WU - Western Union: Buy This Stock For 8% Dividend Yield And Potential Upside

2023-11-06 06:12:58 ET

Summary

- Western Union reported a revenue of $1097.80 million, up 1% compared to $1089.60 million in Q3FY22.

- The comparison of the forward P/E ratio of 5.81x with the sector median of 8.56x shows WU is undervalued.

- With a capital return of 47.3% and dividend yield of 8.01%, investors can expect a total return of 55.31%.

Investment Thesis

The Western Union (WU) Company deals in global money movement and payment services. The company has recently reported its quarterly results and has maintained its revenue levels despite the elevated inflation. I believe it can improve its performance in the coming quarters by leveraging its market presence and strong network effect to capture additional market share.

About WU

WU provides money movement and payment services. The company conducts its business in two operating segments: Consumer-to-Consumer and others. The Consumer-to-Consumer segment mainly includes money transfers from one consumer to another. These services are conducted through its worldwide retail agent locations as well as through mobile applications and websites. It generates revenue through considerations paid by the consumers to transfer money. This segment contributed 89% to the company's total annual revenue in FY2022. The Other segment mainly includes its bill payment services in the United States and Argentina. It provides options to customers to make payments to businesses and other organizations, including mortgage servicers, utilities, financial service providers, auto finance companies, and government agencies. This segment generated 6% of the company's total annual revenue in FY2022. Earlier WU had a segment of Business Solutions, which has been sold for the cash consideration of $910.0 million. It contributed 5% to the company's total revenues in FY2022.

Financials

{kind=link}

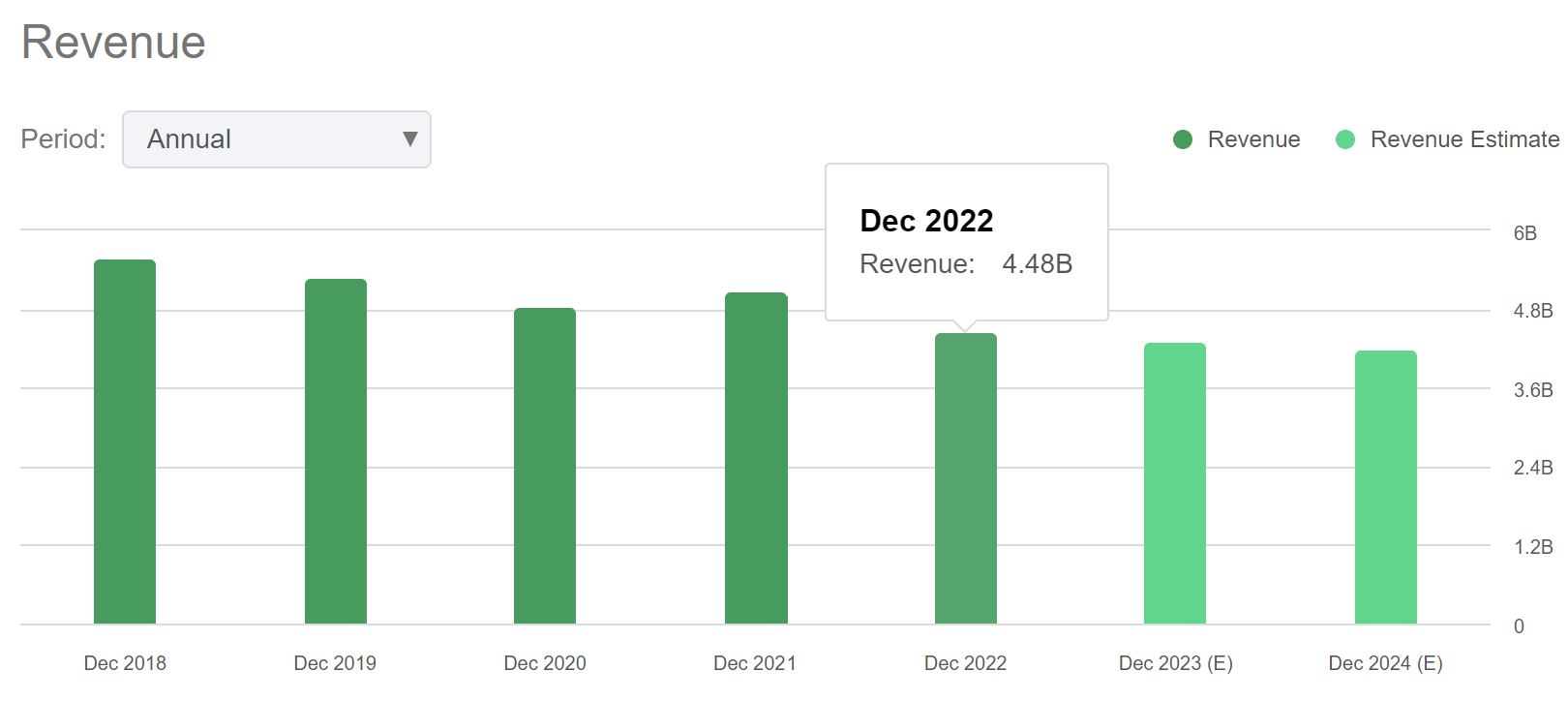

WU has been experiencing a stagnant revenue trend since FY2020. The company has reported a $4.48 billion annual revenue in FY2022 which is a decline of 7.44% compared to $5.07 billion in FY2021. The decline in revenue was fueled by decreasing sales from its retail operations. The company reported a revenue growth of 4.75% in ($5.07 billion) FY2021 compared to revenue of ($4.84 billion) FY2020. The growth was driven by the solid results of Western Union Business Solutions and digital platform which is partially offset by weak performance of the company's retail business.

{kind=link}

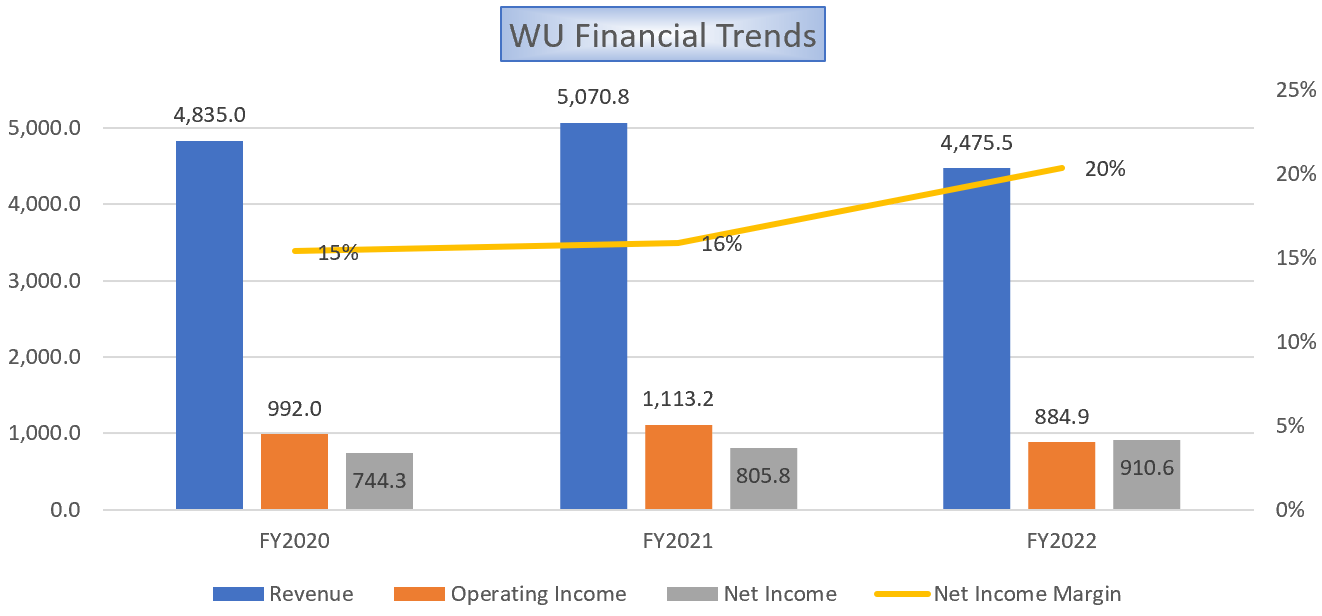

Despite the struggling revenue growth, the company has managed to increase the net income margin significantly in last three years which indicates enhancing financial leverage of the company. The company has reported net income margin ((NIM)) of 16% (NI of $805.8 million) in FY2021 which is an increase of 100 bps compared to NIM of 15% (NI of $744.3 million) in FY2020. In FY2022, WU experienced a strong NIM growth as it reported a NIM of 20% (NI of $910.6 million) which is growth of 500 bps compared to the NIM of FY2021. The net income margin has improved as a result of decreasing interest expenses and improved operating margins as a result of decreased expected marketing costs and agent losses.

The digital revolution has gained significant momentum, especially after the global COVID-19 pandemic which led to a rise in digital payments globally . However, the industry is still highly underpenetrated as some economies have a large portion of the unbanked population. Countries such as Vietnam, Morocco, the Philippines, Mexico, and Egypt have the largest unbanked populations which creates a huge opportunity for the companies operating in the fintech industry. Though there is a large untapped market, the competition in this industry is equally intensified. Companies are more focused on capturing market shares and penetrating deeper into the market which I think is one of the most essential and challenging parts of sustaining and improving profitability. Analyzing WU from these parameters, I believe it has done an impressive job of building a strong network of more than 550,000 agents in over 200 countries which gives it a competitive advantage in acquiring additional customers by its strong market presence and recognition. In addition, the company also has partnerships with retail corporations which can help it to acquire additional customers as partnerships can create a network effect by making WU's platform available for payments of partner's customers.

The company has reported its quarterly results . It reported a revenue of $1097.80 million, up 1% compared to $1089.60 million in Q3FY22. This growth driven by the modification in monetary policy of Iraq and growth in global branded digital sales growth which is offset by inflationary pressures that impacted its cross-currency transactions. The company has managed to surpass the market's consensus by $60 million or 5.78%. The gross margin stood at 37.41%. Net income declined by 1.66% YoY from $173.9 million to $171.0 million. The decreased net income resulted in EPS of $0.46 which is $0.06 or 15% higher compared to the market's expectations of $0.40. The decrease in net income is result of a high tax rate. WU reported $1138.20 million in liquidity and adjusted EBITDA stood at $261.5 million.

Calculation of Average Net Income Margin of WU (Value Quest)

{kind=link}

The company performed decently despite the inflationary pressures as a result of healthy demand dynamics. I believe it can improve this growth level in the coming quarters once the inflationary pressures cool down and by leveraging its fast-growing network effect to acquire more customers. Even the revenue from retail operations is stabilizing. The management has confirmed that the company has managed to achieve flat YoY retail transaction increase in last quarter and improvement in retention of retail clients in major markets such as the USA. After delivering results which is above the market's expectation, the company has reiterated its outlook for FY2023. The company expects FY2023 GAAP EPS between $1.67-$1.74 (previous outlook $1.72). According to Seeking Alpha, WU's revenue for FY2023 and FY2024 might be $4.36 billion and $4.39 billion, respectively. After considering the stabilizing retail segment, increase in global branded digital revenue, and negative effects of rising inflationary pressures, I think Seeking Alpha's estimates are accurate. WU's 3-year average net income margin is 17%. I believe the company can maintain net income margin of 17% with the help of decreasing interest expenses and lower plan marketing expenses. Therefore, I am assuming net income margin of 17% for FY2024 which gives an EPS estimate of $2.02 for FY2024.

Dividend Yield

The company has a consistent dividend payout which indicates its strong positioning. The company has been paying stable dividends for the last 14 years. It distributed four quarterly dividends of $0.235 in FY2022, totaling an annual dividend of $0.94 per share and representing a dividend yield of 8.01% compared to current share price. It distributed a $0.235 dividend in each of the first three quarters of the current year, and given the company's healthy cash positions, I believe it can maintain its quarterly dividend of $0.235 in the last quarter as well, which makes the annual dividend of $0.94 and represents a forward dividend yield of 8.01%. The company's forward dividend yield is 110.42% higher compared to sector median dividend yield of 3.81%. This appealing dividend yield makes the firm an attractive option for risk-averse and retired investors seeking stable income as well as capital appreciation.

What is the Main Risk Faced by WU?

The company outsources several of its services to third-party vendors. These mainly include software application support, cloud-based services, check clearing, processing of returned checks, call center services, and the hosting, development, and maintenance of its operating systems. If these parties fail to provide services in case of labor shortages or any other reasons, it can be challenging to manage operations. In such scenarios it can negatively impact the company's operations and further contract its profit margins.

Valuation

The company has maintained its revenue levels despite macroeconomic pressures which indicates its strong positioning. Observing its strong global agent presence and network effect, I believe the firm can continue to develop and be able to enhance its market share and profitability in the future by increasing its customer base. In Q3FY23, the management has confirmed that the retail segment is stabilizing with the help of client retention in large markets like the USA. Considering estimation calculation in financial section of this report, I am estimating EPS of $2.02 for FY2024 which gives the forward P/E ratio of 5.81x. The comparison of the forward P/E ratio of 5.81x with the sector median of 8.56x shows the company is undervalued. I think the company might grow in the coming quarters and trade at its sector median as a result of significant growth in the industry and its strong market presence which can increase its revenue by helping it acquire more customers. Therefore, I am predicting that WU might trade at a P/E ratio of 8.56x in FY2024, giving the target price of $17.29, which is a 47.3% upside compared to the current share price of $11.74.

Conclusion

WU has managed to perform well despite the macroeconomic pressures which indicates its healthy positioning. I believe the company has a deep market penetration and a strong network effect which gives it a competitive advantage to acquire more customers and increase its profit margins once the inflationary environment improves. However, it depends on third-party vendors for certain services that can contract its contract margins in case of unavailability. It also pays a consistent dividend which makes it an attractive investment option to investors who are seeking stable income. The stock is currently undervalued and we can expect a healthy 47% growth from the current price levels because of growing industry demand and its competitive advantage. With a capital return of 47.3% and dividend yield of 8.01%, investors can expect a total return of 55.31%. Considering these solid returns, I assign a buy rating to WU.

For further details see:

Western Union: Buy This Stock For 8% Dividend Yield And Potential Upside