WCC - WESCO International Holds It Steady Despite The Cracks (Rating Downgrade)

2023-08-08 23:14:00 ET

Summary

- WESCO International is benefiting from long-term secular growth in utility, data center, security, and industrial sectors.

- Supply chain issues are improving, but challenges in the electrical product line will continue in Q3.

- WCC's cash flows have increased, and it plans to use them for stock buybacks, making it a reasonable investment with moderate returns.

WCC’s Drivers And Obstacles

I previously discussed WESCO International ( WCC ); you can read the latest article here . Some of the company’s end markets are in a secular growth that would drive it long-term. Also, the key economic indicators have been relatively steady, despite the US GDP slowdown. The supplier lead times have started shrinking, indicating supply chain rebalancing. This, plus its cost-reduction measures, can improve the company’s operating profit margin in the medium term. Its backlog also increased in Q2.

But, in recent times, wire and cable sales decreased while manufacturing structures in the OEM operating group weakened. The supply chain issues in the electrical product line will continue to pose challenges in Q3. In 1H 2023, its cash flows increased significantly, which it will use for stock buybacks to increase shareholder values. The stock is reasonably valued versus its peers. Investors might want to “hold” it with an expectation of moderate returns.

Long-Term Trend And Economic Indicators

WCC is set to benefit from the long-term secular growth in the utility, data center, security, and industrial sectors. The supply chain deficiencies that affected the company’s performance in the past two years are correcting fast, as reflected in lower supplier lead times. The company is adopting transformational steps to improve its digital capabilities to increase market share. It has also set a target of $25 million annualized cost curtailment. It initiated the plans in June and will likely benefit in 2H 2023.

{kind=link}

The economic indicators have been somewhat confounding. Although the persistent interest rate hike points to continued risks, the other key economic indicators (inflation and unemployment) point to relative stability. However, the US GDP growth rate has squeezed over the past three quarters. The fears of the US economic recession appear to be receding, and the economy will likely settle for a soft landing.

Key Challenges

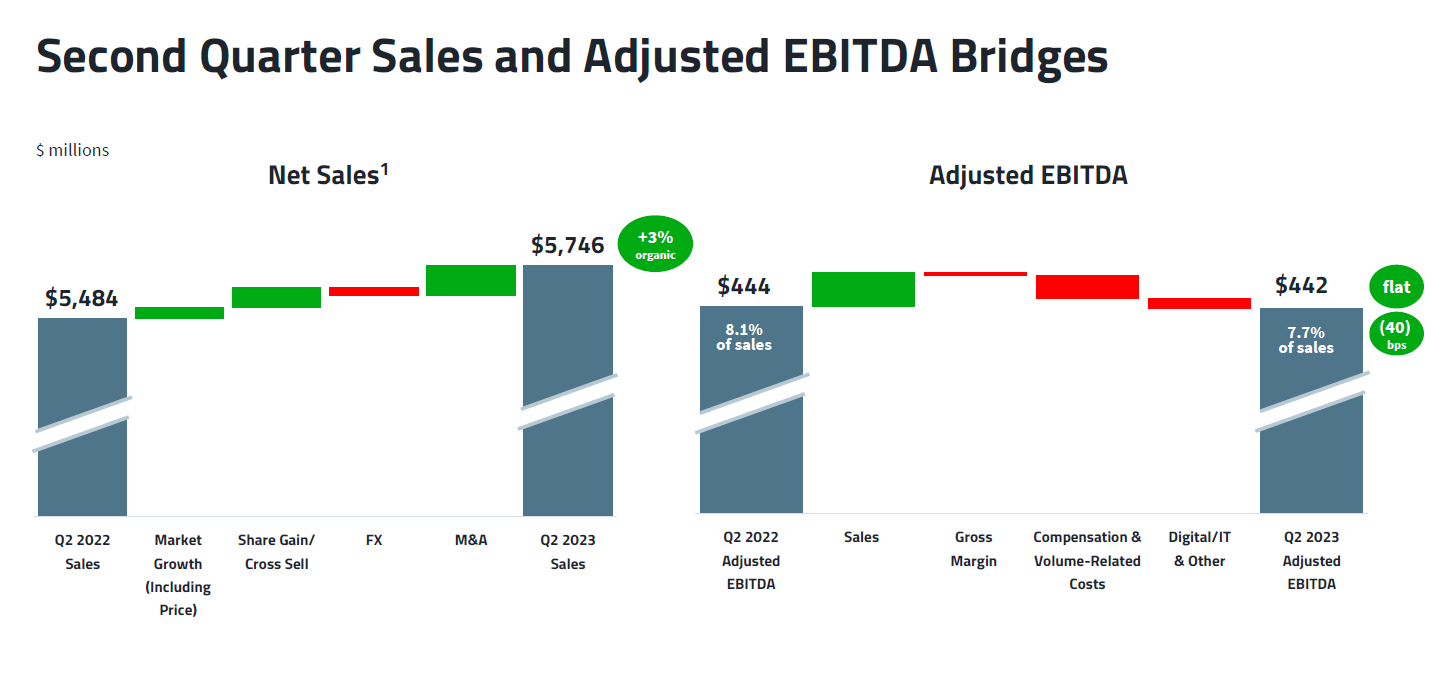

One fundamental weakness was the organic sales drop in the Electrical & Electronic Solutions (or EES) segment in Q2. Year-over-year, sales declined by 3% (excluding intersegment business transfers). This was primarily due to supply chain rebalancing and product lead time normalization. The supply chain factor led to lower stock and flow sales. Wire and cable sales to the contractor customers also decreased. At the same time, manufacturing structures in the OEM operating group weakened. The weakness flowed into commercial construction and manufactured structures.

But the supply chain deficiency appears to be healing. As the situation improves globally, we see a temporary decline in WCC’s stock and flow activity levels in some product lines. The underlying end market growth has also remained stable.

Segment-Wise Outlook

In July, sales in the EES segment continued to weaken following lower construction and OEM activities. The impact of seasonality will affect its Communications & Security Solutions (or CSS) and Utility & Broadband Solutions (or UBS) segment sales positively in Q3. Based on the factors at play and lower expectations for market volume growth, it has recently revised the 2H 2023 organic sales growth from 5%-8% to 4%-6%. Pricing will play a positive role, leading to 3%-4% market growth.

In Q3, year-over-year sales in the EES segment are expected to remain unchanged. As I already discussed, the supply chain rebalancing issue in the electrical industry and weakness in the stock and flow portion of the manufactured structure and commercial construction would put pressure on this segment in the near term. In the UBS segment, its revenues can increase by “high single to low double-digits.” In CSS, year-over-year sales can increase by “mid-teens.”

Margin Outlook

{kind=link}

In Q3, WCC’s adjusted EBITDA margin can expand to 7.8%-8% region versus an adjusted EBITDA margin of 7.5% in Q2. However, year-over-year would represent a decline of 30 basis points due to the top line and SG&A margin headwinds. In June, it initiated cost-reduction measures, yielding an annualized benefit of $25 million.

In 2H 2023, the company’s gross margin should remain stable as it partially overcomes the issue of supplier volume rebate. Investors may also note that its backlog was 6% higher year-over-year in Q2, supporting its relatively resilient outlook in 2H 2023 into 2024 and beyond.

Q2 Results And Drivers

{kind=link}

Owing to a low single-digit sales push from the pricing factor, WCC’s organic revenues were up by 3% in Q2 2023. Volume, however, was flat due to the weakness in the market, mitigated by robust cross-sell opportunities. Year-over-year, the adjusted gross margin was stable (21.6%).

The company prioritizes sales growth while it protects gross margin and pursues an enterprise-wide margin improvement program. The adjusted EBITDA margin was also steady relative to the previous year. Although SG&A costs increased, the company balanced them with cost-reduction actions.

Debt And Cash Flows

WCC’s debt-to-equity (1.15x) is much higher than the peers' (MSM, DXPE, FAST) average of 0.51x. Its leverage is the lowest since the Anixter acquisition (June 2020). The company's cash flow from operations turned positive in 1H 2023 compared to a steeply negative CFO in the past year due primarily to working capital improvement. The company expects to yield a positive FCF in 2H 2023. It plans to use the cash flows for stock buybacks to increase shareholder values.

Relative Valuation And Analyst Recommendation

{kind=link}

In the past 90 days, ten sell-side analysts recommended a "Buy" (including “Strong Buy”) on the stock, while two recommended "Hold.” None of the analysts recommended a "Sell." The consensus target price is $191.6, which, at the current stock price, yields a 25% upside.

{kind=link}

The company's current EV/EBITDA multiple (7.5x) is lower than the average for its peers (MSM, DXPE, and FAST). Its forward EV/EBITDA multiple contractions versus the current EV/EBITDA are less steep than its peers, indicating that its EBITDA can increase less sharply. This, in turn, typically results in a lower EV/EBITDA multiple. However, WCC’s five-year average EV/EBITDA is higher than its current EV/EBITDA. So, I think the stock is reasonably valued with a modest upside on a relative valuation basis.

Why Do I Lower My Rating?

My previous article discussed WCC’s positive momentum based on elevated construction and bidding activity in the non-residential market. It would also benefit from cross-selling synergies through complementary products and services. But the company had clear headwinds from the supply chain disruptions, while the then price hike's impact would be limited. The stock was relatively undervalued. So, I recommended a “buy.” I wrote :

Ongoing construction activity, elevated bidding activity, and non-residential market recovery have helped the company maintain an upward push. The operating margin will get a shot from increased operating leverage on higher sales.

After Q2, I see a long-term secular uptrend in many end markets. The supply chain issues that crippled its growth prospect over the past couple of years are receding. Its revenues from the UBS and CSS segments have been resilient. However, the weakness in the EES segment will likely continue soon. The stock is reasonably valued versus its peers. So, I downgrade the stock to a “hold.”

What’s The Take On WCC?

{kind=link}

The growth in the utility, data center, security, and industrial sectors is WCC’s guiding light in the environment where the industry and economic indicators send mixed signals. It focuses on improving its digital capabilities to increase market share. Better pricing will partially ease the pressure on the margin in the near term. Plus, it has recently initiated cost control measures to maintain profitability. So, the stock outperformed the SPDR S&P 500 Trust ETF ( SPY ) in the past year.

The supply chain rebalancing issue in the electrical industry has lowered its intensity, but its persistence will hamper its efforts to realize the margin expansion potential fully. The main stumbling block appears to be the EES segment’s weakness following lower construction and OEM activities. So, it has lowered its growth estimates for Q3. The other two segments, however, are expected to grow steadily. Its cash flows improved remarkably in 1H 2023 and are set to strengthen further in 2H 2023. Given the reasonable relative valuation and various counter-balancing factors, I suggest investors “hold” the stock for the near term.

For further details see:

WESCO International Holds It Steady Despite The Cracks (Rating Downgrade)