NEX - Weather The Recession With This 3x P/E Stock: Liberty Energy

2023-04-24 10:14:29 ET

Summary

- The March trifecta of oil prices in the $60s, crashing natural gas and the banking crisis did serious damage to onshore oilfield services stocks.

- Yet, the fundamentals for Liberty Energy are holding steady; the company beat its Q1 earnings estimates.

- The sell-off has pushed the forward P/E ratio down to 3.59x, which is quite low for a company with little debt.

- OPEC+'s "put" and the demand growth in emerging markets make it less likely that a U.S. recession will bring North American onshore activity to a standstill as in 2020.

- The compressed multiple presents an asymmetric opportunity with significant upside.

Investment thesis

The wait for the most expected recession in history continues. The start date remains unknown: maybe the recession is already here, but maybe it won't arrive until Q4 2023 or even 2024. Consistent with the playbook from prior cycles, the market ( SPY ) has gone after energy stocks ( XOP ):

At the end of the day, energy is a commodity and prices are set at the margin. Even if a recession were to reduce oil demand only by 1-2%, historically prices would have fallen by 5-10% due to supply inelasticity. When the regional banking crisis intensified the fears, the energy segment that got hit really hard was the pressure pumping industry that provide hydraulic fracturing services to onshore producers. Liberty Energy ( LBRT ) was among the casualties:

Besides the recession fears briefly pushing WTI oil ( CL1:COM ) into the $60s, fracking stocks also suffered due to the natural gas ( NG1:COM ) crash:

After surpassing $9 last summer as Europe was scrambling for LNG cargoes, the warm winter and the Freeport LNG outage brought gas back to the $2s. The rising gas oil/ratios for U.S. shale producers may also be a problem as the associated gas isn't really sensitive to the gas price markers.

The mainstream narrative appears to be that gas producers will reduce gas rigs, mostly in the Haynesville basin where gas production tends to be drier. In contrast, companies in Appalachia like Antero Resources ( AR ) enjoy a higher natural gas liquids yield that lowers their dry gas breakeven. The thought is that as rigs and frac fleets come out of the Haynesville and go to compete for work in other basins, the balance will shift from the services companies to the producers and drive rates down.

ProFrac ( ACDC ), a Liberty competitor with higher gas and Haynesville exposure, has indeed done the worst among the group:

{kind=link}

The recession narrative and the gas bear market have pushed LBRT, as well as other pressure pumpers, like ACDC or ProPetro ( PUMP ), deep into value territory. These companies now trade at super discounted multiples, but, unlike 2020, don't really have debt problems. The only justification for the low multiples would be if North American onshore service activity comes to a halt and significantly reduces earnings over the next few years.

Why the mainstream view may be wrong

The mainstream narrative doesn't consider several factors:

- Oil prices may not fall as much this time around; even if U.S. monetary tightening reduces U.S. demand, China is in an expansionary cycle and India is also growing fast.

- OPEC+'s surprise production cuts announcement also boosts the case for U.S. oil production at least remaining flat.

- Many shale producers are running out of Tier 1 inventory; the completions intensity is increasing even under a maintenance scenario.

- Some industry participants believe that even if the Haynesville does slow down, excess capacity can be absorbed by oilier basins where the services markets are still tight.

- It is not given either that activity in the Haynesville will slow that much; while drier, the basin offers LNG export advantages and also many producers are hedged at generous price levels.

- Q1 earnings calls from industry bellwethers Baker Hughes ( BKR ) and Schlumberger ( SLB ) suggest "plateauing" of North America onshore activity; however, plateauing at 2022 levels would actually be a pretty good thing.

- The oilfield services (or OFS) bear market 2014-2020 eroded much capacity, both equipment and labor. With a recession around the corner, no one is going to make major capital investments in the sector, meaning that the current providers will continue enjoying some sort of barrier to entry.

I will dive into more detail below, but the key message is that, at worst, we are dealing with flattening, not declining fundamentals. A 3x P/E ratio is too low even for the flat scenario.

Liberty background

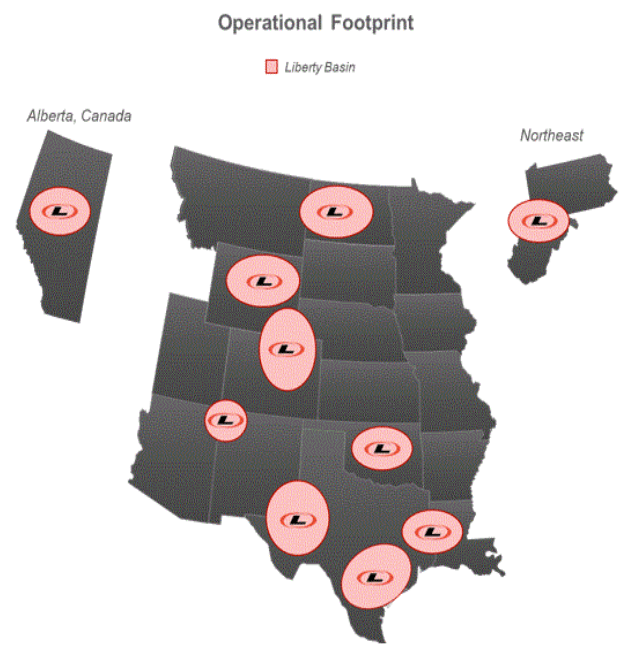

LBRT provides hydraulic fracturing services to onshore oil and gas E&P companies in North America. In addition, Liberty offers complementary services including wireline, proppant delivery solutions, and data analytics. The company operates in most significant U.S. basins and the Western Canadian Sedimentary Basin:

{kind=link}

Some of Liberty's larger customers in recent years have been PDC Energy ( PDCE ), WPX Energy ( WPX ) and Conoco-Phillips ( COP ). The main competitors include the already mentioned ACDC and PUMP, as well as Calfrac ( CFW:CA ) and STEP Energy Services ( STEP:CA ). Integrated OFS giant Halliburton ( HAL ) is also a player in this segment.

While not a well-known retail name, Liberty is actually in the Top 3 by OFS revenue from North America, right after HAL and SLB:

Liberty Energy Investor Presentation

The company is not just competing on cost and service quality, but also seeks to differentiate itself through technology and owns more than 500 patents. Liberty believes its "Quiet Fleet" technology can expand its market share by enabling completions in urban environments while its "digiFrac" pumps that run on natural gas rather than diesel can help operators reduce their carbon emissions.

Like others in the sector, Liberty's profitability has rebounded strongly from the 2020 lows. However, the stock price hasn't quite kept up with the improvement in the business:

The balance sheet has also been repaired and debt to EBITDA is down to only 0.2x:

The EBITDA gains come not just from revenue but from margin expansion too:

A margin in the 20% range is quite good for an OFS company, and LBRT is already there despite trading at lower multiples than companies with lower margins. For example, HAL trades at 11x forward earnings:

But its margin is still short of the 20% mark:

Liberty also just recently beat the Q1 earnings estimates.

The company has 83 job requisitions on its site, which, if filled, would expand headcount by 2%. It is not a lot, but while big tech is laying off personnel, LBRT is still looking to add. Companies expecting reduced demand generally don't expand their workforce.

Q1 earnings and guidance

Q1 was the company's fourth consecutive quarter of record profitability. Another highlight emphasized during the earnings call was the reinstatement of the company's capital return program in July 2022; as of Q1 2023, Liberty has retired 7.1% of its shares and has $300 million remaining in buyback authorizations. This is not chump change; by my rough calculation, that can retire another 13% of the shares at their current price.

Management acknowledges the gas bear market and the coming recession, but believes Liberty's fleets will remain busy, in part due to technological differentiation. They also pointed to the increased quantity of services needed to maintain flat shale production:

North American frac activity predominantly just supports the maintenance of today's oil and gas production levels. The days of breakneck oil and gas production growth are over. The large majority of contract activity is required to simply maintain today's record high oil and gas production levels in the US and Canada.

Service sector margins are now at healthy levels, more in line with our E&P customers that have been experiencing strong margins for many quarters. In this longer, perhaps steadier ahead, there will be episodic challenges like we are seeing today in natural gas markets, and of course, recessionary risks. Today we have excess demand for Liberty Services as our customers want to align themselves with the top performers.

This is part of a broader industry flight to quality trend. We will lead the way in maintaining pricing and profitability as we invest in our digiTechnologies offering and retire older equipment. We believe these actions will support strong long-term returns for both Liberty and our customers. The oilfield is undergoing a transformational change in how frac leads are powered from diesel to natural gas and Liberty is at the forefront of this change .

Management addressed, of course, the expectations for reduced gas activity:

We went from a market, frac market and rig market that was ever tightening to a small pullback, but the magnitude of the pullback is relatively modest , less than 20% of our activity is in gas markets. Maybe 20% of totally industry activities in gas markets. There even if that pulled back by a third, that's a 6% or 7% decline industry-wide in demand for frac fleets.

We already had in oil markets, probably more activity that people wanted to pursue that they were unable to pursue for lack of capacity... So we're going to see a little bit of growth in market share from existing customers that would like to see more of Liberty.

So, LBRT doesn't think it will lose gas fleets, and, even if it does, management is confident oil basins can absorb them. An analyst also probed in the possibility of a worse gas drilling decline, in the order of 30% to 50% reduced activity:

Our [US] exports are going to grow meaningfully. So I think all of that is happening. All of that is positive. Some will be pipeline to Mexico. The bigger chunk will be LNG. So for gas producers, I think they're in a great position, but just productivity just got ahead of export capacity. So, that that happened that will take - that may take as long as the early 2025, where we are going to see a significant growth in demand for gas for growing export markets in the US.

The markets may affirm meaningfully before that as well, we don't know. But again, for us, it's less than 20% of activity, easily deployable elsewhere and we've got great gas customers. So, it's not nothing but it's not hugely significant to the outlook for Liberty’s business over the next, one quarter or two years .

Revisiting the market fundamentals

What do others says

Management appears quite optimistic, but it is important to validate their view against what others in the industry are saying.

COP, singled out as one of LBRT's largest customers, as reported a week ago by the WSJ :

ConocoPhillips expects an average of 7% production growth in the Permian over the next decade...

The company's cost of oil production in the region will average less than $35 a barrel.

The company has "well over two decades" worth of oil inventory in the region.

Despite reports of declining well output in the Permian, the company's drilling efficiency increased by 50% between 2019 and 2022. That was partly due to a lengthening of its wells, over 80% of which are now more than one and a half miles long .

The completion intensity point is also illustrated here:

{kind=link}

Some insights from the Baker Hughes earnings call :

For the full year 2023, we remain positive on the outlook for OFSC. International activity is tracking in line with our expectations, but we now expect North America D&C spending to increase in the low-double digits in 2023 , which is lower than the mid to high-double digit growth expectation that we communicated in January.

Coming into the year, we expected some privates to drop oil rigs early in the year, but that would be gradually offset over the course of the year by the public E&Ps and some majors adding some rigs. The natural gas pricing has been weaker. And so we would expect 30 to 40 rigs also additional to be dropped over the course of 2023.

On the oil side, though, we don't see much risk to the oil activity. If we stay at around $80, we should be able to stay level on the rigs and I don't think we'll see much impact unless we start to go below the $70.

Despite the elevated recession risk for major developed economies, we expect the supply-demand balance in the global oil markets to gradually tighten over the course of the year. Factors driving this include China's economy recovering, non-OECD demand continuing to grow and OPEC+ remaining proactive in maintaining adequate and stable oil price levels.

We continue to believe current environment remains unique with a spending cycle that is more durable and less sensitive to commodity price swings relative to prior cycles.

After its downward revision, BKR still expects double digit growth for North America.

Schlumberger from their Q1 call :

In North America, we still expect tangible market growth but at a lower rate than originally anticipated at the start of the year, mainly as a result of ongoing weakness in gas prices.

Their view seems consistent with that of BKR.

Finally, I wanted to highlight the April 2023 cover story from The American Oil & Gas Reporter, which features the Haynesville and an interview with the CEO of Comstock Resources ( CRK ), one of the largest gas producers there:

“The fact is that 95% of all U.S. LNG shipping capacity is on the Texas/Louisiana Gulf Coast,” Allison explains. He says 10% of U.S. natural gas production is now exported overseas as LNG. That number will more than double in the future, he contends, as Europe becomes more dependent on U.S.-sourced natural gas. The Haynesville Shale is the most economical supply basin because of its close proximity to the Gulf Coast facilities, he reasons.

Allison claims Comstock Resources’ strategy is “completely different” from other companies, as the company is focused on exploration to find reserves while most of its competitors are focused on acquisitions to add drilling inventory.” After laying down two rigs as gas prices have dropped, Comstock still has five rigs operating in the traditional core of the Haynesville/Bossier play and two rigs drilling the deeper wells in the newly acquired acreage in the Western Haynesville...

Allison claims Comstock now has the largest acreage footprint and the largest drilling inventory in the Haynesville with a strong balance sheet and a sector-leading low cost structure. He says Comstock’s break-even Henry Hub price is $2.00-$2.10 an Mcf .

Even if not everyone has Comstock's low breakeven, many gas producers are hedged. Take for example, Chesapeake ( CHK ) which has close to 60% of its production hedged above $3:

{kind=link}

Chesapeake's hedging profile is far from unique among U.S. gas producers.

The activity indicators are steady

Let's also look at the ubiquitous rig count data:

The US gas rig count actually ticked up a bit in the last weeks. It is higher than January, though December 2022 had weather effects, and trending flat since last summer.

The US oil rig count has dropped a bit, but we still have to see the effects of the OPEC+ production cuts :

Canada rig counts have fallen, but it is seasonality driven:

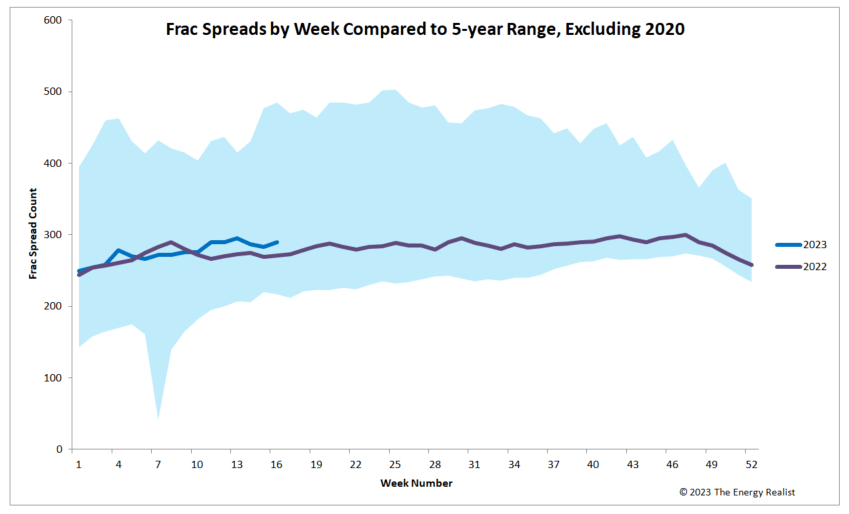

The frac spreads are trending flat and remain above the 2022 levels:

{kind=link}

My 5-year range excludes 2020, so the spreads are comfortably off the lows even against a stronger 2017-2019 benchmark.

In my view, the data suggests 2023 will be flat-ish for onshore OFS. However, flat at the 2022 levels is actually pretty good. Zero percent growth can be a lot when you are valued at three times earnings.

The valuation presents a unique opportunity

The valuation case for Liberty is not just based on comparisons outside of energy; here is how LBRT compares against 31 other OFS companies based on forward estimates from Refinitiv (the table is two weeks old):

Author's Calculations

If you read along so far, this is probably no surprise, but the five most discounted OFS companies are LBRT and its competitors: PUMP, STEP Energy Services ( STEP:CA ), Calfrac ( CFW:CA ) and NexTier Oilfield Solutions ( NEX ).

Note that onshore drillers like Nabors ( NBR ) and Helmerich & Payne ( HP ) are in the 3-4x EV/EBITDA range while LBRT and its peers are in the 1-2x range. ACDC, which as noted is the most gas-exposed peer, actually has a higher EBITDA multiple. This simply doesn't make sense. I don't know what market dynamics have caused this, but my sense is that the pressure pumping stocks should at least normalize to 3-4x EBITDA, which would be a double from here.

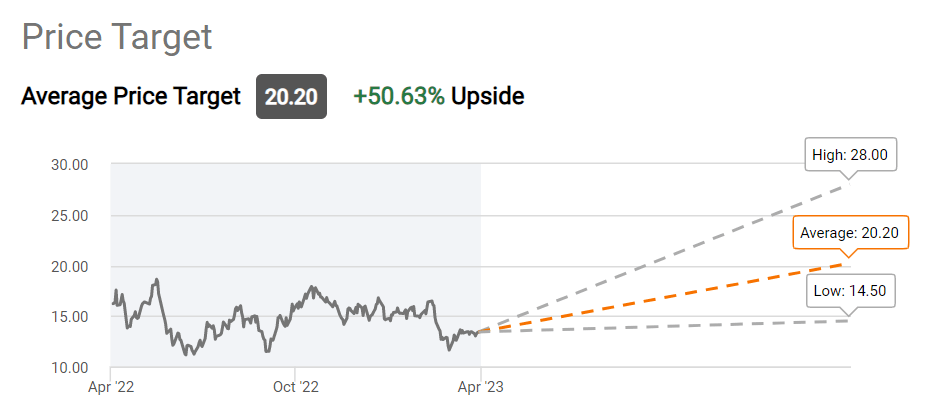

Wall Street gives Liberty a $20 price target for 50% upside:

{kind=link}

I am more inclined to see LBRT as going to the upper $20s in a few quarters or + 100% upside. My view would be consistent with the higher end of the Wall Street targets.

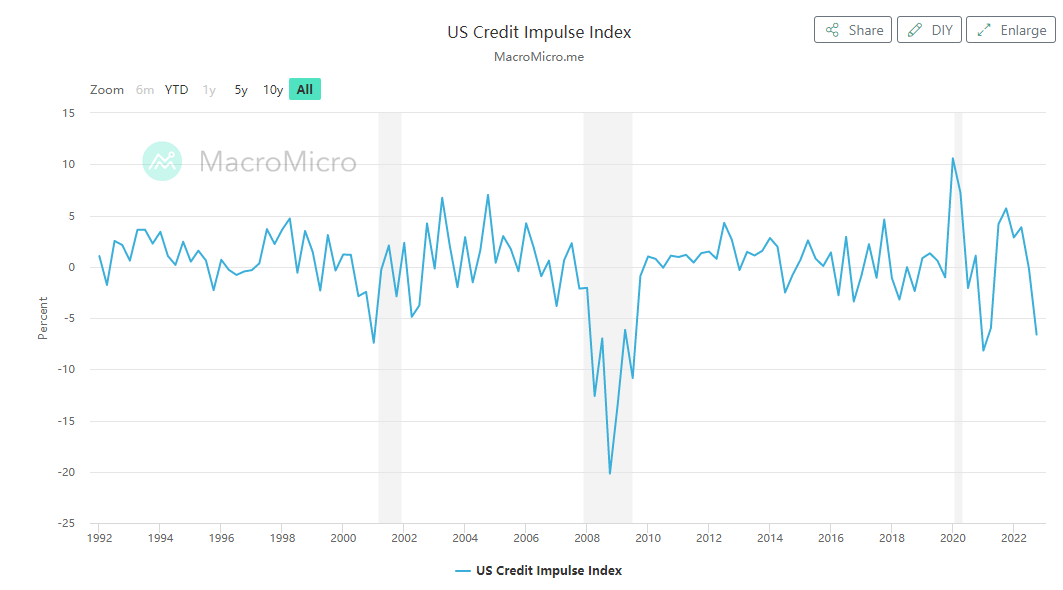

Recession risks and value

As is said, all recessions end the same way, by the Fed inflating credit and re-liquefying the economy. Right now, credit impulse indices don't look good:

{kind=link}

It looks like we are headed for a recession on the 2001-2002 scale rather than 2008-2009, but it is still not good. Possibly based on the 2010-2020 playbook, the baseline expectation of many seems to be that when the Fed reverses the tightening cycle, long-duration growth stocks will get a tailwind and outperform value.

However, that hasn't necessarily been the case historically during actual earnings recessions:

Piper Sandler

Profitability and earnings are factors that have outperformed in such periods. Energy is indeed a cyclical sector, which may suggest underperformance, but the global demand and supply considerations point to a downside that may be more limited in historical perspective.

As a profitable company with little debt, I think LBRT may be a worthy recession investment. There is risk that the 3x P/E multiple compresses even further, but given the already low starting point, I think the opportunity is asymmetric to the upside. To paraphrase Peter Lynch's know-what-you-own principle, if you can get Liberty Energy for 1x P/E, great for you, but even if you buy it at three times earnings, it's still pretty good.

Editor's Note : This article was submitted as part of Seeking Alpha’s Best Investment Idea For A Potential Recession competition, which runs through April 28. This competition is open to all users and contributors; click here to find out more and submit your article today!

For further details see:

Weather The Recession With This 3x P/E Stock: Liberty Energy