WDI - WDI: Latest Financials Continue To Support Strong Distribution

2023-12-13 11:49:46 ET

Summary

- Western Asset Diversified Income Fund has posted strong Q3 2023 financial results, showing once again a fully supported distribution from net investment income.

- The fund carries a portfolio that consists of mostly below-investment-grade issuances, but it is diversified across hundreds of holdings and instruments.

- With the possibility of rate cuts in the future, distribution coverage may come under pressure, but most do not anticipate aggressive cuts (i.e., not returning to a zero rate environment).

Written by Nick Ackerman, co-produced by Stanford Chemist.

Western Asset Diversified Income Fund ( WDI ) posted their latest Q3 2023 financial results. Once again, it showed that the distribution is well-supported, even after the fund's recent distribution increase; this was their fourth distribution bump in the last year. Combine that with the fund's discount, and WDI remains a solid fund for one to consider for their high-income portfolio.

Of course, the leverage in the fund should be considered before jumping in, as it means potentially greater returns, but it comes with greater volatility and further risk for losses overall, too. The fund has also been able to ramp up its distribution primarily because of the rising rate environment.

With Fed rate increases all but assuredly done for this rate hiking cycle, it means that we should probably get more comfortable around this payout level. In other words, I wouldn't anticipate four increases to repeat over the next twelve months.

In fact, the talk is about rate cuts now. If rates are cut meaningfully, then distribution coverage going forward could start to come under pressure. However, most aren't predicting aggressive cuts - at least not if the economy continues to perform well.

The Basics

- 1-Year Z-score: 0.90

- Discount: -9.54%

- Distribution Yield: 12.30%

- Expense Ratio: 1.65%

- Leverage: 32.16%

- Managed Assets: $1.11 billion

- Structure: Term (anticipated liquidation date, June 24, 2033)

WDI's objective is "to seek high current income. As a secondary investment objective, the fund will seek capital appreciation." They will bring a "flexible and dynamic" approach. They anticipate doing this by rotating sectors and securities in response to market conditions, focusing on what we believe are undervalued securities with attractive fundamentals.

Latest Financial Figures

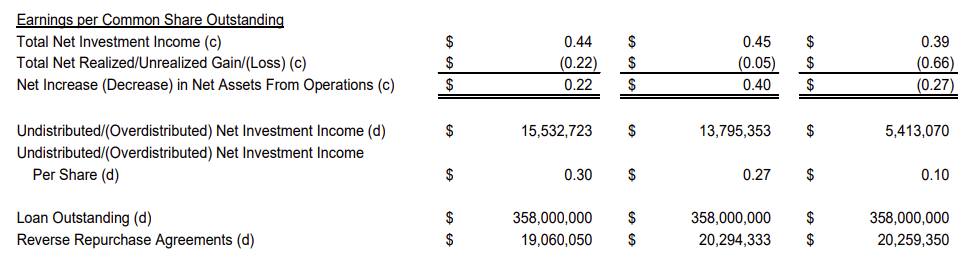

In the latest press release showing how the fund performed in Q3 2023, we see that net investment income once again was covering the distribution. The latest quarter showed a negligible sequential decline from the prior quarter, but year-over-year, the fund's NII rose materially at a nearly 13% increase. The small sequential decline could have been some rounding as well.

{kind=link}

The undistributed net investment income rose year-over-year and quarter-over-quarter as well. That's another indication that the fund was earning its payout during this time.

The quarter that's actually being reflected in the above is for the three months ended September 30, 2023. During that period, the fund paid a distribution of $0.135 for two months before increasing it to $0.14 for the final month of the quarter. Ultimately, during this period, the fund had a cumulative payout of $0.41; thus, we arrived at $0.03 of additional UNII accumulating in the fund.

Given the fund has once again increased the payout more recently to $0.143 monthly or $0.429 per quarter, we are still seeing a fully covered distribution at 102.6%. There were no increases in interest rates from the Fed during this period, meaning that we shouldn't see that being a significant factor in driving yields higher going forward.

On the other hand, if they are turning over their portfolio and making moves to higher-yielding instruments, that could drive yield generation in the fund higher.

That being said, at this point, I think we should get pretty comfortable that most of the increases are behind us as long as the Fed doesn't have to return to hiking mode. Given the fund sports a distribution rate of 12.30%, I'd say this is more than a comfortable place if it could settle in. On an NAV basis, the rate comes to 11.13%.

{kind=link}

At the same time, there is some breathing room here if the Fed does have to start cutting rates next year. That would be assuming we aren't in a deep recession, which would likely drive the Fed to have to reduce rates more aggressively.

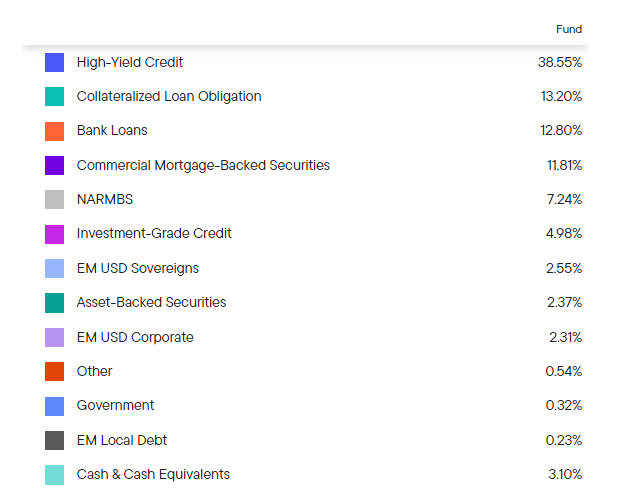

Additionally, being a high-yield or "junk"-oriented fund, the underlying holdings here are going to be more reliant on a sound financial environment to perform their best. Only around 8% of the fund is rated as investment-grade of BBB or higher.

WDI Credit Quality Exposure (Western Asset)

During the last quarter, they reflect that realized/unrealized gains/losses in the fund came to -$0.22, meaning they did see their underlying portfolio generate losses. So, it certainly wasn't all rainbows and sunshine for the fund during the quarter.

Some of this was the result of the 10-year Treasury Rate rising rapidly, but lower-rated debt that comes with shorter maturities often is less interest rate sensitive. WDI has a duration of 4.98 years, meaning that for every 1% change in rates, the fund would be anticipated to move around 4.98%. That's a fair bit, but relatively speaking, compared to something like the iShares iBoxx Investment Grade Corporate Bond ETF's ( LQD ) effective duration of 8.26 years, it is less sensitive. Below is what we experienced in the three-month run-up in the 10 Year Treasury Rate before it started trending lower.

Instead, credit risks also play a role. Fortunately, defaults have remained rather low, but they have been on the rise and are forecasted to accelerate.

As yields stretch higher, income generation might also increase, but so does the strain on the underlying companies that have to pay that additional cash out. Combining that with the distributions paid we did see NAV per share decline quarter-over-quarter.

Interestingly, the report showed that NAV was at $14.90 (up to $15.10 NAV now at the latest close,) and that's where it last closed at the time of this writing. This looks to be mostly because even as rates have been dropping more recently on the risk-free rate, it's been closer to a round trip as, through October, rates continued to surge before receding just as sharply.

YCharts

All that being said, given the risks here of the uncertain future as we enter 2024, this fund is continuing to trade at a deep and attractive discount. The fund's performance might be down slightly from our last update, but that was mostly from the discount widening a bit further since then.

WDI Performance Since Prior Update (Seeking Alpha)

A large discount can reflect these risks that might come to fruition if the economy takes a downturn. We can see that during the October surge in rates, WDI was driven to an even wider discount. So it's always possible to get a wider discount, but the opposite also appears true. There have been periods where the fund's discount has been narrowing. Ultimately, though, this fund doesn't have a lengthy period of time, making it more difficult to try to establish what might be "normal" for this fund.

Conclusion

WDI's distribution remains well covered and that led to once again the fund bumping up its distribution. However, going forward, it doesn't appear that the fund can rely on the Fed to increase rates, thus driving up the fund's income generation. Instead, portfolio turnover and moves within the portfolio are going to be the primary determining factor of the fund's ability to increase the yield it can potentially generate.

At the same time, with strong distribution coverage, the fund looks like it could sustain some drop in rates from the Fed before coverage falls too dramatically. That's what the most popular consensus seems to be, is that we will get at least some cuts heading through next year.

If rates fall, that could produce some capital gains, therefore offsetting the negative effect of slower income generation. This fund is supposed to be "diversified," after all, so some management skills might be required heading through 2024. That could include a shift from floating rate exposure and locking in some higher fixed-rate yields.

{kind=link}

Overall, given the fund's large discount and attractive distribution yield, I would still view WDI as a worthwhile investment, and their latest quarter hasn't dramatically changed that outlook.

y

For further details see:

WDI: Latest Financials Continue To Support Strong Distribution