TBT - Weekly Forecast March 28 2024: No End In Sight For Record Negative Treasury Spread Streak

2024-04-01 12:25:35 ET

Summary

- The Treasury curve was unchanged at 2 years and was down 2 basis points at 10 years over the last week.

- As a result, the current negative 2-year/10-year Treasury spread widened to negative 39 basis points this week compared to negative 37 basis points a week earlier.

- The current negative 2-year/10-year Treasury spread is the longest such streak since the launch of the 2-year note in 1976.

- The probability that the 2-year/10-year Treasury spread is still negative in the 13 weeks ending September 26, 2024, is 68.4%, compared to 65.9% last week.

- The long-term peak in 1-month forward Treasuries is now 5.11%, down 0.01% from last week and still below the near-term peak at 5.47%.

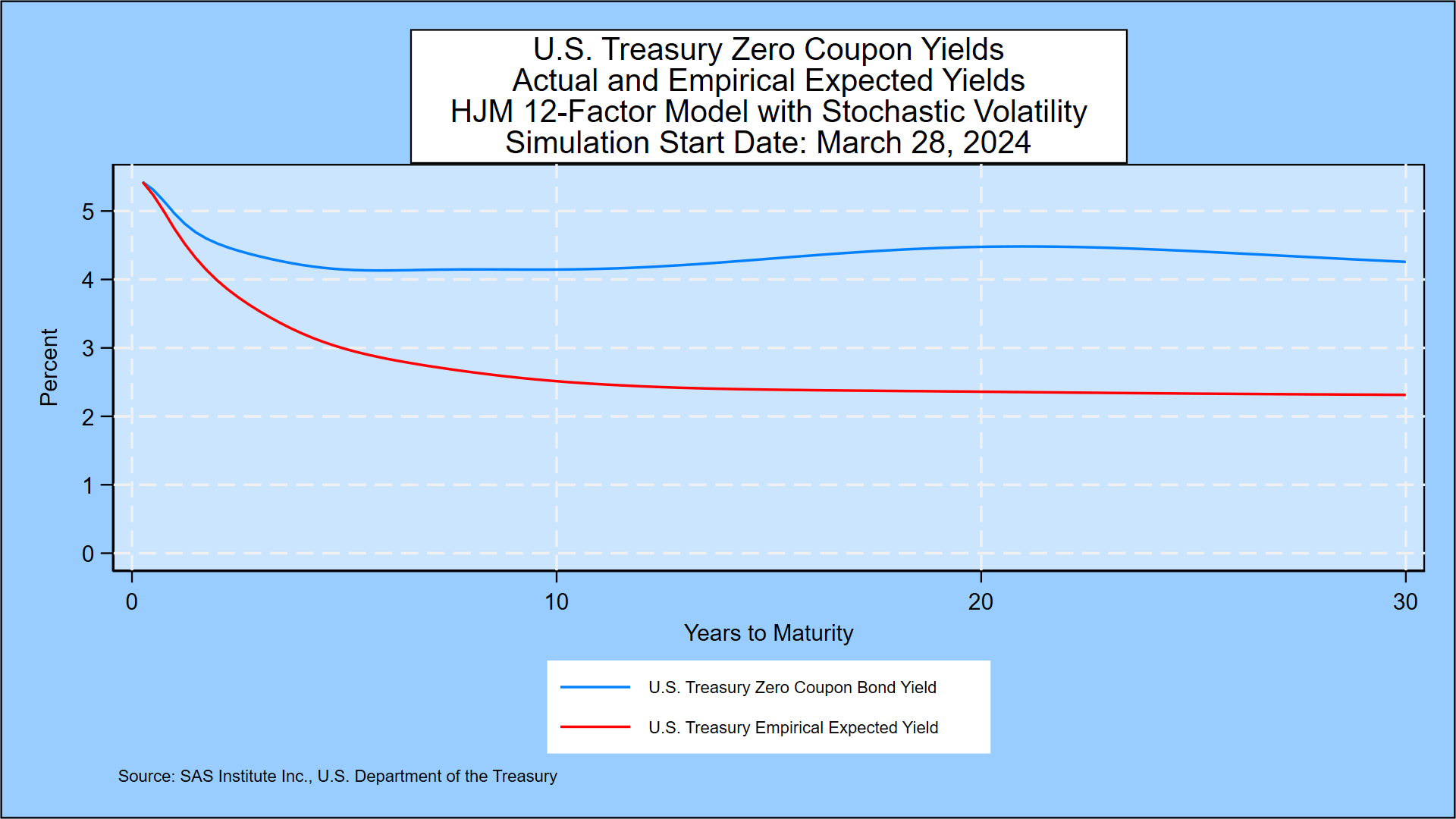

As explained in Prof. Robert Jarrow’s book cited below, forward rates contain a risk premium above and beyond the market’s expectations for the 3-month forward rate. We document the size of that risk premium in this graph, which shows the zero-coupon yield curve implied by current Treasury prices compared with the annualized compounded yield on 3-month Treasury bills (US3M) that market participants would expect based on the daily movement of government bond yields in 14 countries since 1962. The risk premium, the reward for a long-term investment, is large and widens over most of the 30 year maturity range (US30Y). The graph also shows a sharp downward shift in expected yields in the first few years, then the decline continues at a slow but steady pace for the full 30 years. We explain the details below.

Weekly Forecast, March 28, 2024: No End In Sight For Record Negative Treasury Spread Streak{kind=link}