WRK - WestRock: A Packaging Player That's Overvalued Here For 2024

2023-11-24 23:29:09 ET

Summary

- Westrock is one of the largest packaging companies in the USA, but faces challenges in terms of profitability and debt/equity ratio.

- The company is heavily impacted by volatile trends in the packaging industry and struggles to compete with European peers.

- The recent merger with Smurfit Kappa Group may bring long-term benefits, but near-term trends suggest sub-par development.

- I would view the company as a "HOLD" here.

Dear readers/followers,

If you follow my work, you know that I invest capital in forestry companies, which in Europe and other areas, tend to be fairly closely tied to packaging operations and players. I have not reviewed Westrock ( WRK ) before, but I've been looking at the company a few times. Usually, though, investments in the same sector in Europe have been more attractively priced, with better yields, better assets, or better overall upsides.

Westrock is a qualitative business - it deserves a review here. I do believe though if you're interested in Westrock, you should also consider looking at the Scandinavian and European players in the segment. I'm talking about companies like Billerud ( OTCPK:BLRDY ), Enso ( OTC:SEOJF ), UPM ( OTCQX:UPMKY ), SCA ( OTCPK:SCABY ) and Huhtamäki ( OTCPK:HOYFF ).

However, here we're talking about Westrock - so let's look at what this company offers investors.

Presenting Westrock - One of the largest packaging players in the USA

Westrock is primarily a corrugated packaging company. This means it has a different operational mix than the companies I typically review in this segment, because more often than not they also own forest and timber assets to a very large degree.

Westrock employs over 50,000 employees across 30 countries, making it not only one of the largest companies of its kind in the USA but in the entire world. The stock has been punished in a very major way - while we've seen recovery from the worst lows during this year, the company still is nowhere near trading at the highs of over $60/share that it did years ago. It's actually not that far from the COVID-19 trends, which saw the company dip toward the $20/share mark.

This is how these sorts of companies work, given their exposure to very volatile overall trends. Typically, this company manages around 4.5% net margins and upwards of 18-20% gross margins, managing a high, 81%+ COGS and around 10% OpEx. This portion of the business model is, as I would characterize it, not that great. Why?

Two reasons. First, because peers are better - especially if they have a more diversified mix. More importantly, though, this company has this year seen some of the pressures we've seen in Europe as well - but their margins and fundamentals seem far less prepared for what's happening here.

How do I know this?

Because if you calculate their KPIs, you come to an interest coverage of less than 2.5x, and a debt/equity of over 0.8x, which is quite significant. You've also seen a fundamental deterioration in the company's profitability. As of the latest results, we're down to a negative net margin, negative RoE, negative RoA, and a poor ROIC. The EBIT margin is down to 6%, and GM is below 18%.

That this sector is volatile is absolutely no secret - but the secret sauce when it comes to companies here, or really companies in any sector, is profitability. This is one of the first things I look at, and this is where the company isn't doing all that great.

This company is still in a position that Scandinavian companies in the same segment have been fighting in for several years. The company needs to rationalize and make efficient its production base, and optimize its processes, all the while fighting inventory destocking trends, that result in both pricing and volume declines in the company's core segment, this being Corrugated packaging.

{kind=link}

WRK IR (WRK IR)

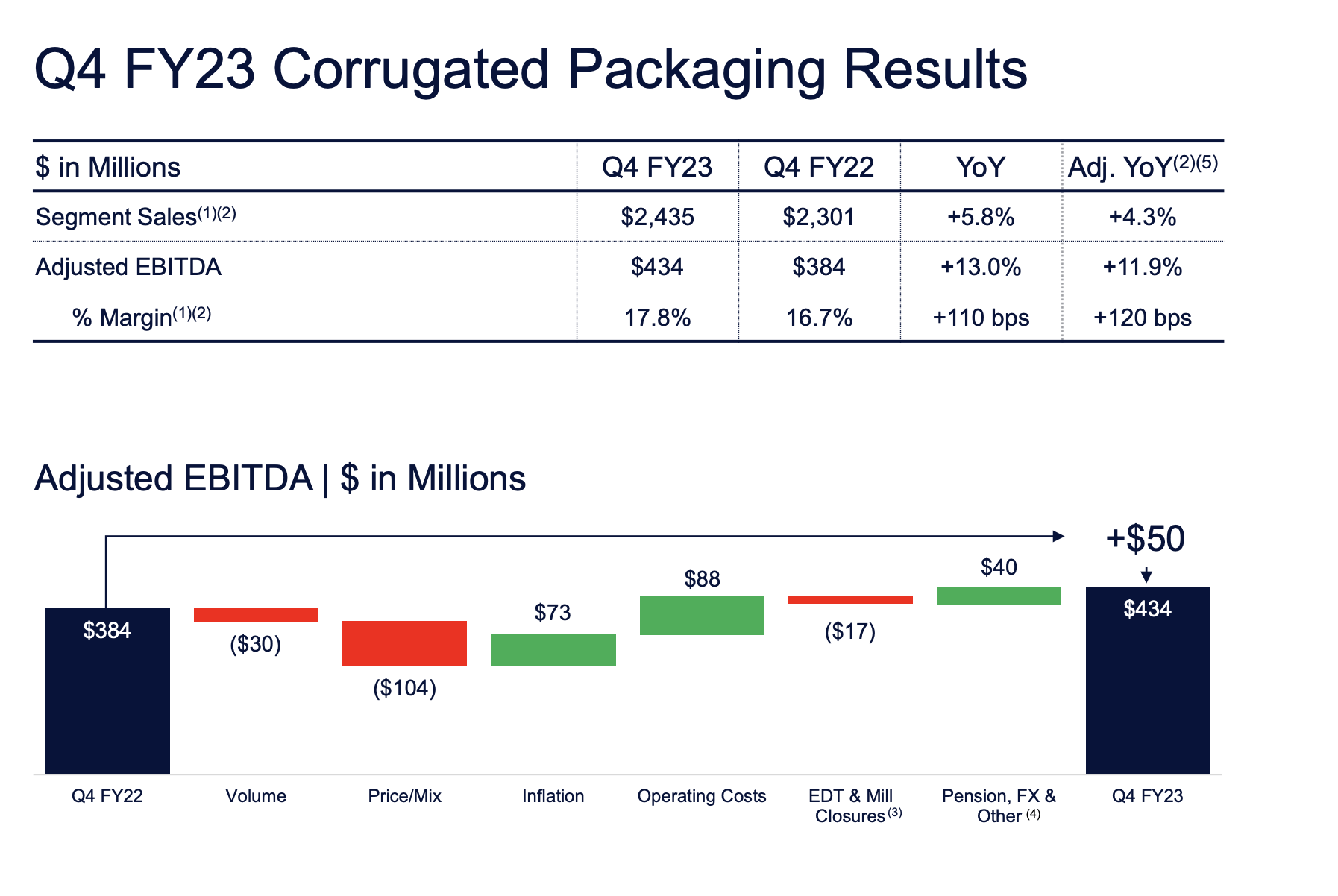

As we can see, these impacts are non-trivial - though the company is doing what it can to right the ship here. On an operational basis, the company is split into Paper (very, minor, but down for the quarter nonetheless), Distribution (even smaller), and the two main segments of Consumer packaging and Corrugated packaging, with the latter being the largest at over $2.4B worth of quarterly sales for the 4Q23 period.(Source: 4Q23 Presentation )

It's fair to say at this point that trends in both EBITDA and sales are heavily characterized by the aforementioned mix of realignment of operations, savings, efficiencies, and volume and price pressures.

With fiscal 2023 closed, we can confirm a slight margin expansion, an improved asset base with closures in non-key locations or due to bad costs (older style mills and paper machines), and investment in the new capacities and better assets. This is exactly the same we've seen across Europe for going on 7-8 years.

WRK's play has been moving into LATAM, with a recent Mexico acquisition and a focus on an attractive LATAM market. Also, in terms of those cost savings , the company is managing better than expected .

This has had the result of a decent enough 2023, which has also caused some justified recovery in the share price. The company expects 2024 to be even more improved, targeting another $400M worth of cost savings, and expecting improved demand toward the second half of 2024. This comes in line to what other companies in the sector are expecting as well.

On the flip side, WRK also needs to account for higher overall costs for fiber, wages, freight, and other feedstock or components due to not being as vertically integrated as others - and this is with the lower energy costs and chemicals already included in the calculation. (Source: 4Q23 Presentation )

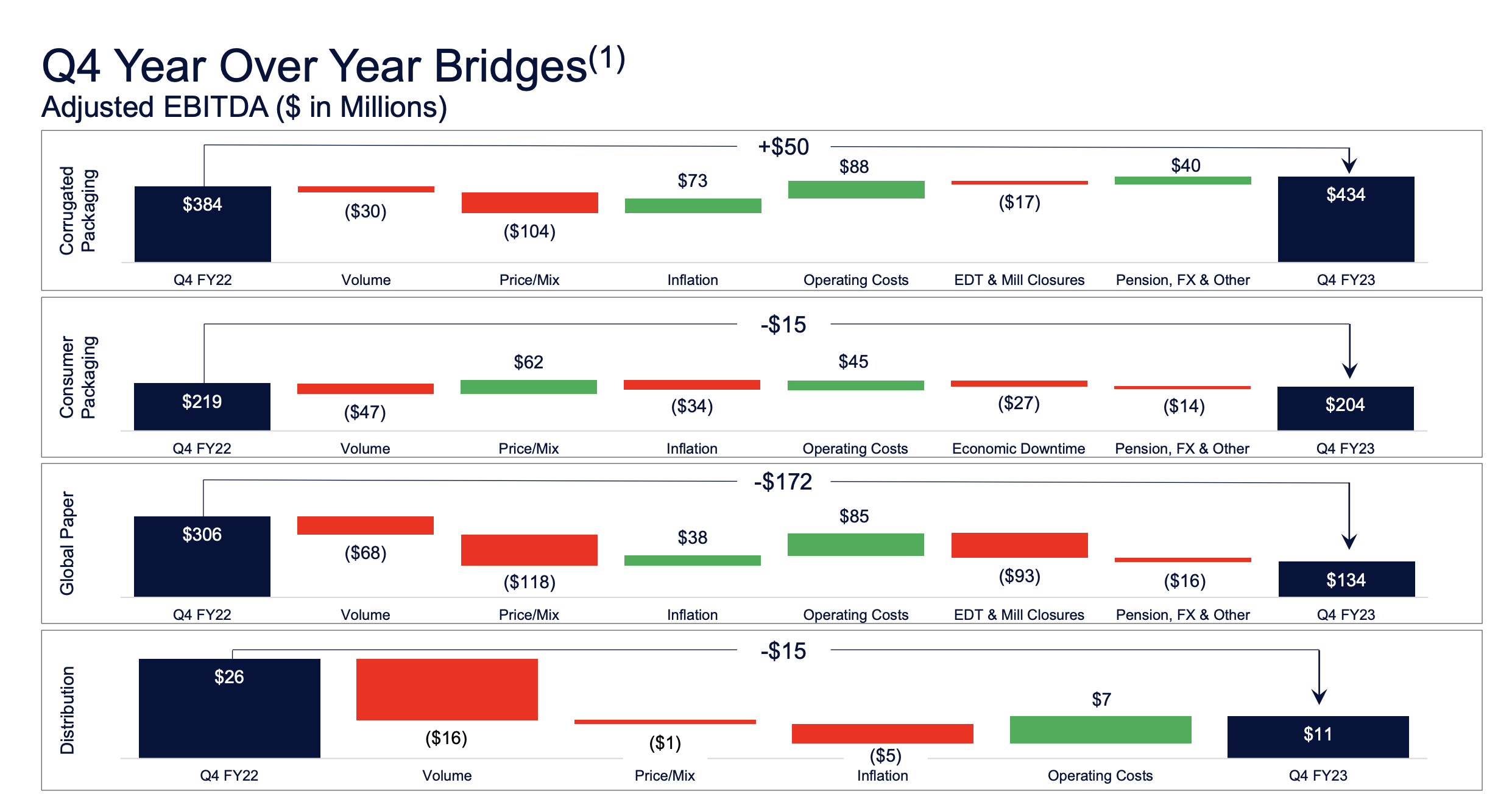

The company will remain heavily dependent on what it does in terms of CapEx. And rationalizations - but a quick look at an excellent overall illustration shows the cadence and specifics of the pressures that not only WRK is undergoing, but that can be said to affect the entire western industry in this sector.

{kind=link}

WKR IR (WKR IR)

Also, it's important to point out at this time the overall impact of maintenance - because 2024E is expected to be a heavy year in terms of overall maintenance for the company, with over $100M more in maintenance costs than in 2022. (Source: 4Q23 Presentation )

The company's lack of diversification or vertical integration means its primary sensitivities are relatively simple - fiber, diesel, natgas, energy, starch, caustic soda, and other chemicals, with every 10% USD appreciation resulting in a negative 1 cent impact on the adjusted EPS side. The volatility here is expected to be high on a forward basis as well.(Source: 4Q23 Presentation )

The recent news that Smurfit Kappa Group and Westrock are merging has of course muddled this even further. Many analysts considered this a net upside over the long term, but if we look at the market share price development since the announcement, the reception has been very tepid over the last 2-3 months. The deal may be logical, and there are certainly synergies to bring to the table here, with WRK being valued at around $20B on an EV basis.

Synergies in these sectors are always difficult - similar to the concrete industry. Both of these players have their legacy assets and portfolios they need to streamline - Smurfit Kappa is no different. While the eventual result may indeed be positive, my reasoning for staying tepid myself, and not immediately buying shares, is the fact that the company is doing this in a headwind market with plenty of company-specific, macro, and even micro pressures. (Source: 4Q23 Presentation )

In short, I do not believe that the near-term trends here are going to be favorable, even with this deal in the bag - and analysts agree.

The combined impacts and headwinds for WRK are expected to bring about a fiscal-year 2024E impact of negative 20% YoY on the EPS side - that's in addition to the 36%+ adjusted EPS drop in fiscal 2023.

This is then combined with the fact that WRK only yields 3.3% in an environment where 5-6% is easy, has BBB but not higher (many peers have BBB+), and an eventual upside with Smurfit Kappa seems realistic to be at least 2 years away in the fiscal of 2025E. (Source: 4Q23 Presentation )

A lot can happen in two years - and this is a market where opportunities aren't exactly hard to find, which makes compromising, especially compromising with a company that has a proven record of negatively failing to meet estimates more than 45% of the time on a 10-year basis a non-starter at this price. (Source: FactSet)

The valuation for WRK - is unattractive from a global perspective.

WRK typically trades at a P/E of around 11-12x, which also represents the trading range we see for European companies in this sector. I have no issue with this range, and I would consider it accurate for the short term. But that's also why I'm not that positive about the company.

An average 11-12x P/E goes no higher than an implied share price of around $33-$36/share depending on how good or bad you estimate 2024E results to be. If you, like me, expect the company to decline in earnings the next year, and like most cyclical in a downtrough , see a decline in valuation, then there is little reason to be all that positive here.

Yes, once things cycle back up, we can see an upside for WRK here as we see an EPS recovery of over 40% (remember though that WRK half the time does miss negatively), but that upside isn't exactly the cause for jumping up and down.

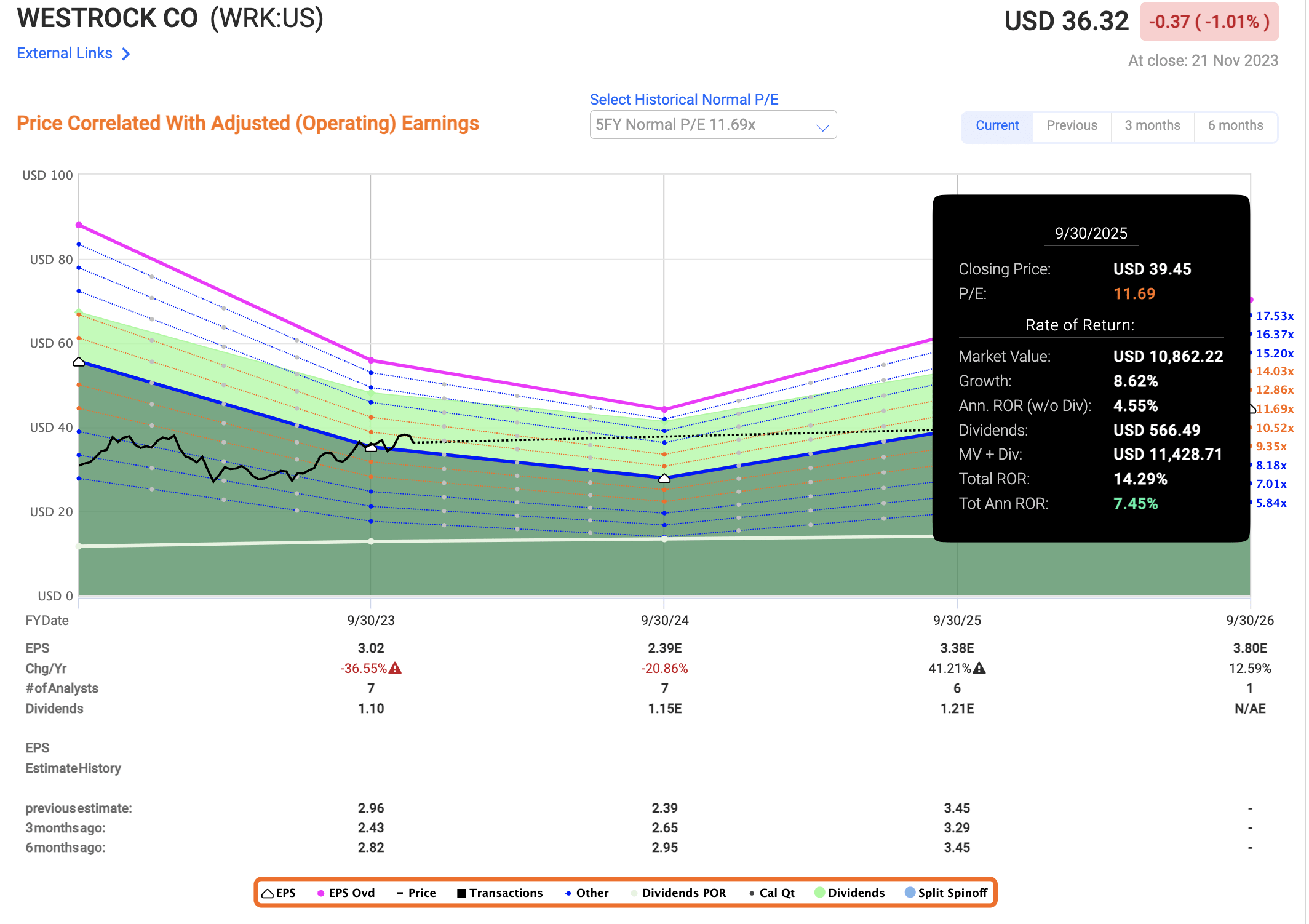

{kind=link}

F.A.S.T graphs WRK Upside (F.A.S.T graphs)

I believe that being positive on WRK here means ignoring many of the far better peers that show an upside well into the double digits with a high yield, or a lack of understanding of the cycles in packaging, timber, and paper. At an attractive valuation, I would be very interested in buying WRK, but this is not the case here.

Analysts give the company a range from $38/share up to $55/share with an average of $41. That means that my own target of $35/share is lower than all of the other ones here - but I want to be clear, that this is a relatively short-term target until we see what happens in 2024. It's just that based on near-term trends and cyclicality, I see a high probability for sub-par development here.

Based on this, I give WRK the following specifics as my introductory thesis here.

Thesis

- Westrock is one of the largest packaging companies in the world. While the company is certainly attractive and has an overall upside from a fundamental and long-term perspective, the short- and medium-term hold enough uncertainties to make me somewhat hesitant to go in significantly at this time.

- I view the company as materially unattractive for the next 12 months at least, based both on overall yield and potential reversal - compared to sector peers in Europe which have more than twice the yield and better near-term upside.

- I would give WRK a PT of around $35/share - though this is near-term , and once visibility improves, I consider an increase here more than likely.

- This means I give the company a shorter-term "HOLD".

Remember, I'm all about:

- Buying undervalued - even if that undervaluation is slight and not mind-numbingly massive - companies at a discount, allowing them to normalize over time and harvesting capital gains and dividends in the meantime.

- If the company goes well beyond normalization and goes into overvaluation, I harvest gains and rotate my position into other undervalued stocks, repeating #1.

- If the company doesn't go into overvaluation but hovers within a fair value, or goes back down to undervaluation, I buy more as time allows.

- I reinvest proceeds from dividends, savings from work, or other cash inflows as specified in #1.

Here are my criteria and how the company fulfills them (italicized).

- This company is overall qualitative.

- This company is fundamentally safe/conservative & well-run.

- This company pays a well-covered dividend.

- This company is currently cheap.

- This company has a realistic upside that is high enough, based on earnings growth or multiple expansion/reversion.

For further details see:

WestRock: A Packaging Player That's Overvalued Here For 2024