URE:CC - West-China Economic Frictions: Gleefully Marching Toward Potential Disaster

2023-08-11 09:55:14 ET

Summary

- There are growing signs of a global geopolitical rupture between the US and China, with the rest of the world caught in the middle.

- Global trade volumes and economic interdependence indicate potential damage from deglobalization.

- Disruptions in global trade, loss of intermediary inputs, and intellectual property could lead to a global economic depression.

Investment thesis: There are growing signs of a grand global geopolitical rupture taking place, which involves two main blocks, one led by the US and the other by China. Much of the rest of the world is potentially caught in the middle, as a battlefield for control or influence. Some nations may already be taking sides, while others are looking to play the two elephants in the room against each other, while trying to avoid getting crushed in the process. Others may get coerced into choosing one camp or another through either economic pressure or other means such as regime change operations and other disruptive and destructive actions. The risk is that in the process of splitting the world in two, economically, financially as well as technologically, we will wreck the global supply chains. Most nations became deeply integrated into the global economic system, thus we are all very interdependent in terms of producing most goods & services. In a worst-case scenario, this can plunge the world into an economic depression. Few investment positions will be safe if this nightmare scenario outcome will come to pass.

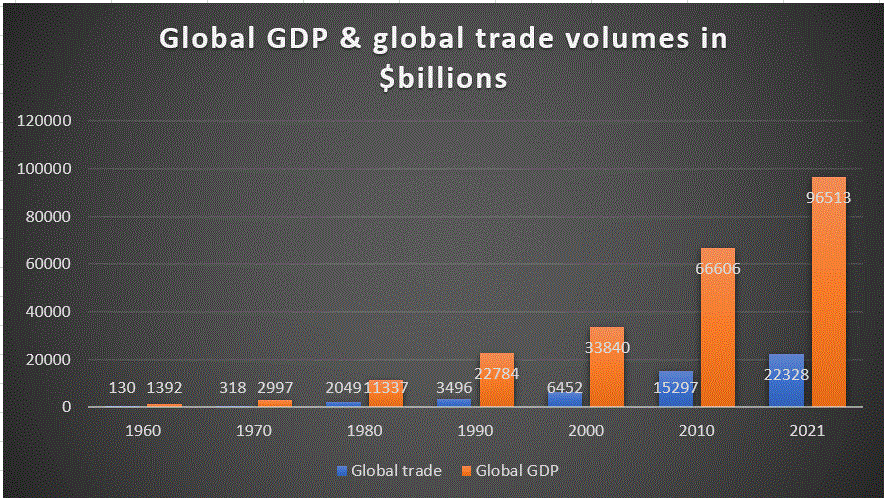

Global trade volumes are a testament to growing global integration in the last few decades, but it is only the tip of the iceberg regarding global economic interdependence

An indicative, albeit not an entirely complete picture of the growing interdependence of the global economy is the rising ratio of global trade volume versus global GDP.

{kind=link}

As we can see, global trade as a portion of GDP rose from less than 10% in 1960 to about 23% as of 2021. This by itself is indicative of the potential damage that deglobalization could potentially inflict on the global economy. In other words, if we stop most trade, it would potentially wipe out almost a quarter of global GDP. This however is only an overly-simplistic calculation, which does not correspond to reality.

The reality of it is far more complex. The increase in global trade also represents a dramatic increase in global dependence on increasingly specialized trade in intermediary goods. Some concentrations of vital products such as semiconductors are extreme, where just a handful of nations produce most of the world's semiconductors that go into most electronic products. China produces most of the mined supplies of rare earth minerals and the specialized processing that the world depends on as inputs for most hi-tech products. These are just some of the many examples where entire global industries could grind to a halt if. On top of it all, there is the cross-border trade in intellectual property or patents that can be weaponized to halt most high-tech and even some lower-tech industries around the world.

There are also all the multinationals operating around the world, which depend on the goodwill of host nations for access to their domestic markets, even if they are producing on the local market. The auto industry is a perfect example of this, where Western car brands produce and sell millions of cars in China each year.

The combined effects of disrupting global trade, the damaging effects on domestic economies due to the loss of intermediary inputs, as well as intellectual property, as well as the potential loss of access to domestic markets that companies can potentially see inflicted on them, the potential effects from global economic disruption on global economic output can be catastrophic. The factors I cited do not provide a complete list of potential disruptions, for I did not account for financial interdependence for instance. Adding it all up, in a worst-case scenario we could head for a global depression if geopolitical and economic frictions continue to be ratcheted up. In other words, I think we could see a yearly global economic contraction of 10% or more for multiple years in a row, before the global economy readjusts.

There are of course some factors that may have a dampening effect on the potential maximum impact of global economic decoupling. For instance, there is no reason to expect the US & the EU, or the UK to stop trading with each other or with other allied or dependent nations around the world. Neither would Iran, Russia, or Kazakhstan stop trading with China or with each other. Continued trade within emerging blocks, to the exclusion of trade with rival blocks could potentially also bring new opportunities. In time, new coalition blocks could potentially find ways to complement each other economically to enough of an extent that a new normal could emerge, where a return to global economic growth would be possible. Before any of that, I think we would still see years of intense misery most likely.

The march towards global economic decoupling continues

I am not entirely sure that there are currently adults in the room available to fully understand and explain the potential consequences of continued geopolitical escalation, which at this point is in my view approaching the point of no return, on a march toward disaster. The situation arguably started with the Trump administration and its curbs on Chinese imports half a decade ago. It then escalated to include attempts to choke off the rise of the domestic Chinese tech industry, with Huawei being most prominently targeted. The tech squeeze in particular continued in the Biden administration and it has been recently amplified with a clear attempt at wiping out China's advanced semiconductors industry.

In a first glimpse of Chinese retaliatory measures, China intends to respond by curbing exports of materials that are critical in the semiconductor industry, which China currently has a near-monopoly over. It was the first forceful response after more than half a decade of taking punches mainly from the US in terms of trade tariffs, tech use restrictions, and other hostile economic measures that were implemented throughout the past two administrations. Chances are that there will be far more to come if this continues, which will prompt US & EU officials to ramp up retaliatory measures. This could be the start of the point of no return, on to the path of mutual economic destruction in my view.

We should note that in parallel, we have the Russia issue, where we have been incurring economic damage on a global as well as local scale for over a year and a half now, with the EU facing a stagflationary situation , with potentially worse yet to come. As I stated on many previous occasions, as a result of the economic war with Russia, Europe is now always one bad winter away from economic disaster. It should be noted that the bad winter weather is not just about Europe, but also about the United States, which is now its largest supplier of LNG by far, accounting for about half of all LNG imports.

The Farmer's Almanac is forecasting a colder winter for the US. If that will be the case, there will probably be less natural gas available for LNG exports. If this turns out to be correct, and Europe's winter will turn out to be colder than average, we are likely to see the first real glimpse into what it means to burn existing economic relations, with potentially far worse to come.

Given the public mood of our time, reflected in MSM rhetoric, as well as that of the political establishment in the Western World, odds are that even if the EU will come out of the coming winter badly damaged, perhaps even destabilized internally, there will be no sobering up. The Western World and a number of its allies around the World see an end to absolute Western-led global hegemony approaching, and we seem to be in the beginning stages of losing complete control. In an attempt to prevent it from happening, we are arguably set to see our leadership engage in more assertive and aggressive behavior around the world. On the other side of the equation, we have countries in Asia, The Middle East, Africa, and Latin America, lining up to join China-led groups such as BRICS, the SCO, and other international structures that it dominates or within which it is influential as a counterweight to our power & influence.

Perhaps the clearest sign of things having already gone past the point of no return is the MSM reaction to Kissinger's latest trip to China , where he received the warmest of welcomes from China's top leadership, in contrast to the mutually antagonistic tone set in recent visits of EU or US dignitaries to China. The media as well as officials have been mostly dismissive of the visit's importance, making sure to highlight its very unofficial nature. In other words, Kissinger was in no way there as a voice for us, just a simple private citizen. I think the era of engagement that his legacy represents has been therefore rejected. What comes next seems to be an era of mutual economic hostility, great power competition for client states, as well as proxy wars evidently, as we see with Ukraine, and possibly soon to be seen in Niger.

Investment implications:

In response to the Western World's efforts to tighten the screws on China's tech industry, we see more and more signs that China is starting to adapt. The latest news is that Chinese firms are making inroads into semiconductor-production technologies. Huawei in particular is thought to be close to replicating EUV capabilities that currently only ASML ( ASML ) can provide to chip producers. There are also other R&D efforts underway meant to look beyond silicon as a semiconductor material. If China will manage to achieve significant breakthroughs, it could shake up the entire global tech scene this decade.

Huawei could, in theory, return as a formidable challenge on the global market to Apple ( AAPL ), Samsung ( SSNLF ), and others in the mobile communications segment. ASML could find itself not only facing challenges but having its technology relegated to second-best if potentially superior materials such as graphene will become the new cutting-edge in the semiconductor industry. The likes of AMD ( AMD ) and Intel ( INTC ) will probably see a rise in global competition, mostly from emerging Chinese competitors. It should be noted also that the efforts to weaponize our technological superiority may lead to countries around the world seeking to break our near-monopoly on certain tech products, which will automatically lead to most of our tech giants seeing global demand plummeting.

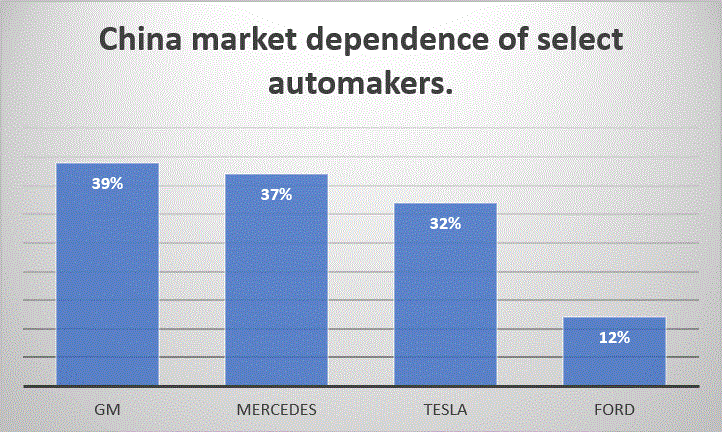

Beyond the unfolding tech war between the Western World and China, there are far more direct and obvious angles of vulnerability. The auto industry for instance has a great deal of exposure to China.

{kind=link}

It should be noted that China has nowhere near the same kind of exposure to our markets for its own domestic or controlled brands. Its domestic industry at the same time is now developed enough to quickly fill the void that an exit of Western brands would cause in terms of total supplies. This would therefore in theory be a very obvious place where China can retaliate against Western industries by pushing them out through various policies.

As we can see, GM ( GM ) & Mercedes ( MBGAF ) would potentially see a catastrophic decline in sales and potential loss of capital if they would be forced to exit the Chinese market. Tesla ( TSLA ) is arguably in a better position to potentially negotiate an exemption, given Elon Musk's arguably amicable relations in that country, but nothing is for certain. Ford ( F ) has a much smaller level of exposure to the Chinese market, therefore it might have the least to lose from a potential flare-up in the emerging economic war, but its exposure is not insignificant. This in my view is a great example where investors might not even think twice about the implications of how exposed certain investments may be to the great economic decoupling that we are currently contemplating and arguably starting to implement. If relations will continue to deteriorate, I see no reason why China would be open to continue allowing Western automakers to continue to sell their cars on their market, given that its own domestic industry can arguably easily fill the void.

Perhaps the most important lesson from my example of how deeply exposed investors are to this emerging geopolitical threat to global stability is that there is nowhere to hide. Ford seems like a decent bet, given its much lower exposure to China, but it is just as exposed as all other car manufacturers to secondary effects if the global economy falters. Trying to understand to what extent the world could potentially falter, once we factor in the magnitude of global trade, the magnitude of interdependence on raw materials and intermediary goods, then add to it systemic risks as secondary ripple effects, I think we could potentially plunge the world into a depression, not just a recession, which would wipe out most investors, regardless of how one allocates investments within one's portfolio.

If we fail to prevent a global economic and geopolitical conflagration, the most likely outcome is a stagflationary trap. The disruption of the global supply chain will inevitably lead to severe shortages of goods, while the real economy disruptions would be severe enough to lead to severe job losses. Those still holding on to their jobs will see their real income shrink drastically, as wages will fail to keep up with inflation.

Classical haven stocks might not perform the function we are used to since the post-WW2 era. For instance, Kimberly-Clark ( KMB ) will not work within the context of global supply chains breaking down. It needs to have access to all the markets where it sells its products, and it needs to have access to all the raw and intermediary inputs, as well as energy inputs for its manufacturing and transport activities. It is currently present in dozens of markets around the world and it sells its products in almost every country on the planet.

Cash is not necessarily a haven either. If severe supply chain disruptions will restrict the volume of goods available, inflation is likely to return and surpass recent high levels. The stock market might go up in nominal terms in that event, even if the rate of appreciation will be far from keeping up with the rate of inflation. Being in stocks, invested in a broadly diversified portfolio might beat cash as a store of value.

There is of course gold, held in various forms, whether in physical form, ETFs like GLD ( GLD ), or mining stocks. While I do believe that having some gold exposure is a must within the current environment, as insurance against everything else going wrong, the shorter to medium-term outlook for gold is quite uncertain in my view. There can be market manipulation, or simply market events that have the potential to push gold prices down significantly, if only temporarily. For instance, central banks that have been massive net buyers in the past decade could be forced to sell gold in large volumes to defend their fiat currencies.

Investors may be forced to sell to cover losses in some cases. I own GLD shares, as well as physical gold, and miners, mostly Barrick ( GOLD ), Wheaton ( WPM ) which is not a miner in the traditional sense, as well as Silvercorp ( SVM ) stock which is more of a silver producer. I am fully prepared to ride out periods of gold price weakness, while I am also somewhat hesitant to take profits on my gold & silver positions because I see it more as insurance against things going wrong with fiat, the global economy as well as many individual stocks, which should be in place at all times.

As I stated in a recent article , I am considering taking some profits this summer or early fall. The one exception is my oil & energy sector position in my portfolio. This is currently mostly represented by Suncor ( SU ), which is currently my largest holding in my portfolio by far, Canadian Natural Resources ( CNQ ), as well as a small position in Chesapeake ( CHK ) in the oil & gas sector. I own Cameco ( CCJ ) stock as well as Ur-Energy ( URG ) in the uranium mining sector. We will probably see an energy price spike, despite already subdued global economic growth late this year or early next year, simply because of a lack of supply growth prospects. Sometime between early 2024 and the middle of next year might be a good time to be taking profits on my energy stocks but for now, it might be the one segment of the market that is likely to beat inflation.

The potential fallout from what seems to be a willful effort to bring the era of global economic integration to an end will leave almost no investments untouched. At this point, I am sensing that the market is failing to appreciate the potential magnitude of the impact. It is entirely possible that the stock market will continue to rise in nominal terms, but in real terms, in other words, adjusted for inflation It will be very hard to preserve wealth. A stagflationary economic environment does not provide for too many opportunities to build wealth through investments. The task will be made all the more challenging as the market will be loaded with minefields that can hit individual stocks or sometimes entire segments of the market, often without warning, potentially wiping out most investment positions. It goes without saying that it would be best if a change in policy will pull us off the current dangerous path we are on. In the absence of that, I think prospects for investors look bleak looking forward, with success being measured in terms of how much of a reduction in real wealth investors will be able to achieve, rather than how much wealth is being gained.

For further details see:

West-China Economic Frictions: Gleefully Marching Toward Potential Disaster