RKT - Wells Fargo Leaves A Rithm Capital Shaped Hole In The Mortgage Market

Summary

- In this rapidly changing world, the ability to pivot is a key to success.

- Rithm Capital is significantly more nimble than its competitors.

- It is well positioned to grow market share and trades at a nice value.

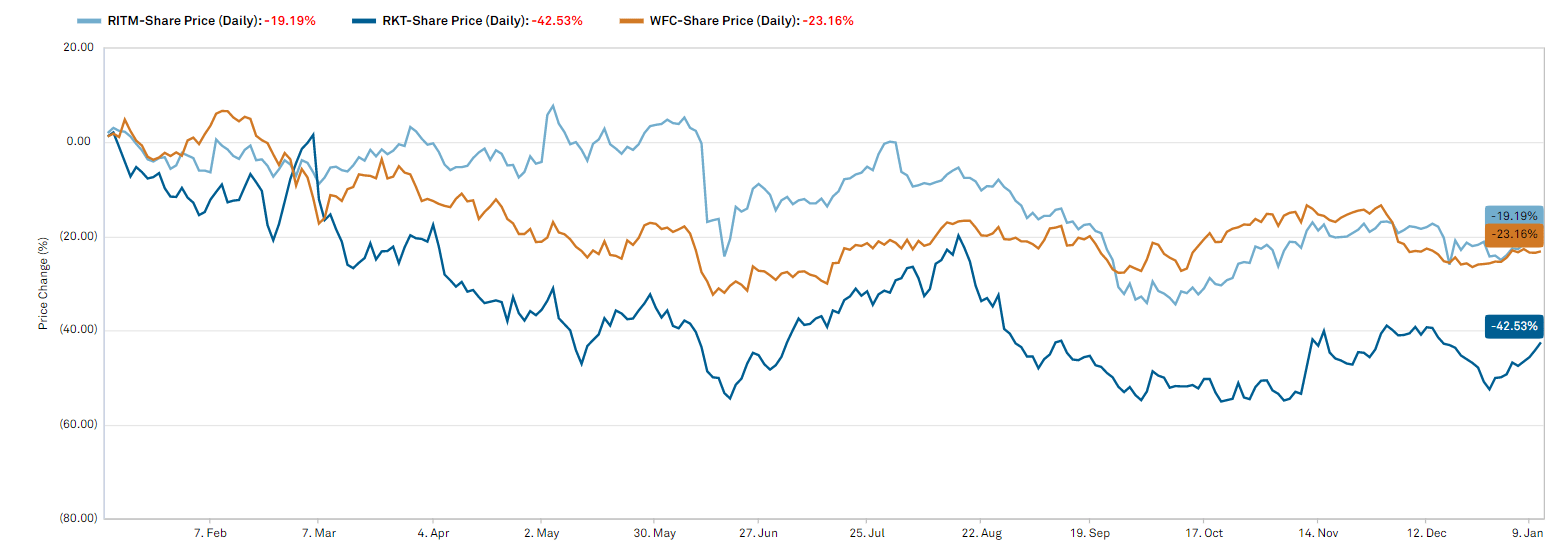

The mortgage origination market is one of the areas most directly affected by the now higher interest rates. Pure-plays like Rocket Companies ( RKT ) are down around 40% while those like Wells Fargo ( WFC ) and Rithm Capital ( RITM ) that only have partial exposure are down a bit less.

S&P Global Market Intelligence

{kind=link}

Most of the price declines in the space are fundamentally justified, but I think Rithm Capital has been unfairly caught in the crossfire. The portfolio weights specific to RITM make it largely immune to what has happened with mortgages which places the company in an opportunistic position to gobble up the market share vacated by competitors.

On January 10 th , Wells Fargo announced plans to largely exit the mortgage origination business with exception to existing WFC customers. This, along with the shrinking of other mortgage originators, has brought supply down to be in balance with the now much lower demand. As the mortgage market recovers, RITM will be among the best positioned to scale back up due to its relatively better financial positioning and non-bank status.

Let me begin with an overview of the industry in terms of what has happened and the forward outlook. We will then follow with RITM’s specific positioning and its individual outlook.

The Mortgage Industry

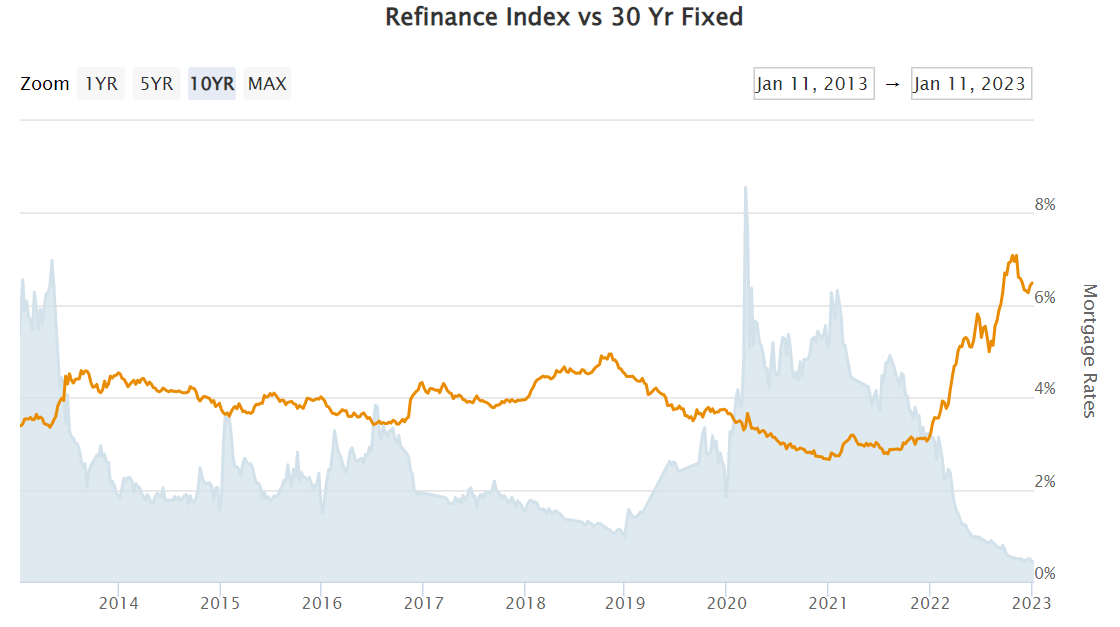

For decades, the mortgage industry has benefitted from new mortgage applications being heavily supplemented by refinancing activity. As rates dropped below the going in rate of existing mortgages, homeowners were incented to refinance resulting in huge volume and the fee income that comes with that.

{kind=link}

As interest rates ticked up in recent quarters the opposite happened. Now the majority of mortgages are at rates lower than the prevailing market rate. Not only are refinances no longer encouraged, but they are actively avoided as doing so dramatically increases one’s carrying cost. Those with cheap existing mortgages are also less likely to move so new mortgage origination volume is also impaired.

As you can see in the chart below, refinance volume (shaded) is inversely correlated with mortgage rates and has now hit by far its lowest level in decades.

{kind=link}

Mortgage origination is a lucrative business when it is active. Each refinancing generates fee revenue for the originator, but it is also a head-count intensive business.

With the volume largely shut off just about the entire industry is having to lay off a substantial portion of its workforce. This scaling down has already been happening continuously and helps supply of mortgage origination more closely match demand for mortgages. It also helps preserve margins.

Wells Fargo is a fairly big player so its full exit represents a rather large step down in the supply that has otherwise been declining more smoothly.

Outlook

Eventually, the volume of origination will rebound to its normal levels regardless of what happens to interest rates. Simply put, people need homes and most need mortgages to buy a home. A decline in interest rates would accelerate the rebound, but I do see volume normalization as an inevitability.

Timing of rebound

Volumes have already been depressed for about a year. I suspect they remain low for 1 to 3 more years depending on the path of interest rates.

Relative positioning within industry

Mortgage pure-plays have to endure an extended period of time in which revenues will be severely reduced. Cost cutting measures will likely see most of them through, but that doesn’t fix the revenue declines. So while the industry wide demand declines are temporary, the damage to earnings is very real.

For this reason, I think the hybrids are much better off and Rithm Capital takes the cake as best positioned. It has 4 distinct advantages that I think will lead to significant market share capture.

- Low overall revenue concentration in mortgage origination

- MSR portfolio value gains fully hedged the rise in interest rates

- Strong business segments will keep earnings flowing while it waits for the return of mortgage market

- Non-bank status makes scaling back up much easier

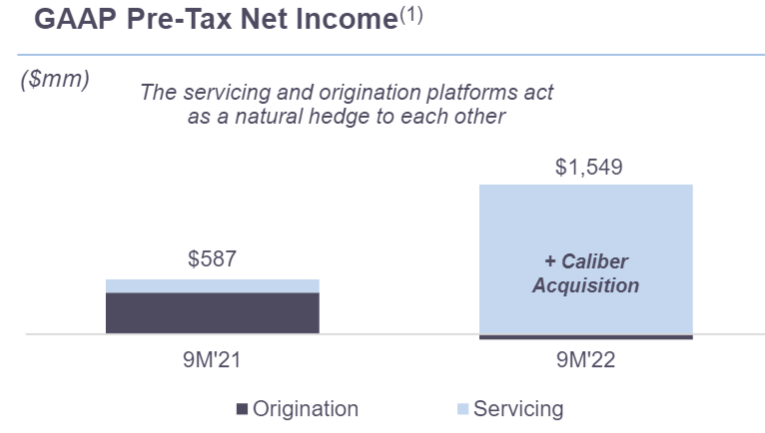

Rithm’s largest portfolio weight is in mortgage servicing rights (MSRs) and the earnings from this segment outweigh those from mortgage origination.

{kind=link}

In many ways it forms a great hedge because the same increase to interest rates that hurt originations caused their MSR portfolio to substantially gain in value. The way these work is that RITM buys the rights to service mortgages and then collects the servicing fee for the remaining duration of the loans.

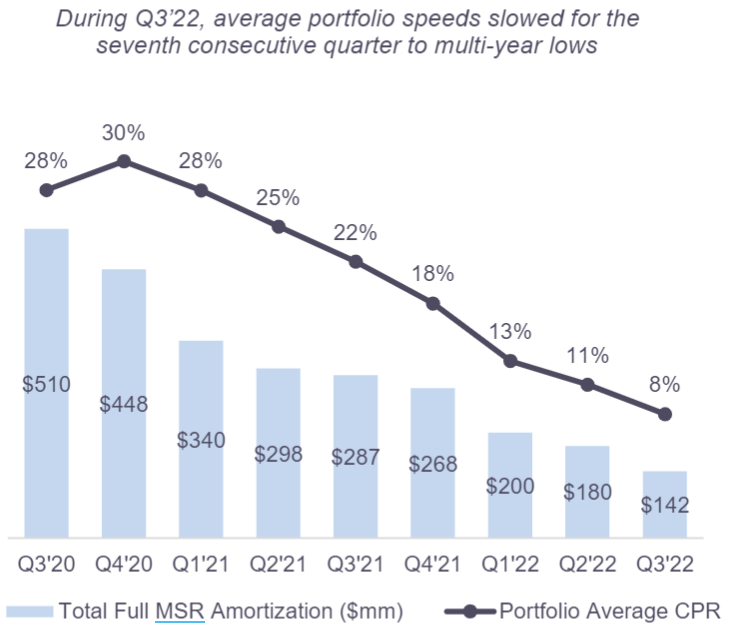

As refinancing rates declined, prepayment rates of these loans dropped from about 28% to 8%.

{kind=link}

This dramatically extends the life of the servicing revenue causing each MSR purchased earlier to deliver far more total income than originally expected. Reflecting this now longer life stream of revenues the market value of MSRs rose significantly, more than offsetting the hit to the rest of RITM’s business from higher interest rates.

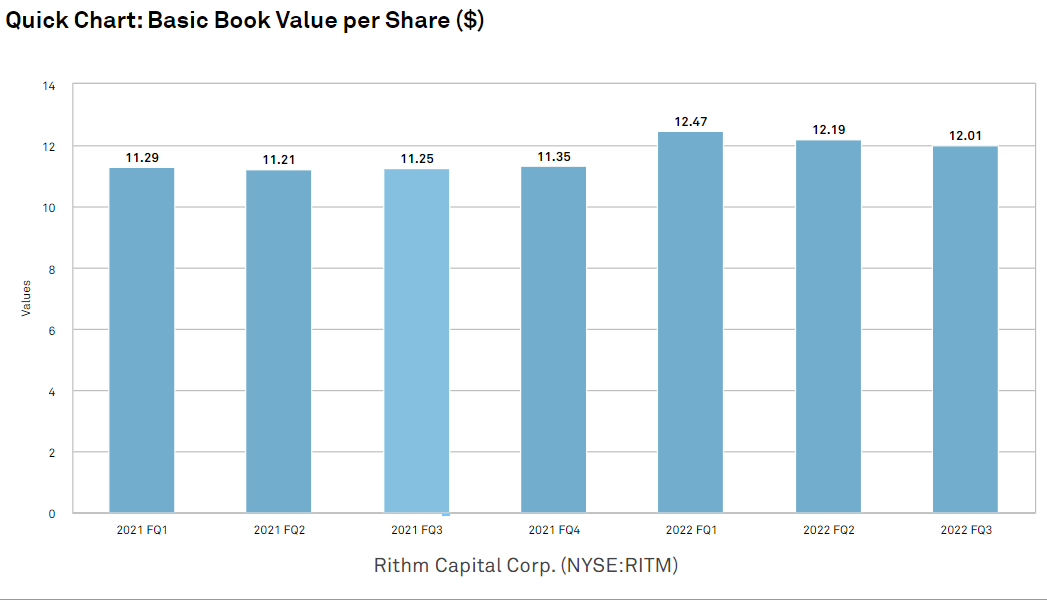

As a result, RITM’s book value is actually up moderately during the rising rate cycle.

S&P Global Market Intelligence

{kind=link}

That is a substantial difference between RITM and much of the mortgage industry which broadly experienced book value declines.

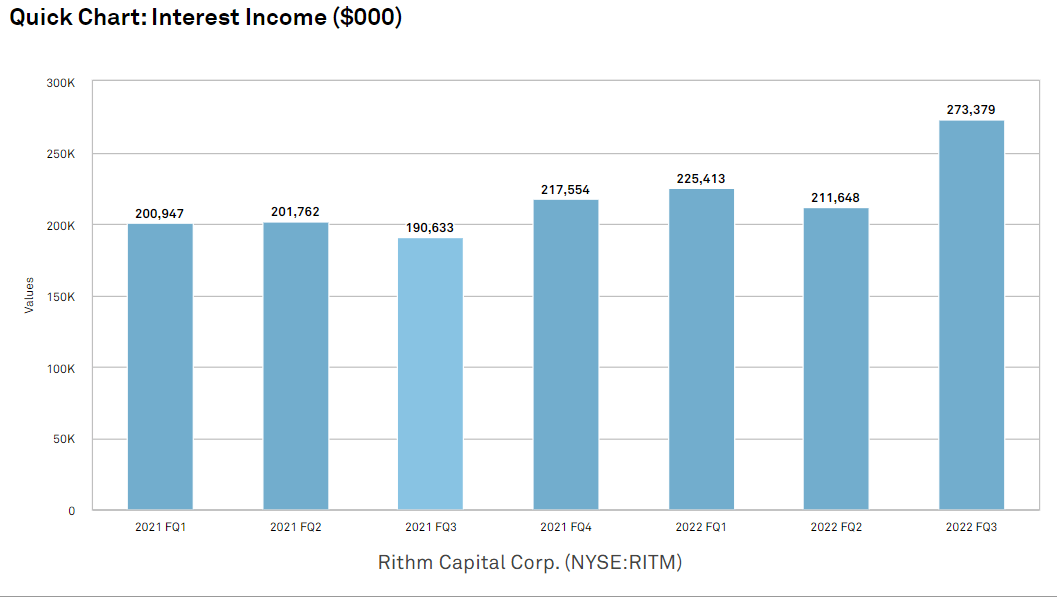

This puts RITM in good financial positioning relative to peers. It is also well positioned to wait for the mortgage market to recover as it is still generating healthy revenues from its other segments. RITM’s interest income has increased, partially from its real estate and mortgage backed securities portfolio.

S&P Global Market Intelligence

{kind=link}

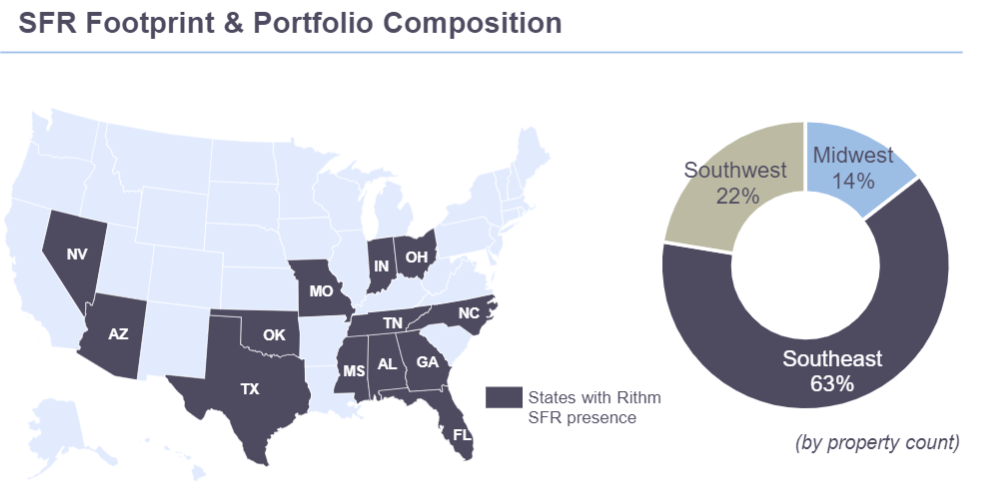

I also find its single family rental segment promising as RITM’s properties are well located in areas with job growth.

{kind=link}

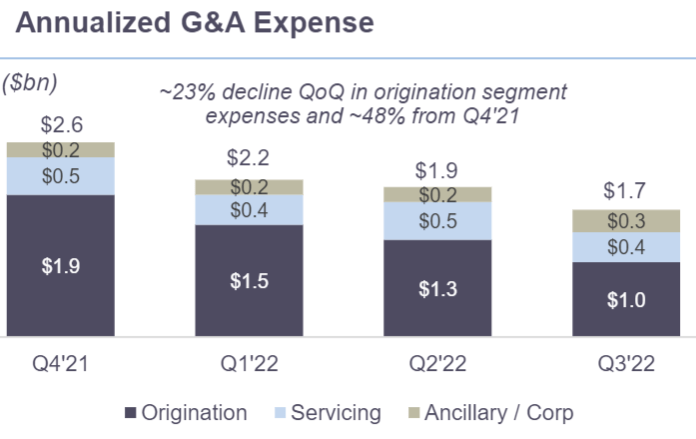

Since RITM is not reliant upon originations to generate its earnings, it was in a position to very swiftly scale down its headcount in that area. Origination based G&A declined by $900 million from Q4 21 to 3Q22.

{kind=link}

Continued cashflows from other business segments in combination with cost reductions keep RITM healthy through the downturn, but the real opportunity is what happens when the mortgage market comes back.

Non-bank status makes it easier to scale back up

Banks are over-regulated. Since the financial crisis there are SIFI rules and extensive oversight on everything they do. Perhaps one could argue that this is beneficial to the economy overall, but from a competitive standpoint it is a huge disadvantage.

As a non-bank mortgage REIT, the regulatory burden on RITM is quite lax in comparison allowing it to operate more swiftly and at lower cost. I believe this will lead to market share capture for the non-banks.

The market share that was vacated by Wells Fargo will be up for grabs and RITM is well positioned to move in.

Valuation

Despite RITM’s MSR portfolio fully offsetting the challenges of rising interest rates, there is a general malaise around home mortgages which I think has incorrectly dragged RITM down by association with its group.

Due to the price decline in combination with the book value gain, RITM now trades at 74% of book value. Since its earnings have largely remained intact due to strength in its other business segments, RITM is now trading at 6.7X forward earnings.

That is a cheap stock and I find the forward outlook to be significantly stronger than what is implied by that pricing. I think RITM will outperform the market.

An even better way to invest in it

While bullish on the common, the preferreds seem to offer a higher return due to extreme discounting to par.

Portfolio Income Solutions – preferred table – data as of 1/12/23

{kind=link}

RITM’s preferreds are a bit unusual in that the convert to floating rate yields and the terms of these were written when interest rates were considerably lower. As a result, the floating rate coupons upon conversion are at anywhere from 496 to 622 basis points above LIBOR (soon to be SOFR). Given how much the short end of the curve has risen it results in some astronomical yields.

Looking at the preferred C as an example, it has a coupon of 6.38% against a $25 par value but since it trades at $18.80 that makes it an 8.48% current yield. In 2025 it will convert to a floating rate of SOFR + 496 basis points which at today’s interest rate is a coupon of 9.78% which again due to discount would be a carrying yield of 13.00%.

On top of the big dividend, one has the potential to capture 33% capital appreciation in the return to par. I find that to be a highly attractive return profile for the preferred tranche of a large mREIT in healthy financial condition.

For further details see:

Wells Fargo Leaves A Rithm Capital Shaped Hole In The Mortgage Market