WFCNP - Wells Fargo: 4 Themes That Matter

2023-06-15 10:49:04 ET

Summary

- WFC has underperformed the broader markets this year and we are not sufficiently convinced there will be a drastic shift in the status-quo.

- We touch upon some of the key operating metrics.

- Shareholder distributions could perk up after the Fed's stress test results on the June 28.

- Valuations look reasonable, but the medium-term earnings growth on offer isn't too compelling.

- The technical picture reiterates a neutral stance.

Introduction

This year, even though the stock of diversified bank - Wells Fargo ( WFC ) has experienced a choppy ride (note how the annualized standard deviation of monthly returns has spiked), on a YTD basis, the return profile has been nothing to write home about.

YCharts

While the broader markets have ended up delivering returns within the mid-teens threshold, WFC’s YTD returns have been less than 4%.

YCharts

In H2-22, we don’t see any outstanding catalyst that could reverse WFC’s prospects, nor do we expect the stock to slump. Here are some of the important themes that weigh on our neutral stance.

NII dynamics

Even though the FOMC decided to keep rates on hold in the latest June meeting, they also suggested that two separate 25bps hikes could still come through later this year. At this stage of the hiking cycle, the “higher for longer” narrative may not be wholly conducive for banks, even as loan growth appetite continues to abate (WFC management only expects low single-digit growth in the loan growth for the year).

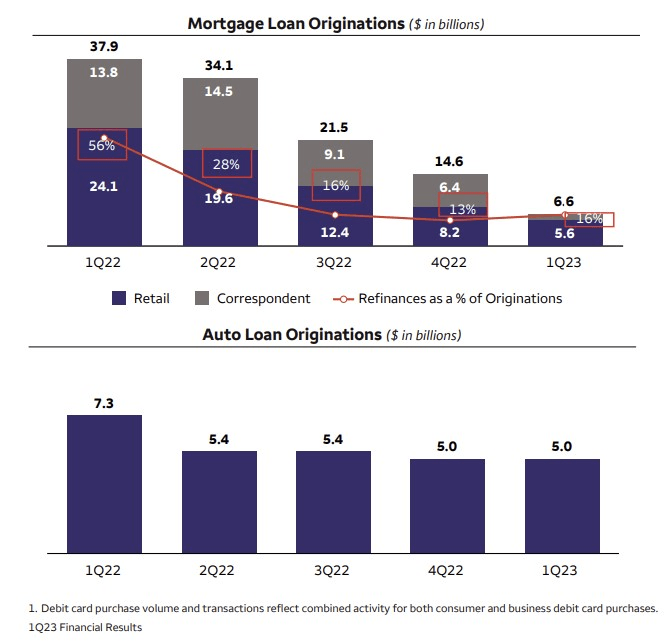

In WFC’s largest division - Consumer banking, note that mortgage originations continue to slump, even as auto loans have gone flat.

{kind=link}

We believe investors ought to pay greater attention to trends on the deposit front, as the deposit betas (particularly on the large corporate side) will start leaving a more profound mark on NII (Net Interest Income) progression (or the lack thereof).

Quarterly Presentations

With Wells Fargo, we’ve already seen the Q1 NII come off by 0.5% sequentially (although this is largely attributable to fewer business days), but it’s fair to expect a more pronounced step down in Q2 as well. Currently, in this environment the banking industry is already poorly positioned relative to other high-yielding arenas, so expect even more competitive intensity on pricing as these banks fight over procuring deposits and maintaining their deposit base. What’s also concerning is that the contribution of WFC’s low-cost non-interest bearing deposits dropped to 32% in Q1 from 35% in Q4.

It’s worth noting that even though WFC benefitted from some flight-to-safety deposit momentum during the regional banking crisis in March, that appears to have petered out. All in all, WFC’s deposit base in Q1 dropped both on an annual basis (-7%) as well as a sequential basis (-2%).

Asset Quality

On the asset quality front as well, investors ought to prepare for further sequential deterioration (the net charge-off ratio has been trending up for four straight quarters now) which could weigh on profitability and limit ROE expansion. Note that a year ago, WFC's bottom line was getting a fillip from a write-back in provisions, but in Q1-22, this even surged to hit levels of $1.2bn (also up by 26% from the December quarter)

Q1 presentation

Whilst it is heartening to note that the troubled commercial real estate segment only accounts for 4% of WFC’s total loan book, investors should not cast aside the risks associated with the credit card side of the portfolio, particularly as the previously sturdy wage growth trends appear to dip.

Capital Position And Shareholder Returns

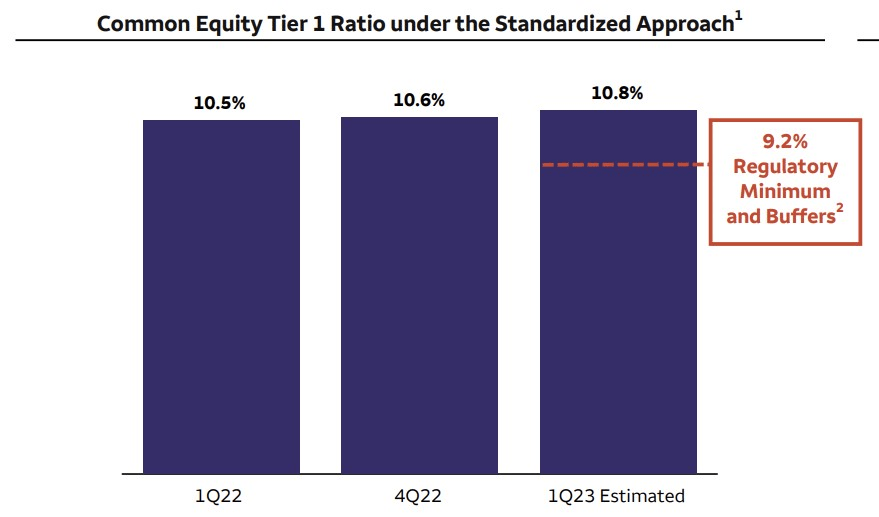

On the capital front, WFC is pretty well-positioned, and we expect it to come through the Fed’s stress test results without too much trouble (for the uninitiated, the results will be announced less th an two we eks from today).

For context, in Q1, WFC's CET1 ratio came in at 160bps over the regulatory minimum of 9.2%. Crucially, there’s another ratio that measures the total loss-absorbing capacity of a bank over its risk-weighted assets; on this front, whilst banks are required to maintain a minimum ratio of 21.5%, WFC’s figure is almost 200bps higher at 23.3%.

{kind=link}

Given some of the excess capital that WFC has, investors can expect the level of buybacks to persist for the next few quarters. After stalling its ongoing buyback program for three quarters, the company ended up repurchasing 86m shares in Q1, spending around $4bn . As things stand, the bank still has around 164m shares to repurchase as part of its 500m share buyback plan announced in Jan 2021.

WFC must continue to press the pedal on the buyback front because this was a stock that traditionally enjoyed an average buyback yield of over 8%, but currently, it only stands at a lowly rate of 2.55%.

YCharts

Some investors would be happy to look past the buyback theme if the dividend angle was burning bright, but at the current price levels, WFC's dividend yield of 2.85% comes across as sub-par, as it is below the long-term average of 3.11%. Perhaps this could change if the bank announced a hike of 20% or so (this could put the yield at 3.4%), after the stress test results on June 28.

YCharts

Closing Thoughts - Valuations And Technicals

On the valuation front, WFC is priced cheaply at less than 1x book value; to be precise, relative to its long-term average, you could pick this up at a discount of 10%.

YCharts

However, before you get too carried away with the discount, also do consider that WFC’s earnings growth is likely to be quite subdued over the next two years, particularly in FY24 where earnings are expected to grow at only 0.6% YoY (based on consensus of 19 sell-side analysts).

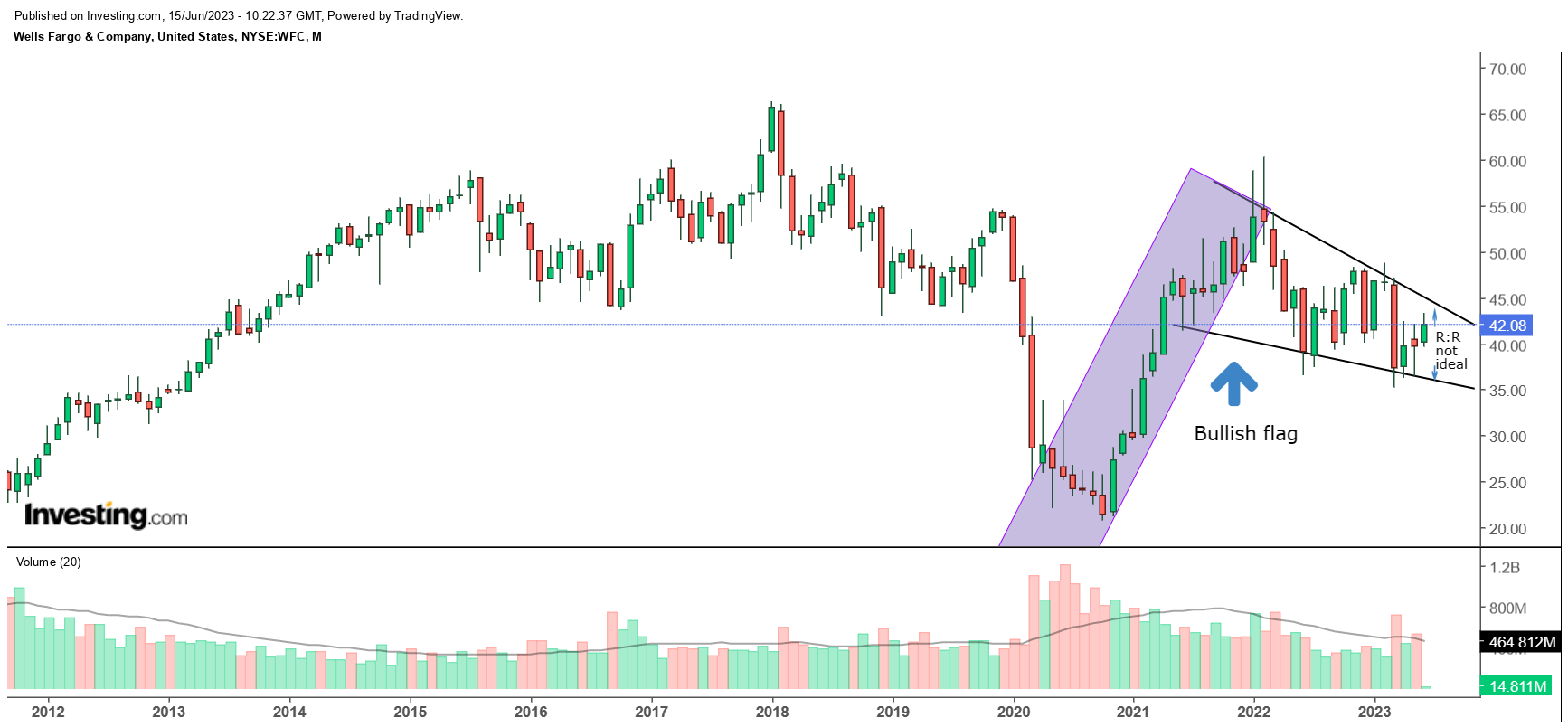

On the technical front, even though we appreciate the long-term bullish flag pattern that has been underway for a while now, we don’t think the risk-reward is at its most opportune point. If we look at the two downward-sloping lines, we can see that the price is currently a lot closer to the upper boundary; we believe investors ought to buy the stock closer to the $35 levels, the lower line support.

{kind=link}

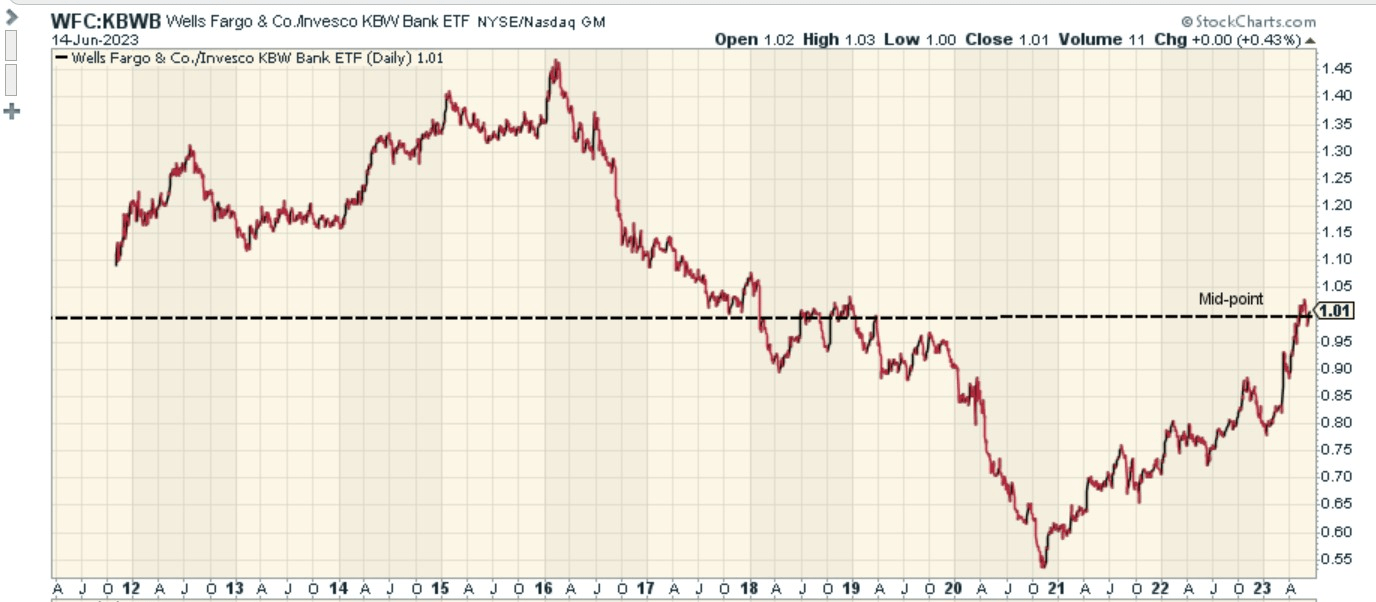

Also note that WFC is unlikely to receive too much interest from mean-reversion-oriented market players. The chart below highlights WFC's strength relative to the Invesco KWB Bank ETF. We can see that after four years of trading below the mid-point of the decade-long range, that ratio has finally mean-reverted, implying limited scope for rotation into WFC.

{kind=link}

For further details see:

Wells Fargo: 4 Themes That Matter