WFCNP - Wells Fargo's Share Price Run-Up Isn't Over

2024-01-16 08:58:53 ET

Summary

- Wells Fargo has faced numerous scandals and is still under a cap on its assets and growth imposed by the Fed.

- Despite this, the company has performed well financially, with strong profits and a strong balance sheet.

- The company is facing challenges with rising interest rates and increased charge-offs, but it is expected to continue driving substantial shareholder returns.

Wells Fargo ( WFC ) is one of the largest banks in the country. However, it's faced scandal after scandal, including a key scandal for making accounts for customers without their permission to hit targets. That indicates a cultural problem similar to what Boeing is going through now. The problems got so significant that the Fed capped the company's assets and growth.

That cap still hasn't been lifted. Despite that, Wells Fargo has performed incredibly well as the company has managed strong profits in a tough market. As we'll see throughout this article, we expect the company to continue outperforming, making it a valuable long-term investment.

Wells Fargo Financial Performance

Wells Fargo has continued to perform well financially, with strong performance in the most recent quarter.

{kind=link}

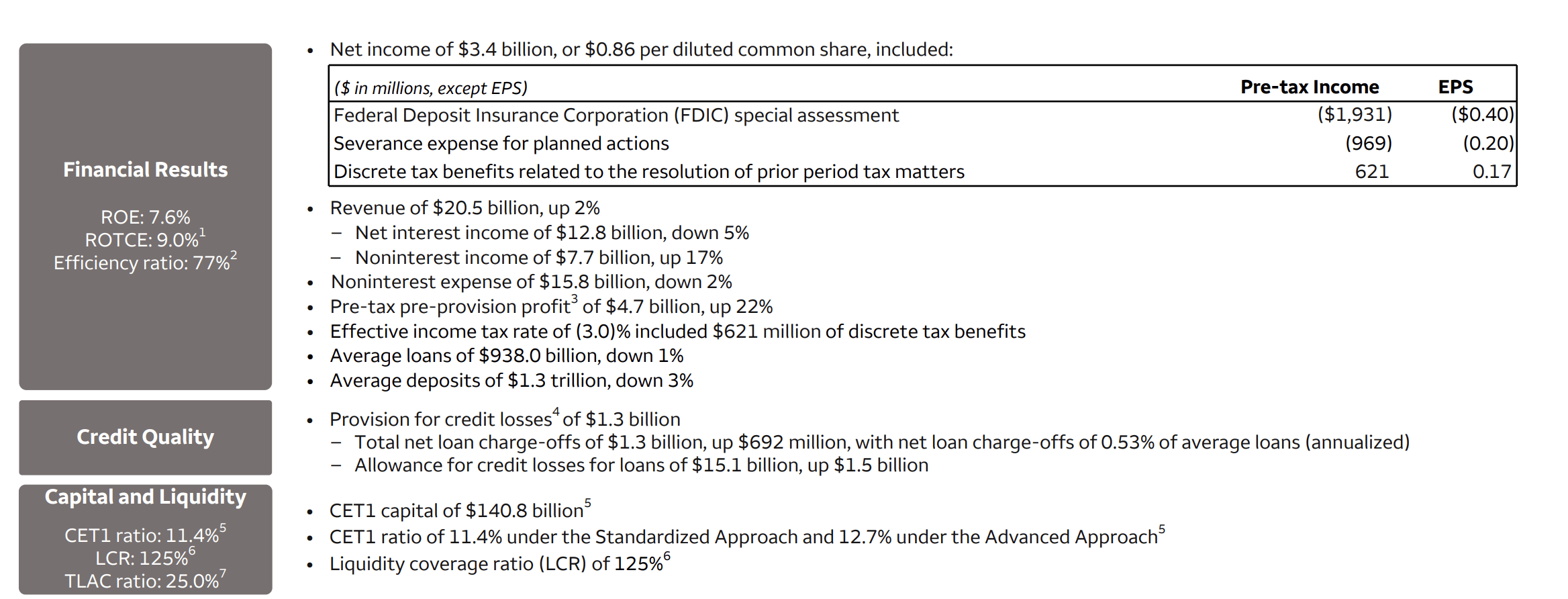

The company had $3.4 billion in net income counting a $1.9 billion FDIC special assessment after the fallout of the March 2023 bank bankruptcies, along with almost $1 billion in severance expenses for planned actions. The company managed to earn $20.5 billion in revenue up 2%, and net interest of $12.8 billion remained strong but dropped 5%.

The company maintains $140.8 billion in CET1 capital, or an 11.4% ratio, and a 125% liquidity coverage ratio. Its strength has improved due to struggles in the industry, and we expect it to maintain that strength.

Wells Fargo Financial Data

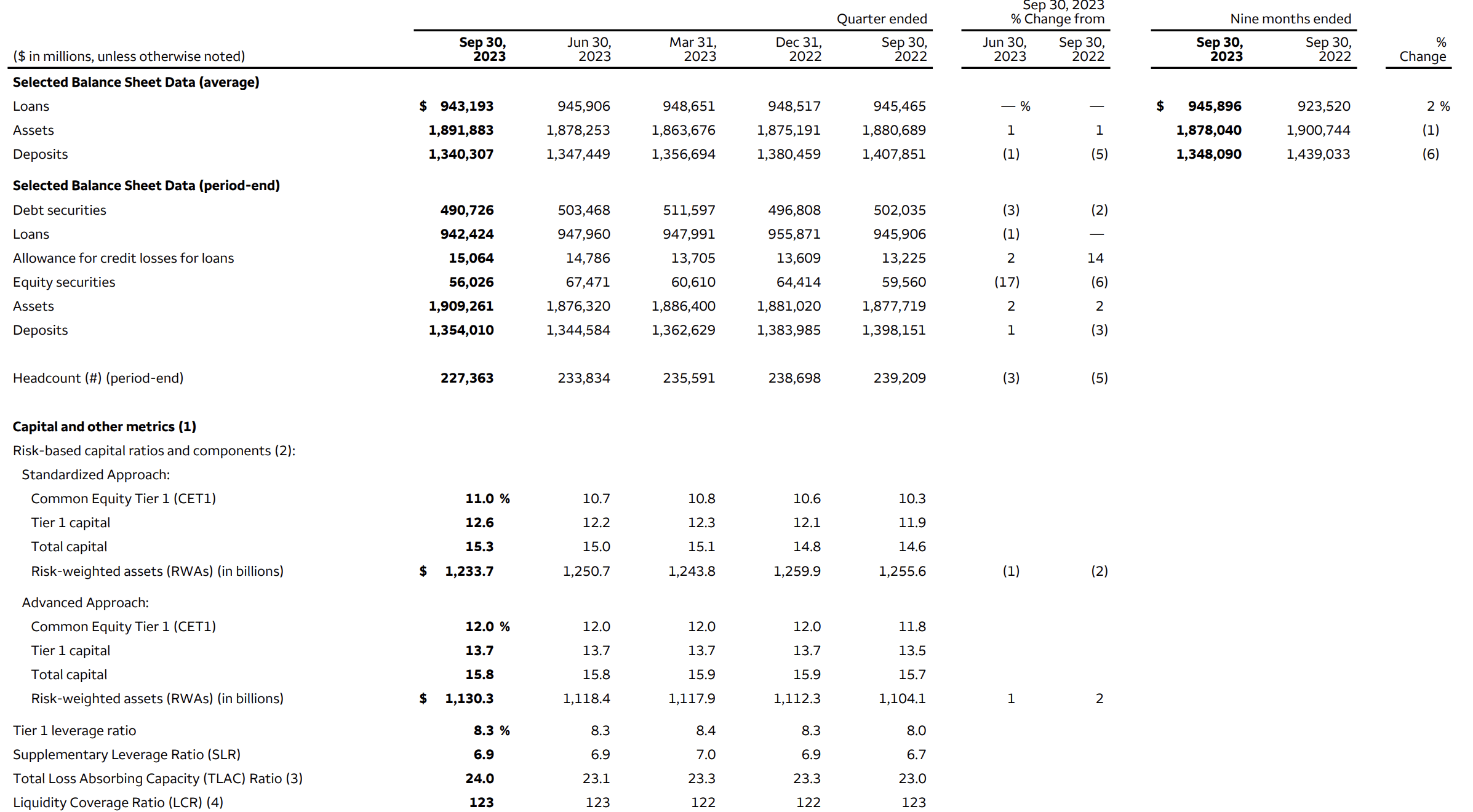

The company's financial data is visible below, with the company's assets at $1.91 trillion, or near the $1.95 trillion asset cap.

{kind=link}

The company's headcount of 227k has declined slightly. The company has $1.34 trillion in deposits and $940 billion in loans. Its assets are primarily loans, with debt securities, and other equity securities. The company's strong balance sheet enables it to both continue earning strong interest income and cover increased payouts to depositors.

The company's annualized net interest income has trended down to $50 billion and one of the biggest impacts has been increased rates the company needs to pay to depositors. The company initially was able to take advantage of raising interest rates, but as more banks raise the rates they're paying in a competitive market, the big banks are forced to adjust.

Wells Fargo Credit Charge-offs

The company in a tough rising interest rate market is also facing increased charge-offs.

{kind=link}

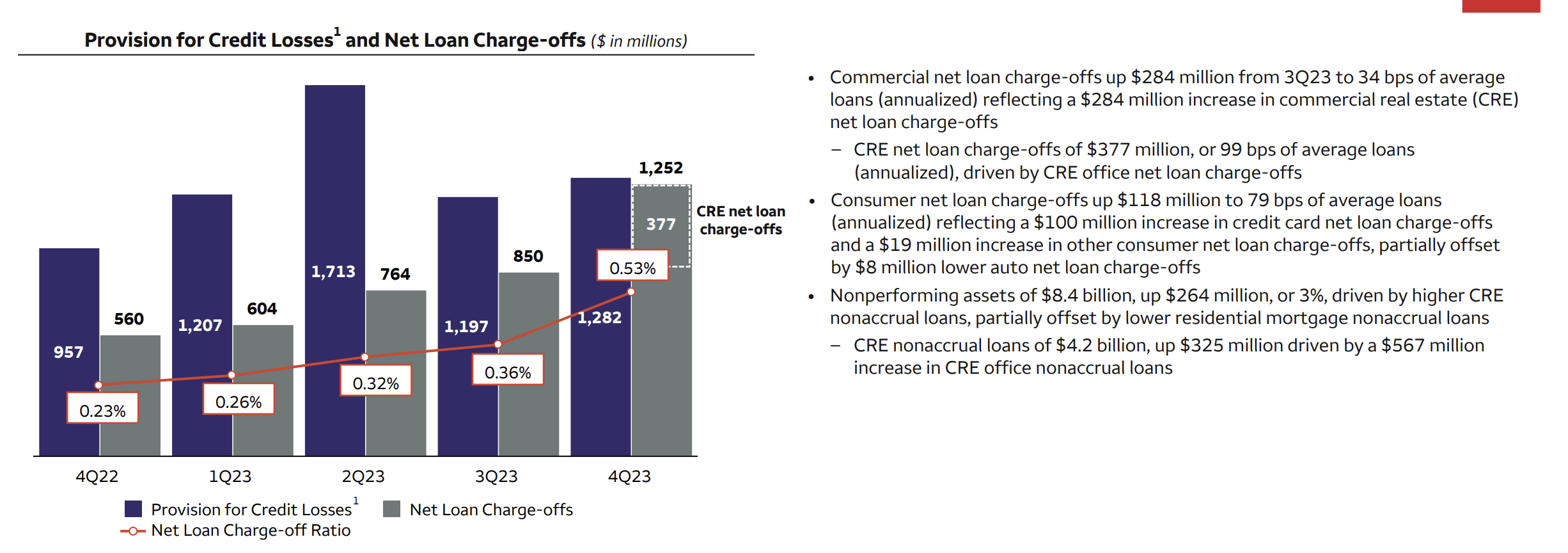

The company might earn the same on a 0-3% Fed to customer spread that it does on a 5-8%, but the default rate on one is going to be much higher as debt needs to be rolled over. The company has increased its provision for charge-offs and net loan charge-offs almost passed its provision for credit losses for the first time in a long time.

The company has also seen nonperforming assets expand to $8.4 billion, specifically led by commercial real estate. The company's loans here are $4.2 billion for CRE. We expect commercial real estate to continue to be a thorn in the side of the company.

Wells Fargo Future

Despite that, Wells Fargo has a strong future which we expect it'll be able to drive substantial shareholder returns.

{kind=link}

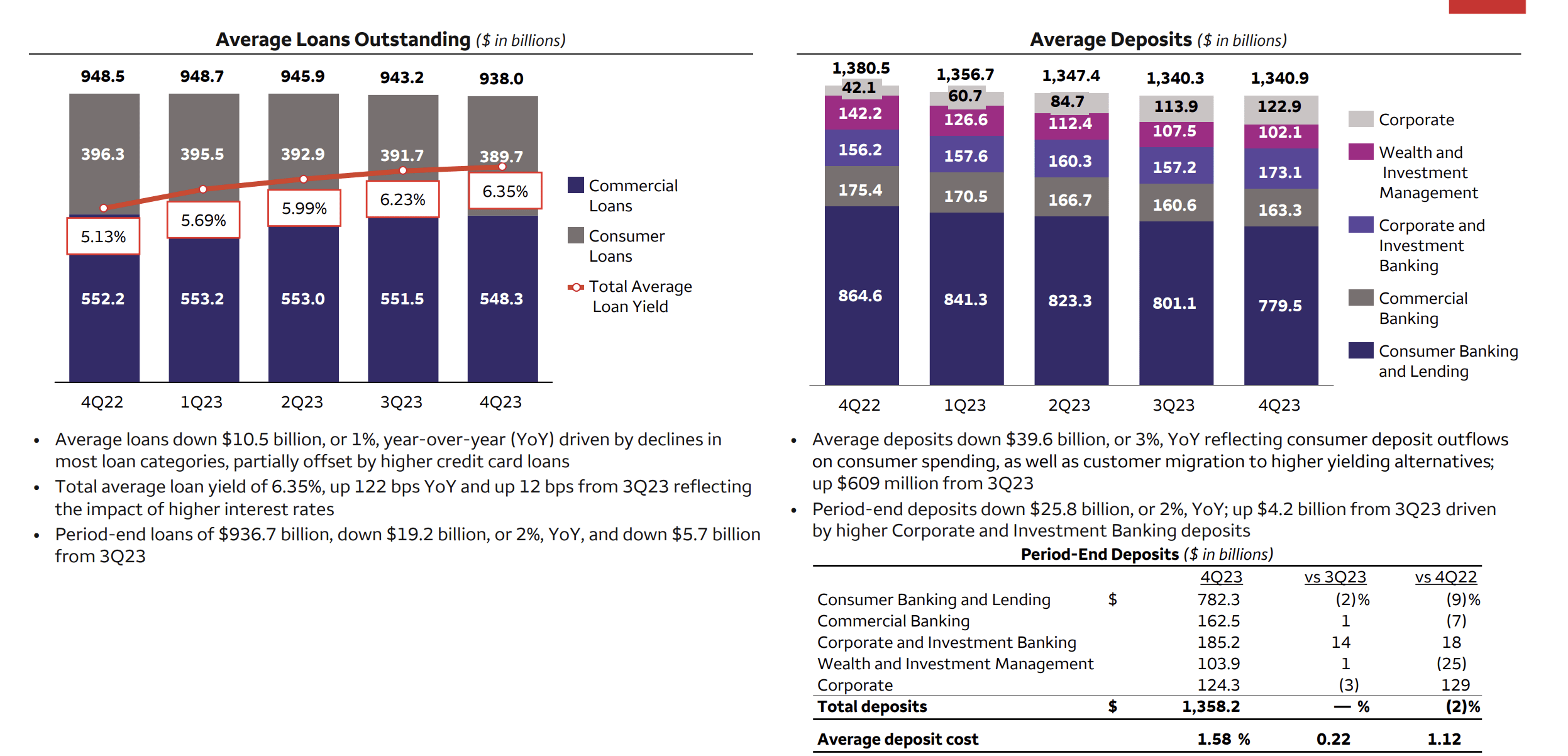

The company has managed to keep its average loans outstanding roughly constant, but thanks to rising interest rates, the average rate here has increased to 6.35%. That's a more than 1% YoY improvement for the company. The company's commercial loans continue to outweigh its consumer loans as the company takes advantage of a focus on reliability.

The company's average deposits have also trended down impacted by consumer outflows on both spendings (lower savings) and a migration to high-yield alternatives. The company's average deposit cost has gone from 1.12% to 1.58% and we expect that to continue trending up with some banks offering close to 5%.

However, if the Fed stabilizes rates, that could also stabilize outflows. Wells Fargo can continue to earn at a P/E of almost 10, earning more than $10 billion in annual profits that it can use for a variety of shareholder returns. The company has a dividend of almost 3% and recently approved a $30 billion share buyback .

That could enable the company to repurchase almost 20% of its outstanding shares, saving on dividends, and enabling future shareholder returns. At the same time, the company could have its asset cap lifted next year, which will dramatically increase potential growth and returns. The company has been forced to potentially cap businesses because of its asset cap .

Thesis Risk

The largest risk to our thesis is Wells Fargo's culture and whether the company has truly resolved the shortcomings within the company. The Fed doesn't seem to think so, and in a high interest environment, where customers are shopping around, with numerous options, that might be enough of a reason to move away from Wells Fargo. That can hurt its long-term earnings.

Conclusion

Wells Fargo has an impressive portfolio of assets. The company has managed to take advantage of rising interest rates while working to stop that from trickling down to depositors. That's customers who are interested in the bank are interested in the reliability that it offers to customers and the stability it has in a tough market.

The company's future is partially tied to the Fed revoking the $1.95 trillion asset cap that it currently has. The company is continuing to generate strong interest income, and it's repurchasing shares along with paying a strong dividend. We expect the company to be able to pay a double-digit shareholder returns with growth, making it a valuable investment.

Let us know your thoughts in the comments below.

For further details see:

Wells Fargo's Share Price Run-Up Isn't Over