MPLX - WDI: This 10%-Yielding CEF Is Worth Considering To Add Diversity To Your Portfolio

Summary

- WDI invests in a portfolio of fixed-income securities that are intended to provide investors with a high level of current income.

- The fund has significantly underperformed a few of the major fixed-income indices over the past year, which is disappointing.

- The fund's assets are very different than most other income-focused funds so it can help reduce concentration risk in a portfolio.

- The fund can sustain its 10.86% distribution yield solely out of net investment income so it should be reasonably safe.

- The fund is trading at a fairly attractive discount to the net asset value.

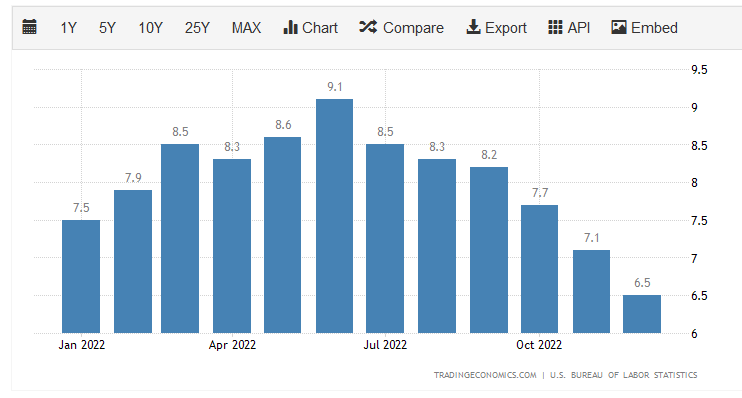

Without a doubt, one of the biggest problems facing most Americans today is the incredibly high level of inflation that has prevailed across the economy. Indeed, the country has not seen a single month this year in which the consumer price index was not at least 6.5% higher than in the prior-year month. In fact, during most months, the index increased substantially more on a year-over-year basis:

{kind=link}

That is substantially higher than the 3.29% year-over-year rate that has been the average since 1914. It also represents a 40-year high. This inflation has been most pronounced in necessities such as food and energy, so it has had a devastating effect on low-income households. In fact, according to Goldman Sachs , many households will have exhausted the $2.7 trillion that they managed to save in aggregate due to the lockdowns and government stimulus in response to the pandemic by the end of the year. We have also seen a surge in the number of people seeking out second jobs or entering into the gig economy in an effort to obtain the extra money that they need to cover their bills and feed themselves. This is likely one contributing factor to the consistently strong jobs reports despite massive layoffs across a variety of sectors.

Fortunately, as investors, we have the advantage of putting our money to work for us and do not have to resort to such methods in order to get the extra money that we need to cover our own rising consumer expenses. One of the best ways for us to do this is to purchase shares of a closed-end fund that is focused on the generation of income. This is because these funds provide easy access to a professionally-managed portfolio of assets that can usually deliver a higher yield than any of the underlying assets possess.

In this article, we will discuss the Western Asset Diversified Income Fund ( WDI ), which is one closed-end fund that falls into this category. This fund boasts a very impressive 10.86% yield as of the time of writing, which is well above the 1.54% yield of the S&P 500 Index ( SPY ) and is certainly enough to allow it to provide us with a large amount of income. Unfortunately, most funds that have a yield above 10% are at fairly high risk of a distribution cut so we will need to investigate that as part of our analysis. Fortunately, this fund is currently trading at a fairly attractive price so it does have a nice margin of safety. Therefore, let us investigate and see if this fund could be a worthy addition to your portfolio today.

About The Fund

According to the fund’s webpage , the Western Asset Diversified Income Fund has the stated objective of providing its investors with a high level of current income. This is hardly surprising considering that the fund’s name alone indicates that it will be focusing on income. In addition, the generation of income is the typical objective of funds that invest in fixed-income securities, such as this one. In fact, the fund has almost no exposure to anything that is not either a bond or a preferred stock:

CEF Connect

There will undoubtedly be some investors that notice that the fund’s bond weighting is significantly above 100% of its assets. This is because the fund utilizes leverage, which we will address later in this article. The most important thing for right now is the fact that it is clearly focused on investing in fixed-income securities. These securities are generally purchased for those that are seeking income as their potential for capital gains is quite limited. The reason for this is that these securities have no link to the growth and prosperity of the underlying company. After all, a company will not increase the amount that it pays to its creditors just because its profits go up. As such, bonds and fixed-income securities deliver essentially all of their returns through direct payments to their investors.

Fixed-income securities are generally priced based on interest rates, which gives them the limited potential for capital gains that everyone reading this is no doubt familiar with. In short, when interest rates increase, fixed-income prices go down and vice versa. The reason for this is that newly issued securities will carry a yield that is dependent on the prevailing interest rate in the market. Thus, during a period of rising interest rates, existing securities will have lower interest rates than brand-new ones so nobody will buy the existing security when they could buy an otherwise identical brand-new one and get a higher yield. Thus, the market value of existing securities will decline when interest rates rise so that they deliver the same effective yield-to-maturity as a newly-issued security with otherwise identical characteristics.

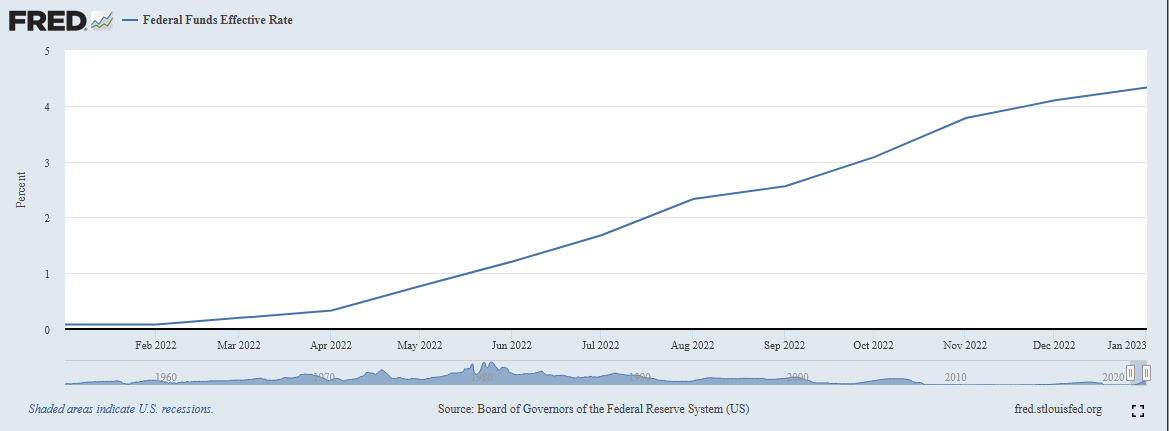

The reason that this is important is that the Federal Reserve has been aggressively increasing interest rates over the past year in an effort to combat the high level of inflation that we see across the American economy. In February 2022, the effective federal funds rate was 0.08% but today it sits at 4.33%:

{kind=link}

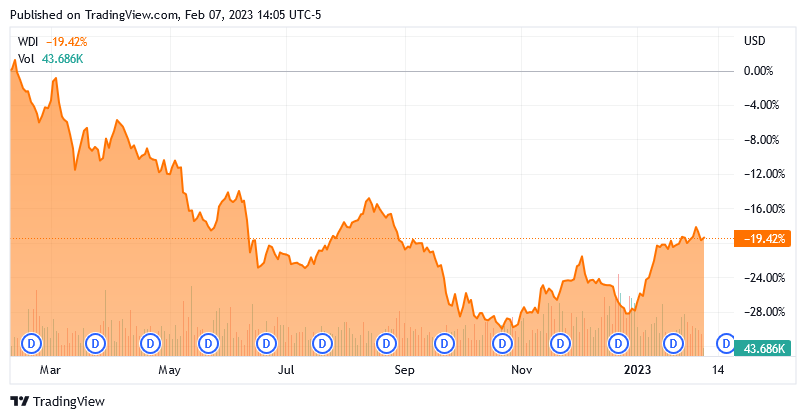

This has had a devastating effect on fixed-income prices. Over the past year, the Bloomberg U.S. Aggregate Bond Index ( AGG ) has fallen by 10.14% and the ICE Exchange-Listed Preferred & Hybrid Securities Index ( PFF ) has fallen by 7.87%. This has had an effect on the Western Asset Diversified Income Fund as well, which is likely expected due to the fund’s focus on investing in securities that will be included in these two indices. The closed-end fund is down a whopping 19.42% over the past year:

{kind=link}

Clearly, this fund has underperformed the broader market indices by quite a lot. Although the closed-end fund does boast a much higher yield, that is not sufficient to make up the difference. Thus, an investor in either of the indices would have more money today than if that investor had purchased shares of the fund. This is disappointing, but it is not exactly unusual for a closed-end fund to underperform a passive index fund, either.

One reason why many actively-managed funds struggle to beat the indices is that they engage in a significant amount of trading. It costs money to trade bonds, preferred stocks, and other assets, which are billed to the fund’s shareholders. This creates a drag on the fund’s performance and makes things more difficult for management because they need to generate sufficient returns to cover these added expenses and still have enough left over to satisfy the shareholders. With that said, the Western Asset Diversified Income Fund only has an annual turnover of 19%, which is not particularly high for a fixed-income fund. Thus, it does not appear that there is a big drag on the fund’s performance due to high trading costs.

A look at the largest positions in the fund does reveal that its portfolio is substantially different than the indices, however. Here they are:

CEF Connect

The first thing that we immediately see here is that this fund does not include any Treasury or agency securities in its largest positions. This is somewhat atypical for a bond fund as U.S. Treasuries are an outsized portion of the bond market. They are generally considered to be safer than other bonds so in times of uncertainty, investors will flock to these bonds, frequently causing them to outperform corporate bonds. This is likely one reason for the underperformance of this fund versus the indices over the past year.

One interesting thing here is that we see some preferred securities issued by pipeline operators. For example, we have the MPLX ( MPLX ) Series A Preferreds ( MPLXP ) and the Rockies Express Pipeline Preferred units. We do not see these securities very often in a fixed-income fund. A bond fund tends to include substantial exposure to U.S. Treasuries and agency securities while a preferred stock fund tends to focus on preferred stock issued by banks. It is nice to see though, particularly the MPLX preferreds as MPLX has long been one of the best midstream master limited partnerships on the market, as subscribers to Energy Profits in Dividends are very well aware. The fund’s fact sheet does state that this fund does have the ability to invest in private debt and other non-traded fixed-income securities so that should be an indication that this fund will invest in somewhat different securities than other funds do. The fact that the largest positions are in companies that we do not often see represented in fixed-income closed-end funds is further evidence of that.

The fact that this fund invests in different securities than many other closed-end funds is quite nice because it helps to reduce our concentration risk. Concentration risk refers to the fact that most funds hold the same or very similar securities. As a result, an investor in several different funds may believe that they hold a diversified portfolio but they actually do not because all of the funds are investing in the same things. The fact that this fund includes different assets means that including it in your portfolio helps to reduce your overall risk because a smaller percentage of your assets will ultimately be invested in any single issuer.

The Western Asset Diversified Income Fund also invests somewhat more aggressively than the indices. We can see this by looking at the credit ratings of the securities in the fund’s portfolio, which consist of a great many speculative-grade securities:

Franklin Templeton

An investment-grade bond is anything rated BBB or above. As we can clearly see, that is only 3.92% of the portfolio. The remainder of these securities consists of speculative-grade issues, which are colloquially known as “junk bonds.” This is something that may be concerning to more risk-averse investors since we have all heard that issuers of these securities are at a fairly high risk of default. However, we can see that 61.27% of the portfolio is invested in securities rated either BB or B by the major rating agencies. According to the official bond rating scale , a company whose securities have this rating has a strong enough balance sheet to weather short-term economic disruptions without serious problems. Although these companies may be challenged by long-term economic problems, the United States has not experienced a situation like that since the Great Depression. Thus, the majority of the portfolio seems to be invested in reasonably safe securities and when we combine this with the fact that the fund has 311 separate positions to spread its risk, investors in the fund should be reasonably protected against losses due to defaults.

Leverage

As stated in the introduction, closed-end funds like the Western Asset Diversified Income Fund have the ability to utilize certain strategies that can boost their portfolio yields above that of any of the underlying assets. One of the strategies that are employed by this fund is the use of leverage. Basically, the fund borrows money and then uses that borrowed money to buy bonds and preferred stock. As long as the purchased assets carry a higher yield than the interest rate that the fund has to pay on the borrowed money, the strategy works pretty well to boost the overall yield of the portfolio. As the fund is capable of borrowing money at institutional rates, which are significantly lower than retail rates, this will usually be the case.

However, the use of debt is a double-edged sword. This is because leverage boosts both gains and losses. This is therefore another possible reason why this fund has underperformed the indices as severely as it did over the past year. As a result of this, we want to ensure that the fund is not employing too much leverage since that would expose us to too much risk. I do not generally like to see a fund’s leverage above a third as a percentage of its assets for this reason. Fortunately, the Western Asset Diversified Income Fund is satisfying this requirement as its levered assets comprise 32.77% of the portfolio as of the time of writing. Thus, the fund is overall striking a reasonable balance between risk and reward, although some readers might prefer a lower leverage level that would allow its share price to hold up a bit better in the market.

Distribution Analysis

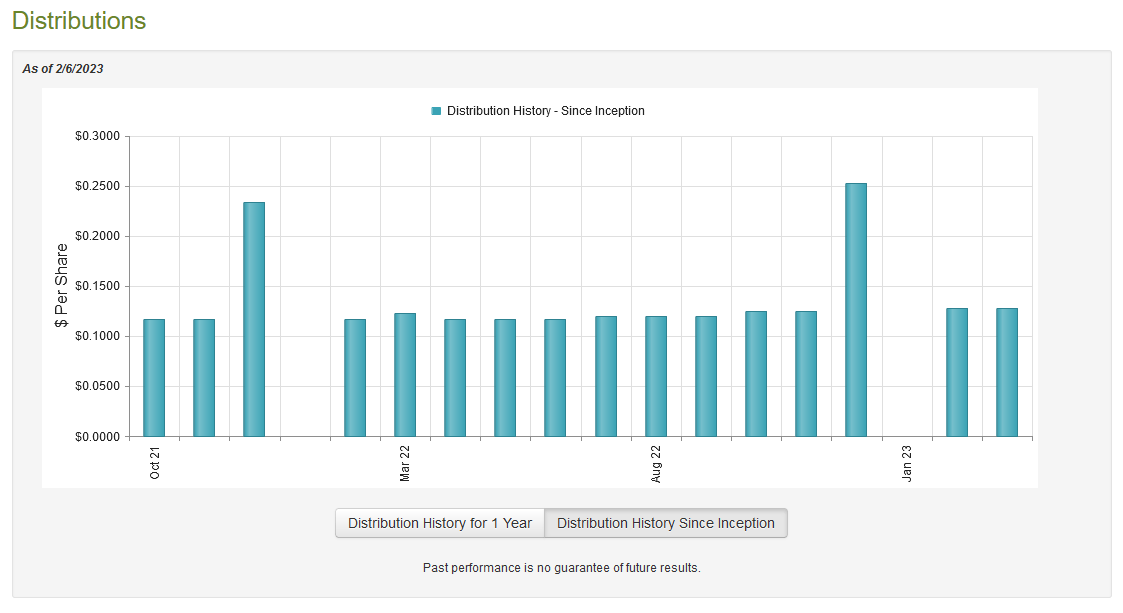

As stated earlier in this article, the Western Asset Diversified Income Fund has the objective of providing its investors with a high level of current income. In pursuit of this strategy, the fund is investing its assets in a variety of high-yield bonds and preferred stocks and then applying leverage in order to boost the effective yield. As a result, one might expect that the fund is able to boast a respectable distribution yield. This is certainly the case as it currently pays out a monthly distribution of $0.1280 per share ($1.536 per share annually), which gives it a 10.86% yield at the current price. This fund is fairly new and only has a limited history, but the distribution has varied a bit over its short life:

{kind=link}

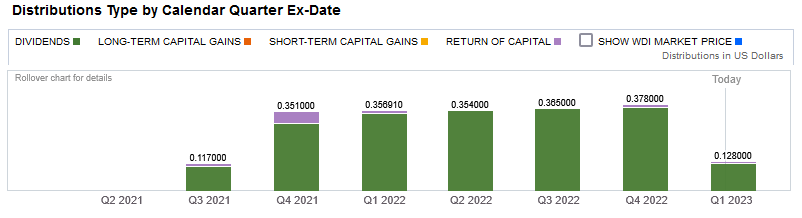

With that said, the fluctuations in the distribution were not really very much and unless you own a very large number of shares, it is unlikely that you would even care about the slight month-to-month differences. The fact that the fund did increase its distribution as we entered 2023 was rather nice to see, though. However, the fluctuating distribution might still reduce the appeal of this fund in the eyes of those investors that are looking for a steady source of income as some other fixed-income funds are able to provide. Fortunately, the fund’s distributions consist entirely of dividend income and include a minimal return of capital or capital gains components:

{kind=link}

The reason that this may be comforting is that dividend income is generally the most sustainable of any distribution types that a closed-end fund can make. This is because a return of capital distribution can be a sign that the fund is returning the investors’ own money back to them, which is obviously not sustainable over any sort of extended period. A capital gains distribution requires that the fund consistently generate high enough capital gains to maintain the distribution, which may not always be possible. A dividend is paid directly out of the interest and dividend income that the fund receives from the assets in its portfolio so it is likely to be sustainable over extended periods. However, as I have pointed out in the past, it is possible for these distributions to be misclassified. As such, it is important for us to investigate exactly how the fund is financing its distributions so that we can determine how sustainable they are likely to be.

Unfortunately, we do not have an especially recent document to consult for that task. The fund’s most recent financial report corresponds to the six-month period that ended on June 30, 2022. As such, it will not include any information about the fund’s performance over the past several months. However, the Federal Reserve began hiking interest rates in March so this report should still be able to provide us with insight into how well the fund handled that situation. During the six-month period, the Western Asset Diversified Income Fund received a total of $49,067,087 in interest along with $1,420,847 in dividends from the assets in its portfolio. This gives the fund a total income of $50,487,934 during the period. The fund paid its expenses out of this amount, which left it with $39,956,332 available for the shareholders. This alone was sufficient to cover the $36,510,688 that the fund paid out in distributions during the period. Thus, it does appear that the fund is generating enough money solely through the payments that it receives in order to cover its distributions and we do not really have to worry too much here. The fund did suffer both realized and unrealized losses during the period but as bond payments do not vary with the price of the bond, we should not really have to care. It appears that this fund is simply paying out its net investment income.

Valuation

It is always critical that we do not overpay for any asset in our portfolios. This is because overpaying for any asset is a surefire way to generate a suboptimal return on that asset. The usual way that we value a closed-end fund like the Western Asset Diversified Income Fund is by looking at its net asset value. The net asset value of a fund is the total current market value of all the fund’s assets minus any outstanding debt. It is therefore the amount that the shareholders would receive if the fund were immediately shut down and liquidated.

Ideally, we want to purchase shares of a fund when we can acquire them at a price that is less than the net asset value. This is because such a scenario implies that we are buying the fund’s assets for less than they are actually worth. This is certainly the case with this fund today. As of February 6, 2023, the Western Asset Diversified Income Fund had a net asset value of $15.58 per share but the shares only trade for $14.21 each. This gives the shares an 8.79% discount to the net asset value at the current price. This is very much in line with the 8.77% discount that the shares have traded at on average over the past month so the price is certainly right today.

Conclusion

In conclusion, the Western Asset Diversified Income Fund certainly lives up to its name as the fund’s assets are very different from most other fixed-income funds in the market. This works out pretty well for anyone that needs to achieve diversity in a portfolio that includes a number of other funds, many of which probably contain the same assets. Unfortunately, the fund’s leverage has been a major contributor to its underperformance against various market indices. The fund should be able to maintain its very attractive yield and boasts a reasonably attractive valuation though so it is certainly worth considering.

For further details see:

WDI: This 10%-Yielding CEF Is Worth Considering To Add Diversity To Your Portfolio