FRC - Wedgewood Partners - First Republic Bank: Continuing To Hold For The Prospect Of A Better Valuation

2023-04-20 23:30:00 ET

Summary

- We have some explaining to do given the collapse in the stock of First Republic Bank.

- We earnestly believed First Republic’s long-held, loyal customer base would hold fast through the burgeoning turmoil.

- The key issue now with First Republic, and the banking industry, is once a bank suffers a large, immediate deposit outflow, a liquidity issue can quickly become a vicious solvency issue because the lack of funding must be quickly shored up.

- We continue to hold our precrisis position in the shares for the prospect of a better valuation the longer First Republic can remain independent.

The following segment was excerpted from this fund letter.

First Republic Bank ( FRC )

BERT. I hate to break anything up but there’s something funny going on down at the bank. I’ve never really seen one, but it has the earmarks of a run.

MRS. MARTINI. Oh, my God.

BERT. If you got any money in the bank, folks, you better hurry. (The townsfolk all react in panic and run off.)

GEORGE. You wait here, dear. I’ll be just a minute. (He starts to exit.) MARY. George, let’s not stop. Please, let’s go.

GEORGE. I’ll be back in a minute, Mary…

It’s a Wonderful Life. 1946.

Source: It’s a Wonderful Life.

{kind=link}

We at Wedgewood Partners earnestly believe if there is bad news to report in your portfolio, we report it up front, in detail, no sugar coating and we are blunt in owning up to our mistakes. Well, as you all know painfully well by now, we have some explaining to do given the collapse in the stock of First Republic Bank.

The short explanation is that the Company got caught in a ruthless deposit run. We didn’t see it coming. Keep this stat in mind throughout this Letter’s commentary:

According to the FDIC, as of year-end 2022, the nation’s banks held $17.7 trillion in deposits. 50% are uninsured.

In the early innings of the current banking crisis which began with the swift failure of both Silicon Valley Bank and Signature Bank of New York ( OTC:SBNY ), our focus on First Republic was on the asset (loans) side of the Company’s balance sheet. In other words, we were first focused on the Company’s exemplary history as one of the best, most conservative lenders in the industry. Historically, bank failures, by far, have been due to credit risks. Our focus was on the wrong side of the balance sheet. Our mistake here would quickly prove to be dire. Our focus should have been on the liability side of the Company’s balance sheet - in other words, the deposit funding side of the balance sheet. Specifically, when word spread quickly (particularly on social media from a few notable venture capital firms that fanned the fires urging their portfolio of companies to immediately withdraw all their deposits from SVB) of a deposit run on Silicon Valley Bank, we earnestly believed First Republic’s long-held, loyal customer base would hold fast through the burgeoning turmoil. This would prove to be our greatest mistake. In four short, chaotic trading days, beginning March 9, the day after Silicon Valley Bank announced a $2.25 billion capital raise to shore up its capital base, including the bank being seized on the morning of Friday March 10, and finally with the sudden failure of Signature Bank NY over that weekend, panic and fear were in the air.

By Monday, First Republic’s stock collapsed -85% , despite First Republic’s Chairman’s Herbert assuring CNBC viewers that the bank was not seeing depositors fleeing the bank. The stock plunge spoke to a different reality – shattering the confidence in the bank. The deposit run on First Republic was on. Just two days later rumors swirled of massive deposit outlflows by the bank’s largest competitors redepositing fleeing customers.

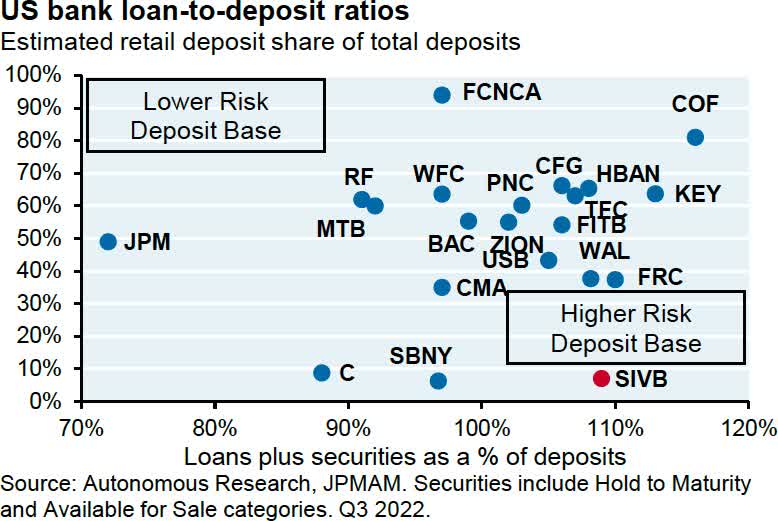

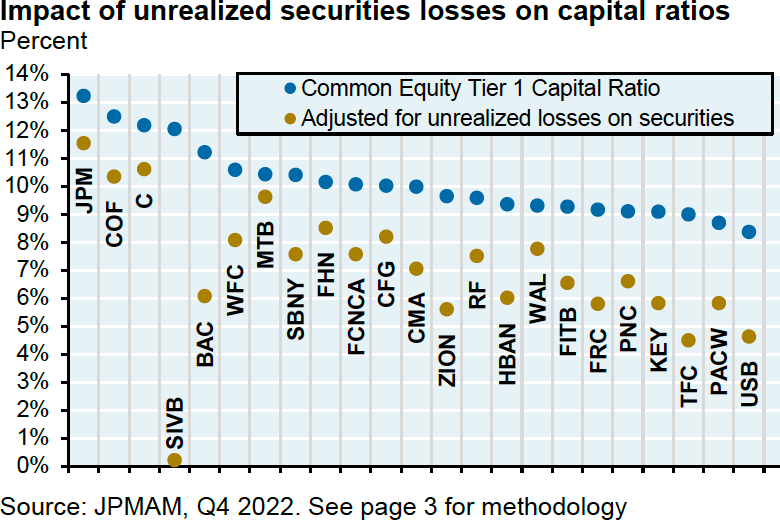

Here are a couple of graphics on the leading banks on the eve of the banking crisis in terms of loan-to-deposit ratios and the impact of unrealized securities losses on capital ratios.

{kind=link}

{kind=link}

Since then, as of this Letter, considerable efforts from both industry and regulators (reminiscent of the Panic of 1907) continue with the apparent goal to firewall off the failure of more banks to quelch what would likely become a renewed spark of nationwide deposit runs, with considerably more failures of regional and community banks.

The key issue now with First Republic, and the banking industry, is once a bank suffers a large, immediate deposit outflow, a liquidity issue can quickly become a vicious solvency issue because the lack of funding must be quickly shored up. If not, the need to quickly reduce a bank’s loan book and investment securities to a level congruent with the new, lower deposit funding base becomes paramount. In other words, a not-too-small amount of the bank’s loan book and investment securities would need to be sold quickly. In the current interest rate environment, such liquidations would book large losses. (See graphic, bottom page 18.) These losses would in turn be charged against a bank’s capital base. If the capital base then becomes imperiled, any subsequent capital raise would likely wipe out a large portion of a bank’s equity capital (i.e., shareholders).

We note the piercing sting of the apocryphal words in Ernest Hemingway’s The Sun Also Rises , “How did you go bankrupt? Two ways. Gradually, then suddenly.”

Here is a current timeline of the Panic of 2023:

March 8: Silvergate Capital, a “crypto” bank voluntarily liquidates.

March 8: Silicon Valley Bank, a commercial bank (really more of a specialty investment bank, than commercial bank), financing over half of U.S. venture capital-backed technology and health-care companies, plus over +40% of more recent publicly traded companies of the same ilk, due to “a textbook case of mismanagement,” announces a significant capital raise demanded by Moody’s Investor Service in order to avoid a sharp credit rating downgrade.

March 10: The California Department of Financial Protection and Innovation seizes Silicon Valley Bank and places it under receivership of the FDIC. At that time, approximately 89% of the bank’s $172 billion in deposits is over the FDIC’s $250,000 insured limit. The FDIC would later report that the 10 largest accounts of the bank held over $13 billion in deposits; the day before the bank was seized $40 billion in deposits were withdrawn; and the day the bank was seized, $100 billion in deposits was set to be withdrawn 80% of deposits in just two days . Silicon Valley Bank was the second-largest bank failure in U.S. history – and likely also the fastest.

March 10: In a regulatory filing, First Republic Bank “reiterates First Republic’s continued safety and stability and strong capital and liquidity… deposit base is strong and very-well diversified. Consumer deposits have an average account size of less than $200,000 and business deposits have an average account size of less than $500,000. Within business deposits, no one sector represents more than 9% of total deposits, with the largest being diversified real estate. Technology-related deposits represent only 4% of total deposits… liquidity position remains very strong…sources beyond a well-diversified deposit base include over $60 billion of available, unused borrowing capacity at the Federal Home Loan Bank and the Federal Reserve Bank…very high-quality investment portfolio is stable and represents a modest percentage of total bank assets. The investment portfolio is less than 15% of total bank assets. Of this, less than 2% of total bank assets is categorized as available for sale. First Republic has consistently maintained a strong capital position with capital levels significantly higher than the regulatory requirements for being considered well-capitalized. First Republic has a long-standing track record of exceptional credit quality. Nonperforming assets are only 6 basis points of total assets. Since 2000, First Republic’s average annual net charge-offs have been just 1/10th those of the top U.S. Banks.”

March 10: Treasury Secretary Janet Yellen meets with banking regulators.

March 11: The U.S. Federal Reserve and the FDIC weigh the creation of a liquidity fund that would allow regulators to backstop more deposits at banks.

March 12: FDIC, in coordination with the U.S. Treasury announces that all Silicon Valley Bank’s depositors – insured and uninsured – would be made whole. This announcement crystalizes deposit runs on banks with larger percentages of uninsured deposits, such as First Republic – which given the banks focus on the extremely wealthy, 68% of the banks deposit base was uninsured. In the immediate days, the issue of insured versus uninsured deposits becomes the focal point of confused policy statements from Treasury Secretary Janet Yellen, including the statement on CBS’ Sunday Morning Show that there would be no “bailout” of Silicon Valley Bank, yet the bank’s unsecured creditors (depositors), particularly, and specifically, uninsured depositors would be made whole. Signature Bank, an important apartment lender in New York, tragically morphed into a “crypto” bank, due to 30% of deposits came from the crypto arena failed – the third largest in U.S. history. Similar to SVB, Signature Bank failure was designated as “systemic risk” and thus allowed extraordinary measures to protect all depositors. Treasury Secretary Yellen is “working closely” with banking regulators.

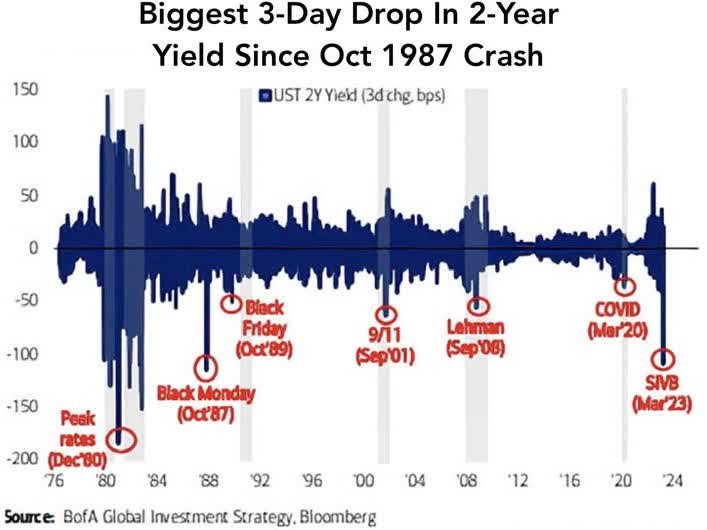

March 13: U.S. President Joe Biden says the administration's actions should give Americans confidence that the banking system is safe. U.S. Federal Home Loan Bank opens its lending war chest to provide even more liquidity to banks amid continued higher-than-usual demand for funds. There is a historic collapse in U.S. Treasury yields. The 2-year Treasury (a very useful market proxy to gauge the efficacy and direction of Fed policy) collapses from over 20 bps over the Federal Funds rate to under the rate by 90 bps!

{kind=link}

March: 13-17: During this fateful week, at the height of the banking panic, the flight into cash-rich technology stocks was nearly historic as well. It is the best week for growth stocks vs. value stocks in 22 years (Dot-Com) and also the best week for the NASDAQ 100 versus the S&P 500 Index since 2008 ( GFC ). Anticipating a sharp change to an ease in Fed policy, the rally in tech stocks continues sharply throughout all of March. The NASDAQ 100 rises 21% during the first quarter – its best quarterly gain in a decade.

March 14: Moody revises its outlook on the U.S. banking system to "negative" from "stable", citing heightened risks.

March 16: Treasury Secretary Yellen tells a U.S. Senate hearing that uninsured deposits would only be guaranteed in banks deemed a contagion threat, which in turn raising fears about smaller banks. Led by J.P. Morgan, large U.S. banks inject $30 billion in deposits into First Republic Bank to shore up the lender's finances.

March 17: Moody’s downgrades First Republic, citing “a deterioration on the bank’s financial profile.”

March 19: UBS agrees to buy Credit Suisse for 3 billion Swiss francs in stock and agrees to assume up to 5 billion francs in losses. Senator Elizabeth Warren says Fed Chair Jerome Powell “has failed…and should not be Fed chair.”

March 21: U.S. Treasury Secretary Janet Yellen tells bankers that she is prepared to intervene to protect depositors in smaller U.S. banks.

March 22: Secretary Yellen tells lawmakers that she has not considered or discussed "blanket insurance" to U.S. banking deposits without approval by Congress, again stirring up investor worry. Federal Reserve Chair Jerome Powell says SVB's failure is not indicative of wider weaknesses in the banking system.

March 24: Deutsche Bank shares drop over -8% in Europe and the cost of insuring the company's bonds against the risk of default spike. Other banking stocks also slump in Europe.

March 25: U.S. authorities consider the expansion of an emergency lending facility that would offer banks more support, notably for First Republic, according to a Bloomberg News report.

March 31: Senator Warren expresses the need to address the inadequacies of current FDIC insured deposit levels.

Banking is hard. Leveraged businesses that lend short and invest long are inherently risky. In extreme economic environments, much of that risk is out of managements control, particularly with interest rates – both short and long – that often swinging wildly throughout an economic cycle. Such swings are punctuated by policy errors of judgement by central banks. Much of the U.S. banking industry is dominated by commodity-like features. Checking account fees, interest rates on money-market funds, certificates of deposit and mortgages don’t vary that much from competitor to competitor. Long-term banking relationships aren’t the norm. In the banking industry, outside of the C-suite, top positions on both bank arms of investment banking and investment management typically are rarely lucrative. Last, but certainly not least, banking is a capital-intensive industry. To grow, a bank needs more capital. Depending on the inning of an economic cycle, plus the concomitant shape of the yield curve, capital costs are often too dear to access. So why invest in an industry with so many headwinds to success?

In our +30-years of investing, and recognizing all the above, we have rarely invested in banks. We agree - banking is too damn hard. That said, we have had success being highly selective in what we consider to be the very best-in-class banks. Our success investing in banks was not among our best investments over our past + 30 years to be sure, but worthy at the time of investment in Norwest/Wells Fargo, Commerce Bancorp of New Jersey and U.S. Bancorp. (We particularly enjoyed the journey with the enigmatic Vernon Hill of CBH.) These three banks shared one thing in common when we owned each, they were best-in-class banking operators in their respective chosen activities.

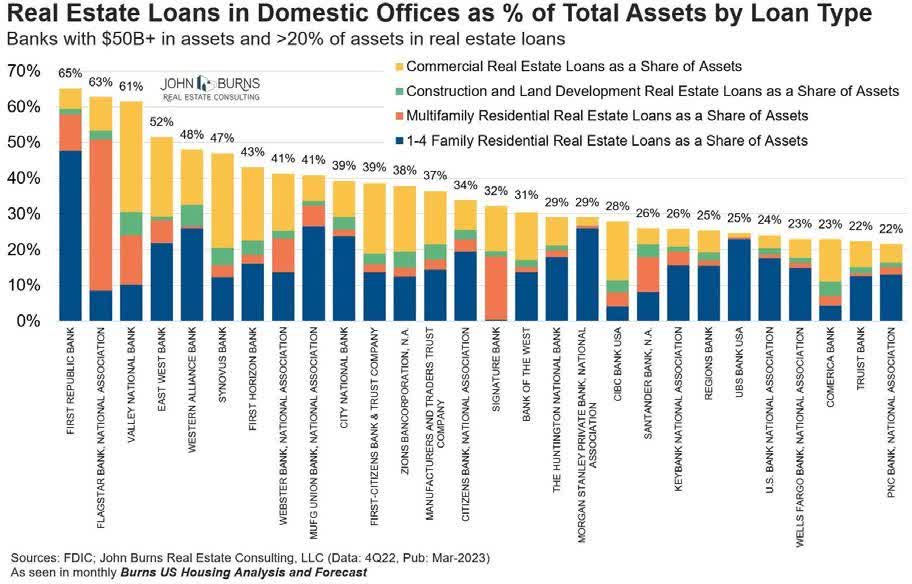

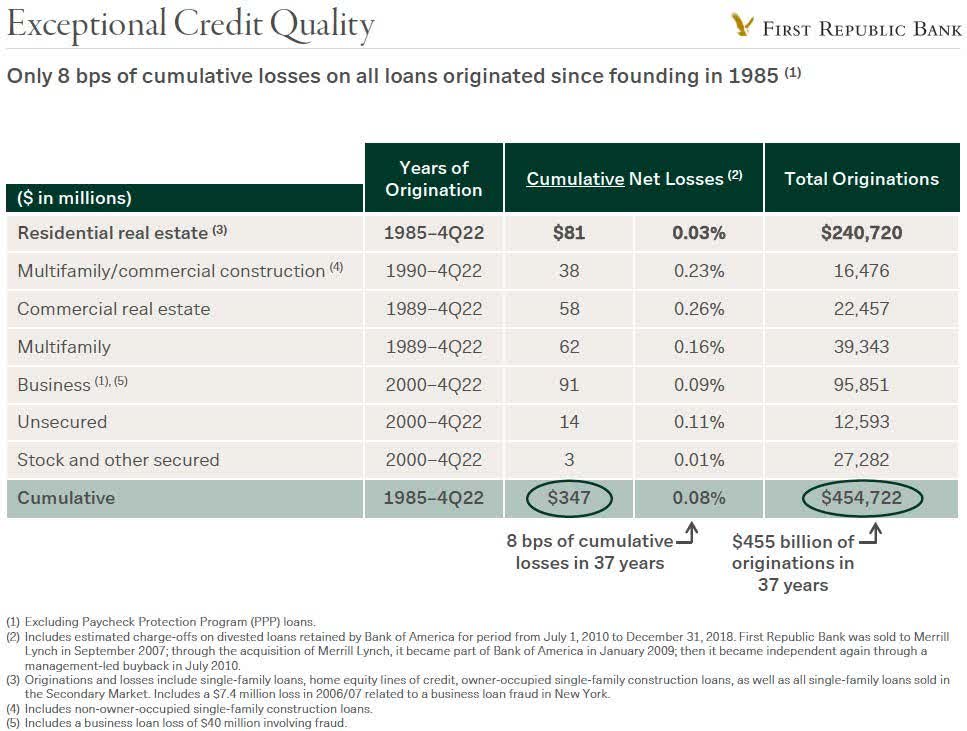

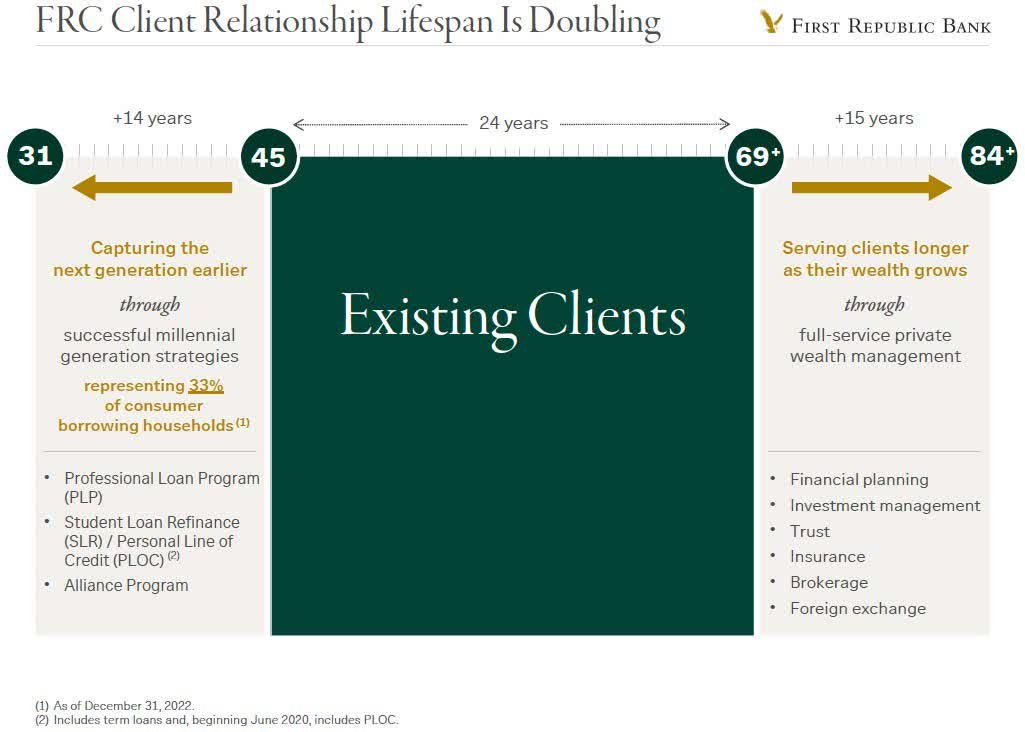

Our thesis on First Republic Bank was similar: best-in-class, white-glove service to the very wealthy – the sticky, very wealthy. In addition, and most key, the bank’s bankers were outstanding, conservative lenders. When First Republic makes a loan – more focused on residential mortgages than most banks - it would be the most exceptional circumstance that said loan didn’t get repaid. With wealthy clients, very high FICO scores and an abundance of collateral, loan losses, again, were the rare exception. Mix in too a highly reputable, market share-taking asset management division, and such tailwinds and non-commodity attributes make for a consistent recipe for compelling growth. The following graphics encapsulate the First Republic Bank story – and our attraction to the Company – which, in our view, is the story of a bank too good to fail.

{kind=link}

{kind=link}

{kind=link}

At this date, our investment team is trying to determine what path, likely a slim path at best, to claw back from the stock collapse. Our view on the near future of the bank is shaped by the significant efforts by both the U.S. Treasury and Federal Reserve, plus historic efforts by the leading banks to ring off the bank from collapse. In other words, First Republic is now a “systemically important bank.” Too big to fail. Too important to fail. If First Republic “fails,” who’s next? The list of “who’s next?” regional banks of equally considerable import is long. Many of these bank stocks are making new 52-week lows as we write this Letter.

The stock price of First Republic is now akin to a long-dated call option – without an expiration date. It appears that the Company will not be sold. Such an event would likely be a fire sale. However, the collective words to-date from Treasury Secretary Yellen imply de jure, versus de facto industry deposit insurance. Plus, given the liquidity provided by both the Fed’s Bank Term Funding Program and Discount Window, plus the industry’s collective deposit of $30 billion a fire sale seems remote. An independent First Republic would be the best outcome for shareholders. As it stands now, the bank needs to quickly reduce the asset side of its balance sheet to offset the +$80 billion in deposit outflows. Loans rolling off over the next few months, plus the sale of recent loans, if successful would be the first key step to remaining independent.

That said, all the actions taken thus far – and needs to take in the near term - by the Company to keep the lights on, even if successful, will considerably diminish the earning power of the bank for the foreseeable future. If said earning power is significantly negative for even a relatively short period, a capital raise will be dilutive to shareholders. Given these critical uncertainties we have not added to our position in the stock.

Again, the deposit run on the bank, plus the collapse in the stock, caught us off guard. We missed it. A most difficult mistake on our part. We continue to hold our precrisis position in the shares for the prospect of a better valuation the longer First Republic can remain independent. You will have received this Letter right before First Republic reports its first quarter. This report will be ugly. This report too will be the first detailed report from management since the banking crisis began. The investment team anxiously awaits this report.

Editor's Note: The summary bullets for this article were chosen by Seeking Alpha editors.

For further details see:

Wedgewood Partners - First Republic Bank: Continuing To Hold For The Prospect Of A Better Valuation