USD - Weekly Bund Yield And FX Forecast May 31 2024: 10-Year Bund Range In 10 Years

2024-06-03 17:35:19 ET

Summary

- The inverted Bund yields continued this week with the negative 2-year/10-year yield spread at negative 43.5 basis points compared to negative 50.5 basis points last week.

- As a result, today’s simulation shows that the probability of negative spreads in the 91-day period ending November 29, 2024, has moved to 69.5% from 74.6% in the prior week.

- That means the probability that the inverted Bund yield curve ends by November 29, 2024, is 30.5% versus 25.4% last week.

- The most likely one percent ranges for the 3-month yield (zero to 1%) and 10-year yield (1% to 2%) in 10 years are unchanged this week.

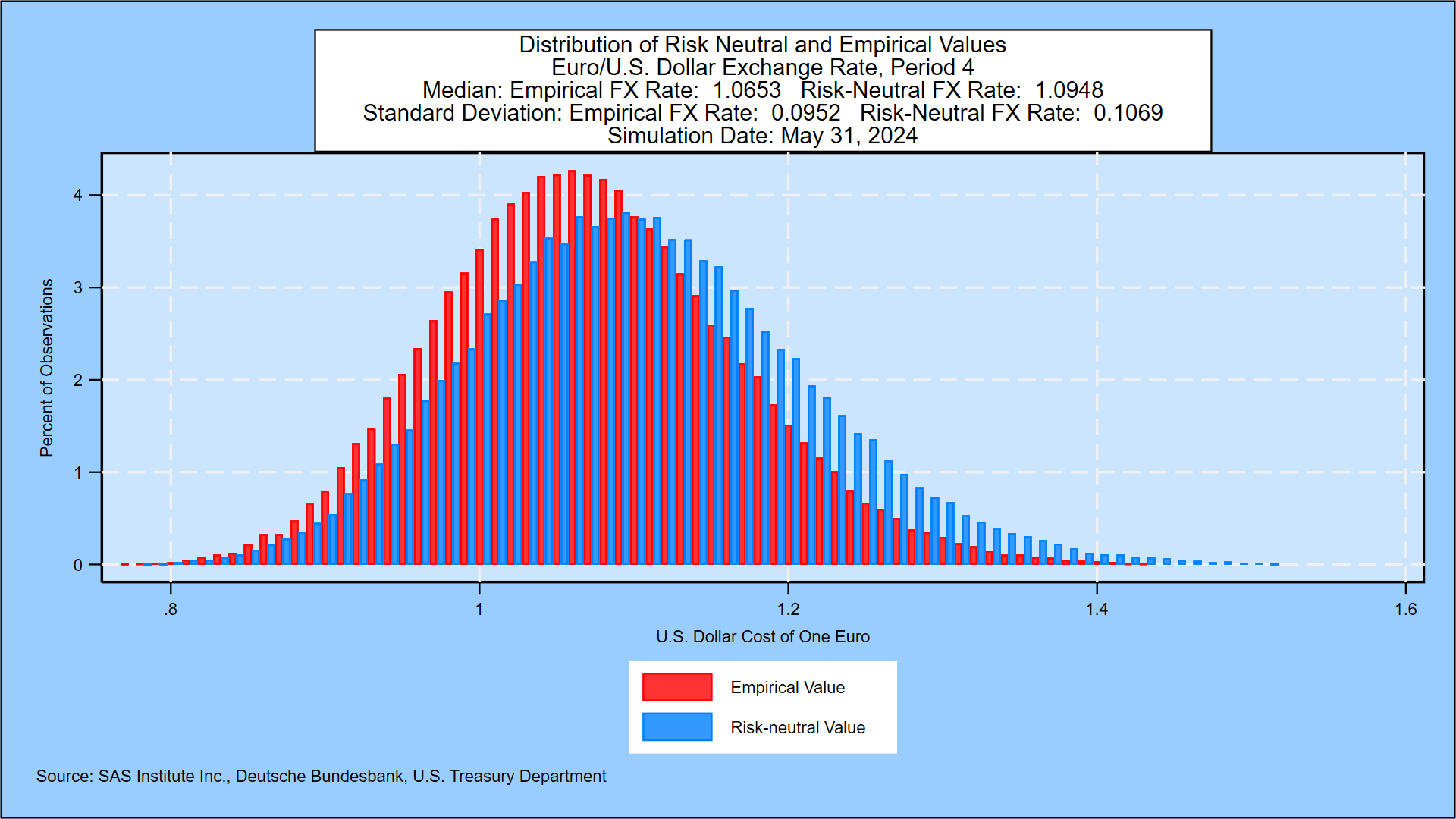

- The simulation with U.S. Treasuries shows a Euro/U.S. Dollar exchange rate at a median value of 1.0653 and a standard deviation of 0.0952 one year forward. The same simulation is used to price short and long-dated foreign exchange options on the Euro versus the U.S. dollar at a strike price of 1.07.

Author’s Note

This simulation has been done jointly with a U.S. Treasury yield simulation in a way that reflects the correlation among the 12 factors driving yields in each country. For more on the companion U.S. Treasury simulation, please contact the author. Both the Bund and the U.S. Treasury yield simulations impact foreign exchange rates, resulting in the following distribution of the Euro/U.S. dollar exchange rate one year forward:

{kind=link}

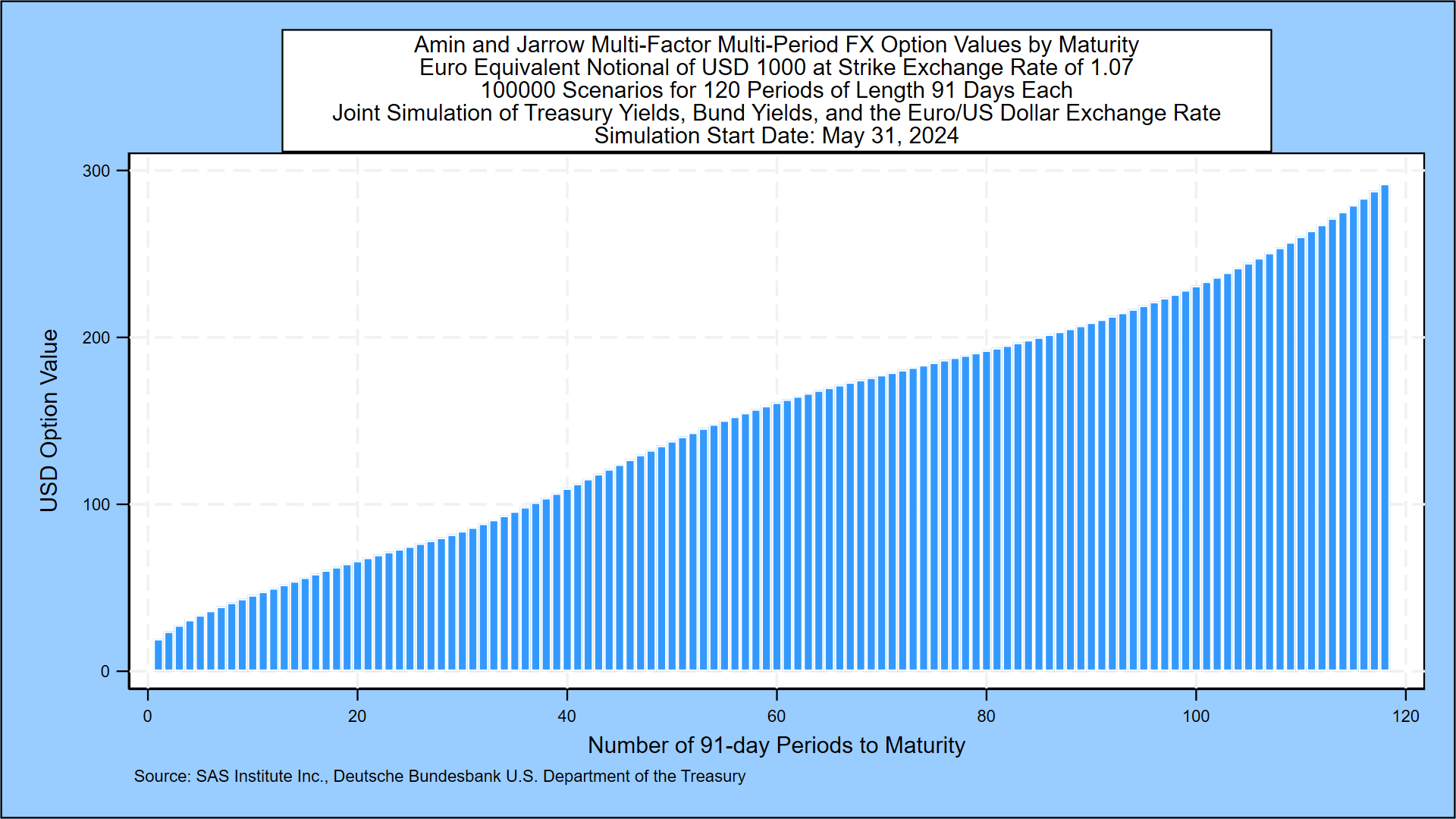

Pricing for short- and long-dated options to buy Euros versus U.S. dollars at a strike price of 1.07 for quarterly maturities out to 30 years is given below:

Weekly Bund Yield And FX Forecast, May 31, 2024: 10-Year Bund Range In 10 Years{kind=link}