WERN - Werner: Risky But M&A And Automated Tracking Could Imply Undervaluation

2023-04-16 03:00:32 ET

Summary

- Werner is a provider of transportation and logistics services within the United States. The company presents itself as one of the largest truck carriers in the country.

- I assumed that assessment of real-time global positioning data and automated possible late load tracking could lead to better customer service and perhaps more efficiency.

- I also believe that the company will be able to find new targets at completing prices. I am not expecting anything that Werner has not done in the past.

Werner Enterprises, Inc. ( WERN ) is delivering meaningful acquisitions like that of Reed Transport Services, Inc., RTS-TMS, Inc., or FAB9, Inc. In addition, WERN continues to look for targets in a highly fragmented market. Assuming successful new acquisitions, addition of new customers, and successful use of big data technologies to assess truck positioning, I believe that the stock is significantly undervalued. There are serious risks from failed acquisitions or concentration of clients, but I believe that the stock could trade at higher marks.

Werner

Werner is a provider of transportation and logistics services within the United States. The company presents itself as one of the largest truck carriers in the country.

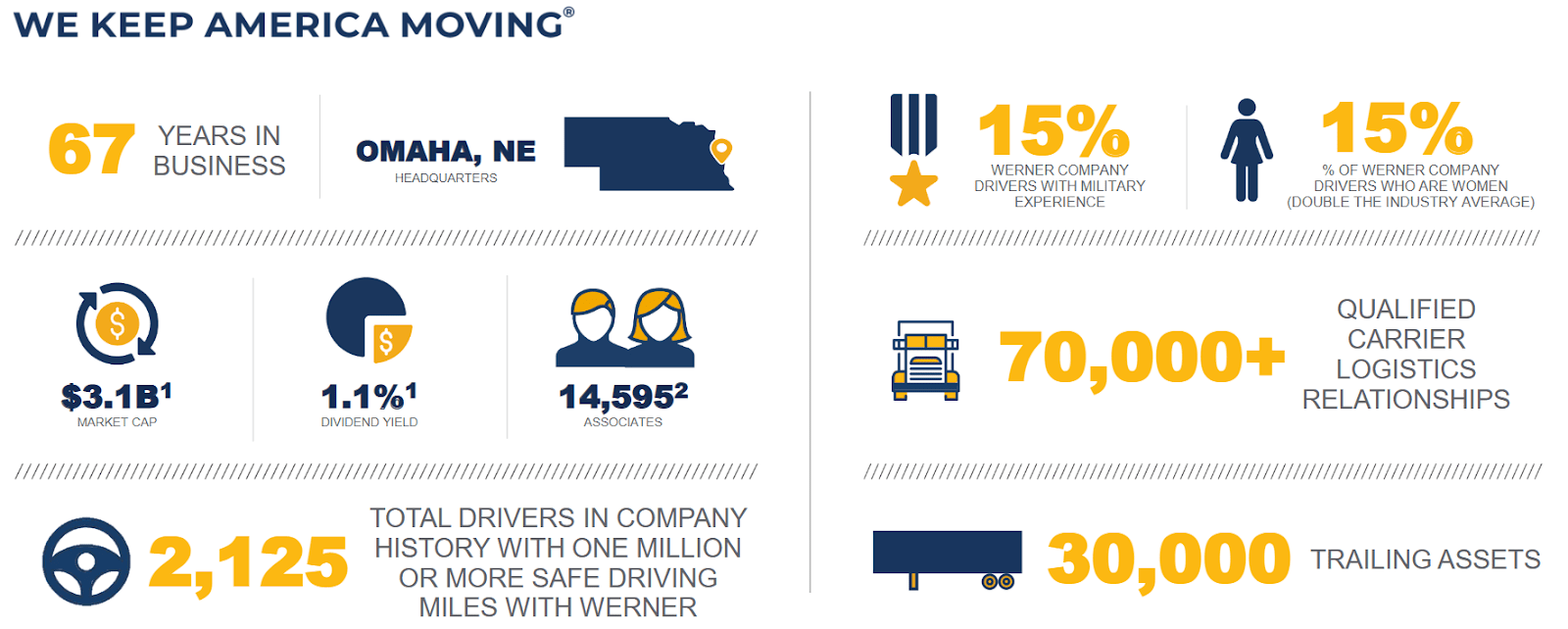

Currently, the company's fleet of trucks is estimated at 8,600, of which 8,305 are operated by the company, while the remaining trucks are in the hands of independent dealers or smaller companies. In the logistics area, according to data provided at the end of 2022, Werner has 39 haulage trucks and 101 distribution trucks. According to a recent presentation, the company also reported close to 30k trailing assets and 70k qualified carrier logistics relationships. In sum, I believe that the activity is well diversified.

{kind=link}

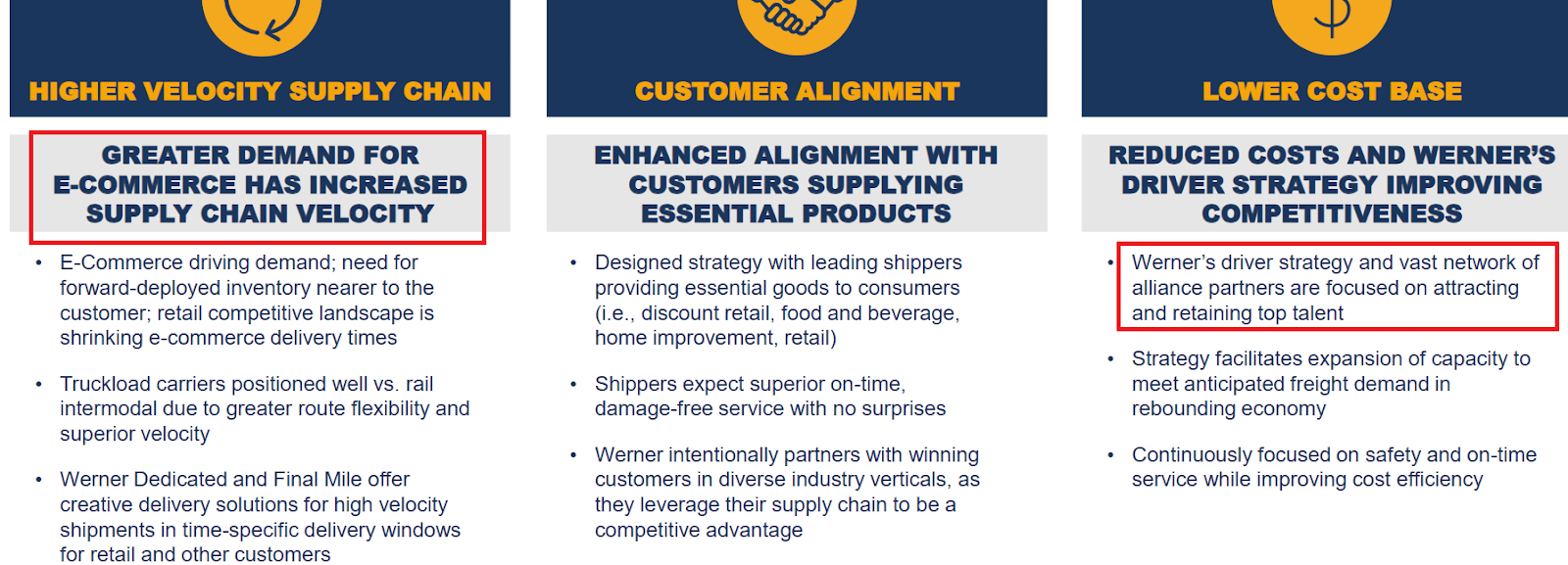

There are several reasons to have a careful look at the company, but the most relevant, in my view, is the beneficial impact that demand for e-commerce is having on the cash flow statement. Truckload carriers offer greater route flexibility and superior velocity than other transportation options. On the top of it, Werner did react well to the demand from clients by creating a large network of alliance partners and expanding capacity. Among all the slides I saw from management, the following appears quite relevant.

{kind=link}

It is also worth noting that management is accelerating property growth and the drivers count by acquiring a significant number of targets. In 2022, the company acquired Reed Transport Services, Inc., RTS-TMS, Inc., and FAB9, Inc. In my view, the current balance sheet would most likely allow Werner to acquire more competitors.

On November 5, 2022, we acquired 100% of the equity interests in Reed Transport Services, Inc. and RTS-TMS, Inc., doing business as ReedTMS Logistics (“ReedTMS”). ReedTMS, based in Tampa, Florida, is an asset-light logistics provider and dedicated truckload carrier that offers a comprehensive suite of freight brokerage and truckload solutions to a diverse customer base. Source: Annual Report

On October 1, 2022, we acquired 100% of the equity interests in FAB9, Inc., doing business as Baylor Trucking, Inc. (“Baylor”). Baylor, based in Milan, Indiana, operates 200 trucks and 980 trailers in the east central and south central United States. Prior to the acquisition, Baylor achieved revenues of $81.5 million for the 12-month period ended August 31, 2022. Revenues generated by Baylor are reported in One-Way Truckload within our TTS segment. Source: Annual Report

Source: Annual Report

As a result of previous efforts to lower the costs, partnerships, economies of scale, and acquisitions, Werner successfully reported an impressive increase in adjusted operating margins from 2016 to 2022. Most importantly, Werner expects to deliver 2023 adjusted operating margin close to 12%-17%, which is larger than what we saw in the last ten years.

Source: Investor Presentation

Business Segments

The company's operations are organized into two business segments: TTS and Werner Logistics. These business segments respond to transport and logistics services respectively. The first segment, in turn, is divided into dedicated transport and one-way transport. The difference between these two service models is that the first offers the transport of specific loads for a client, from one direction to another, complying with agreed deadlines and routes. The other transport model offers the possibility of carrying a load on the routine routes of the companies, without the transport service to the door of commerce or the distribution center. These routes include the company's authorization to operate within Canada and to transit through Mexican territory.

The logistics service, for its part, also offers different types of services, which include truck loads, and intermodal. The first of these is intended for companies that frequently move and transport their assets or products, with Werner being the company that diagrams these distribution lines and schedules. The intermodal, in addition to truck loads, includes a section by train, other speeds, and shorter routes for transport, while the final mile is available for residents and businesses that need to transport a heavy load of difficult management.

Balance Sheet

The last balance sheet reported by Werner Enterprises included a meaningful increase in the total amount of assets driven by increases in property and equipment, cash, goodwill, and intangible assets. The total amount of liabilities also increased with increases in total long term debt and accounts payable. With that, the ratio of assets/liabilities stands at close to 1.5-2x, and the amount of leverage does not seem at all worrying.

More in particular, management reported cash and cash equivalents worth $107 million, accounts receivable of $518 million, inventories and supplies of $14 million, and total current assets close to $762 million. Total current assets are more than two times the total amount of liabilities, so I would not say that there is a liquidity problem here.

Property and equipment included buildings and improvements of $309 million, revenue equipment close to $2.169 billion, and service equipment of $306 million. In sum, total property and equipment stood at $1.825 billion, which is significantly larger than the total amount of long term debt. Finally, with goodwill worth $132 million and intangible assets of $81 million, total assets stood at $3.097 billion.

Source: Annual Report

The list of liabilities includes accounts payable worth $124 million, current portion of long-term debt of $6 million, insurance and claims accruals close to $78 million, and total current liabilities of $309 million. Besides, with long-term debt of $687 million, other long-term liabilities close to $59 million, and deferred income taxes of $313 million, total liabilities were equal to $1614 million.

Source: Annual Report

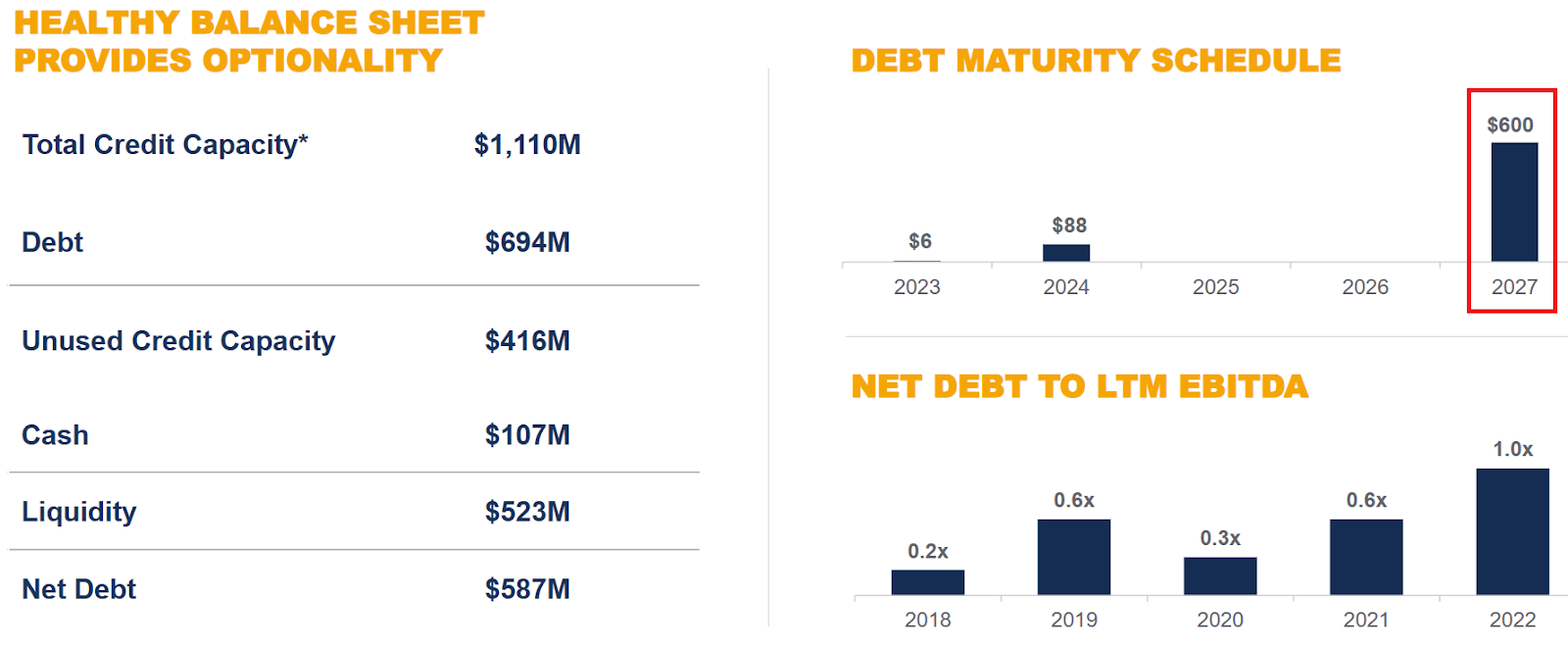

For investors who may be concerned about the total amount of debt, I believe that having more information about the debt obligations makes sense. The company will have to make a payment of $600 million in 2027. I believe that management will likely be able to renegotiate the debt terms, or find alternative debt sources in the next four years.

{kind=link}

My Assumptions Include Successful Acquisitions, New Customers, Big Data Assessment Of Global Positioning Data, And Automated Load Tracking

Under normal conditions, I assume that the company will successfully manage to expand its contact with customers. I also believe that management will likely offer new services to customers who are interested in distance coverage, diversification of transport and logistics services, and technological developments. More clients will likely lead to economies of scale, which may push the operating margin down, and may enhance the stock valuation.

In my financial model, I also assumed that future acquisitions will successfully close, which means that Werner will obtain the synergies expected by management. I also believe that the company will be able to find new targets at completing prices. I am not expecting anything that Werner has not done in the past. Besides, in the last annual report, management noted that it is clearly looking for acquisitions.

Our business acquisitions expanded our fleet size, customer base, geographic market presence, and network of operational facilities. We remain open to considering acquisitions in North America truckload and logistics companies that are both additive to our business and accretive to our earnings. Source: Annual Report

In my view, if market participants find that Werner Enterprises is delivering successful M&A operations, the demand for the stock will likely grow. As a result, I believe that the stock price could increase.

Finally, I assumed that assessment of real-time global positioning data and automated possible late load tracking could lead to better customer service and perhaps more efficiency. I invite investors to read carefully about the tech developments already implemented by Werner. In my opinion, the use of big data technologies in combination with new software could bring operating efficiency and further operating margin improvements.

(1) an electronic logging system which records and monitors drivers’ hours of service and integrates with our information systems to pre-plan driver shipment assignments based on real-time available driving hours; (2) software that pre-plans shipments drivers can trade enroute to meet driver home-time needs without compromising on-time delivery schedules; and (3) automated “possible late load” tracking that informs the operations department of trucks possibly operating behind schedule, allowing us to take preventive measures to avoid late deliveries. Source: Annual Report

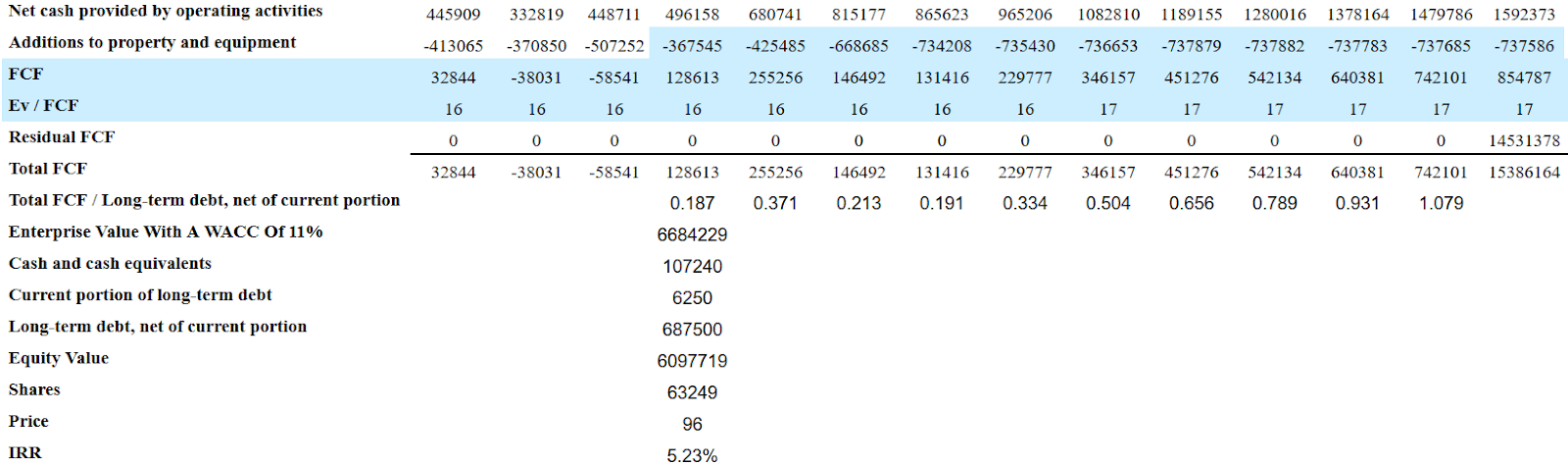

My Financial Model Implied Significant Upside Potential Driven By FCF Growth

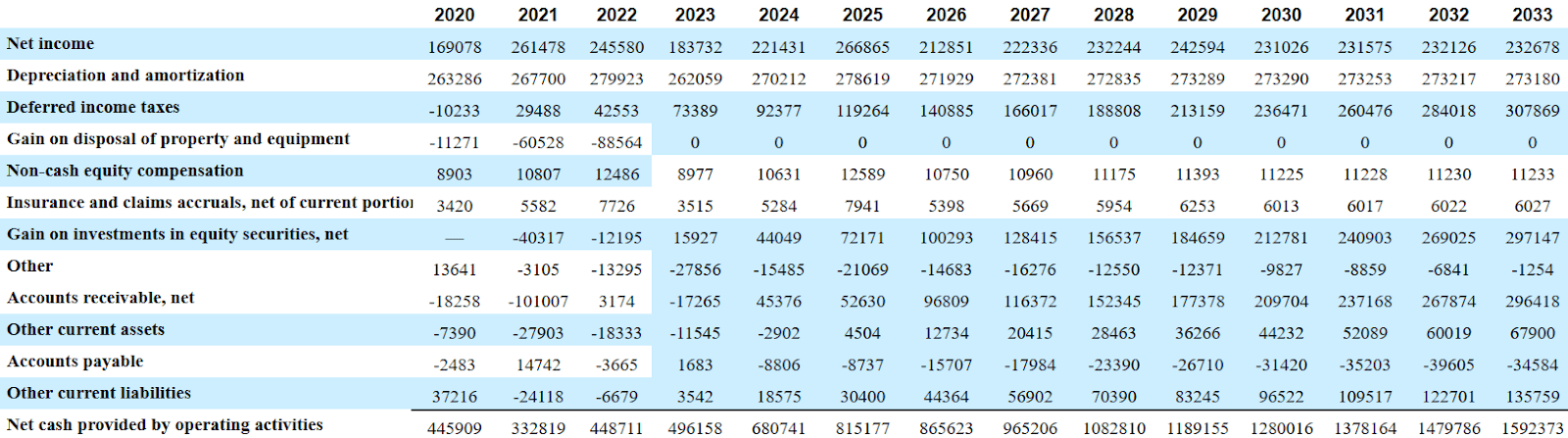

My cash flow statement forecasts include net income growth, depreciation and amortization growth at a slower pace than capex growth, and non-cash equity compensation growth. I also included some gain on investments in equity securities in line with the gains seen in previous years and positive changes in accounts receivable. I believe that my numbers are conservative.

The results include 2033 net income of $232 million, 2033 depreciation and amortization of $273 million, 2033 deferred income taxes of $307 million, and non-cash equity compensation of $11 million. Also, with 2033 insurance and claims accruals of $6 million, changes due to accounts receivable of $296 million, and changes in accounts payable of -$35 million, the net cash provided by operating activities would stand at $1.592 billion. Finally, with additions to property and equipment of $738 million, 2033 FCF would be close to $854 million.

{kind=link}

If we assume an EV/FCF multiple of 17x, the residual FCF would be close to $14.531 billion, and the enterprise value would be close to $6.684 billion. If we add cash and cash equivalents of $107 million, and subtract the current portion of long-term debt close to $6 million and long-term debt of $687 million, the implied equity value would stand at $6.097 billion, and the implied price would be $96 per share. Besides, I obtained an IRR close to $5.22%.

{kind=link}

Highly Fragmented Market

Competition in this market is highly fragmented and changing depending on the region analyzed. Werner generally has portions of the markets in which it operates, due to the company's long history and recognition.

Competitors range from companies that offer similar services nationwide to small carriers and independent agents or small businesses. In the transportation segment, competitors are other large transportation companies. In logistics, it is also necessary to take into account private carriers, railway companies, other vendors of intermodal services, and the distribution lines of some companies.

Risks

Werner is exposed to fluctuations in the general economy, the transportation activity of its customers, and increases or fluctuations in fuel prices. To this we must add the usual seasonality in this market, which together with the above factors can mean risks of unpredictability in the company's projections.

On the other hand, the company's main client, Dollar General (DG), represented 14% of the profits during 2022. The lack of diversification in its clients is a risk factor, since the 5 main clients concentrate almost 40% of the company’s revenue, while the top 50 clients account for almost 80% of the company’s revenue.

In a sense of competition, although the company is well positioned and has significant portions of the transportation market at the national level, there are risks associated with growth. In my view, if business growth or operating margin growth is lower than expected, some investors may dump their shares, which could bring the stock price down. Failed acquisitions could also disappoint investors, and goodwill impairment could have detrimental impact on the book value per share.

My Takeaway

Werner Enterprises recently signed meaningful acquisitions of Reed Transport Services, Inc., RTS-TMS, Inc., and FAB9, Inc., and announced that acquisitions will likely continue in the near future. Assuming successful closure of existing transactions, new beneficial M&A operations, addition of new customers, and big data assessment of truck positioning, Werner appears undervalued. Even considering risks from M&A integrations, lower growth than expected, and concentration of clients, I believe that Werner is a must-follow stock.

For further details see:

Werner: Risky, But M&A And Automated Tracking Could Imply Undervaluation