WEBR - Weber Inc.: Shares Have Overheated

Summary

- Weber is slated to be acquired quite soon, with the deal expected to close in the first half of this year.

- Even so, the market has pushed shares above the agreed-upon price, likely anticipating a higher bid.

- While this is always possible, the overall risk-to-reward scenario looks bearish for investors, especially given the firm's recent performance.

Late last year, news broke that Weber ( WEBR ), a business focused on the production and sale of outdoor cooking equipment, had agreed to be acquired by its majority shareholder, BDT Capital Partners, in a deal valuing the company at $8.05 per share. This represented a 60% premium over where shares were trading in late October 2022. Clearly, that move higher, especially in light of weak financial performance, proved to be a blessing for shareholders. Having said that, the stock has gotten ahead of itself and now looks too risky for investors to realistically consider. Given the circumstances surrounding the business, combined with its fundamental performance as of late, I do think that a bearish stance makes sense at this time. As such, I have decided to rate the business a 'sell' to reflect my view that the stock should decrease in value before too long.

Not all that great a play these days

About two months ago, on December 12th, 2022, news broke that BDT Capital Partners had agreed to acquire Weber in an all-cash transaction valuing the stock at $8.05 per share. This represented a significant premium over where shares traded at in late October and translated to a 23.8% premium over the $6.50 per unit that the stock was at only one day earlier. For any investor who bought in prior to that moment, the upside was certainly great to see. Since then, however, things have gotten a little out of control. At its peak following the announcement, shares traded as high as $8.34 and, as of this writing, are at $8.19 apiece.

Seeing this kind of premium is highly irregular, but it does happen from time to time. Normally, when this kind of scenario comes to pass, it's because the market believes that another suitor might come into the picture and pick up the company instead or that it may strike up a bidding war with the original suitor. When this kind of scenario does transpire, the end result for investors can be great, with shares rising often more than they deserve to. While it's clear that this is what the market is thinking at this time, I do not believe that such a scenario is likely to actually occur.

{kind=link}

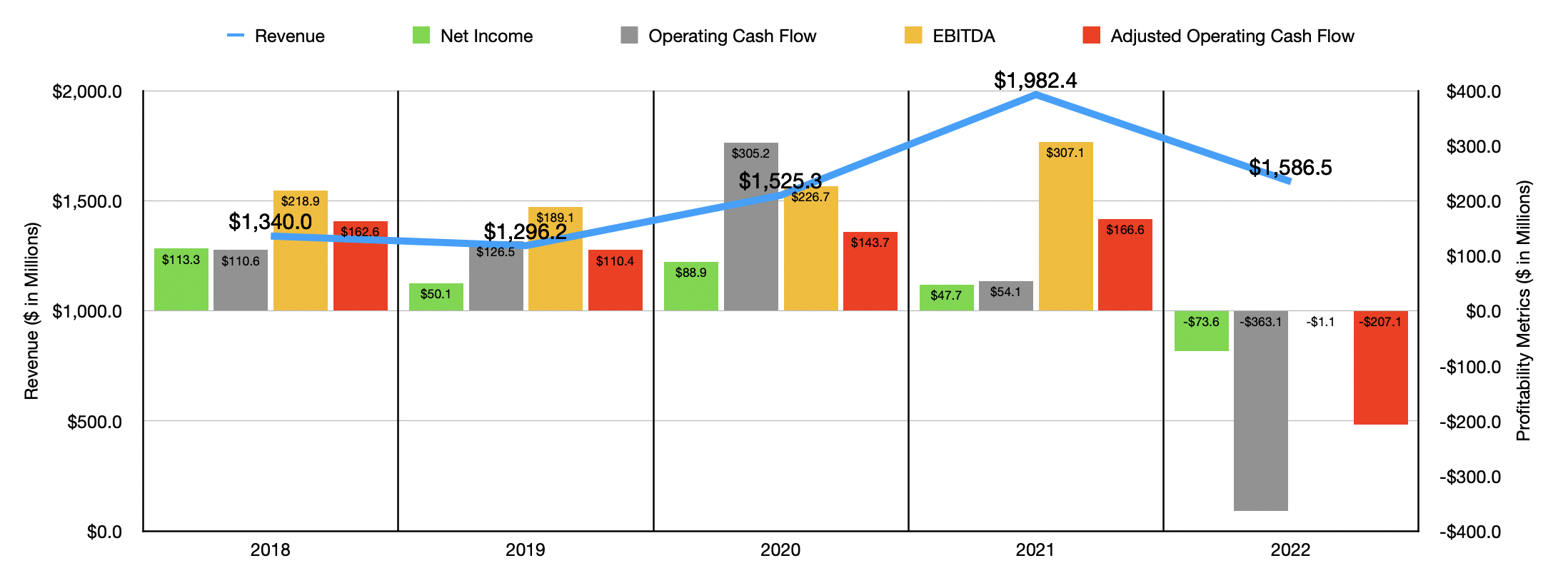

I say this for a couple of reasons. For starters, Weber is already majority owned by BDT, with that company having roughly 67% control over the enterprise. Second, at current prices, Weber does not look fundamentally appealing whatsoever. To see what I mean, we should touch on its recent financial performance. During the company's 2022 fiscal year , sales came in at $1.59 billion. That was actually down significantly from the $1.98 billion reported for the 2021 fiscal year, but it did come more in line with what the company experienced back in 2020. This roughly 20% drop in sales was driven by consumer traffic, both in-store and online, slowing as a result of macroeconomic factors. In the first half of the year, sales were negatively impacted by a reduction in volume, driven by supply chain disruptions. In addition, foreign currency fluctuations impacted sales negatively to the tune of $65.3 million year over year.

When looking at the historical sales data of the company and management's own notes on the matter, it's clear that, instead of the company worsening, it was merely reverting back to a more typical trend when it comes to sales. The 2021 fiscal year was propped up not only by foreign currency fluctuations totaling $76.3 million but also by strong consumer demand for outdoor cooking products and continued inventory restocking at its retail customers as the global economy continued to reopen and life started to revert back to normal.

The real pain for the company comes not necessarily from the return to normalcy from a sales perspective but, instead, from what has happened on its bottom line. As you can see in the initial chart of this article, for most of the past five years, profits under the company had been worsening. The 2022 fiscal year was the absolute worst, with the business generating a net loss of $73.6 million. On this front, the company was confronted with a meaningful decline in its gross profit margin as a result of higher inbound freight costs, rising commodity costs, foreign currency fluctuations, and lower sales volumes. If it were only the net income for the business that struggled, I might be able to look past that. However, other profitability metrics became troubled. Operating cash flow went from $54.1 million in 2021 to negative $363.1 million in 2022. Even if we adjust for changes in working capital, the metric would have dropped from $166.6 million to negative $207.1 million. Even EBITDA took a beating, plunging from $307.1 million to negative $1.1 million.

{kind=link}

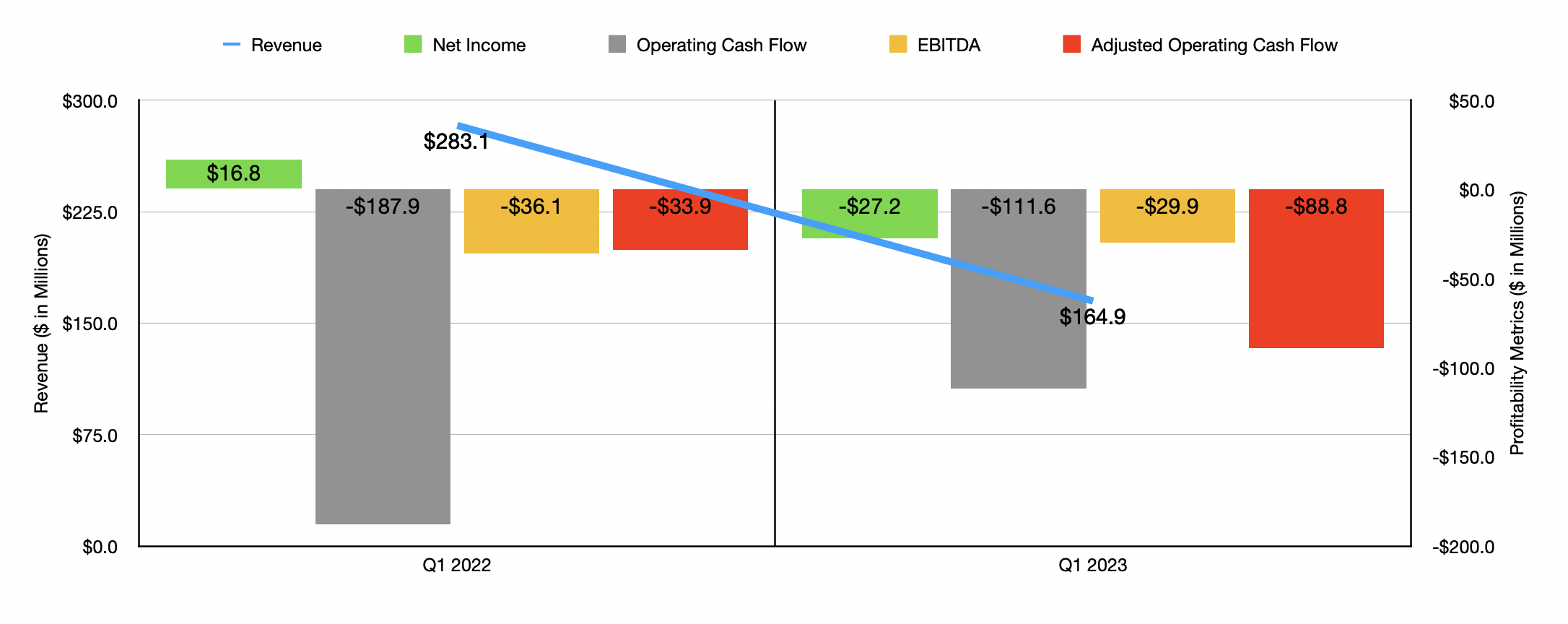

Pain for the business continued into the 2023 fiscal year. Sales in the first quarter of the year totaled $164.9 million. That's 41.8% lower than the $283.1 million generated at the same time one year earlier. Elevated retailer inventories carried over from the 2022 fiscal year resulted in lower customer orders, slowed consumer sales caused by economic conditions, and more. It also doesn't help that foreign currency fluctuations impacted sales to the tune of $7.6 million. All of these issues resulted in most of the company's bottom line results worsening as well. The firm went from a net profit of $16.8 million in the first quarter of 2022 to a net loss of $27.2 million in the first quarter of 2023. Operating cash flow did improve, going from negative $187.9 million to negative $111.6 million. But on an adjusted basis, it worsened from negative $33.9 million to negative $88.8 million. The only real improvement came from EBITDA, which went from negative $36.1 million to negative $29.9 million.

Clearly, elevated inventory levels caused by an overreaction by companies to the initial supply chain issues and inflationary pressures in the broader economy led to a scenario where the company is struggling to keep sales and profits up. Eventually, this will come to pass. However, the pain could persist for several quarters before truly alleviating. The thought of some other suitor stepping in to handle this pain may not seem preposterous if it weren't for the fact that shares don't look all that cheap even upon a return to more normal levels of profitability. And that brings us to the third reason why I don't think another suitor will step in. In short, shares look more or less fairly valued even upon a return to normalcy.

{kind=link}

As we already established, the 2021 fiscal year was peculiar for the business in a positive way. In a more normal environment, the company's financial data might look more similar to what it was in 2020. For full transparency, in the chart above, I placed valuation data for both 2020 and 2021. If we do go back to the levels of profitability seen in 2020, the firm would be trading then at a price to adjusted operating cash flow multiple of 16.6 and at an EV to EBITDA multiple of 17.4. By comparison, using data from the 2021 fiscal year, we would see these multiples at a more reasonable but still not exactly cheap 14.3 and 12.9, respectively. To buy a company going through issues and paying these kinds of multiples would not exactly be a great move unless significant synergies could be unlocked.

One other scenario that should bother those who are long the stock right now involves a failure of the deal entirely. This probably also will not happen. But in the event that it does, the current fundamental condition of the business suggests to me that shares should decline rather materially in price. Typically, when deals like this do fall apart, the stock of the company that was supposed to be acquired for a premium sees its price drop closer to the levels it was at before a deal was made.

Takeaway

The way I see it, there are three scenarios moving forward. The most likely scenario is that Weber does ultimately get acquired by BDT at the price agreed upon. In this case, investors buying the stock today would see a 1.7% decline in the value of their investment. The second scenario is that the deal could fall apart entirely, in which case downside would be significant. Perhaps on the order of 20%. And the third scenario, and least likely, is that there might be a marginal amount of upside if another buyer comes in. But for the reasons I already covered, that doesn't seem all that likely. When you weigh out the probabilities of these different scenarios, it becomes quite clear to me that a 'sell' rating makes sense at this time.

For further details see:

Weber Inc.: Shares Have Overheated