USD - Weekly Bund Yield Forecast Feb. 16: Negative 2/10-Year Spread Probability Rises To 62.6% In August

2024-02-19 09:27:34 ET

Summary

- The inverted Bund yields continued this week with the negative 2-year/10-year yield spread at negative 44.0 basis points compared to 34.7 basis points last week.

- As a result, today’s simulation shows that the probability of negative spreads in the 91-day period ending August 16, 2024, has moved to 62.6% from 55.2% in the prior week.

- That means the probability that the inverted Bund yield curve ends by August 16, 2024, is 37.4% versus 44.8% last week.

- The most likely one percent ranges for the 3-month yield and 10-year yield in 10 years are unchanged this week.

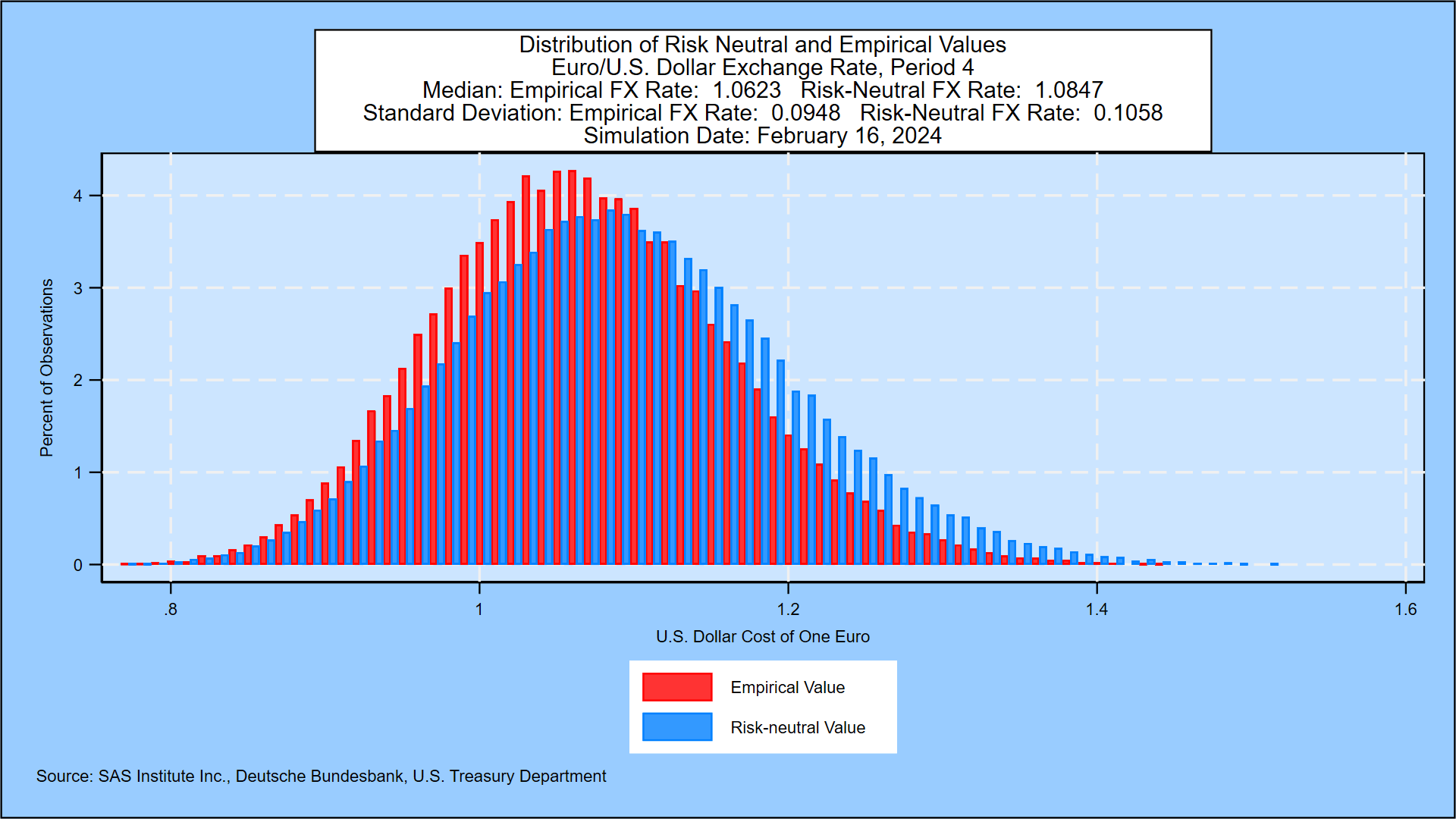

- The simulation with U.S. Treasuries shows a Euro/U.S. Dollar exchange rate at a median value of 1.0623 and a standard deviation of 0.0948 one year forward.

Author’s Note

This simulation has been done jointly with a U.S. Treasury yield simulation in a way that reflects the correlation among the 12 factors driving yields in each country. For more on the companion U.S. Treasury simulation, please contact the author. Both the Bund and the U.S. Treasury yield simulations impact foreign exchange rates, resulting in the following distribution of the Euro/U.S. dollar exchange rate one year forward:

{kind=link}

This Week’s Simulation of Bund Yields

As explained in Prof. Robert Jarrow’s book cited below, forward rates contain a risk premium above and beyond the market’s expectations for the 3-month forward rate. We document the size of that risk premium in the graph below, which shows the zero-coupon yield curve implied by current German Bund prices compared with the annualized compounded yield on 3-month bills that market participants would expect based on the daily movement of government bond yields in 14 countries since 1962. The risk premium, the reward for a long-term investment, is moderately positive and remains so over the full maturity range to 30 years. The graph also shows a steady downward shift in yields in the first seven years, as explained below....

Weekly Bund Yield Forecast, Feb. 16: Negative 2/10-Year Spread Probability Rises To 62.6% In August