WFRD - Weatherford: Unexpected Global Integrated Oilfield Services Winner

2023-10-29 11:03:57 ET

Summary

- Weatherford International is an unexpected winner in the oil field services boom, with strong earnings and projected double-digit revenue growth.

- The company offers differentiated services with higher margins and has the capacity to meet incremental market demand.

- Weatherford is undervalued compared to its peers, presenting an investment opportunity with potential for significant upside.

While consensus estimates and news headlines continue to suggest that oil market will be well-supplied, forward-looking oil & gas companies are predicting the opposite and are ramping up drilling, exploration, and development activity across the globe. Bison first discussed the possibility of an oilfield services boom in March 2022, and it has now become evident that one is already well underway: E&P capital budgets have rebounded dramatically since their 2020 nadir, DUC inventories have been depleted, and resultingly, services day rates rose dramatically in late 2022 and early 2023.

There also remain critical shortages parts, equipment, and skilled labor needed to drill and maintain oil and gas wells, driving significant cost inflation for E&P's and supporting higher oil prices versus pre-Covid levels. In our view, recent strong earnings reports from the 3 major oil field services companies, Halliburton (HAL), Schlumberger (SLB) and Baker Hughes (BKR), and optimism amongst their management teams, confirm that we are in the early innings of a multi-year oil field services & equipment boom.

Offshore Services Activity

There is uncertainty surrounding where the world's future oil supply will come from: the most easy-to-access, low-cost and economic oil reserves have already been depleted. Additionally, shale productivity has been declining in the U.S, the political environment for oil and gas extraction is becoming increasingly challenging in Western countries, and there's been material underinvestment across the global oil value chain since the prior cycle.

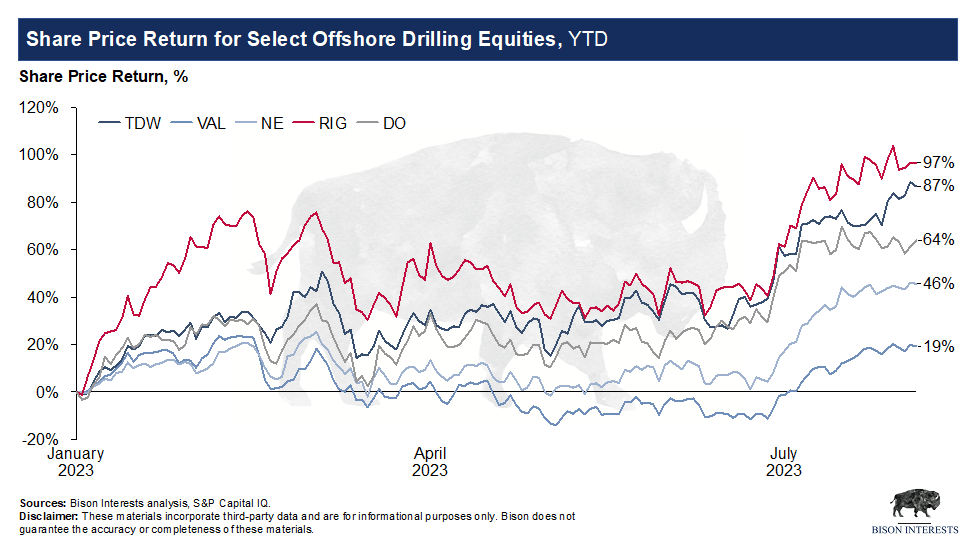

Given these realities, it is no surprise that exploration activity has been accelerating, day rates and utilization on drilling rigs and drill ships have been surging, and many of the major companies-including some that emerged out of bankruptcy-have seen their share prices soar:

{kind=link}

The recent ramp-up in offshore drilling activity also reflects the world's skepticism that OPEC+ has sufficient spare capacity remaining to be the "supplier of last resort". With the prospect of higher prices due to limited future supply, oil and gas companies are undertaking capital-intensive and complex offshore exploration and drilling projects in hopes of finding major discoveries, such as in Guyana.

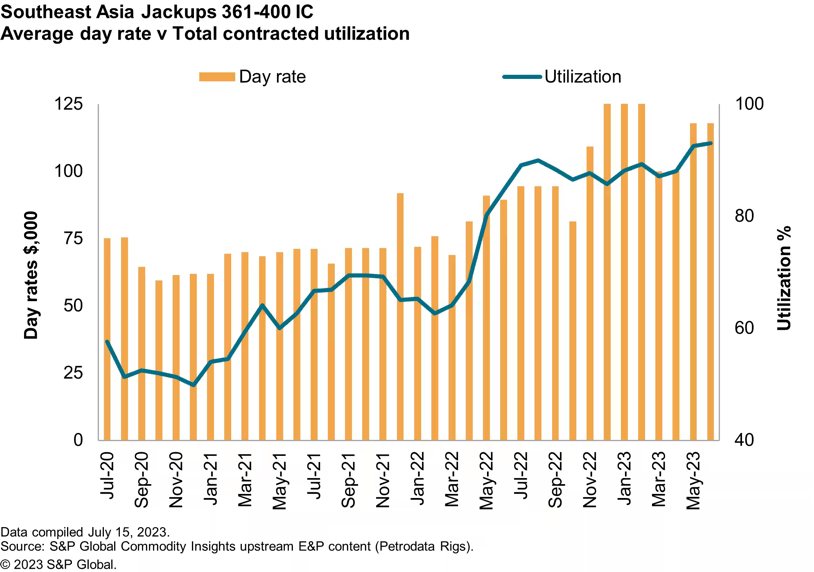

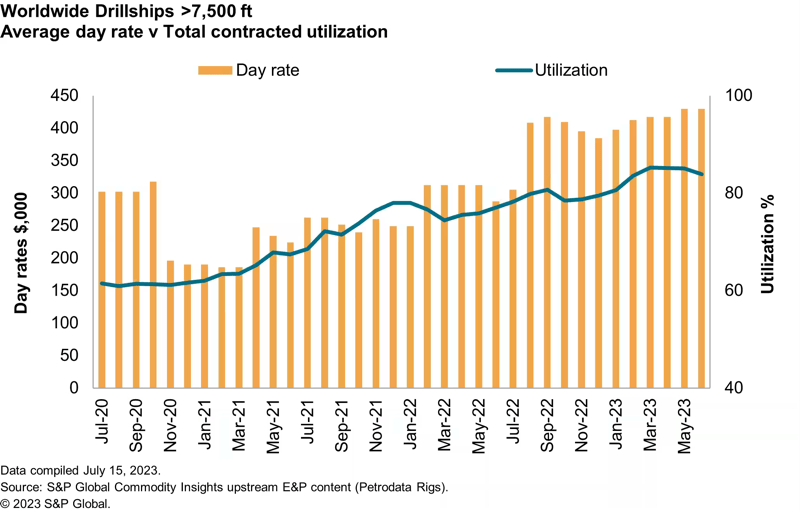

It is likely that most of the world's incremental oil may come from offshore sources, which are more expensive to drill and support structurally higher oil prices. With higher offshore demand, day rates and utilizations for offshore rigs, particularly drill ships and jack ups, have been rising:

S&P Global, Twitter S&P Global, Twitter

{kind=link}

{kind=link}

Weatherford International: Compelling Investment Opportunity

Bison has been investing in equities that stand to benefit from increased offshore and international drilling and development activity and higher day rates. One that remains oddly under the radar is Weatherford International WFRD , the forgotten fourth largest global oilfield services company behind Halliburton, Schlumberger, and Baker Hughes.

Weatherford also recently reported strong quarterly earnings. Following excellent third quarter results, it is projecting double digit revenue growth in 2024 on the back of higher international revenues, particularly in the Middle East. The investment case for WFRD is compelling: revenue and margins should continue to expand faster than peers as it continues to secure multi-year contracts, to invest in oil field technologies with a better margin profile, and as lower equipment utilization results operating leverage. And despite these tailwinds, WFRD continues to trade at a material discount to peers, offering upside to a re-rate.

Differentiated Services Driving Higher Margins

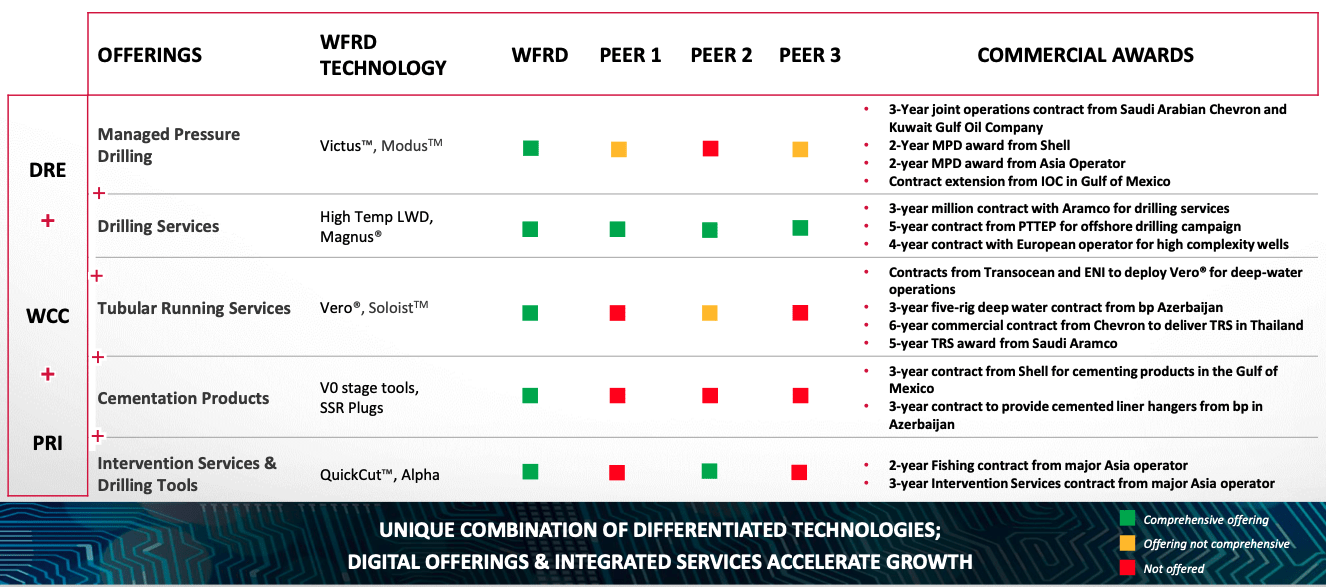

Weatherford offers a broad range of services, albeit not as broad as Halliburton and Schlumberger. WFRD successfully competes for the same business, as the #1 or #2 in multiple major services lines. And Weatherford has long-term contracts with state-owned supermajors Saudi Aramco and Brazilian Petrobras .

Weatherford Corporate Presentation

{kind=link}

While Weatherford competes with the big 3 in traditional lines of business, it also continues to invest in technology to grow its specialty services offerings. Weatherford made notable technological advancements in the second quarter, such as growth in the VERO offering and the launch of StingGuard in their tubular running services business, both which enhance safety and efficiency, and the commercialization of Modus in their drilling and evaluation segment. It is also worth noting that Weatherford's higher margin integrated projects offering-a full scale project management service-has delivered impressive yearly and sequential revenue growth of 289% and 68% respectively.

Weatherford is at the forefront of technology focused growth segments, yet the market is valuing its business as an undifferentiated competitor. In reality, Weatherford has pricing power from high levels of industry utilization, a differentiated service offering with higher margins, and excess capacity to meet incremental market demand. As the oil exploration cycle progresses, we expect Weatherford to capture market share from competitors and to continue to deliver higher margins and cash flow.

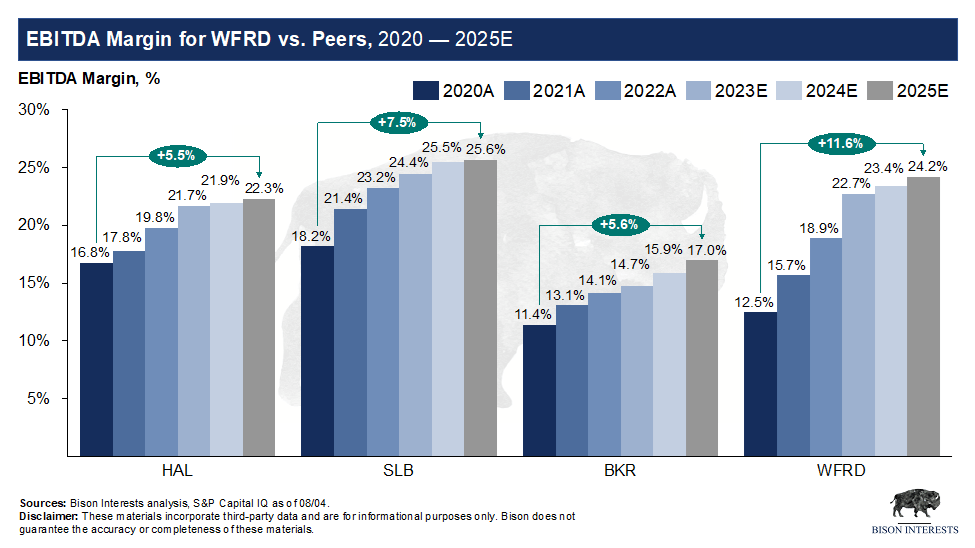

In that regard, Weatherford has been growing in line with competitors, but its margins are improving faster and projected to be on the higher end of the peer set by 2025:

{kind=link}

Despite its growth and profitability being in line with peers, and its well differentiated service offering, Weatherford remains out of favor with investors resulting in a compressed valuation:

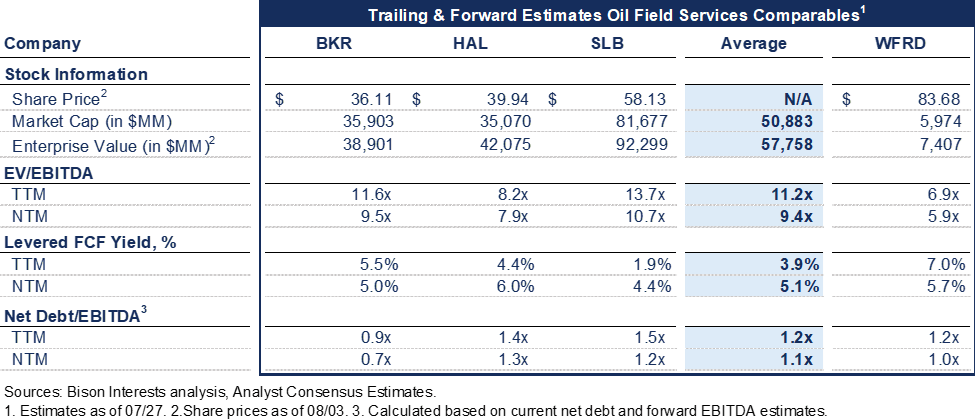

{kind=link}

As can be seen above, Weatherford has traded at a ~60% discount to peers over the last twelve months on an EV/EBITDA basis, despite generating 80% more free cash flow with similar levels of leverage. On a forward basis, this implies ~80% upside to Weatherford's equity if it were to trade in line with peers. And given Weatherford's rapid growth and better margin profile, we contend that it should command a valuation premium to peers.

Weatherford is Best Positioned to Benefit from the Oil Field Services Boom

Another underappreciated driver of Weatherford's historical and projected margin growth is the relative under-utilization of its equipment and services compared to peers. There has been considerable tightness of supply for oil field equipment, we believe Weatherford has more capacity to service incremental demand than peers.

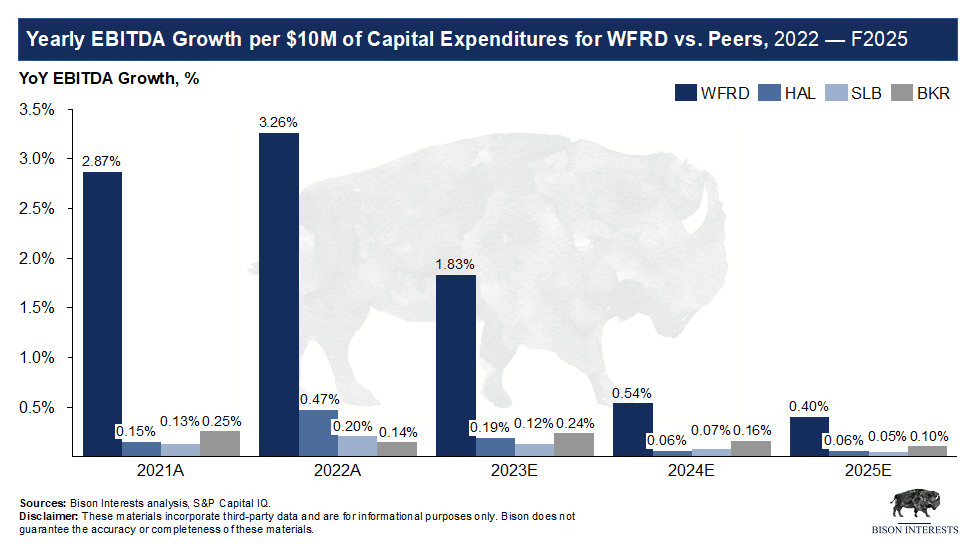

Weatherford does not disclose utilization rates for its equipment in its public filings. Instead, we proxied its equipment and crew utilization rate relative to peers by determining the contribution of capital expenditure relative to EBITDA growth. We found Weatherford's capital efficiency to be substantially higher than peers in this regard:

{kind=link}

Day rates for rigs and various other services have risen substantially since the start of the oil field services boom, and some of those contracts are locked in at a fixed price over multiple years. With more spare equipment and services capacity, Weatherford is in a unique position to be able to service incremental demand better than competitors at a higher market price, which may be a driver of Weatherford's further outperformance over time.

Risks & Mitigating Factors

The most prominent risk for Weatherford is a slowdown in global oil drilling and exploration activity, for which the most likely catalyst is a recession-induced drop in oil prices.

We have discussed recession concerns extensively in prior white papers. While a recession is possible, key economic indicators suggest that it may not come as soon as consensus expectations. And even if a recession does materialize, it isn't immediately clear that oil demand would drop sufficiently to balance a market which is already undersupplied. It is also worth noting that Weatherford secures its revenue primarily via multi-year contracts, which dampens the effects of short-term commodity price fluctuations on its revenues.

As with all undervalued securities, there is always the risk that Weatherford's equity valuation discount persists even as profitability improves, implying that it might take longer to re-rate than expected. In our view, an investment in Weatherford has multiple paths to a successful outcome: even if the shares continue to trade at a discount to peers, Weatherford is expected to more than double its free cash flow in 2023 to ~$500MM from $217MM. The implication is that there is always room to retire stock or institute a dividend to close the valuation gap in public markets.

Conclusions/Takeaways

The oil field services boom is already well underway, and Weatherford is the most likely beneficiary given its higher margin services and spare equipment capacity. Weatherford has fallen out of favor with investors following its bankruptcy in 2019, and few seem to have taken notice of its improved balance sheet, rapid growth and rapidly improving margin profile. Despite these improvements, consensus estimates show Weatherford trading at a ~40% discount to peers. This presents an opportunity to invest in a well-run and capitalized competitor in the oil field services business, whose profitability is rapidly improving, at a fraction of the price.

For further details see:

Weatherford: Unexpected Global Integrated Oilfield Services Winner