WCC - WESCO: Executing Well But Upside In The Short-Term Could Be Capped

2023-12-26 09:12:14 ET

Summary

- WESCO International stock has delivered solid returns of 42% in 2023, twice as much as its peers in the industrial space.

- We take a look at some of the factors behind the interest in the stock.

- We examine if WCC would represent a good investment at current levels.

Introduction

{kind=link}

The stock of WESCO International ( WCC ), an entity specializing in B2B distribution, logistic services, and supply chain solutions has enjoyed a resolute 2023, delivering 42% returns, thus outperforming the broader markets, and doing twice as well as its peers from the industrial space.

What's driving the interest in the stock, and can the momentum be sustained? Read on to find out.

Executing Well

WESCO reports under three different units - Electrical & Electronic Solutions ((EES)), Communications & Security Solutions ((CSS)), and Broadband Solutions ((UBS)), and it is fair to say that all these sub-segments are well-positioned to benefit from secular tailwinds such as automation/IoT, the electrification wave, infrastructure grid modernization, consolidation and reshoring of the supply chain, etc.

{kind=link}

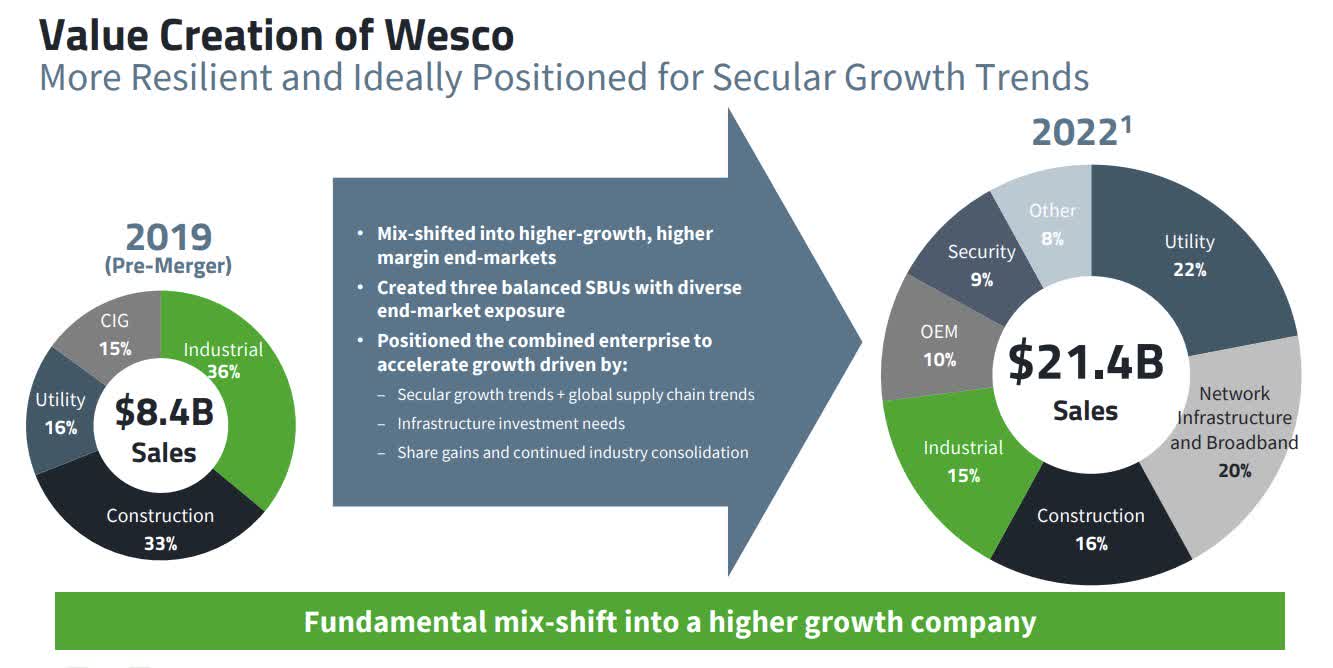

This wasn't quite the case, during the pre-pandemic era, when it could be argued if WESCO's topline was diversified enough or competitive enough to flourish in the new world. Now after getting into a merger with Anixter in 2020, we are witnessing a more well-rounded business profile, with exposure to high-growth and high-margin terrains such as communication, security, wire, etc.

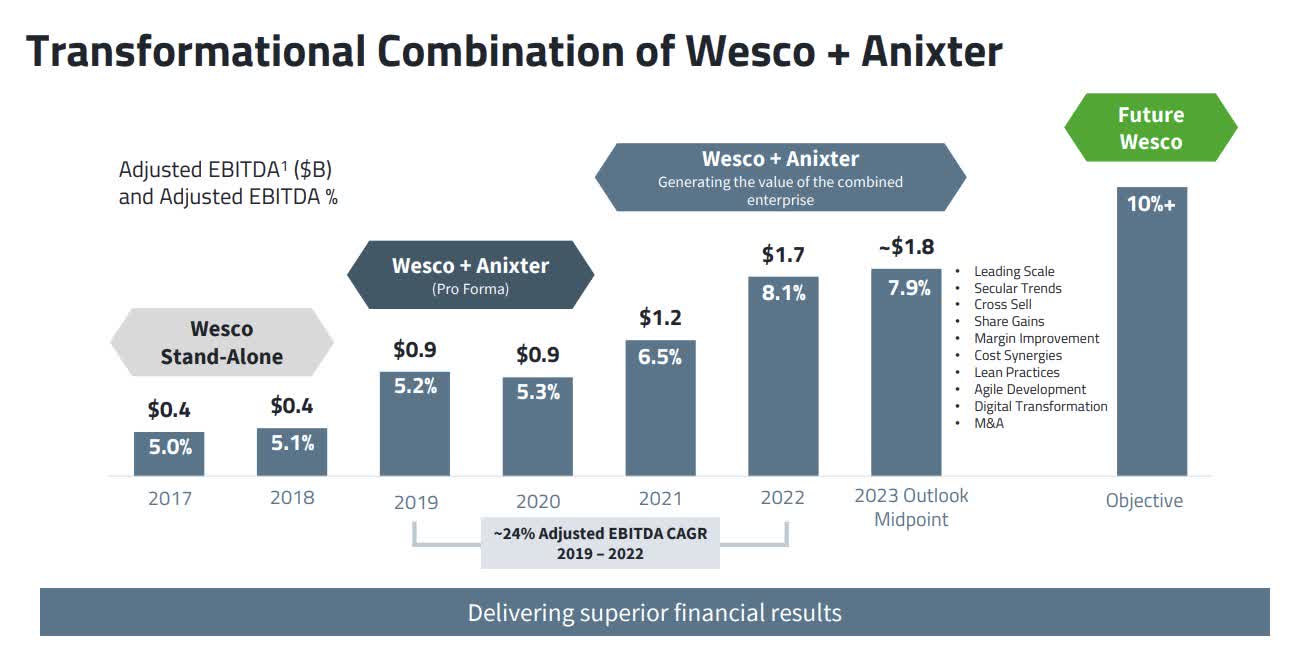

There have also been a lot more opportunities to cross-sell between various units, and after witnessing around $270m of cross-sell synergies in Q3, management recently dialed up their cumulative cross-sell target from $2bn (August 2023 target) to $2.2bn. Besides the topline synergies, WCC also believes they could generate cost savings of $0.315bn for the year (close to 40% of this is in supply chain-related areas), a 17% improvement from last year.

Then, it's also encouraging to note that the division with the best EBITDA margin profile (UBS, with EBITDA margins of close to 11%) is currently witnessing the best growth. Against a flattish performance for EES, and 4% growth for CSS, UBS's Q3 topline grew by 6%.

A combination of all these factors is thus translating to a much better margin profile for WCC over time.

{kind=link}

As opposed to the 5% thresholds seen during the pre-pandemic phase, the group's EBITDA margins are now closer to the 8% mark, with the desire to get it to double-digit levels over time. So could the improvement persist? Well, sell-side estimates point to around 14bps of EBITDA margin improvements through FY25.

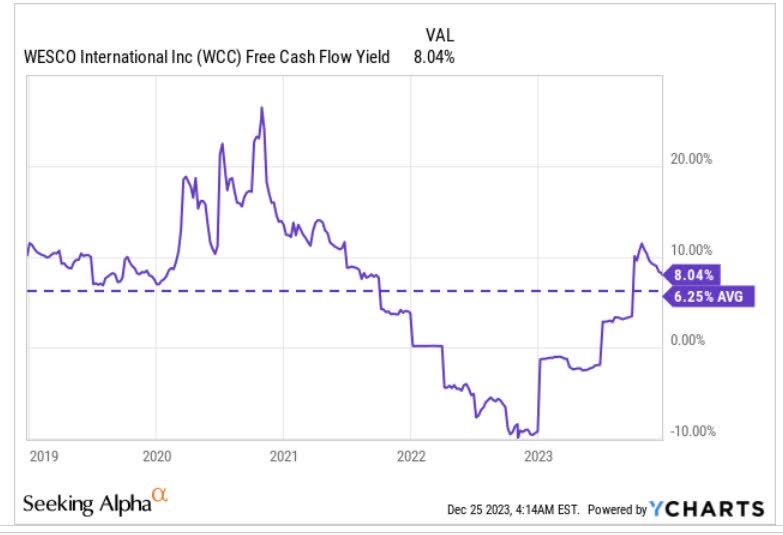

Then, one of the other standout themes associated with WESCO in recent periods is the marked step-up in its cash generation (+357m of FCF in Q3), after some difficult periods from Q4-21 through Q1-23 (across these six quarters, WCC managed to generate positive operating cash flow only in Q4 last year).

Over the last couple of quarters, inventory drawdowns have been a positive source of cash flow, whilst recently in Q3, we also saw the company extract positive numbers from better receivables management. All this has meant that the stock's FCF yield is now once again trending well over its 5-year average of 6.25%.

{kind=link}

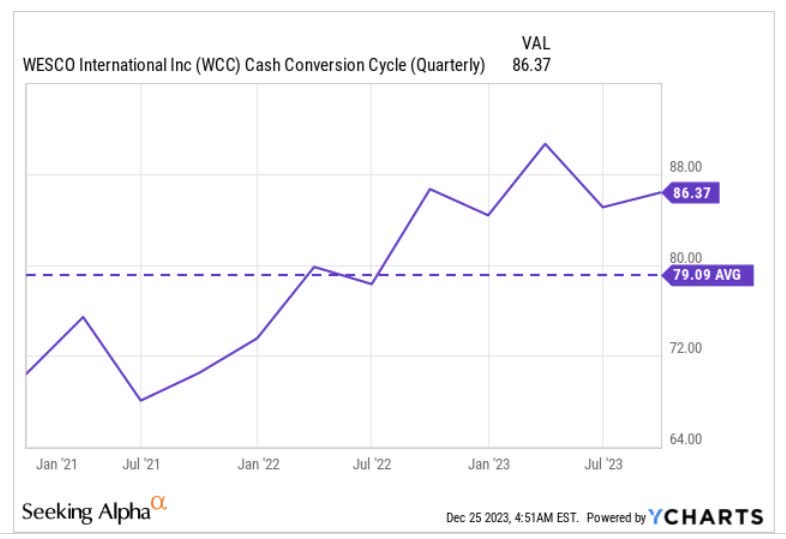

It wouldn't be unreasonable to expect even further improvement here, as WCC's cash conversion cycle (the number of days cash is tied up with working capital investments) is still around a week more than its long-term average, offering further scope for improvement.

{kind=link}

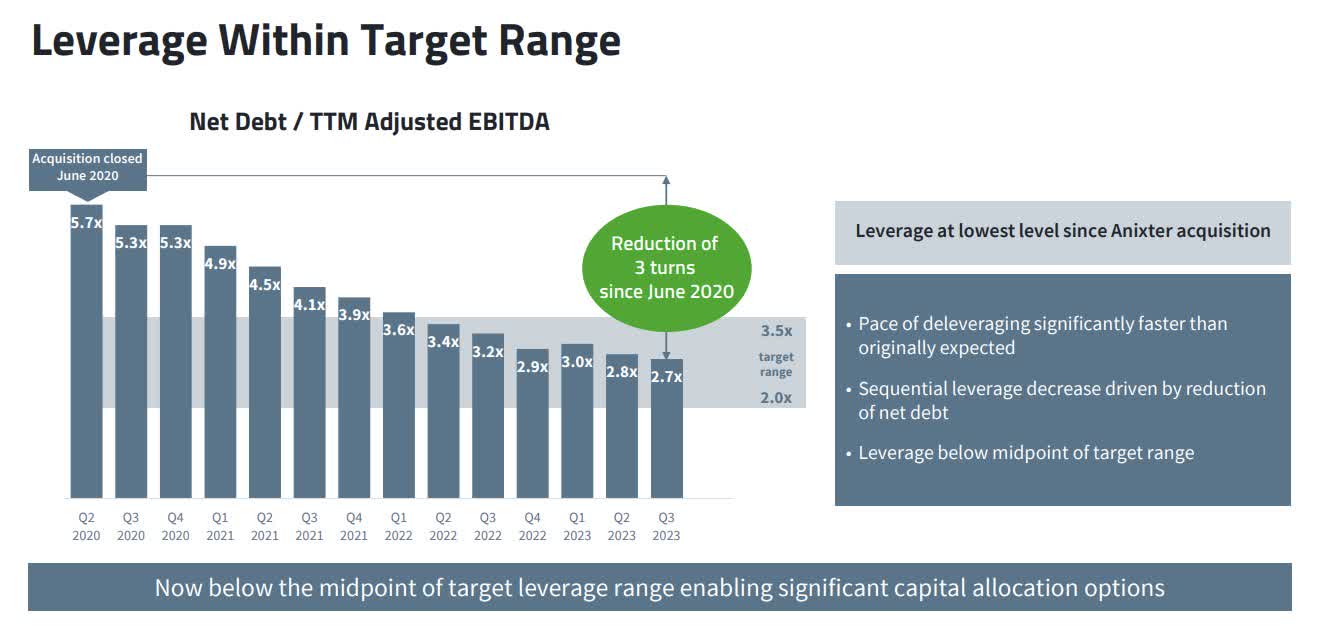

Nonetheless, if WCC can keep up its FCF generation, it will open up all sorts of doors with capital allocation. Firstly, the inordinate level of debt that the company had taken to fund the Anixter acquisition can be paid down (as of 9M-23, a good 48% of WCC's debt represented flexible rate debt). In Q3, they were able to pay down around $250 mn of debt, sending the leverage down to more acceptable levels of 2.7x (net debt/adjusted EBITDA). For context, during the start of the pandemic, this stood at a whopping level of 5.7x.

{kind=link}

We also have a situation where WCC's cash on its books is now at record highs of $630mn , so this inevitably leads to better prospects of shareholder distributions. Earlier this year, we saw the company kick-start its common equity distribution program with a quarterly figure of $0.375 , and crucially, we've also seen a recommencement of buyback activities with the company deploying $50m to this effect in Q3 alone. Management suggested that they would persist with buying back stock in Q4 as well.

Closing Thoughts - Is WESCO Stock A Buy, Sell, Or A Hold?

Whilst WESCO's management deserves a pat on the back for their execution in recent periods, prospective investors who are considering a long position in the stock at this juncture may want to curb their enthusiasm.

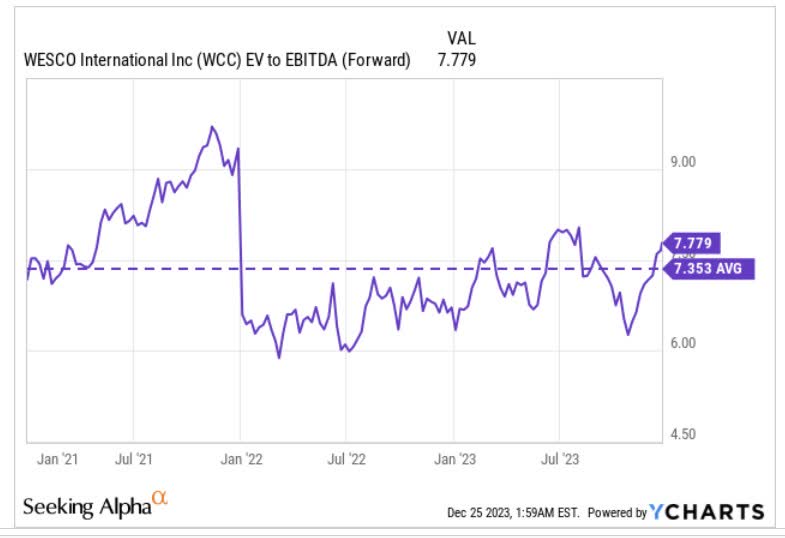

Firstly, quite unlike the situation a couple of months ago, the stock no longer looks cheap. Back in October, the stock could be picked up at -13% discount to its 5-year forward EV/EBITDA average multiple, but as things stand, we are now in a period where the stock is trading at a +7% premium over the long-term average.

{kind=link}

The premium valuation is not too ideal when you note that WCC's record-high backlog continues to slip (down -6% YoY and -7% QoQ) and will likely normalize as supply chain lead times ease. Management has also suggested that end-market demand trends will likely ease off in the current quarter.

Then, if we switch over to the charts, it's fair to say that WESCO doesn't quite come across as the most dazzling bet for those looking for mean-reversion opportunities in the broad industrials sector. Note that WCC's relative strength ratio ((RS)) versus the Vanguard Industrials ETF is now almost in line with the mid-point of its long-term range (you ideally want to consider long positions when the RS ratio is perched somewhere towards the bottom end of the chart, with a substantial gap from the mid-point of its long-term range).

{kind=link}

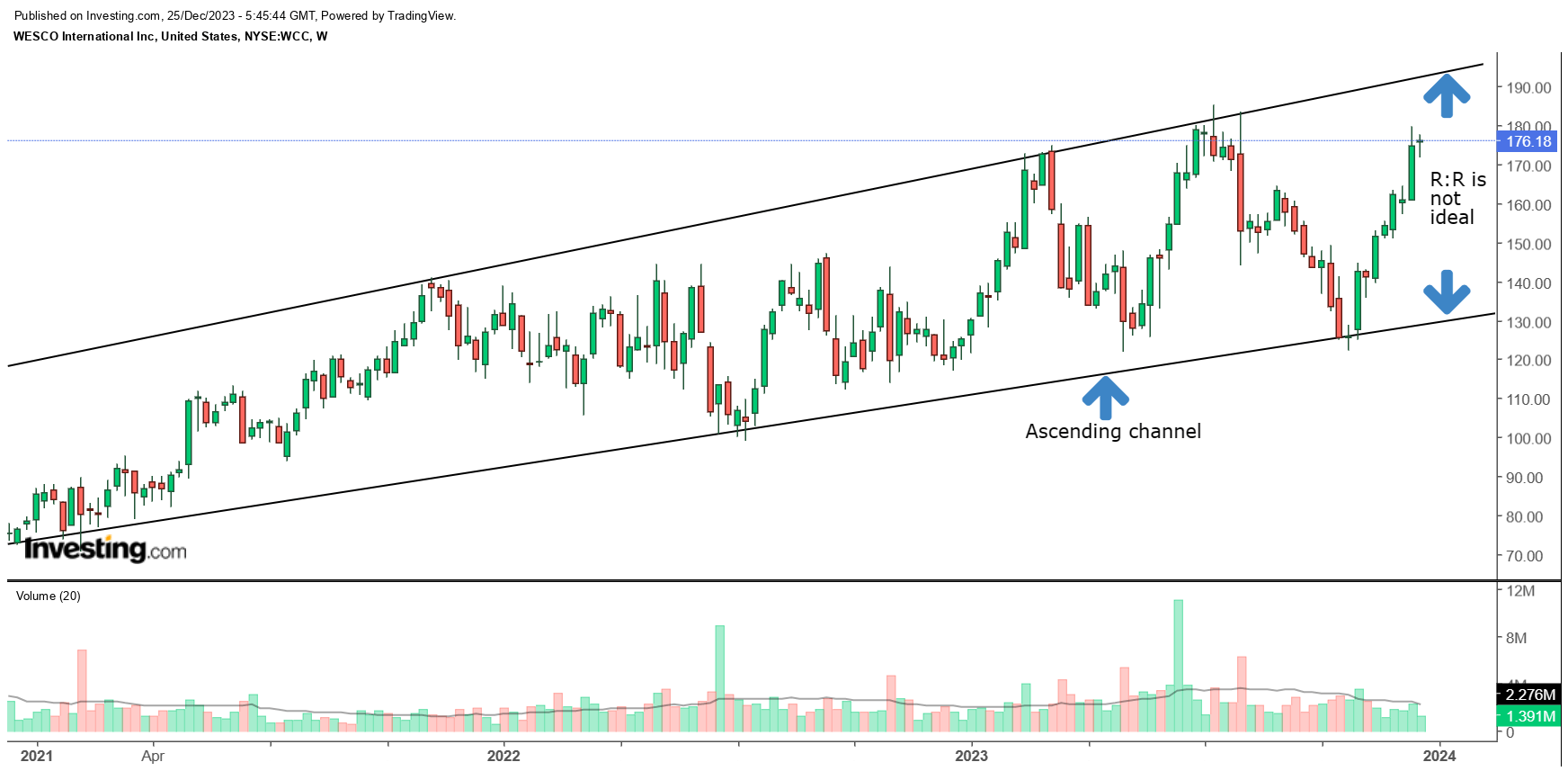

Then, if we look at another chart which showcases the 3-year price imprints of WESCO on a weekly basis, we can see that it has largely followed that of an ascending broadening wedge pattern , with the range expanding in recent periods.

What we can also see is that since the end of October, the stock has been trending up in a fairly strong manner (7 out of the 8 preceding candles have been green-bodied candles, implying a higher close than the open for every week); now, if one were to contemplate a long position at current price levels using the two boundaries as pivot zones, the reward to risk looks rather unappealing at only 0.35x (you ideally want to pursue long positions when the R:R is over 1x).

{kind=link}

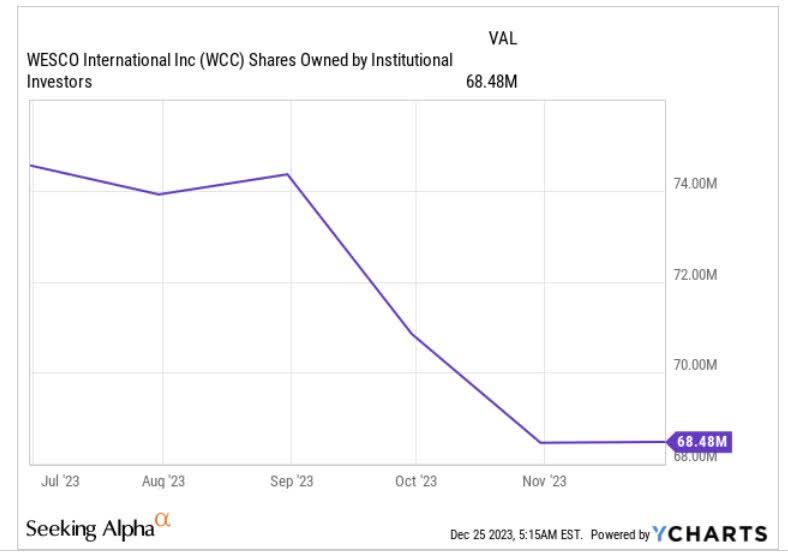

Separately, it is also worth highlighting that the influential institutional segment, hasn't really participated in this uptrend; in fact, on a net shares owned basis, their stake in WCC is actually down by -8% over the last six months.

{kind=link}

The implied takeaway is that the move in recent months has been largely retail-driven, and when the stock is on the cusp of hitting a potential pivot zone, you want to be doubly careful about loading up. WCC is a hold .

For further details see:

WESCO: Executing Well, But Upside In The Short-Term Could Be Capped