WST - West Pharmaceutical Services: A Solid Buy For Long-Term Investors

2024-01-09 22:45:04 ET

Summary

- Century-old West Pharmaceutical Services has a strong history of growing its top and bottom lines.

- It remains a growth stock, with very good margins, seasoned management and a proven strategy.

- It will be overvalued for short-term investors, but fairly priced for investors with medium and long-term horizons.

Thesis

For the first seven months of 2023, West Pharmaceutical Services, Inc. ( WST ) was a market star, rising from $234.41 on January 3, 2023 to $412.41 on August 29. It went on to hit a low for the year of $318.29 on October 31 before rising to $352.12 on the last trading day of the year, December 29.

I expect the share price to keep heading upward over the medium to long term, although not necessarily at the same pace as last year.

About West

Now in its 101 st year, the company manufactures and sells what it calls “innovative, high-quality injectable solutions and services.” On its website , it also wrote that it does this in partnership with drug developers to contain and deliver medicines for patients. It reported that it delivers some 47 billion components per year.

At the close on Monday, January 8, 2024, it traded at $351.85 and had a market cap of $25.12 billion.

Competition

In its 10-K for 2022 , West reported that it competes with several companies across its product lines. Competitors and comparables include Baxter International Inc. (BAX), Mettler-Toledo International Inc. (MTD), and ICON Public Limited Company (ICLR).

It has several competitive advantages, including:

- Specialized knowledge of container closure components.

- A global presence, including the global scope of its manufacturing capabilities.

- Innovative solutions, backed by its own research and development activities. In 2022, it received more than 150 patents worldwide.

Morningstar assigns it ‘wide moat’ status, which is very strong. With this type of moat, we expect the company to have strong margins and profitability (more on this later).

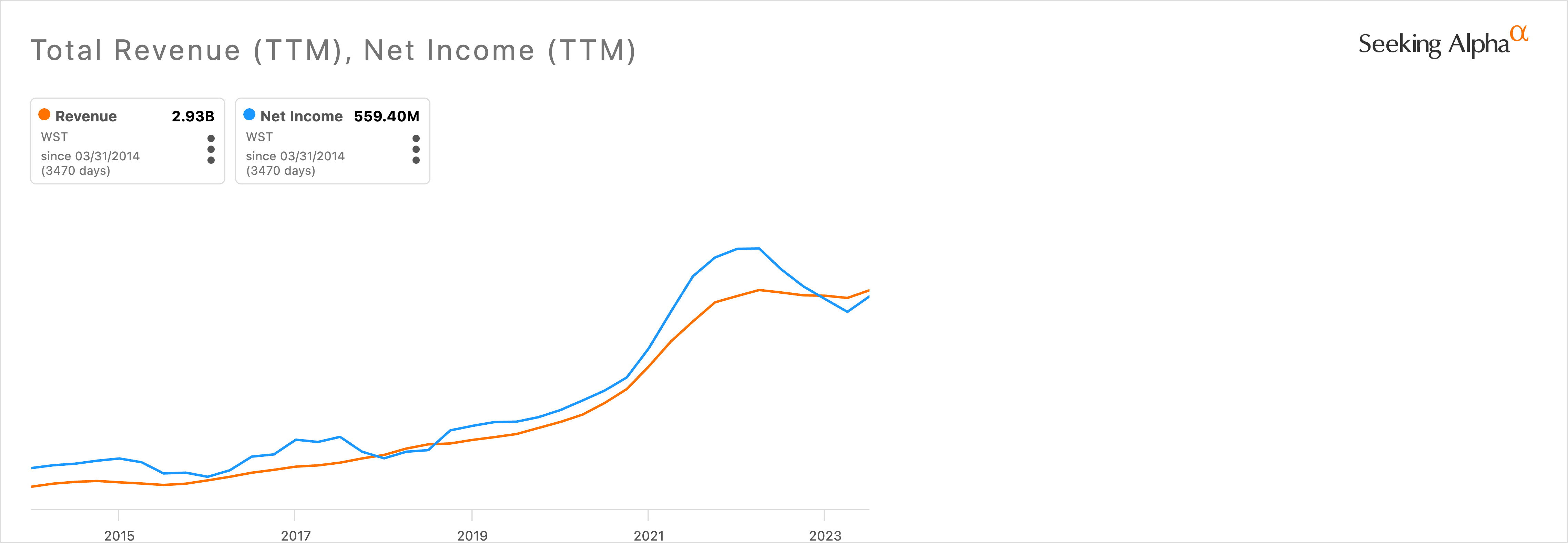

Growth

West has put that financial prowess to good use, growing its revenue and net income significantly over the past decade:

{kind=link}

Why was there a decline in net income during 2022? CEO Eric Green explained it this way in the third quarter press release , “While our base, non-COVID-19 demand continues to grow, we have had multiple constraints that impacted our financial results. Delays in expansion projects as well as customer delivery timing and mix-shift related productivity impacts resulted in lower-than-expected overall high-value product (HVP) net sales. We expect to resolve these issues in early 2023."

The company reported in its Q3-2023 press release that net sales had grown by 8.8% over Q2-2022 and earnings per share had grown by 34.6%. Green did warn, though, that the firm had seen a slowdown in restocking by large pharma and generic customers.

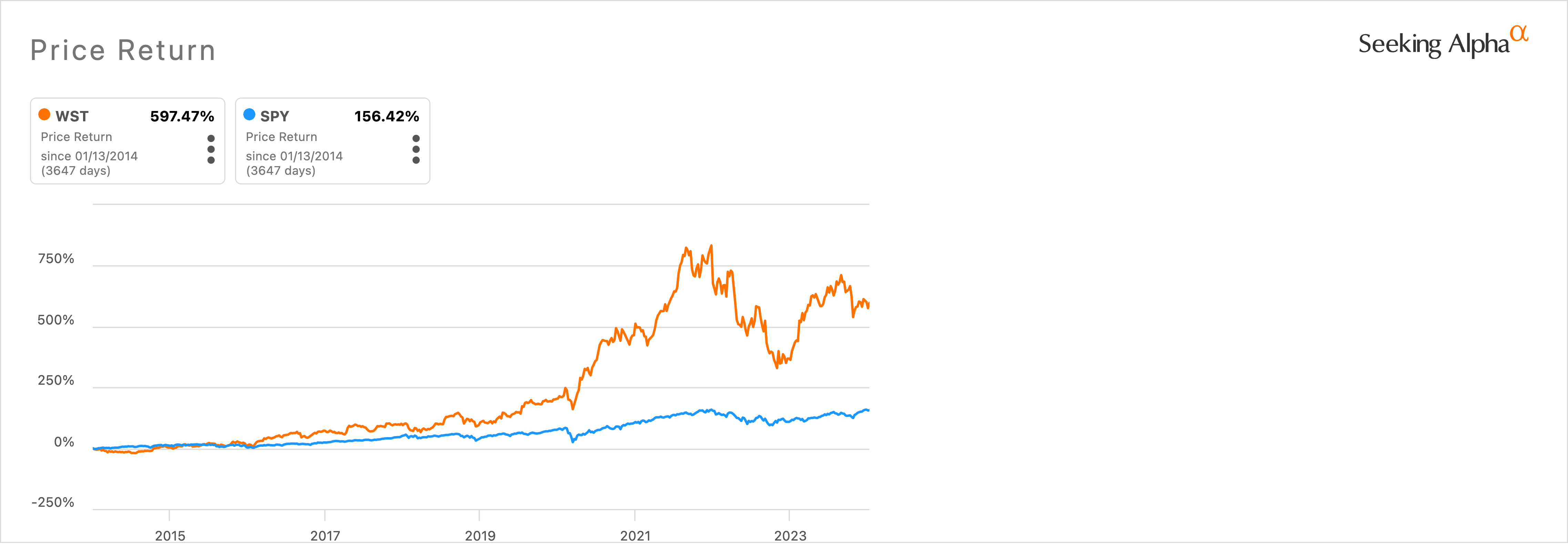

Despite the hiccups, West’s price return has seriously outpaced that of the S&P 500 over the past decade:

{kind=link}

Return on equity, or ROE, on a TTM basis, is a healthy 20.96%

Margins

Given its competitive advantages, we would expect West to have strong margins. And that is the case, with a gross margin of 38.13%, an operating margin of 24.19%, and a profit margin of 19.12%. Ample margins also provide free cash flow for capital expenditures.

As shown in the revenue and net income chart above, net income has been quite consistent with revenue growth. That suggests management has been disciplined, allocating its cash flow to projects and growth that drive steady growth.

It also has been disciplined about taking on debt; its current total debt is $306.80 million, which compares favorably to its cash holding of $898.60 million. That gives it a debt-to-equity ratio of 0.11, which is low.

Management and strategy

President and CEO Eric Green has held these positions since 2015, as well as board chair since 2022. He has a Master of Business Administration degree and served in senior positions at the chemical sciences firm Sigma-Aldrich before moving to West.

Bernard J. Birkett, the Chief Financial and Operations Officer, is an accountant and has a master’s degree in banking and finance. Before joining West, he held senior positions at Merit Medical Systems, Inc. (MMSI), a manufacturer of disposable medical devices.

West summed up its business strategy this way on its website , “West is committed to growing its business and the industry through strategic capital investments and partnerships that will drive innovation. Through strategic investments across the industry, West can support innovative practices and products that will improve the healthcare process, help clinicians to deliver better care, and ultimately benefit patients.”

Based on results delivered over the past decade, the company has successfully executed its strategy.

Risks

West is not the only healthcare company competing for the business of other providers, the medical community, and patients. Disruptive new technologies could slow or stop its growth.

Its credibility and reputation could be affected by bad news, making it a less attractive partner to other corporate providers.

As a medical products developer and manufacturer in multiple countries, West is subject to extensive regulations and rules.

Sales outside the U.S. accounted for 55.4% of net sales in 2022, exposing it to currency exchange risks and geopolitical turmoil.

Consolidation is ongoing in the pharmaceutical and healthcare industries, and could pressure its prices.

Because it buys its raw materials and supplies on open markets, it could face supply chain failures and disruptions in its operations.

Valuation

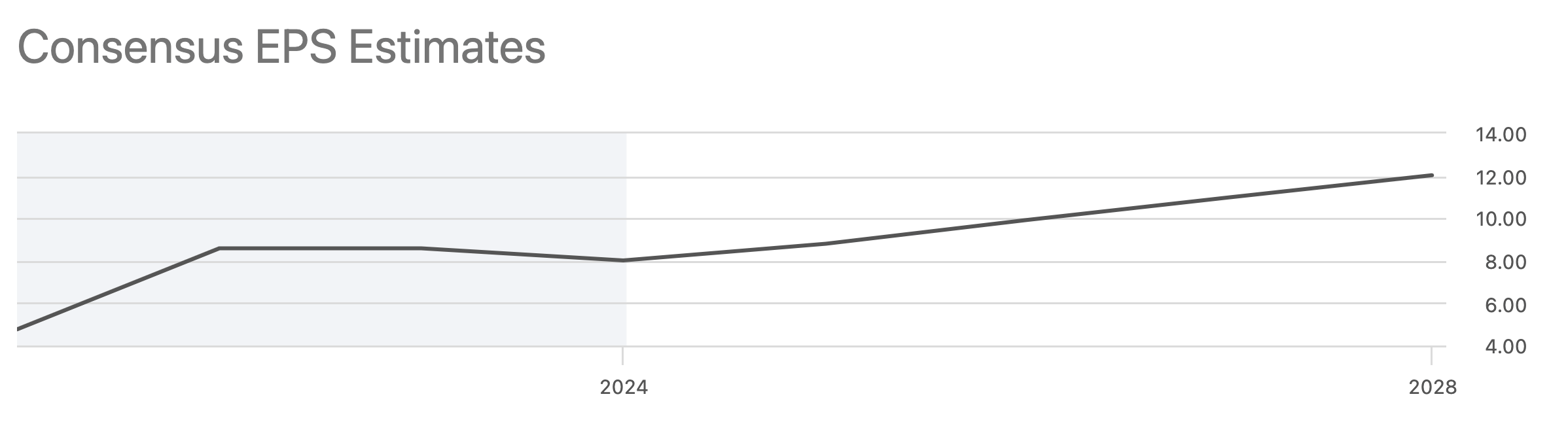

The following chart shows consensus earnings per share estimates for West:

{kind=link}

This year’s estimate comes from eight analysts, the 2024 estimate from nine analysts, and one analyst for 2026 and 2027.

The estimates suggest that EPS will climb from $8.01 for 2023 to $12.03 for 2027. That’s a 50% increase over four years, or an average of 12.5% yearly. The figure is conservative in relation to its earnings growth over the past decade.

Since the share price has a history of following net income, then we would argue that a 50% increase in earnings would suggest a 50% increase in the share price over four years. That would take the price from $351.85 (at the close on January 8) to $577.28 in four years.

That’s a relatively optimistic forecast for a stock that’s been given an F grade by the Seeking Alpha system. The components of that grade include:

- P/E Non-GAAP FWD: 42.36 vs. the Healthcare sector median of 18.97.

- PEG NON-GAAP FWD: 5.41 vs. 2.16 for the sector.

- EV/EBIDTA FWD: 29.44 vs. 13.33 for the sector.

- Price/Sales FWD: 8,49 vs. 3.93 for the sector.

The components also include an F for the low dividend yield, of 0.23%. Turning to other ratings, Quants give West a Hold rating, while a SeekingAlpha analyst gave it a Sell, and Wall Street analysts rate it a Buy. Altogether, this stock is expensive--in the short term.

If we treat it as a medium to long-term holding, then I believe its shares are fairly valued. They are expensive when compared with where they were recently, but not so pricey when compared with where they might be in a year or five years from now.

The legendary fund manager Peter Lynch wrote about stalwarts in his book One Up On Wall Street , one of six categories of stocks. Stalwarts are large, well-established companies that continue to offer long-term growth potential. I believe West fits that pattern, even though it has grown its earnings by more than 10% - 12% per year (Lynch’s criterion).

Conclusion

West Pharmaceutical Services has delivered generously to shareholders over the past decade, and there’s no reason to think it won’t continue to do so in the future.

It has steadily grown its revenue and earnings, despite the many economic challenges over the past 10 years. Thanks to its enviable margins, it has enough free cash flow to keep that growth coming. It has a seasoned management team and a proven strategy to guide it. And, while it may be overvalued in the short term, it is fairly valued when considered over four to five years.

Based on these details, I believe West is a solid Buy.

For further details see:

West Pharmaceutical Services: A Solid Buy For Long-Term Investors