PYPL - We Called Shopify's $1.7 Billion Q3 2023 Revenue Here's Our Prediction For Q4

2023-11-02 09:30:43 ET

Summary

- Shopify Inc. posted a strong double beat in Q3 in line with our previously discussed expectations, underscoring a swift and solid comeback from its 2022 struggles.

- The combination of robust merchant uptake of Shopify's expanding ecosystem of commerce solutions and massive increase in operating leverage mitigates its exposure to inherent business sensitivities to ongoing macroeconomic uncertainties.

- Paired with its relentless market share gains and improving GMV take-rates, the stock's latest pullback makes a compelling entry opportunity to partake in Shopify's organic growth roadmap.

Shopify Inc. (SHOP) shares have fallen more than 20% since our last coverage , but regained momentum earlier this week after rival PayPal Holdings ( PYPL ) posted a better-than-expected quarter and markets cheered on a seemingly dovish Fed. The upsurge was further reinforced by Shopify's solid Q3 results released today, with a double beat that underscores a sustained increase to operating leverage and monetization of total addressable market ("TAM")-expanding opportunities in commerce solutions as discussed in the previous coverage.

Despite ongoing uncertainties over the consumer spending backdrop as inflationary pressures persist while borrowing costs remain at historical highs, Shopify's latest results continue to demonstrate company-specific strengths, spanning robust merchant uptake of solutions offered and sustained margin expansion through improving operating leverage. Taken together, the stock's latest pullback creates a compelling entry opportunity to partake further in Shopify's longer-term organic growth prospects.

Shopify's Relentless Market Share Gains

As discussed in our previous coverage on the stock, Shopify continues to benefit from an expanded TAM within commerce solutions through its comprehensive portfolio of offerings spanning online payments, merchant financing, and more recently, offline POS and B2B services. And this was evident in the company's Q3 results , with Plus subscribers expanding further from Q2, and GMV expanding 22% y/y to $56.2 billion (GPV +31% y/y to $32.8 billion).

Shopify Plus

The results are consistent with our expectations for increasing merchant stickiness, particularly in Shopify Plus following the price increases implemented earlier this year. Specifically, Shopify has continued to observe minimal churn, with many existing merchants - large and small - choosing to up-tier from the lower-priced plans to Plus instead to partake in better value-for-money economics. While Shopify does not separately disclose data pertaining to its merchant count by subscription tier, independent market data estimates 7% y/y growth in Plus merchants during Q3, similar to the 8% expansion observed in Q2. This has accordingly bolstered Shopify's monthly recurring revenue ("MRR") in Q3, which expanded 32% y/y in line with consensus estimates to $141 million. More than a third of this amount was attributable to Plus merchants, underscoring Shopify's strength in monetizing on upmarket opportunities.

Strong adoption of Shopify Plus among merchants has also benefitted Shopify Payments, which was a core driver of GMV growth in the quarter and represented a penetration rate of 69% (vs. 58% in Q2). In addition to Shopify Plus, adjacent offerings such as Shop Pay checkout and Shopify's emerging offline POS business were also key contributors to Shopify Payments penetration during the quarter. Independent market data estimates Shop Pay adoption grew by 21% y/y in Q3 (vs. +18% y/y in Q2 and +6% y/y TTM average), with management disclosing an increase in the feature's facilitated GMV during the quarter compared to $11 billion in Q2. This has continued to reinforce Shop Pay's growing market share in the branded checkout segment, with its penetration rate exceeding 69% during Q3, making it the "fourth most commonly available wallet at Shopify merchants" after PayPal, Amazon Pay ( AMZN ), and Apple Pay ( AAPL ).

{kind=link}

Buy With Prime

We believe Shopify's integration of Buy With Prime during the quarter was another tailwind to GMV, as well as its take-rate economics (discussed in later section). Recall that the formal partnership between Shopify and Amazon entered into on August 30 requires Shopify merchants that have integrated Buy With Prime to process the related transactions through Shopify Payments. This official endorsement of Buy With Prime by Shopify has accordingly jumpstarted merchants' adoption of this Amazon fulfilment service - close to 3,000 Shopify merchants now have Buy With Prime integrated into their online store-fronts, up from just under 2,000 in Q2 and a handful of about 130 in Q1.

With the formal endorsement of Buy With Prime at Shopify also coinciding with Amazon's annual Prime Big Deal Days in October and the upcoming holiday shopping season, we expect further merchant integration of the feature in the coming months. This is likely to bring a stronger tailwind to Shopify Payments GMV and take-rates in the current quarter, which is already corroborated by Amazon's confirmation that the October Prime Big Deal Days event was its largest ever, with observations of Prime members taking greater advantage of Buy With Prime outside of Amazon.com.

Shopify's endorsement of Buy With Prime is also likely to benefit from the increasingly price sensitive consumer backdrop given tightening financial conditions. More than 60% of consumers are on the hunt for discounts, and free and fast delivery perks heading into the holiday shopping season, as they look to "spend the least amount of money possible." This is likely to incentivize greater adoption of Buy With Prime among Shopify merchants ahead of the holiday season, which will be accretive to Shopify Payments over the longer-term.

Point-of-Sales

Meanwhile, Shopify's emerging POS business continues to gain momentum in supporting merchants' ongoing transition from offline to hybrid multi-channel business models. Specifically, Shopify POS facilitated continued offline GMV growth during the third quarter, driven by additional multi-location merchant wins from Q2. Incremental features added to the business in Q3 - including the tailored Retail Plan for brick-and-mortar merchants and an upgraded POS Terminal in North America - were also likely value-add drivers encouraging of strong merchant uptake. More than 70% of POS transactions were processed through Shopify Payments in Q3, underscoring increasing stickiness to Shopify's commerce solution ecosystem, which provides reinforcement to its moat. We believe the addition of Shopify POS will remain a key growth driver to long-term MRR, as it expands the company's TAM beyond online opportunities.

Wholesale B2B

In addition to POS, Shopify's expanding wholesale presence is also extending the company's reach into commerce growth opportunities beyond retail merchants and consumers. The company reported accelerating B2B GMV growth in Q3, underscoring a continuation of momentum observed in the 61% expansion through 1H23. We expect this trend to accelerate further over the longer-term, as Shopify's recent stake acquisition in key partner Faire - a B2B marketplace - deepens the integration of its expanding wholesale business with the company's broader ecosystem of commerce solutions, particularly Shopify Payments.

Taken together, Shopify's Q3 results continue to underscore a strengthening moat, which reinforces prospects for further market share gains in the commerce solutions industry. This is already consistent with Shopify's robust merchant net adds in recent quarters. As mentioned in the earlier section, independent market data estimates a 7% y/y growth in Shopify's merchant count during the third quarter, which outperforms the -7% y/y decline observed across its commerce solutions peer group. And this trend has been consistent, with Shopify growing its merchant count by 112% since 2019, doubling the 55% average observed amongst its commerce solutions peer group over the same period. Not only does this consistent pace of outperformance provide validation to the value proposition Shopify offers to its merchants, but it also bolsters visibility into the company's longer-term prospects of sustained market share gains in the business.

Take-Rate Expansion

In addition to GMV and GPV expansion, Shopify has also demonstrated improvements to its take-rate economics driven by strong adoption of its core commerce solutions offerings as discussed in the earlier section. Specifically, robust up-tiering to Plus plans, alongside incremental adoption of recent offerings such as POS and Audiences advertising have been key tailwinds to Shopify's GMV take-rate in recent quarters - or percentage of GMV facilitated that gets realized into merchant solutions revenue.

Merchant solutions revenue as a percentage of GMV in Q3 remained at about 2.2%, in line with the 2.3% observed in 1H23 and expanding from about 2.08% in 2022. This continues to highlight Shopify's ability to monetize from its expanding merchant base through the introduction of new commerce offerings, which have also reinforced the stickiness of its ecosystem and enabled broader market share gains. We believe this is progression in the right direction, improving visibility into the longer-term sustainability of Shopify's profitable growth trajectory, while also mitigating the company's exposure to near-term weakness in the consumer spending environment.

Fundamental and Valuation Considerations

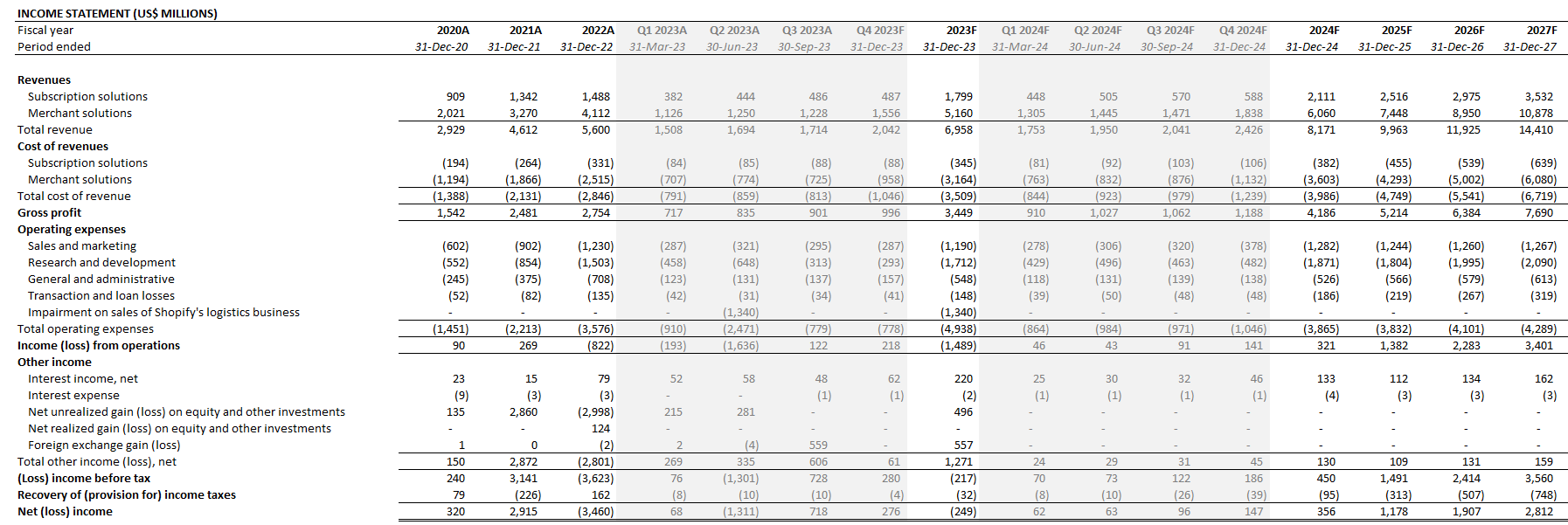

Adjusting our previous fundamental forecast for Shopify's actual Q3 results and its forward outlook based on the foregoing analysis, we expect the company's revenue to expand by 24% y/y to $7.0 billion for full year 2023. Specifically, merchant solutions revenue are likely to accelerate into the upcoming holiday quarter with 27% sequential growth in Q4, offset by some conservatism considering the overhanging macroeconomic risks over the consumer. Specifically, U.S. non-store sales growth slowed to 6.2% y/y in September from 8.4% in August and 10.2% in July, while total retail sales performed stronger than expected in Q3, highlighting a mixed consumer spending backdrop. Taken together with the consideration of plan price increases that went into effect in April 2023, we expect merchant solutions revenue to moderate heading into 1H24, offset by the continued ramp in new service uptakes.

{kind=link}

On the cost front, we expect Shopify to continue on its delivery of increasing operating leverage. This is expected to be realized through improving economies of scale in merchant adoption rates, as well as disciplined operating spend management following the headcount reductions and internal restructuring to leaner operations implemented earlier this year. Specifically, revenue is expected to expand at a 16% CAGR through 2027, while cost of revenue and operating expenses expand at a 9% CAGR (ex-impairment charges related to the Deliverr divestment) over the same period.

{kind=link}

Shopify_-_Forecasted_Financial_Information.pdf .

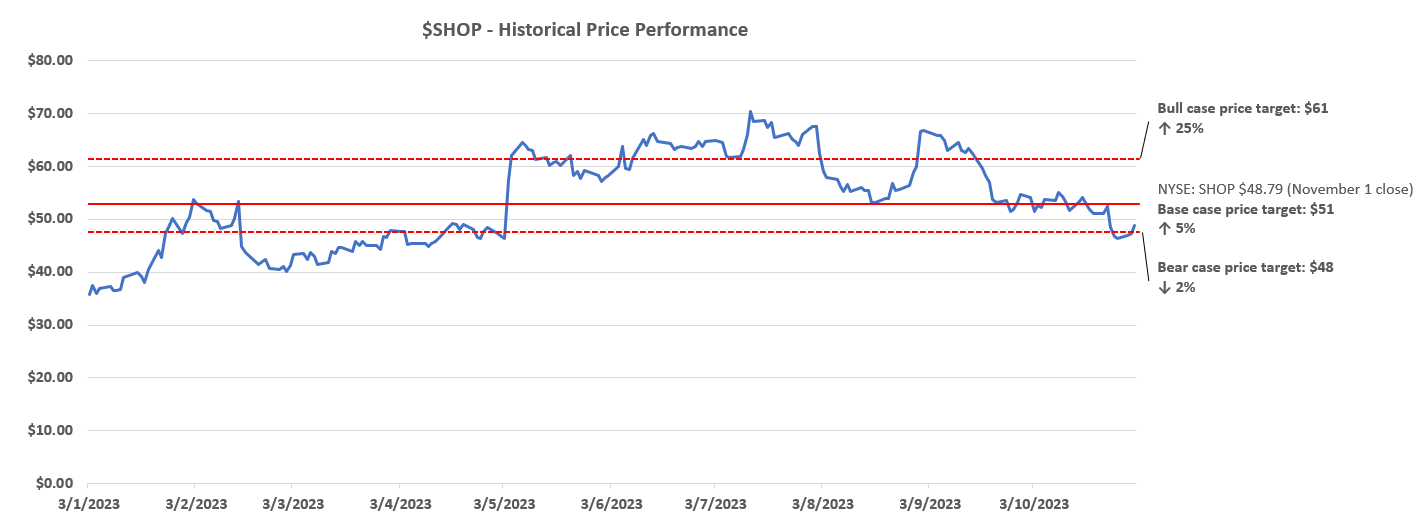

Despite Shopify's positive fundamental progression coming out of the third quarter, we are revising our base case price target to $51 from the previous $64 in light of a heightened normalized interest rate environment.

{kind=link}

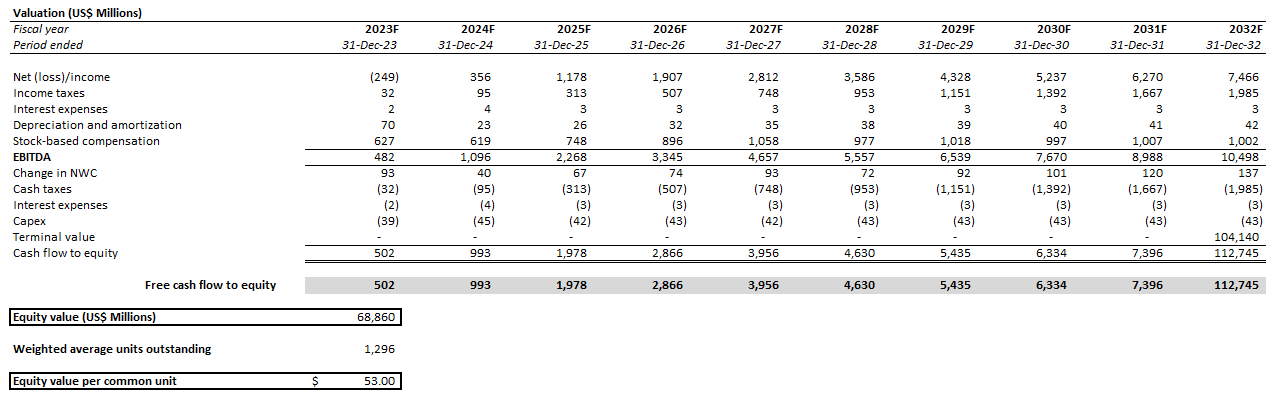

Our base case price target is derived by equally weighing outcomes from the discounted cash flow ("DCF") and multiple-based valuation approach. We believe the chosen valuation method better reflects both the estimated intrinsic value of the company's fundamental performance, as well as market's sentiment on the stock given its inherent sensitivity to ongoing macroeconomic uncertainties.

{kind=link}

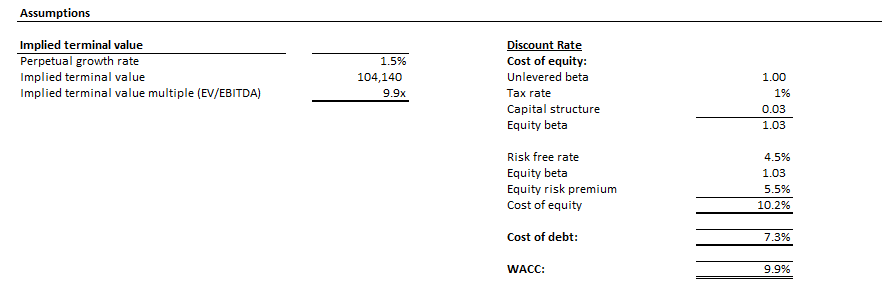

The DCF component takes into consideration the cash flow projections over a 10-year discrete period in line with the fundamental analysis discussed in the earlier section. A 9.9% WACC in line with Shopify's capital structure and risk profile relative to the elevated risk-free benchmark Treasury yield is applied, alongside an implied perpetual growth rate of 1.5% on steady-state terminal cash flows.

{kind=link}

{kind=link}

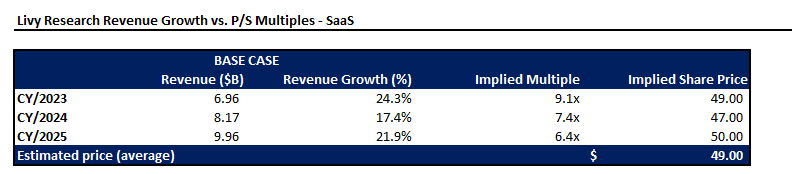

Meanwhile, the multiple-based component takes into consideration the Shopify stock's current performance relative to its SaaS peers, and applies an average 7.7x P/S multiple on the company's projected sales through 2025 (versus SaaS average of 6.0x through 2025). We believe the stock has benefitted from a valuation re-rate this year closer towards its SaaS peers instead of the e-commerce technologies peer group, as Shopify reverts to an asset-light business model with a higher growth and profitability profile.

{kind=link}

Final Thoughts

We believe Shopify's valuation re-rate upwards this year has continued to gain durability. The stock's gains continue to be sustained by Shopify's consistent positive progress in monetizing its merchant base, growing its market share in commerce solutions, and improving operating leverage. This continues to be supportive of return on capital expansion, which is value accretive for the stock. The upcoming seasonality tailwinds, and the eventual cyclical recovery will be accretive to Shopify's recent demonstration of idiosyncratic strengths in improving demand for its ecosystem of commerce solutions and take-rate economics, bolstering further upside potential for the stock from current levels.

For further details see:

We Called Shopify's $1.7 Billion Q3 2023 Revenue, Here's Our Prediction For Q4