltered account would be the most appropriate.

WDI Distribution Tax Classifications (Western Asset)

{kind=link}

WDI's Portfolio

WDI runs a fairly consistent portfolio that emphasizes high-yield credit. Given the average weighted life of the portfolio comes in at a fairly high 13.13 years, that's why we see effective duration fairly high, too, at 5 years. However, the fund's exposure to bank loans and collateralized loan obligations is going to be based on floating rates to help offset the fixed-income portion of its portfolio.

WDI Portfolio Asset Allocation (Western Asset)

Turnover in the last report came to 14%, which is reflected in the fact that we haven't seen too much change in terms of this allocation for the fund since our last update. Again, my primary reason for putting an update on WDI comes from wanting to touch on the distribution coverage and another increase in the distribution.

WDI emphasizes a higher allocation to below-investment-grade fixed-income investments. That isn't too unusual for most multi-sector bond CEFs. This is also consistent with where we've seen the fund previously, and it's consistent with its "high-yield" credit focus.

WDI Portfolio Credit Quality (Western Asset)

However, it should be noted that this may not always be the case. The fund is looking to allocate dynamically and has an incredible amount of flexibility. It will be up to the manager to see if she can navigate through various environments.

Under current market conditions, the Fund anticipates it will initially focus on shorter-duration and floating rate securities, which have lower sensitivity to higher interest rates. The Fund's duration and mix of fixed and floating rate investments is subject to change over time. As market conditions change, Western Asset will seek to dynamically rotate investments into sectors and securities that it believes to be undervalued from a fundamental perspective with an attractive return profile and away from investments that it believes to be overvalued. The Fund will provide exposure to residential mortgage-backed securities ("RMBS") and commercial mortgage-backed securities ("CMBS"), both agency and non-agency, consistent with its investment policies.

The Fund may invest in investment grade and below investment grade corporate debt securities (commonly referred to as either "high yield" securities or "junk bonds"), senior loans, agency and non-agency RMBS and CMBS, government ( i.e. , sovereign) debt (including U.S. government obligations), floating rate securities, bank loans, CLOs, asset-backed securities (whose underlying asset classes include, but are not limited to, equipment leases, solar and student loans), private debt and mortgage whole loans.

The fund goes with the usual high-yield strategy of investing in hundreds of positions; however, at 301 holdings, it's well below its benchmark that carries 1959 holdings. This is a strategy employed so that no one position is going to have a material impact on the fund. If a position defaults or the company goes bankrupt, the damage should be minimal. Of course, if we see defaults tick up across the board due to an economic slowdown or rates now being higher, that will still negatively impact the fund as a whole.

This diversification is reflected in the top ten positions where no position carries an overly large weight. In fact, by the seventh largest holding in the fund, we are already under a 1% allocation.

WDI Top Holdings (Western Asset)

{kind=link}

Conclusion

WDI has been raising its monthly distribution with the announcement in early August, giving us the sixth increase since inception. This has been driven by an increasing amount of income the portfolio has been generating. All fixed income was demolished in 2022, and WDI more so due to being leveraged.

However, with interest rates looking like they could be nearing a peak, we should see yields also stabilize. That should bode well for this fund in terms of the underlying portfolio volatility. Admittedly, that can come with the downside of not seeing as many distribution increases going forward, as the income generated would also start to top out. That said, we've already seen some stabilization start to take place, as the fund has been rebounding this year with positive performance. At the same time, the fund's discount remains incredibly attractive.

For further details see:

WDI: Attractive Discount, ~12% Distribution Yield, And Solid Coverage