CSGP - Weitz Value Fund Q1 2023 Commentary

2023-06-29 10:29:00 ET

Summary

- Weitz Investment Management is a boutique, employee-owned asset management firm headquartered in Omaha, Nebraska.

- The Value Fund's Institutional Class returned +6.05% for the first quarter compared to +7.46% for the Russell 1000.

- On balance, it was a reasonable quarter for the Fund. Solid absolute returns were welcome after a tough year.

- At a minimum, the Fed's inflation-fighting formula just became more complicated - as banks repair their balance sheets, financial conditions will further tighten.

The Value Fund's Institutional Class returned +6.05% for the first quarter compared to +7.46% for the Russell 1000. For the fiscal year ended March 31, 2023, the Fund's Institutional Class returned -10.88% compared to -8.39% for the Russell 1000.

On balance, it was a reasonable quarter for the Fund. Solid absolute returns were welcome after a tough year. Several stocks that had been laggards in 2022 rebounded nicely. A few new issues cropped up along the way, which we addressed head-on. Relative results were not yet back to our standards, as more aggressive growth stocks not held in the Fund drove the broader indexes.

Despite widespread positive returns, conditions were far from placid. The March failures of Silicon Valley Bank ( SIVBQ ) and Signature Bank (SBNY) set off a wave of concern across financial markets.

While swift action by the Federal Reserve, Federal Deposit Insurance Corporation (FDIC), and Treasury Department ensured that depositors of those institutions would not lose money, confidence was shaken in all but the largest financial institutions. Please see this quarter's "Value Matters" for our take on how the bank failures fit into the bigger picture.

At a minimum, the Fed's inflation-fighting formula just became more complicated - as banks repair their balance sheets, financial conditions will further tighten. Fearful of recession and chastened by 2022's market declines, Wall Street has become even more adamant that the Fed should pause rate hikes now and move to cut interest rates later this year. This widely held consensus view is squarely at odds with the Fed's stated intentions, setting up a showdown that will keep things "interesting" for the foreseeable future. In our view, the case for owning durable, resilient, and adaptable businesses has never been stronger.

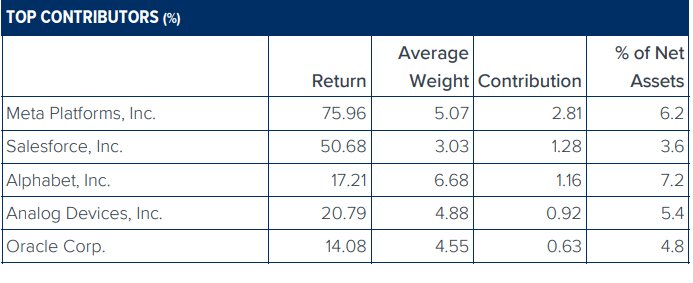

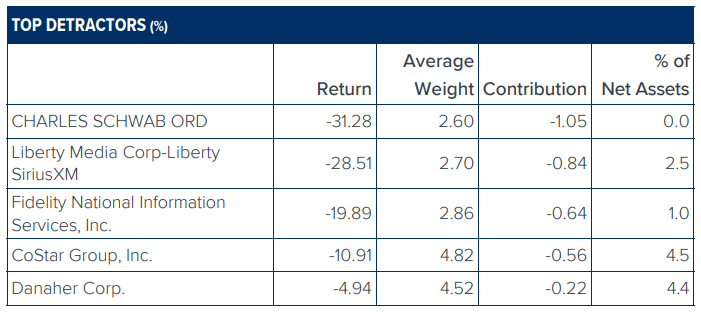

The Fund's technology-related stocks were the largest quarterly contributors, with Meta Platforms ( META ), Salesforce ( CRM ), Alphabet ([[GOOG]], [[GOOGL]]), and Analog Devices (ADI) pacing the gains. Meta was the standout, as the company's "Year of Efficiency" mantra (an initiative to restructure and improve financial performance) drove a dramatic stock price rebound from depressed levels. Meta continued to adapt to Apple's iOS changes that had impaired its ad targeting capabilities. We are encouraged by the combination of solid engagement trends, enhanced tools for advertisers, and prudent expense management. Charles Schwab ( SCHW ), Liberty SiriusXM ( LSXMK ), Fidelity National Information Services (FIS), and CoStar Group ( CSGP ) were the Fund's largest quarterly detractors.

We sold the Fund's Schwab position in March. Our concerns were primarily related to the depth and length of a potential earnings valley. As the Fed pushed up short-term interest rates, money market funds and Treasury bills provided savers with clear alternatives to banks' ultra-low yielding deposits. Schwab's near-term cost of funding seemed likely to rise materially, one way or the other. Some earnings erosion is reflected in the stock price, but we sold as our view of the risk/reward framework shifted considerably. While our final exit price was well below the highs, Schwab was an exceptional contributor to Fund returns over the past three years.

Analog Devices, Oracle ( ORCL ), CoStar Group, and Meta Platforms were the Fund's largest contributors for the fiscal year. Analog Devices and Oracle delivered strong business results with few surprises, while timely buying and selling helped boost CoStar and Meta onto the leaderboard. Liberty Broadband, Alphabet, FIS, and Liberty SiriusXM were the largest detractors for the Fund's fiscal year.

Necessary capital investment cycles at Liberty Sirius XM (new satellites and streaming technology) and Liberty Broadband (fiber-competitive speed upgrades and network expansions at Charter Communications) disappointed investors looking for quick wins. The spending will no doubt crowd out some share repurchases in the short run. Still, we think these investments are prudent and should bolster the businesses' competitive positions with acceptable returns, and we remain confident in the long-term potential of both stocks.

We sold over half of the Fund's FIS position after the company announced the planned spin-off of the merchant business. These sales generated a capital loss, which will help offset realized gains elsewhere. Our original investment thesis has changed, triggering another deep review of the company and stock. Our plan is to either rebuild a core position size or exit the stock entirely after we clear the 30-day "wash sale" period. We also added to the Fund's holdings of Accenture and Liberty SiriusXM in March at attractive price levels.

The portfolio is focused and well-aligned with our vision for successful large-cap investing. We have concentrated ownership stakes in 25 companies, with the top ten representing over half of the portfolio. Each position is significant enough to matter, yet none can individually make or break our results. Our current estimate is that the portfolio trades at a price-to-value in the mid-70s, though these estimates remain more fluid than usual. We believe that many holdings have a chance for healthy gains over a multi-year period. Others are priced for adequate return potential primarily from expected growth in per-share business value.

Top Relative Contributors and Detractors

{kind=link}

{kind=link}

Data is for the quarter ending 03/31/2023. Holdings are subject to change and may not be representative of the Fund's current or future investments. Contributions to performance are based on actual daily holdings. Returns shown are the actual returns for the specified period of the security. Additional securities referenced herein as a percent of the Fund's net assets as of 03/31/2023: Accenture plc, 3.2%; Apple, Inc., 0.0%; Charter Communications, Inc., 0.0%; SVB Financial Group, 0.0%; Signature Bank, 0.0%.

{kind=link}

The opinions expressed are those of Weitz Investment Management and are not meant as investment advice or to predict or project the future performance of any investment product. The opinions are current through 04/20/2023, are subject to change at any time based on market and other current conditions, and no forecasts can be guaranteed. This commentary is being provided as a general source of information and is not intended as a recommendation to purchase, sell, or hold any specific security or to engage in any investment strategy. Investment decisions should always be made based on an investor's specific objectives, financial needs, risk tolerance and time horizon.

Data quoted is past performance and current performance may be lower or higher. Past performance is no guarantee of future results. Investment return and principal value of an investment will fluctuate, and shares, when redeemed, may be worth more or less than their original cost. Please visit weitzinvestments.com for the most recent month-end performance.

Investment results reflect applicable fees and expenses and assume all distributions are reinvested but do not reflect the deduction of taxes an investor would pay on distributions or share redemptions. Net and Gross Expense Ratios are as of the Fund's most recent prospectus. Certain Funds have entered into fee waiver and/or expense reimbursement arrangements with the Investment Advisor. In these cases, the Advisor has contractually agreed to waive a portion of the Advisor's fee and reimburse certain expenses (excluding taxes, interest, brokerage costs, acquired fund fees and expenses and extraordinary expenses) to limit the total annual fund operating expenses of the Class's average daily net assets through 07/31/2023.

The Gross Expense Ratio reflects the total annual operating expenses of the fund before any fee waivers or reimbursements. The Net Expense Ratio reflects the total annual operating expenses of the Fund after taking into account any such fee waiver and/or expense reimbursement. The net expense ratio represents what investors are ultimately charged to be invested in a mutual fund. Performance quoted for Institutional Class shares before their inception (07/31/2014) is derived from the historical performance of the Investor Class shares and has not been adjusted for the expenses of the Institutional Class shares, had they, returns would have been different.

Index performance is hypothetical and is shown for illustrative purposes only. You cannot invest directly in an index. The Russell 1000 measures the performance of the large-cap segment of the U.S. equity universe. It is a subset of the Russell 3000 and includes approximately 1,000 of the largest securities based on a combination of their market cap and current index membership. The S&P 500 is an unmanaged index consisting of 500 companies generally representative of the market for the stocks of large-size U.S. companies.

Consider these risks before investing: All investments involve risks, including possible loss of principal. These risks include market risks, such as political, regulatory, economic, social and health risks (including the risks presented by the spread of infectious diseases). In addition, because the Fund may have a more concentrated portfolio than certain other mutual funds, the performance of each holding in the Fund has a greater impact upon the overall portfolio, which increases risk. See the Fund's prospectus for a further discussion of risks related to the Fund. Investors should consider carefully the investment objectives, risks, and charges and expenses of a fund before investing. This and other important information is contained in the prospectus and summary prospectus, which may be obtained at weitzinvestments.com or from a financial advisor. Please read the prospectus carefully before investing. Weitz Securities, Inc. is the distributor of the Weitz Funds.

Editor's Note: The summary bullets for this article were chosen by Seeking Alpha editors.

For further details see:

Weitz Value Fund Q1 2023 Commentary