QSR - Wendy's: Analyzing Its Position In A Competitive Industry

2023-08-07 13:13:24 ET

Summary

- Wendy's has a strong business model and is expected to grow through international expansion, new location openings, and technological development.

- Economic conditions represent a near-term risk to the business, primarily due to slowing demand, although margins are not necessarily protected, either.

- WEN has a significantly larger debt balance relative to earnings, when compared to peers. This has the potential to restrict the future growth of the business and its attractiveness.

- WEN's financial performance looks good relative to peers, while being undervalued. When factoring in its weaknesses, however, we do not see sufficient upside.

Investment thesis

Our current investment thesis is:

- Wendy's (WEN) has a solid business model, with healthy growth ahead through international expansion, menu, and marketing innovation, as well as technological innovation. Demand could slow in the coming quarters due to economic conditions, as discretionary spending declines.

- The business has many attractive financial qualities, with above-average profitability and consistent sale-restaurant growth. The issue is that the business is highly indebted, impacting the future of the business. For this reason, we are hesitant to apply a buy rating without an attractive risk-adjusted return.

Company description

Wendy's Company is a leading quick-service restaurant ((QSR)) chain that operates and franchises a global network of Wendy's restaurants. With headquarters in Dublin, Ohio, Wendy's is known for its high-quality food, innovative menu offerings, and unique customer experience. The company is committed to providing fresh, made-to-order meals and prides itself on its signature square hamburgers, freshly prepared salads, and Frosty desserts.

Share price

WEN's share price has performed extremely well in the last decade, returning over 180% to shareholders and outperforming the market. This is a reflection of its consistent financial improvement.

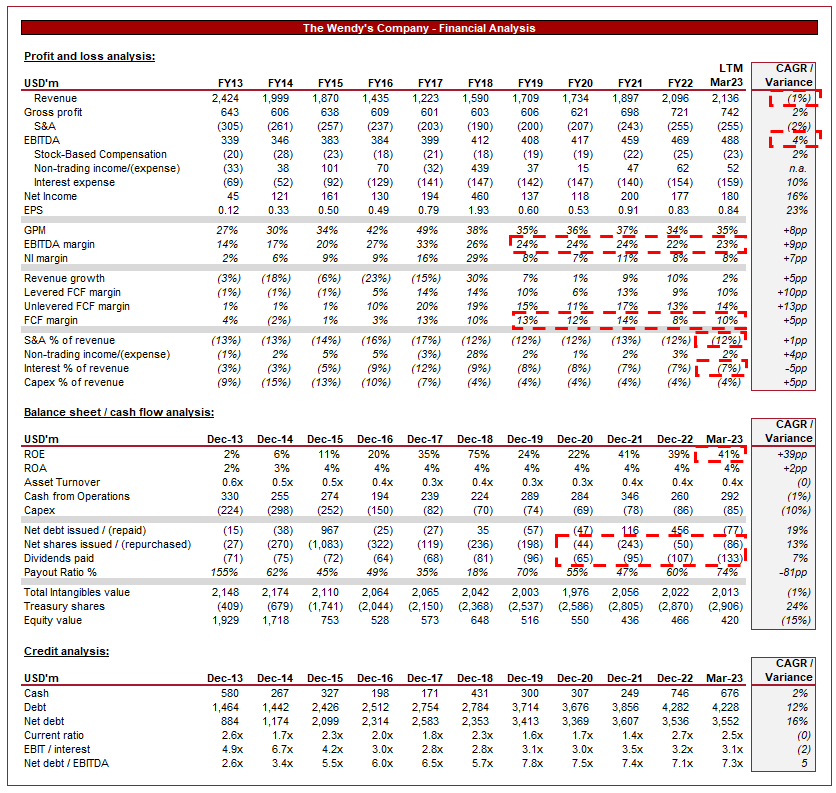

Financial analysis

Wendy's Financial Analysis (Capital IQ)

{kind=link}

Presented above is WEN's financial performance for the last decade.

Revenue & Commercial Factors

WEN's top-line revenue is not a true reflection of the company's growth trajectory, as it is muddied by a strategy of re-franchising. During this period, WEN has achieved healthy same-restaurant sales ((SRS)) growth, averaging MSDs.

Business Model

WEN operates through a combination of company-owned restaurants and franchised locations. Franchisees play a crucial role in expanding the Wendy's brand and driving growth while benefiting from the established operational systems to maximize returns. As of Jan23, WEN had 5,994 restaurants in the US (another 1,101 overseas), of which 403 are operated by the company (1,089 overseas operated by franchises). The restaurant industry as a whole has experienced a rapid transition to franchising, as it provides greater certainty over revenue and improved returns on invested capital. Finally, the business de-risks operationally, as it no longer is responsible for the operations of the restaurant. Finally, it is far easier to expand rapidly as WEN does not need to fund the new locations with its balance sheet.

WEN competes with its peers by focusing on developing unique and differentiated menu items to attract customers and meet changing consumer preferences. This includes introducing limited-time offers, and expanding the use of fresh and high-quality ingredients. The use of limited-time promotions in particular has been highly successful in recent years, as the data suggests consumers are more likely to try new products.

WEN is expanding its Breakfast offering and highly promoting this, seeking to capture the market that is dominated by a smaller number of players. The business has launched similar products to McDonald's ( MCD ), which is a slightly underwhelming approach but is potential enough. Further, the business has focused promotional activities on its late-night business, seeking to increase awareness of the option. From a financial perspective, this makes sense. It increases the returns from each restaurant, improving efficiency, while tapping into a segment it is positioned well to win in. Consumers want convenience and a good product. WEN provides a leading offering in both. This has the potential to drive healthy SRS in the coming years.

WEN has embraced technology and digital platforms to enhance customer engagement and convenience. This includes mobile ordering, delivery partnerships, loyalty programs, and digital marketing initiatives. The drive to utilize this technology has been rapid in recent years, as businesses have increasingly realized the value that can be gained through developing a closer relationship with customers. Through intelligent direct marketing (loyalty program and promotions), the propensity to dine can be increased, again supporting SRS growth. In the most recent quarter, global digital sales increased 12% while WEN continues to develop its capabilities, implying further outsized growth is ahead.

Restaurant growth is inevitably a key value driver long term, as it enhances the value proposition of the business, as well as generating accretive gains. It is far easier to grow revenue through restaurant numbers than SRS. 39 new locations were opened in Q1, with the lion's share of 2023's pipeline ahead (~45% have been opened or are under construction in Q1). Healthy openings imply the brand remains an attractive franchising option, which is critical to achieving the location growth required to drive a material improvement in revenue YoY. Management's objective is to achieve annual net unit growth of 3% in 23/24, followed by 3-4% in '25. Based on the current trajectory of the business, this looks reasonable.

The key growth opportunity of WEN in our view is capitalizing on the untapped international markets to grow its global footprint. Despite its strong US presence, the company has yet to achieve the same success overseas, especially compared to the likes of McDonald's, Subway, and Domino's. Given its strong relative position in the US, the implication is that it is able to translate this to overseas markets. As an example, WEN only has 30 locations in the UK . Domino's, which has close to 20k stores, has just over 1000 locations in the UK. The ratio is clearly disjointed with WEN.

Continuing to develop an innovative menu to cater to changing consumer preferences is critical, including plant-based alternatives, healthier options, and regional-specific offerings. The importance of this is driven by the increasing consumer focus on healthier eating habits, leading to demand for more nutritious menu options and reduced spending on traditional QSRs. Many of the traditional players have taken a lazy approach to this, knowing their primary target market is not overly influenced currently. This provides significant scope to get ahead, especially because we do not see this trend going away and so will become increasingly important over time.

Competitive Positioning

Wendy's operates in a competitive fast food landscape, with competition driven by product, access to customers, dining experience, and price. WEN's primary competitors are McDonald's, Burger King ( QSR ), KFC ( YUM ), Subway, Taco Bell, Domino's ( DPZ ), Wingstop ( WING ), and Chipotle ( CMG ).

Wendy's competitive advantages revolve around the following factors:

- Brand Recognition. The Wendy's brand is well-established and recognized globally, providing a strong competitive advantage and customer loyalty.

- Quality and Taste. Individuals make choices on where to eat based on the quality of the products primarily. Using the most objective data point possible, Wendy's impressive growth trajectory thus far reflects what must be a great suite of products.

- Customer Reach. In addition to a good product, consumers want convenience. That is why there is a Q in QSR. With WEN's substantial US footprint, and internationally too to a lesser extent, it is able to effectively market to consumers and benefit from increased traffic.

With these factors in mind, it is difficult to materially gain or lose market share. This is due to the maturity of the industry and relative stickiness of comparative differences, the industry is saturated. The McDonald's menu is fundamentally as it has been for an extended period of time, as is Wendy's. People like what people like. This acts to defend WEN's position but also reduces the potential for material upside.

Economic & External Consideration

The current economic conditions, characterized by high inflation and elevated interest rates, have the potential to negatively impact WEN in the near term.

Firstly, increased costs. High inflation is contributing to increased costs of ingredients, labor, and other inputs, pressuring WEN's profitability. The response has been to increase menu prices but given how competitive the industry is, this is not necessarily a margin-neutral exercise.

Secondly, a reduction in consumer spending. Elevated interest rates in conjunction with inflation are contributing to a rapid deterioration in consumers' finances, impacting discretionary spending. This is compounded by the recent Supreme Court ruling on Student Loans, with Wells Fargo estimating a student loan repayment headwind of up to $6B per month, impacting discretionary consumer spending by 1% to 2%.

WEN is due to announce its earnings in the coming days. Based on our analysis, we expect a softer performance relative to prior months. Given this quarter straddles summer, which generally means an improvement in growth due to more social activities, we see an inevitable improvement on Q1. This said, the growth rate YoY we believe will be lower. Q4-22 was 13.4% YoY, Q1-23 was 8.2%, and so we believe WEN will land between 5-6%.

Margins

WEN's margins have gradually improved over the last decade, reaching an EBITDA-M of 23% and a NIM of 8%. This improvement has been driven by the push toward franchising, as well as the benefits of scale.

The recent decline is a reflection of inflationary pressures, with pricing unable to offset this. In the most recent quarter, OPM has improved compared to both Q4-22 and Q1-22, implying pressures are subsiding somewhat. The US has been above average in combating inflation, likely the reason for the improvement.

Balance sheet & Cash Flows

Wendy's is heavily indebted, with a ND/EBITDA ratio of 7.3x. Interest payments represent 7% of revenue and the company's coverage is 3x. Although this is not concerning from a solvency perspective due to the consistency of its cash flows, the business is not in a position to materially raise more.

Debt has been utilized to fund distributions, as although profitability is high, cash flows have been mediocre on an absolute basis. We are not a fan of this strategy, unless it is carefully done to match profitability (i.e. maintaining a target ND/EBITDA that is long-term sustainable - 7.3x is not in our view due to the interest levels). This has the potential to restrict WEN's ability to reinvest and may lead to operational cuts to boost cash flows.

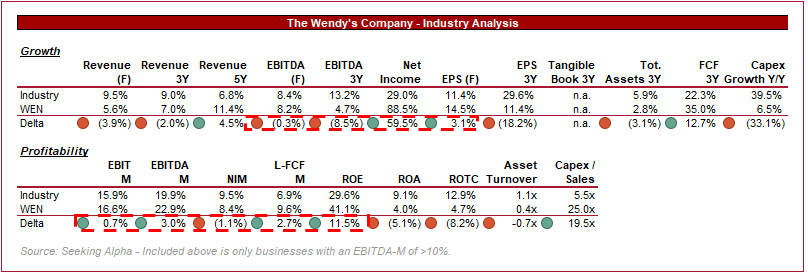

Industry analysis

{kind=link}

Presented above is a comparison of WEN's growth and profitability to the average of its industry, as defined by Seeking Alpha (21 companies).

WEN performs well when compared to the leading businesses within its industry. Growth in profitability sends slightly different signals based on the metric considered but WEN is broadly in line with the industry.

From a profitability perspective, however, WEN has a noticeable premium, even with the recent margin contraction. Further, it generates superior cash flows, supporting higher distributions.

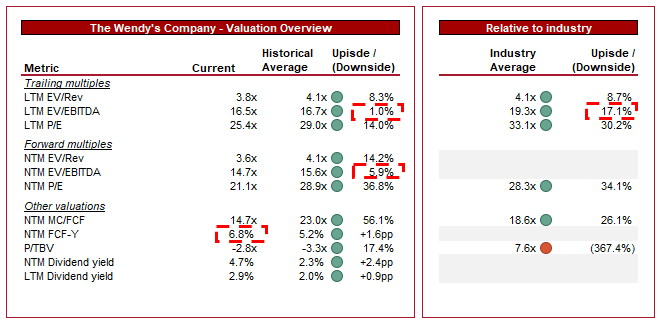

Valuation

{kind=link}

WEN is currently trading at 17x LTM EBITDA and 15x NTM EBITDA. This is a discount to its historical average.

Our view is that WEN should trade in line with its historical average, reflecting its improved profitability but offset by the rapid increase in debt. We attribute value to businesses that are set up well for a lucrative future, not burdened from a lucrative past.

Relative to its peers, multiples parity, or a small discount is likely fair. This would conservatively value its superior profitability while punishing the business for its large debt balance (Domino's has a ND/EBITDA ratio of 5.5x, McDonald's is at 3.3x, and Yum! is at 5x.

Based on this, there is potentially small upside with WEN but when considering the risks around a slowdown in demand, or the market reaction to a future reduction in distributions, we do not see an attractive risk-adjusted return.

Final thoughts

Wendy's serves a fantastic suite of meals and is comparable in experience to its larger peers, such as McDonald's. With the exploitation of commercial trends, such as international expansion, menu innovation, intelligent marketing, and technological development, we believe WEN is positioned well to drive healthy SRS. The issue is that the WEN business looks hamstrung. With high debt impacting distributions and the ability to invest in growth, as well as the potential for near-term growth slowing, we believe WEN could underperform.

For further details see:

Wendy's: Analyzing Its Position In A Competitive Industry