WFRD - Weatherford International: I Think We Are Consolidating Here

2023-09-21 11:29:00 ET

Summary

- Weatherford International plc's share price has surged 200% in the past year due to improved financial performance and an optimistic outlook.

- The company is gaining market share and expanding internationally, particularly in Latin America through partnerships like Petrobras.

- While Weatherford's cash position and debt reduction are positive, its valuation is a concern, trading at a significant premium to the sector.

Investment Rundown

The share price for Weatherford International plc ( WFRD ) has run up an astounding 200% in the last 12 months alone. The bull run seems to have come from the rapid improvement the company is seeing in the top and bottom lines and how optimistically the company views its coming years of operations.

WFRD has been very proactive in getting more and more market share and most recently started to partner up with Petrobras for some offshore intervention services. International growth has been very present for WFRD, and it seems to continue this way. However, I think that the massive run-up the share price has had over the last 12 months is due for some consolidation in the short-term at least, with the possibility of a correction. We have to keep in mind that WFRD is trading at a significant premium to the sector, with a p/e of 17. The estimates for WFRD may be very positive, but I think we aren't getting the best possible deal here, and I will as a result rate the business a hold.

Company Segments

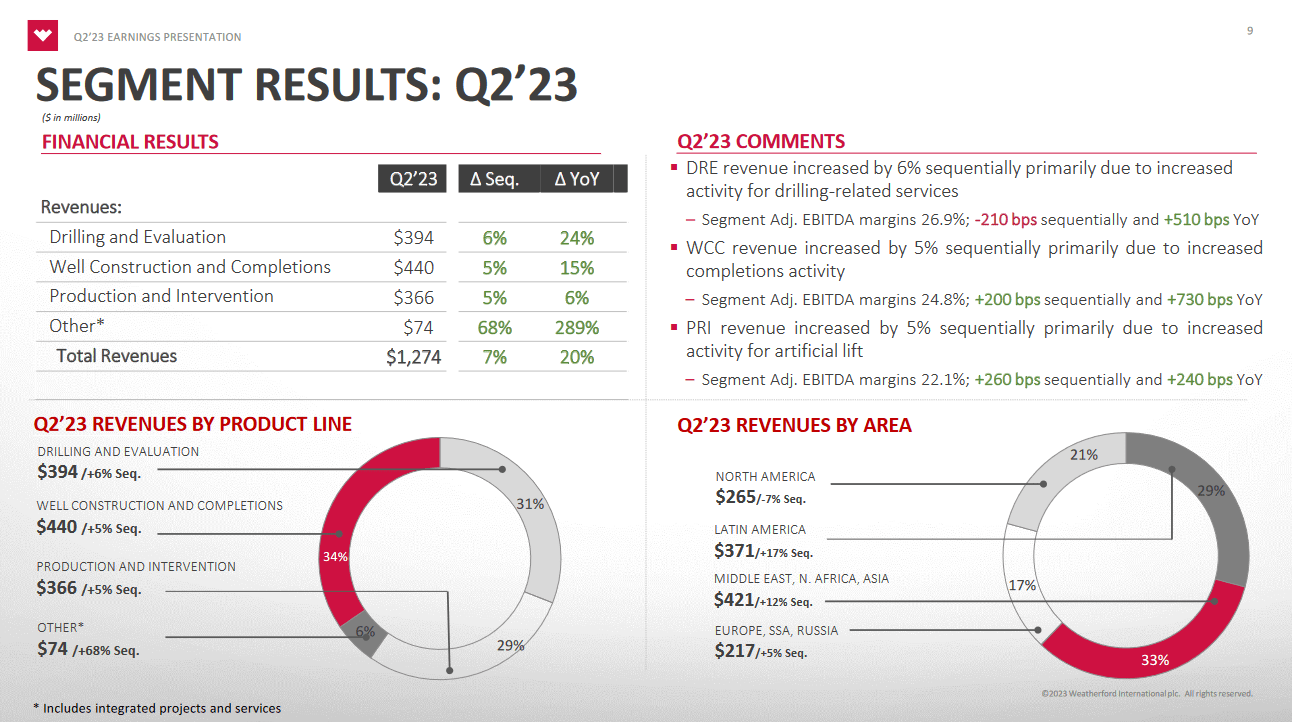

WFRD serves as a pivotal equipment and service provider within the oil and gas industry. The scope of their services encompasses a wide array of solutions, ranging from drilling innovations to the restoration of gas wells and beyond. Notably, WFRD assumes a critical role in offshore drilling operations, and their dominance is most evident in sectors such as Managed Pressure Drilling and Tubular Running Services. This market leadership positions them advantageously, allowing them to tap into revenue streams that exhibit robust growth potential, driven by the industry's high activity levels.

{kind=link}

As I have mentioned earlier, WFRD is experiencing a significant amount of demand from international customers and this has been a main driver behind the growth of the business I think. Going forward, I think this can be maintained. The Latin American market for example has displayed a 17% sequentially growth rate. This is further aided by partnering up with companies like Petrobras. The partnership includes a 5-year contract for WFRD to supply intervention services. WFRD has already been doing these things in Brazil for over 20 years, so the partnership didn't come as a major surprise, WFRD has already made itself quite established here.

{kind=link}

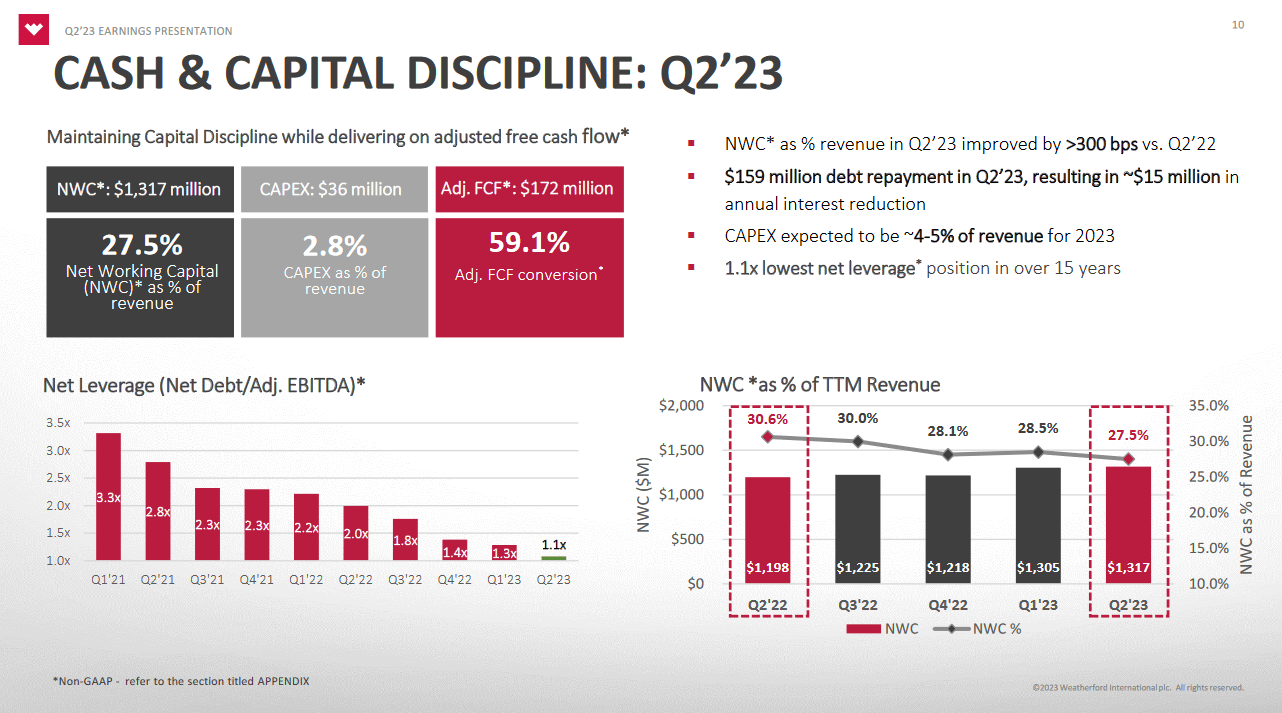

As far as the cash and capital deployment that WFRD has, I think it looks solid on paper. The company maintains 27.5% of revenues as networking capital and has a CAPEX of revenues at 2.8% right now. But where I am looking perhaps the most is the strong FCF conversion rate of nearly 60%. This strong rate has lent WFRD the ability to significantly pay down debt efficiently over the last quarters. In Q2 FY2022 alone, WFRD alone paid off $159 million. This, of course, improves the interest expenses for the company and $15 million was taken off. This ultimately ends up benefiting shareholders mostly, as the additional available earnings increase the chance of significant buybacks happening. With the cash position looking very strong at $787 million, WFRD is capable of paying off a significant portion of the $1.9 billion long-term debts.

Markets They Are In

The market for both oil and natural gas has been quite volatile over the last few quarters, but it seems that prices are improving and trending upward for both of them right now. Oil for example managed to pass $90 and seems to be sticking around here. Heading into winter, I think that prices will further appreciate and that will improve drilling activity and the serviceable market that WFRD has as a result.

{kind=link}

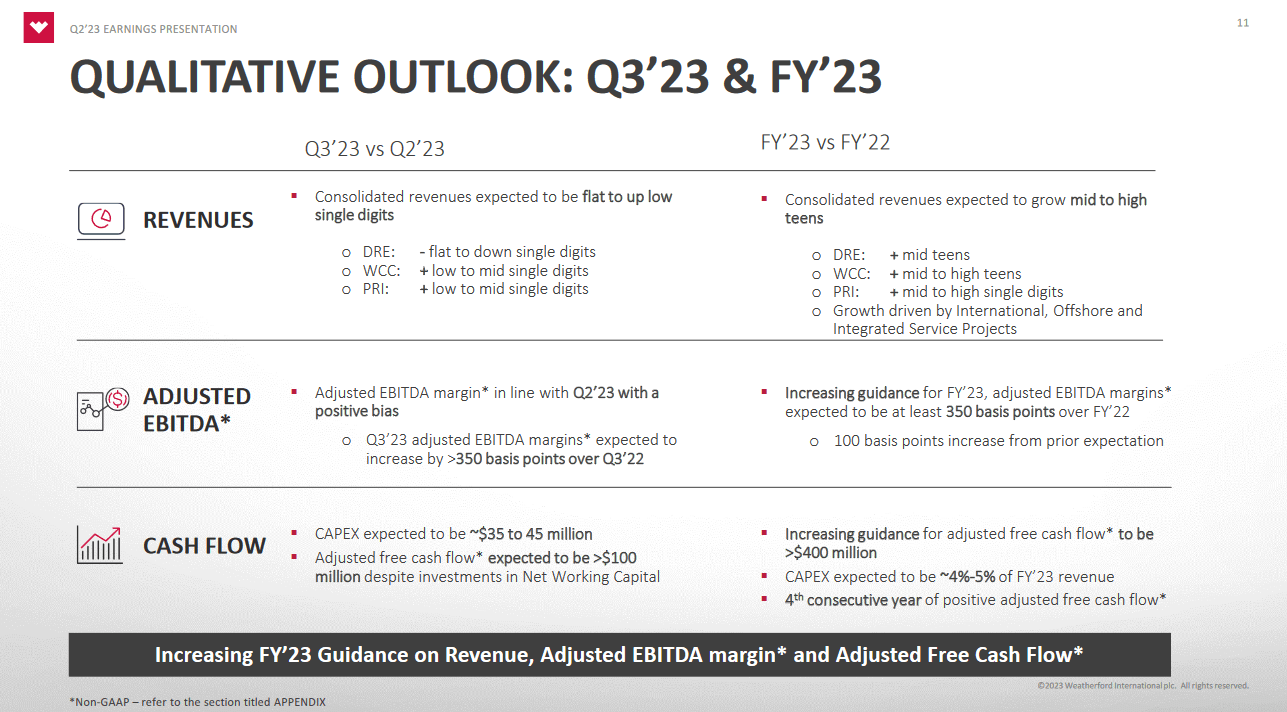

From the last report by WFRD, they are raising their 2023 guidance and this has further ignited the share price. The FCF, for example, is expected right now to be over $400 million at least for 2023 and be the fourth consecutive year of positive cash flows for the business. The long-term goal continues to be solid and positive cash flows for the company. This should be achievable if they manage to capture the demand that the industry is placing on them. Looking at the p/fcf for the company though, it doesn't look like investors are getting such a good deal, unfortunately. The multiple is 10x, over 100% higher than where the rest of the sector is trading.

With WFRD, you are not necessarily getting a pure play commodity company, but rather one that services the industry. The additional stability that comes with revenues is possibly rewarding a higher multiple here, but not one that should be 100% higher than the sector, in my opinion.

Risks

Regarding potential risks for WFRD, drilling activity, and energy prices continue to hold a prominent position. It's worth noting that the company has grappled with bankruptcy in the past during periods of energy price downturns. Additionally, a cloud of geopolitical uncertainty looms large, particularly about the Russia-Ukraine conflict and the complex dynamics with China. Meanwhile, labor inflation and persistent supply chain disruptions further add to the list of challenges that the company must navigate. Notably, the company's exposure to Russia may also exert a negative influence on its overall performance.

P/FCF (Seeking Alpha)

Valuation is perhaps the biggest concern for investors with WFRD right now. If there is a broader market correction I think that WFRD could potentially see a harsher decrease than the others given that it's trading so far above sector medians. This gives less cushion to the share price if it were to fall.

Final Words

The share price has run up very quickly for WFRD and in the energy sector, it has been one of the best plays, yielding a return of over 200% in the last 12 months alone. The additional activity and serviceable market that WFRD has been, seemingly, one of the reasons for these positive moves. However, I would stay worried, as the price could correct significantly from here as it begins to consolidate.

WFRD doesn't have a strong buyback program or a dividend, so there isn't any immediate shareholder value to gather up here. For this reason, I am rating WFRD a hold as I await hopefully better entry prices in the short term.

For further details see:

Weatherford International: I Think We Are Consolidating Here