SSNLF - Western Digital: Upgrade To Buy - The Turnaround Moment Is Here

2023-04-13 16:00:47 ET

Summary

- We’re upgrading Western Digital Corporation to a buy after Samsung Electronics Co., Ltd. pledged to cut memory chip production to a “meaningful level”.

- We expect Samsung and other industry players' production cuts will accelerate the memory market recovery toward 2H23, benefiting WDC’s flash business.

- We continue to expect a true market recovery will take time but believe the industry turnaround has now been triggered by the industry leader.

- We also expect the PC, smartphone, and data center markets to transition to higher-capacity storage devices as new models and platforms launch in 2H23 and again in 1H24.

- We believe longer-term investors should now explore entry points at current levels as we expect WDC to be in a better position to outperform expectations in 2024.

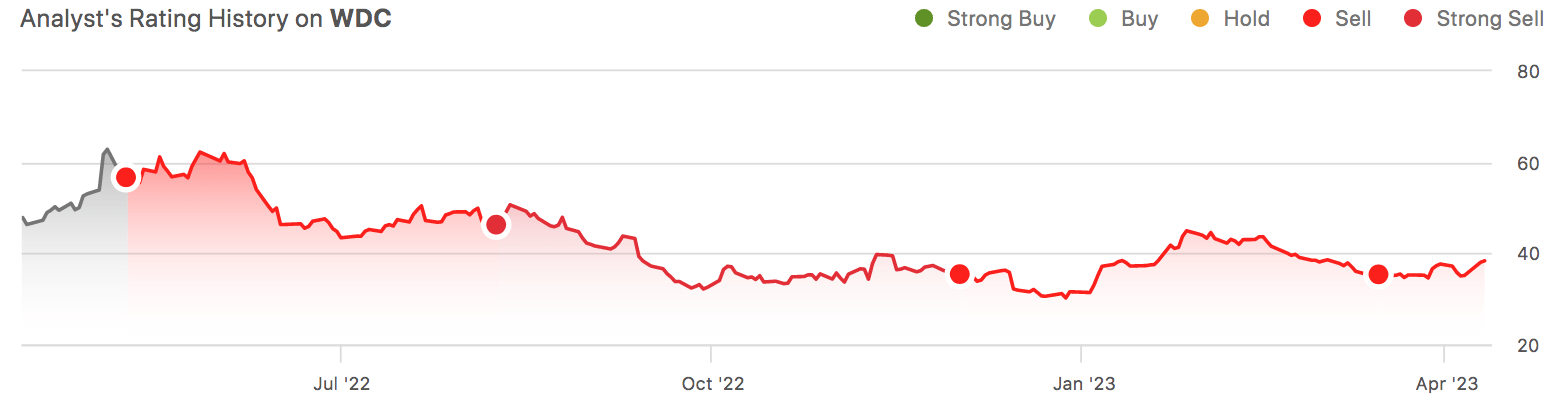

We're upgrading Western Digital Corporation (WDC) to a buy after Samsung caves to the macroeconomic environment and pledges to cut memory chip production to a "meaningful level." We expect Samsung's production cut, alongside that of Micron Technology, Inc. (MU) and SK Hynix, will accelerate the memory market recovery toward the second half of the year. Our upgrade is driven by our belief that the memory market recovery will benefit WDC's struggling flash business, a major concern in our previous bearish sentiment on the stock. The following graph outlines our rating history on WDC.

{kind=link}

We expect true market recovery will take time, but we believe the industry turnaround is set in motion. We expect industry supply-demand dynamics will come into balance more meaningfully in 2H23. We're also seeing the industry transition to higher-capacity storage devices in PC, smartphone, and data center markets, with new models and platforms to be launched in 2H23 and in 2024. We recommend long-term investors begin looking for entry points into the stock at current levels.

Industry turnaround: Triggered

We're revising our sell rating on WDC after being bearish on the stock since 1H22. We see WDC outperforming toward the end of the year as the memory market recovery is sped up by Samsung Electronics Co., Ltd.'s production cut, estimated to be around 20%. Why does it matter that Samsung cut production? In order to understand our upgrade rating, it's necessary to understand the significance of Samsung joining the production cut wagon to improve supply-demand dynamics in the memory market. Samsung has resisted production cuts since the beginning of the weaker spending environment; the company tried to expand its market share by increasing production while others in the industry cut production and reduced Capex.

MU announced it would reduce DRAM and NAND wafer production by approximately 20% last November. More recently, in 2Q23 earning results , the company expected industry supply growth in both DRAM and NAND to be below demand, moving along inventory correction cycles. MU made further reductions to their FY2023 Capex plan, now expecting to invest around $7B in FY2023, down 40% from last year. Meanwhile, SK Hynix reduced its investments by 50% for 2023 compared to 2022; the company's co-CEO, Park Jung-ho, announced that the company wouldn't be implementing any further production cuts this year.

We believe Samsung, the company with the largest market share in memory markets, cutting production was the last shoe to drop to trigger true market recovery. Samsung's move to cut production highlights just how bad the demand slump is; the news came as Samsung estimates its operating profits to drop 95.8% Y/Y to $600B in 1Q23 from $14.12T a year earlier. We expect the weaker PC and smartphone demand levels to result from consumer demand contracting from pandemic levels. We're more constructive on the memory market now, expecting inventory correction cycles to improve supply-demand dynamics.

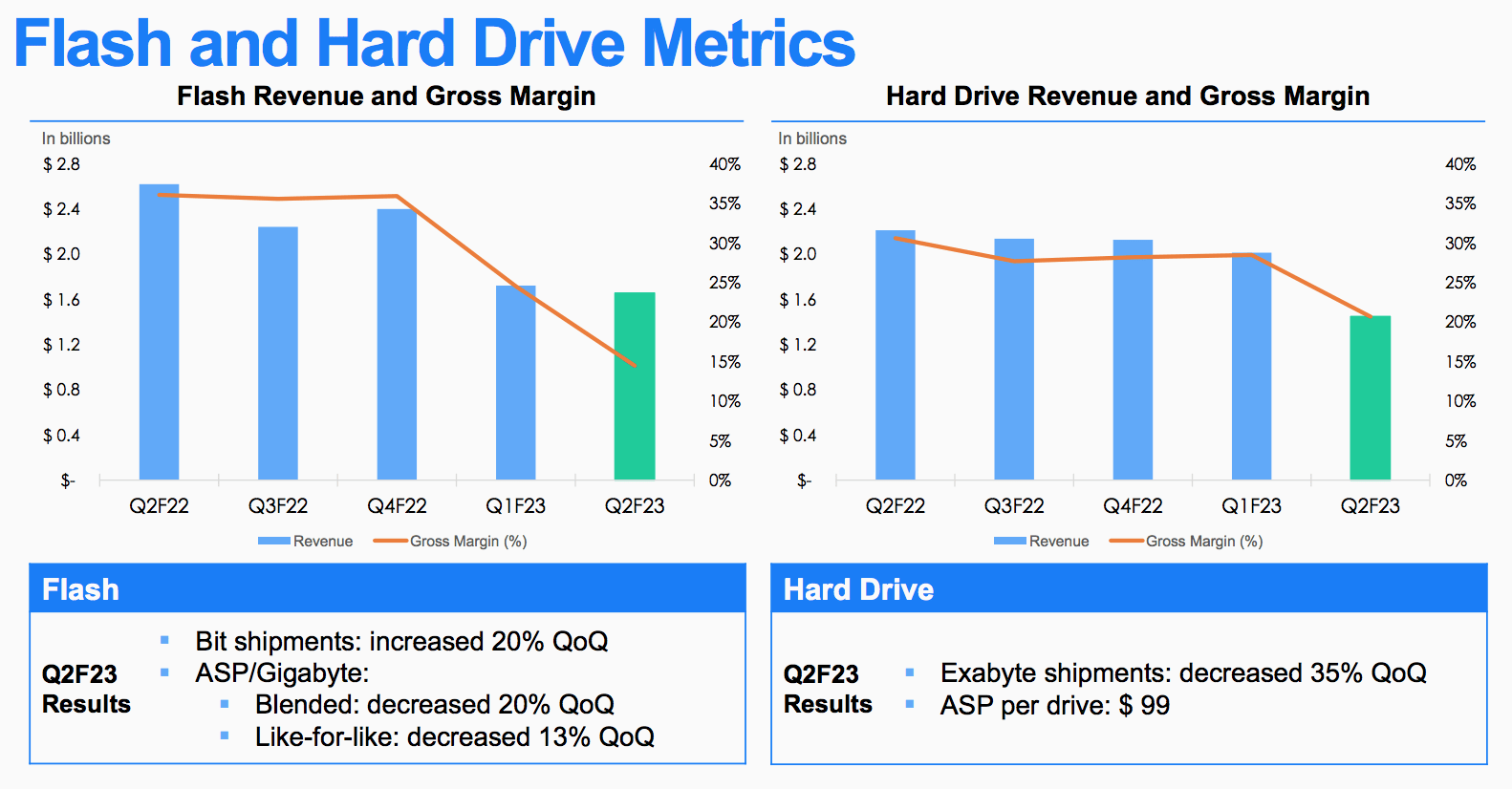

WDC stock surged 9% on Monday after the news, giving the stock a much needed-boost as more than 4.3M shares of the stock traded hands in early Monday. WDC has also taken steps to further reduce Capex across its flash and HDD businesses to moderate supply. WDC's projected cash Capex for FY2023 "declined nearly 40% from six months ago" as of its 2Q23 earnings call . The company cited seeing drops in both client and enterprise demand due to digestion issues and hence decided to cut wafer starts to manage inventory buildup. Our previous note on WDC referenced our concerns over WDC's gross margins being under pressure in its flash business. We continue to see near-term pain due to weaker demand from PC and smartphone end-markets. The following graph outlines WDC's flash and HDD metrics as of 2Q23.

{kind=link}

We expect smartphone and PC total addressable markets ("TAMs") to shrink this year compared to last year due to the persisting macro headwinds pressuring consumer and enterprise spending. Still, we're seeing a clearer path to market recovery toward the end of the year. We expect Samsung's production cut will not only ease inventory buildup but also help prop up prices. In 2Q23 , WDC's flash ASP/Gigabytes decreased 20% sequentially, and HDD ASP dropped to $99 from $125 a quarter earlier. We expect chip price pressure to ease in the mid-to-long term as market recovery is underway.

We also expect WDC to benefit from the global transition to higher-capacity storage devices in PC, smartphone, and data center markets. We expect HDD industry supply-demand dynamics to continue to recover toward 2H23 as we've seen HDD inventory corrections begin earlier this year. WDC and Seagate Technology Holdings plc ( STX ) dominate the HDD market; as both companies cited decreased shipments to move along HDD inventory correction cycles, we're more constructive on HDD industry dynamics improving in 2H23.

Both companies forecast HDD exabyte shipments to pick up toward the end of the year. WDC discussed improving HDD dynamics in the 2Q23 earnings call , referencing the slowdown in HDD revenue to intense cloud inventory digestion "while demand for retail and client HDD improved." We also expect HDD industry recovery to be driven by WDC ramping up 22 terabyte CMR products and driving along SMR variants, including its 26TB UltraSMR drives, to keep up with cloud customer adoption of higher capacity storage devices. Still, we believe WDC will face pricing pressure due to underutilization, but our bullish sentiment is driven by our belief that the second half of the year will be much better than the first.

We've recently upgraded WDC competitor STX. We believe STX will experience improved ASP as it launches its 25TB-plus drives to feed increased cloud customer demand for higher-capacity HDDs. We recommend long-term investors begin looking for entry points into WDC at current levels.

Valuation

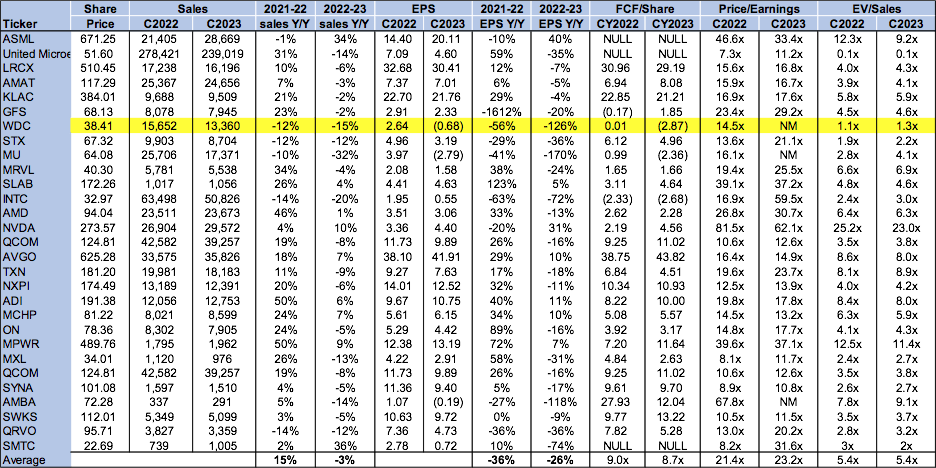

Western Digital Corporation stock is extremely cheap, trading well below the peer group average. The stock is trading at 1.3x EV/C2023 Sales versus the peer group average of 5.4x. We see favorable entry points into the stock at current levels, as we believe the memory market is en-route to recovery toward the end of the year. There's still a long path ahead, but we believe investors buying the stock at current levels will be well rewarded in 2024.

The following table outlines WDC's valuation compared to the peer group.

{kind=link}

Word on Wall Street

Wall Street doesn't have a clear consensus on the stock. Of the 28 analysts covering the stock, 13 are buy-rated, 14 are hold-rated, and the remaining are sell-rated. The stock is currently priced at $38 per share. The median sell-side price target is $48, while the mean is $47, with a potential 22-25% upside.

The following graphs outline WDC's sell-side ratings and price targets.

TechStockPros

What to do with the stock

We're moving WDC to a buy after the industry leader, Samsung, vouched to cut memory chip production, joining MU and SK Hynix in accelerating the memory market recovery. We expect WDC's flash businesses to benefit as industry supply-demand dynamics come back into balance toward 2H23. We also expect to see increased adoption of higher capacity storage devices in PC, smartphone, and data center markets, positively impacting WDC's HDD business.

Western Digital Corporation stock is down roughly 40% from its 52-week high of $63.26. We expect WDC to outperform expectations toward the end of the year. We recommend long-term investors begin exploring entry points into the stock at current levels.

For further details see:

Western Digital: Upgrade To Buy - The Turnaround Moment Is Here