WEC - WEC Energy Group: Well Positioned For A Recession But The Stock Is Not Cheap

2023-08-31 16:57:47 ET

Summary

- WEC Energy Group, Inc. is a stable utility company with a 3.66% dividend yield, making it attractive during a potential recession.

- The company has a large customer base and stable cash flows, providing resilience in economic downturns.

- WEC Energy Group plans to invest in its rate base to drive future growth, but its projected earnings growth rate is lower than historical levels.

- The company has a stronger balance sheet than many of its peers, which positions it better than some other companies in a high-rate environment.

- The stock is at best fairly valued, but it could very easily be overvalued relative to its peers. As such, it is not a discount buy right now.

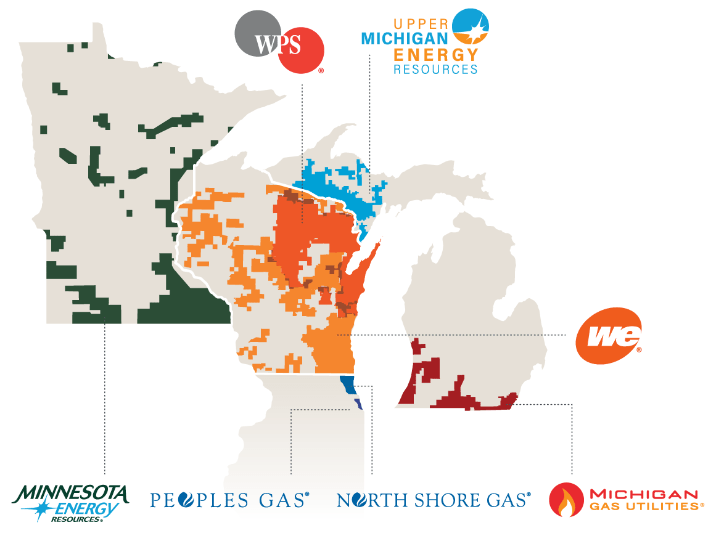

WEC Energy Group, Inc. ( WEC ) is a regulated electric and natural gas utility that primarily serves Wisconsin and the surrounding states:

{kind=link}

The company’s service territory also includes the third-largest city in the United States (Chicago, Illinois), although it is not the sole provider of utility services in this city. As might be expected from the company’s large service territory, it has a fairly large customer base. The most important thing for our purposes today, though, is that WEC Energy Group is an extremely stable company that boasts a respectable 3.66% dividend yield. This is a characteristic that could be especially valuable right now, as the American economy is showing numerous signs that it will enter a recession in the near future. WEC Energy Group should be better positioned to handle such a situation and continue to provide investment returns to its shareholders in such an environment.

I last discussed this company back in May, so a few things have changed since then. In particular, WEC Energy has released a new earnings report and the economy has weakened somewhat. As such, it is a good idea to revisit our thesis and see how it is playing out.

About WEC Energy Group

As stated in the introduction, WEC Energy Group is one of the largest regulated electric and natural gas utilities in the United States. The company primarily serves the state of Wisconsin and the Upper Peninsula of Michigan, but it also has operations in a few other surrounding states. This includes natural gas service in the city of Chicago, which is one of the largest cities in the nation. As such, WEC Energy Group has approximately 4.6 million retail customers. That is more than most other utilities possess. However, as I pointed out in my last article on WEC Energy Group:

“The size of a utility is generally irrelevant to its characteristics, as most utilities have a very similar business model. The most important of these characteristics is that WEC Energy Group has very stable cash flows over time and through any economic conditions.”

This chart shows the company’s operating cash flows during each of the past eleven twelve-month periods:

{kind=link}

As we can see, the company’s operating cash flows do not usually vary very much from period to period. There are a few occasional declines, such as we saw earlier this year due to the warm winter. However, even that did not represent a significant decline. I explained the reason for this in various previous articles, including the previous one on this company:

“The reason for this stability is that WEC Energy Group’s product is the provision of electric and natural gas services to homes and businesses. Most people consider this to be a necessity for modern life, so they will usually prioritize paying their utility bills ahead of making more discretionary expenses.”

We can actually see this reflected somewhat in the operating cash flow chart above. The earliest periods shown in the chart include the COVID-19 lockdowns that resulted in numerous people becoming temporarily unemployed or otherwise suffering a decline in their incomes. However, they still made efforts to pay their utility bills as shown by the fact that WEC Energy’s cash flows were still relatively in line with what the company had in other periods that did not include such an event. There are reasons to believe that the same would be the case should consumer finances become strained in the future.

There are a growing number of signs that consumers are beginning to struggle in the current environment. For example, Bloomberg recently reported that 42% of consumers receiving Supplemental Nutrition Assistance skipped meals in August and 55% ate less than usual because they could not afford to feed themselves. The same report also states that a growing number of people cannot afford their monthly utility bills or rent in full. It is highly unlikely that anyone who is struggling to cover utilities will be able to make discretionary expenses, which are the main thing keeping the economy afloat right now. Next month, student loan payments will resume, which will reduce the discretionary income of about forty million Americans by an average of $390 per month. Numerous retailers cited that as a near-term headwind in recent conference calls. When we consider all of these things, we can conclude that it is probably a very good idea to invest in companies that will not be affected very much by consumer or economic weakness. WEC Energy Group appears to fit into that category very well.

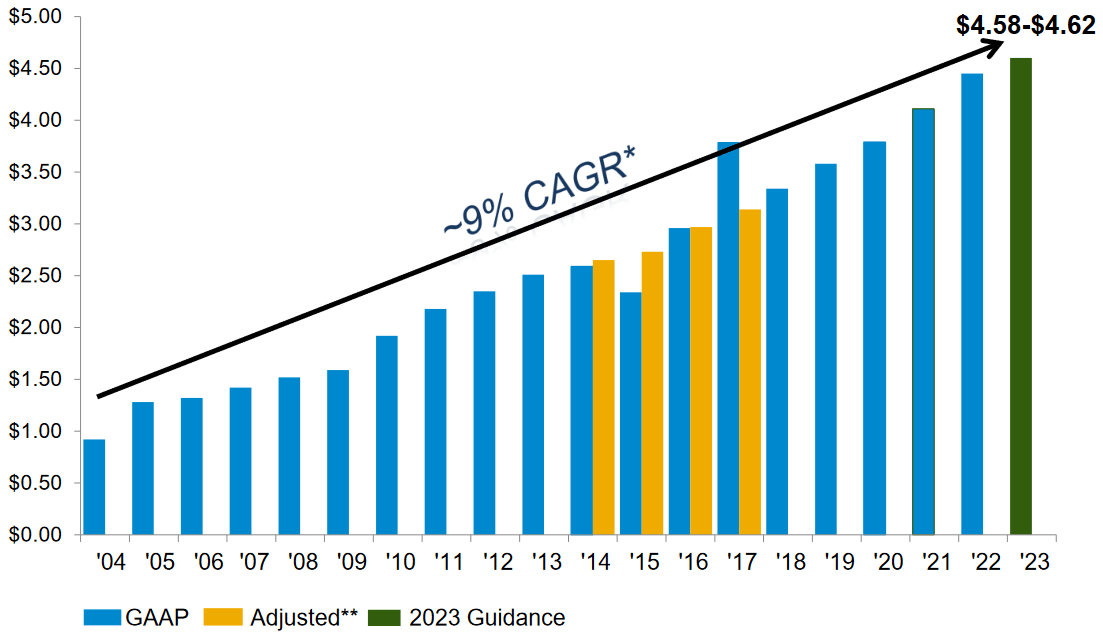

In fact, WEC Energy Group has a long track record of doing exactly that. This chart shows the company’s GAAP and adjusted earnings per share over the past twenty years:

{kind=link}

As we can clearly see, the company has managed to grow its earnings per share at a 9% compound annual growth rate over the past twenty years. In fact, we can see that even the financial crisis of 2008 or the worst recession since the Great Depression was not enough to reduce the company’s earnings per share. This reinforces our thesis that WEC Energy Group should be at least relatively immune to whatever the economy brings in the near term. This is something that will undoubtedly be appealing to any investor who is looking to reduce their risk of losses.

Growth Prospects

WEC Energy Group is well-positioned to deliver growth going forward. This is a very good thing since investors are unlikely to be satisfied with mere stability, although stability is preferable to the declining earnings that many other companies will likely deliver in a recession.

There are two ways through which a utility company can grow its earnings. One of these is by increasing its customer base. This makes sense, as the more people that it has paying their monthly bills the higher the company’s revenue, all else being equal. That means that more money is available to cover the company’s fixed expenses and make its way down to profits.

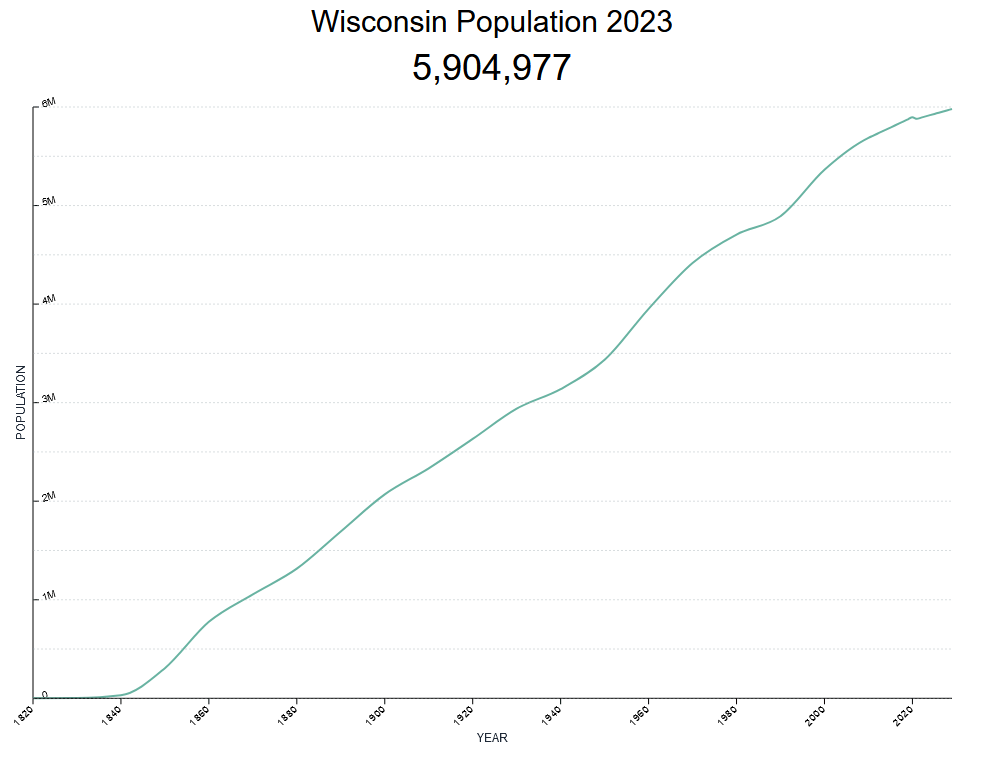

WEC Energy may have mixed results here. Fortunately for the company, Wisconsin is growing in terms of population:

{kind=link}

However, as the map above shows, WEC Energy Group’s service territory does not cover the entire state of Wisconsin. However, this is the only state that the company’s service territory sufficiently covers for us to make some assumptions about its customer base growth. If the above projections from the U.S. Census Bureau hold true, then WEC Energy Group should experience some positive customer growth in its home state. Unfortunately, the city of Chicago is experiencing population decline and the city is large enough that this may be sufficient to offset any population growth in other areas. According to the U.S. Census Bureau, the population of Chicago declined by 81,000 over the 2020 to 2022 period. Currently, anecdotal trends suggest that this is not going to reverse anytime soon, but the census data is the only authoritative source that I am able to find. For its part, WEC Energy Group is staying silent on the demographic trends of its service territory, so that is a sign that the company is not relying on a growing population to grow its business. We should adopt the same attitude as investors.

The primary way through which WEC Energy Group will grow its business going forward is to increase the size of its rate base. I explained how this works in various previous articles, including my last one on WEC Energy Group:

“A utility’s rate base is the value of its assets upon which regulators allow it to earn a specified rate of return. As this rate of return is a percentage, any increase in the rate base allows the company to positively adjust the prices that it charges its customers in order to earn that allowed rate of return. The usual way through which a utility grows its rate base is by investing money into upgrading, modernizing, or even expanding its utility-grade infrastructure.”

WEC Energy Group is planning to invest approximately $20.1 billion into its rate base over the 2023 to 2027 period. The company has stated that this will allow it to grow its earnings per share at a 6.5% to 7.0% rate over the period. That is disappointing to say the least. As we saw earlier, WEC Energy Group has historically grown its earnings per share at a 9.0% compound annual growth rate. Now its own guidance states that the growth will slow down.

With that said, the company’s projected earnings per share growth combined with its current 3.66% dividend yield gives us a total average annual return of 10% to 11% over the period. That is a very reasonable rate of return for a conservative utility. When we consider the likelihood of economic weakness during at least some of this projection period, that return starts looking very attractive since the company should be able to deliver it regardless of whether the economy falls into a recession or not.

Financial Considerations

The last time that we looked at WEC Energy Group, the company looked somewhat less leveraged than many of its peers. This is a good thing considering the rising rate environment, which has already begun to apply pressure on the earnings of some peers like Eversource Energy ( ES ). Let us see if this is still the case.

As of June 30, 2023, WEC Energy Group had a net debt of $18.0214 billion compared to $12.0314 billion of shareholders’ equity. This gives the company a net debt-to-equity ratio of 1.50 today. That is roughly in line with the 1.49 ratio that the company had the last time that we discussed it, which is a good sign as it implies that the company is not leveraging itself up. Here is how WEC Energy Group compares to some of its peers:

| Company |

| Net Debt-to-Equity Ratio |

| WEC Energy Group |

| 1.50 |

| CMS Energy ( CMS ) |

| 1.91 |

| DTE Energy ( DTE ) |

| 1.89 |

| Eversource Energy |

| 1.58 |

| Exelon Corporation ( EXC ) |

| 1.68 |

This is largely in line with what we saw the last time that we discussed this company. In short, WEC Energy Group remains the least leveraged company out of this peer group. As such, we can conclude that the company is probably not employing too much debt in the financing of its operations. As such, we probably do not need to worry too much about the company’s debt at this time.

Dividend Analysis

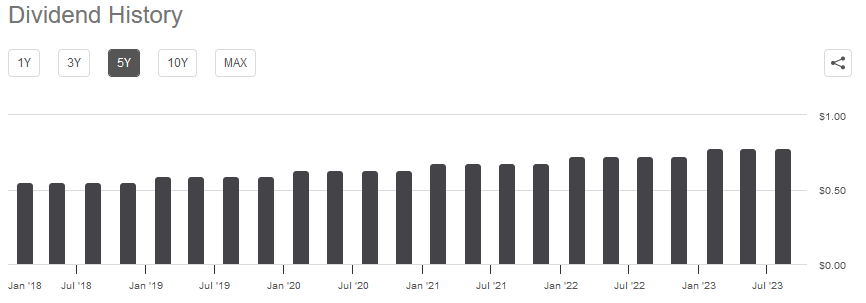

One of the biggest reasons why many investors purchase shares of utilities like WEC Energy Group is that these companies typically have higher yields than many other things in the market. Indeed, WEC Energy Group yields 3.66% as of the time of writing, which is considerably higher than the 1.45% current yield of the S&P 500 Index (SP500). WEC Energy Group also has a long history of raising its dividend on an annual basis:

{kind=link}

As such, someone who buys the company today should have a more attractive yield-on-cost in only a few years. The fact that the dividend is regularly increased also helps to offset the adverse impact that inflation has on the purchasing power of the dividend.

As is always the case, we want to ensure that the company can actually afford the dividends that it pays out. After all, we do not want to be the victims of a dividend cut that reduces our incomes and probably causes the stock price to decline.

The usual way that we judge a company’s ability to afford its dividends is by looking at its free cash flow. During the twelve-month period that ended on June 30, 2023, WEC Energy Group had a negative levered free cash flow of $502.6 million. Clearly, that is not enough to afford any dividends, yet the company still paid out $951.0 million to its shareholders over the period. At first glance, this could be concerning as the company cannot pay its dividends solely out of its internal cash generation.

However, it is common for a utility to finance its capital expenditures through the issuance of equity and debt. The company will then pay its dividends out of operating cash flow. This is due to the incredibly high costs of constructing and maintaining utility-grade infrastructure over a huge geographic area. In the twelve-month period that ended on June 30, 2023, WEC Energy Group had an operating cash flow of $2.0524 billion. That was easily enough to cover the $951.0 million that the company paid out in dividends with a substantial amount of money left over for other purposes. As such, we probably do not need to worry about a dividend cut in the near future.

Valuation

According to Zacks Investment Research , WEC Energy Group will grow its earnings per share at a 5.76% rate over the next three to five years. This is quite a bit less than the company’s historical 9% growth rate. It is also a lot less than the 6.50% to 7% growth rate that the company’s management is projecting based on its rate base growth through 2027. As such, this estimate might be a bit lower than the company will actually deliver. Nevertheless, WEC Energy Group has a price-to-earnings growth ratio of 3.22 assuming that this growth rate is accurate. Here is how that compares to the company’s peers:

| Company |

| PEG Ratio |

| WEC Energy Group |

| 3.22 |

| CMS Energy |

| 2.34 |

| DTE Energy |

| 2.83 |

| Eversource Energy |

| 2.60 |

| Exelon Corporation |

| 2.73 |

According to the above numbers, WEC Energy Group appears to be substantially overvalued relative to its peers. However, this is using the Zacks earnings growth estimate. If we use the 7% high-end that the company has guided us to, WEC Energy Group would have a price-to-earnings growth ratio of 2.64 at its current stock price. That is relatively in line with its peers. Thus, it appears that this company is fairly or overvalued right now. It is certainly not cheap compared to its peer group.

Conclusion

In conclusion, we are seeing a great deal of evidence that the United States may be about to enter a recession as consumers have reached the limits to which they can prop things up through spending. WEC Energy Group is better positioned to weather such an event than many other companies due to its non-cyclical business and the fact that most people will prioritize paying their utility bills. The company is also likely to deliver a very acceptable total return and has a strong balance sheet. The only real downside here is that it appears that WEC Energy Group, Inc. is at best fairly valued, so bargain hunters may want to wait for a dip in the share price.

For further details see:

WEC Energy Group: Well Positioned For A Recession, But The Stock Is Not Cheap