MLPS - Westlake Chemical Partners: Attractive And Overlooked Income Play

2023-10-03 10:39:12 ET

Summary

- Westlake Chemical Partnership (WLKP) is a unique company in the chemicals industry, trading at a discount due to lack of publicity and institutional investors fleeing the asset class.

- WLKP has a stable earnings agreement with its parent company, providing long-term stable margins and making it an attractive income play.

- The possibility of future asset drop-downs and decreasing interest rates further contribute to the attractiveness of WLKP as an investment.

Thesis

Westlake Chemical Partners (WLKP) is a very unique company in the chemicals industry and is part of a dying breed. Not only is it a master limited partnership that hasn't seen many new IPOs since the 2014/2015 oil crash, but it is also a drop-down company, with Westlake Chemical Company ( WLK ) being its general partner. We believe that as a result of its lack of publicity and size, WLKP trades at an undeserved discount due to institutional investors flee from the asset class and the difficulty in classification.

Our opinion is predicated on three ideas: The current ethylene sales agreement gives WLKP earnings stability, the possibility of a future asset drop down, and interest rates likely decreasing.

As of September 26th, WLKP has a per share price of $22.03 and with a well-covered quarterly dividend of $0.4714. This makes WLKP, in our opinion, a very attractive income play, even in the current interest rate environment offering many alternatives.

Company Overview

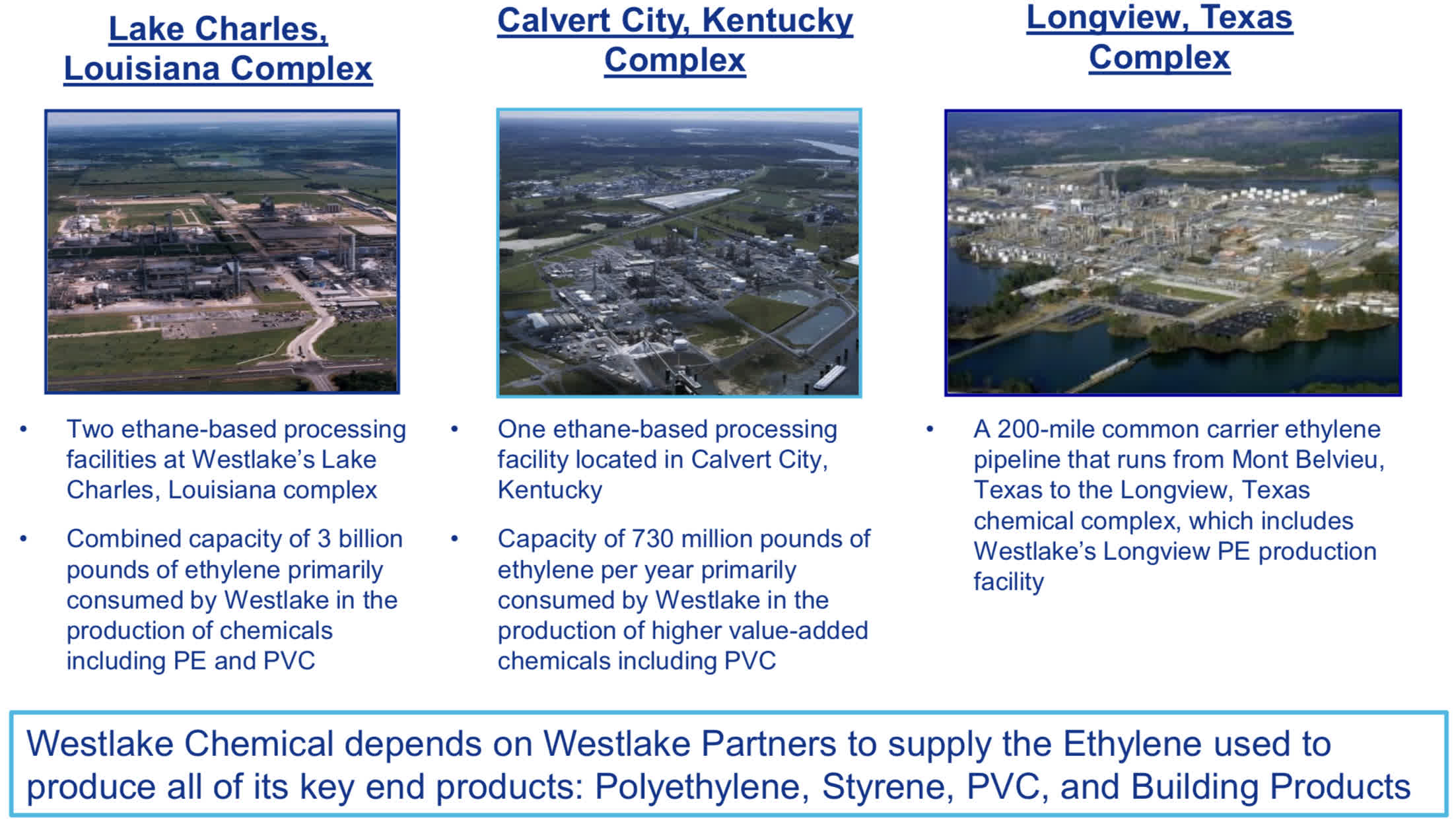

Westlake Chemical Partners is a producer of olefins, vinyls, and chlorinated products. WLKP has 3.73B lbs of ethylene production capacity, equivalent to 75% of WLK’s ethylene needs. This capacity is composed of 3 facilities: Petro 1 (1.5B lbs), Petro 2 (1.5B lbs), and Calvert City (730M lbs), along with the partnership havin a non-core 200 mile ethylene pipeline.

Westlake Chemical Assets (Westlake Investor Relations Website)

{kind=link}

Q2 2021 WLKP Investor Presentation

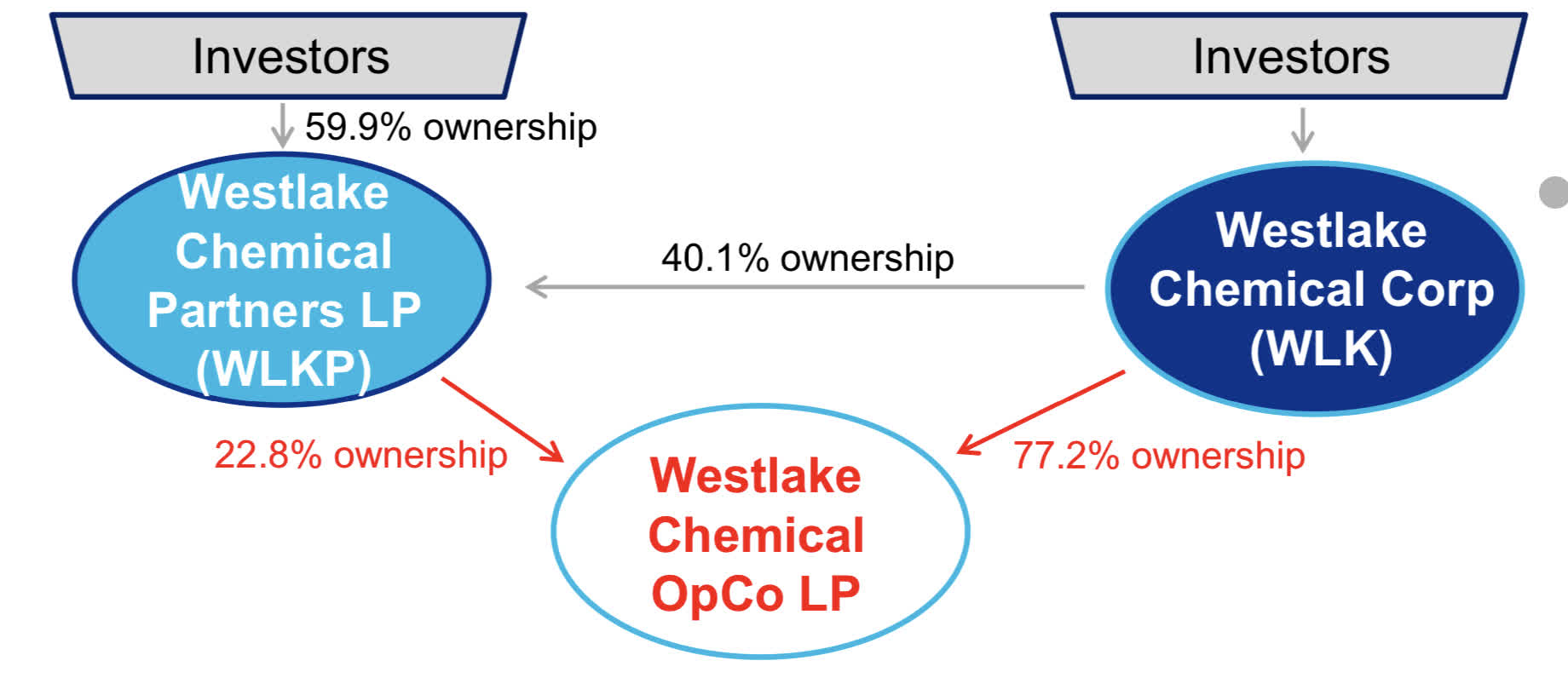

The partnership is structured as an MLP meaning it receives favorable taxation with distributions taxed as qualified income and no entity-level taxation. It derives this income from its 22.8% interest in the Operating Company (“OpCo”) which holds the 4 assets mentioned. Though the partnership has economic control over OpCo. In return for this minority interest in the OpCo and the fact that WLK owns 40% of WLKP, the partnership gets a very lucrative sales agreement.

WLKP corporate structure (Westlake Investor Presentation Q2 2021)

{kind=link}

Q2 2021 WLKP Investor Presentation

Ethylene Sales Agreement Provides Long-term Stable Margins

What makes WLKP unique and allows it to pay such a high consistent dividend is its Sales Agreement with its parent Westlake Chemical Corporation. The agreement requires WLK to purchase 95% of OpCo’s planned ethylene production of 3.7B-3.8B lbs and the option to buy 95% of any excess production. The remaining 5% is sold to third parties at market prices.

WLK’s purchase price includes a $0.10 per pound margin on all costs including feedstock, natural gas, estimated operating costs, maintenance and turnaround capital expenditures, less co-product proceeds. In other words, the $0.10/lbs margin is very comprehensive and it only makes it so the OpCo and Partnership have to pay their respective interest expense and growth expenditures.

We view this as a very attractive agreement as the traditional ethylene producer has varying margins that can result in unpredictable long-term results. This agreement, through creating a reliable high dividend, makes WLKP more comparable to preferred stock of energy/infrastructure-focused MLPs than that of common stock.

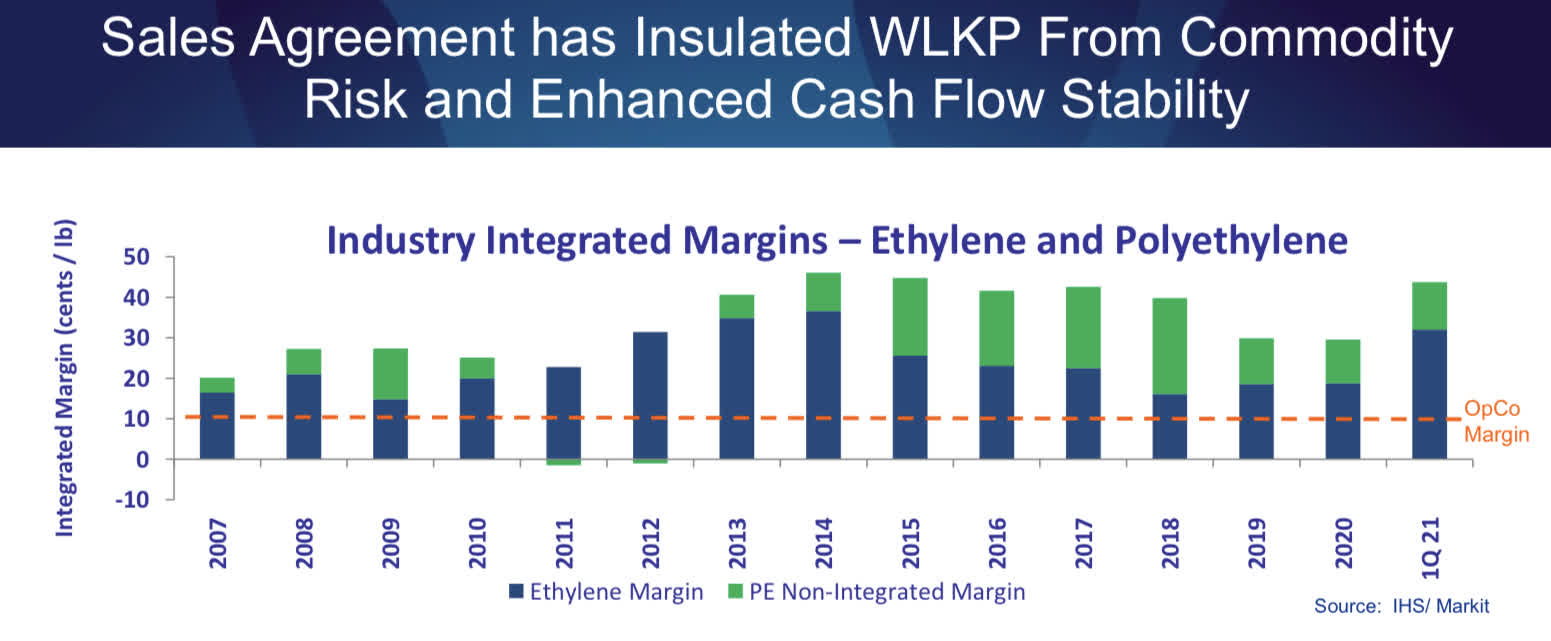

There is also the fact the 10 cents per pound margin is historically below average margins:

Industry ethylene cracker margins (WLKP Q2 2021 Investor Presentation)

{kind=link}

Q2 2021 WLKP Investor Presentation

When the current agreement expires in 2026, there is a small chance that the fixed margin will increase, though we believe it is more likely management will keep the current rate.

Asset Drop Downs

As stated before, WLKP is specifically a drop down MLP. This function of asset drop downs is based on the valuation differential between WLKP and WLK as this allows them to have a gain when they monetize an asset. As a result of being in a relative peak of the O&G commodity cycle, WLK is trading at an above median multiple, but once this cycle ends, WLK may trade at a low enough multiple for a dropdown to be accretive. Another way this valuation differential may expand is that interest rates go down and due to WLKP trading like hybrid debt or preferred equity, it will trade at a low yield, possibly making a dropdown accretive whether or not the O&G commodity cycle is at a trough.

The other thing to consider for the attractiveness of drop downs is the taxation differential between qualified income (20%) and corporate income (21%) taxation. Given that the corporate income taxations is historically low, in the case it rises to say 28% in the second term of a possible Biden presidency, a drop down becomes more attractive because the partnerships’ preferable tax status is more valuable.

As of current, the parent company WLK has only one other facility producing ethylene (Lotte Axiall Joint Venture) producing 1.1B lbs of ethylene. In our opinion, there is a good chance that once one of the conditions mentioned occured improving the valuation differential, WLK will likely drop down the facility.

Interest Rates Decreasing

Besides the fact that interest rates going down would result in the valuation for a fixed income-like equity to go up naturally, interest rates decreasing would significantly lower interest expense. For context, the company has $400M in debt , $377M of that is in credit facility at the partnership level bearing interest at SOFR plus 185BPS. The other $23M of debt is in another credit facility that is on the OpCo level in the capital structure, meaning that the partnership is only responsible for 22.8% of it, equivalent to its interest in the entity.

What you may be thinking is: wait one second, aren’t all expenses covered by the ethylene sales agreement? Well, due to the fact that interest isn’t an operational expense, WLKP is not reimbursed for it. In Q1 of 2023, the net interest expense was $7.3M, versus $2.2M in the same period the prior year. Fortunately, the company also has $153.6M in cash, with 60% of that being in the money market. This interest income has partially offset the interest expense, with net interest expense decreasing to $6.1M in Q2 of 2023, a $1.2M sequential decrease. Assuming that the SOFR declines to 3.50% in 2 years, as predicted by interest rate futures, then interest for this past quarter would’ve been roughly $4.5M, or an almost 10% increase in income due to an eventuality.

Relevant Financials

As stated before, the ethylene sales agreement provides long-term stability in cash flow, though let's cover the balance sheet first. We have already mentioned the $400M in credit facility debt, but one unique thing is that the two facilities have been amended 3 times, extending the initial maturity from 2018 to 2027 , with the debt being held by Westlake. As a result, this debt is in my mind perpetual in nature due to WLK’s incentive not to allow it to mature as they hold 40% of partnership units and the Chao Family owns another 4%, giving them almost majority voting power. We see this “perpetual” debt as another benefit of the entity structuring and WLK being the general partner..

Besides this “unique” debt view that changes how we view debt in the capital structure, the balance sheet is very strong with $154.2M in net working capital as of June 30, 2023. Of this, $153.6M is cash held in an investment management account with WLK and held directly by the partnership. This investment management account earns 5BP above money market returns and requires a 6-9 month lockup..

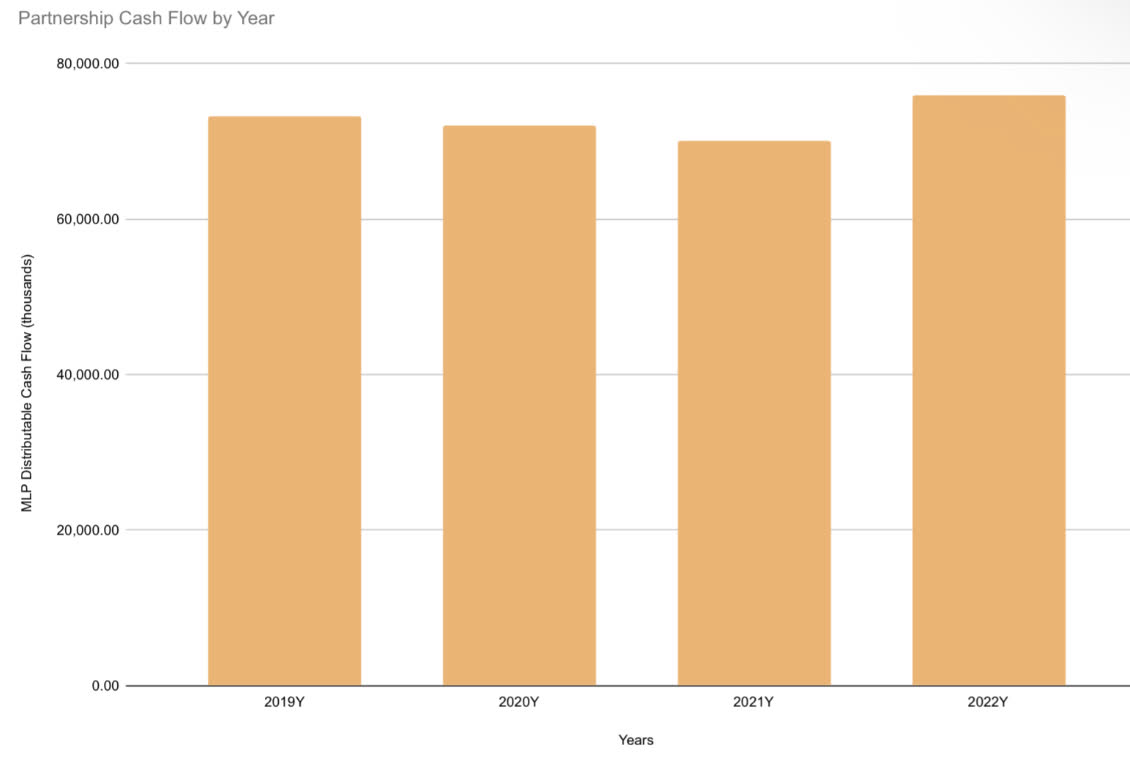

Going into the operating results, the partnership has seen stable cash flow over the long-term, though from 2014-2018 it was skewed by capacity additions and weather events, though that was made up for buyer deficiency fees charged.

Historical MLP Distributable Cash Flow (WLKP Investor Presentation) Author Created Image using WLKP Financial Statements (WLKP SEC Filings)

{kind=link}

WLKP Investor Relations Website - Financial Statements

As can be seen, the distributable cash flow sees little fluctuation with the only fluctuation being due to the 5% of production sold to third parties and interest rate changes affecting interest expense. In 2023, MLP distributable cash flow should be in the $65M-$67.5M range due to the negative impact of interest rates, but in 2024, it should be closer to a more normal $70M, assuming no other changes in assets and OpCo structure occur.

Benefits of the Partnership for Westlake Chemical Corporation

Though I haven’t mentioned it cohesively, the benefits of the partnership are important in determining in the extrinsic value:

-

Sales Agreement - the chemical industry is known for its volatility and given its largely commoditized and cyclical nature, having a sales agreement which fixes a significant portion of WLK’s input costs is very valuable. WLK has a specific focus of being the most diversified and vertically integrated chemical manufacturer, and this agreement is a main tenant of that.

-

Preferred Taxation - WLK is able to flow sales revenues and costs through this entity at a lower taxation as corporate income is currently taxed at 21%, but due to being an MLP, the taxation is that of long-term capital gains or 20% as of current

-

Asset Monetization - as already discussed, assets are drop down when WCC’s valuation is significantly below that of WLKP, meaning that when WLK sells an asset to WLKP with the associated sales agreement, it receives not only a good price, but it allows it to have more liquidity. Along with this, WLK owns 40% of WLKP units and can sell them if it needs the capital, or in other words, it allows WLK to sell portions of its normally illiquid production facilities.

It is my opinion that the incentive to be friendly towards WLKP unitholders so that the units are higher on the credit structure than standard preferred equity. This is shown by the fact that after WLK sold a 5% interest in OpCo to WLKP at an unfavorable valuation, the market reacted badly and management (both companies have the same management), in order to win back unitholder’s favor, increase the Incentive Distribution Rights (IDRs) from a minimum of $0.3163 per quarter, to $1.2938 per quarter. With the current dividend of $0.4714 per quarter, they decided to destroy any chance of getting any IDR income in order to satisfy unitholders. In my opinion, this really just shows the power of unitholders of WLKP in the capital structure of WLK.

Credit Analysis and Comparable Valuation Analysis

With 80%-85% of revenue is derived from the sales agreement with WLK and ethylene is the main component in the majority of WLK’s products, WLKP does not only have tax and asset monetization benefits, but it also is essential to WLK’s operations

Due to this unique nature of the partnership, the credit risk associated with the partnership's income stream is directly linked to the credit rating of its parent, Westlake Chemical Corporation. As of current, Moodys has assigned Westlake Chemical corporation a BAA2 or BBB credit rating with a positive outlook, and they have had this rating for over 10 years.

The dilemma is determining which debt/equity in the capital structure is best to base the rate on, which is based purely on quantifying credit risk due to the assumed perpetual nature of the partnership. The assets within the partnership are essential to the operations of the parent corporation and given the equity ownership of the partnership and OpCo, I believe the obligation of the ethylene sales agreement is equivalent to that of senior notes secured by the production plants. As such, I believe looking at BBB corporate bond indices, Westlake unsecured senior notes, and MLP preferred securities.

BBB corporate bond index (St Louis Fed Index)

{kind=link}

( St. Louis Fed BBB Corporate Bond Index )

Author Created Westlake Corporate Bond Overview using Moody’s and Finra Data (Moodys.com & Finra Fixed Income Center)

{kind=link}

( Moodys Investor Service & Finra Fixed Income Center )

First looking at comparable debt securities, we can see that the BBB effective yield is at 6.25%, while the variety of senior notes of Westlake Chemical Corporation that have over 10 years left average a yield 6.40% One notable thing is that these bonds are taxed very differently from WLKP distributions with WLKP dividends being taxed at 20% in the top margin bracket which we will go off of as it applies to most institutional investors. With 60% of the YTM coming from the coupons and the rest coming from discount to par, thus resulting in a blended tax rate of 30%, while the tax rate for WLKP is a qualified 20%, meaning this 6.40% bond yield is comparable to a 5.60% yield for WLKP.

The good thing is that WLKP is technically at a higher seniority to unsecured notes of WLK as the ethylene plants produce most of the inputs for production and in order to repay the notes, it needs to pay distributions to the partnership and operate the facilities. At the same time, the variability in distributions inversely correlated with interest rates due to interest expense amplifies the effects of interest rate changes.

Given the relative peak in interest rates and the aforementioned likelihood of MLP distributable cash flow increasing from $65M - $67.5M to $70M over the next two years. Applying a 6% yield, with this yield being higher than 5.6% to account for the time it takes to interest to decrease, to the $70M in distributable cash flow expected in 2 years, we get a valuation of $1166M or $33.10 per share intrinsic value, a 50% upside to current price of $22.03

Risks

1) Third Party Margins - though on average historically, margins have been above 10 cents/lbs and are only rarely negative, in these cases of third-party margin compression, the facilities are protected by the ability to lower utilization by only a small percentage (<5%) if conditions are unprofitable without hurting efficiency.

2) Unattractive Drop-Downs/OpCo purchases - it is unlikely that a future dropdown would be unattractive considering it brings monetization benefits and not just the tax and cost benefits an OpCo purchase does. Since the IPO, interest in OPCO was purchased 4 times over 9 years at the following 2022 cash flow multiples in chronological order: 13.9x,13.0x, 11.9x, & 11.6x. As less capital has flown into the MLP sector, management has had to go to more attractive multiples in order to align with investors, they clearly have shown their alignment with investors and have an incentive to make attractive drop-downs and OpCo interest acquisitions.

Conclusions

As a result of the fixed price ethylene sales agreement, future asset drop downs, and future lowered rates, Westlake Chemical Partners represents not only an attractive income play with a tax-advantaged 8.5% yield, but it also has significant potential for modest distribution growth as interest rates decrease, ethylene margin possibly increases, and the Lotte Axiall Joint Venture ethylene plant is likely dropped-down

For further details see:

Westlake Chemical Partners: Attractive And Overlooked Income Play