WRK - WestRock: Asymmetric Opportunity At $35

Summary

- WestRock shares fell nearly 8% last week as management withdrew full-year guidance following weak results in the company's global paper segment.

- While 2023 will likely be a disappointing year, WestRock has many attractive attributes, including a solid position in an improved corrugated packaging industry.

- With a stable demand profile in its consumer and corrugated packaging businesses, WestRock has consistently generated $4+ per share in free cash flow over the past 7 years.

- WestRock's balance sheet is in good shape with Net Debt to EBITDA of 2.35x. Management plans to further reduce leverage to 1.75-2.25x.

- I see modest upside even if the business continues to experience weak results and significant (+150%) upside should management achieve its 2025 targets.

It has been a rough ride for WestRock ( WRK ) shareholders. The stock has declined 45% over the past five years and is down nearly 25% in the last year, significantly underperforming the broader market. Shares declined last week after the company withdrew full-year EBITDA guidance citing weakness in its global paper segment and an uncertain demand outlook (high customer inventories) given the economic environment.

While the global paper segment, which represented ~30% of EBITDA (3 year average), is subject to greater volatility than the company's consumer packaging and corrugated packaging segments, I believe the market has overly discounted WestRock shares which now sell for just ~8x current year (depressed) free cash flow per share.

As I discuss below, I see modest upside even if the business continues to experience weak results and significant (+150%) upside should management achieve its 2025 targets.

Reasons to like WestRock

- Improved industry structure following years of industry consolidation. Ten years ago, the top five players controlled less than 50% of the corrugated packaging market. After a decade of consolidation, the top 4 players now control 75-80% of the market which creates a much more favorable dynamic in terms of capacity additions and pricing.

- Long-term outlook for demand remains favorable - e-commerce is all but certain to grow and environmental consciousness points to a continued movement away from plastic packaging.

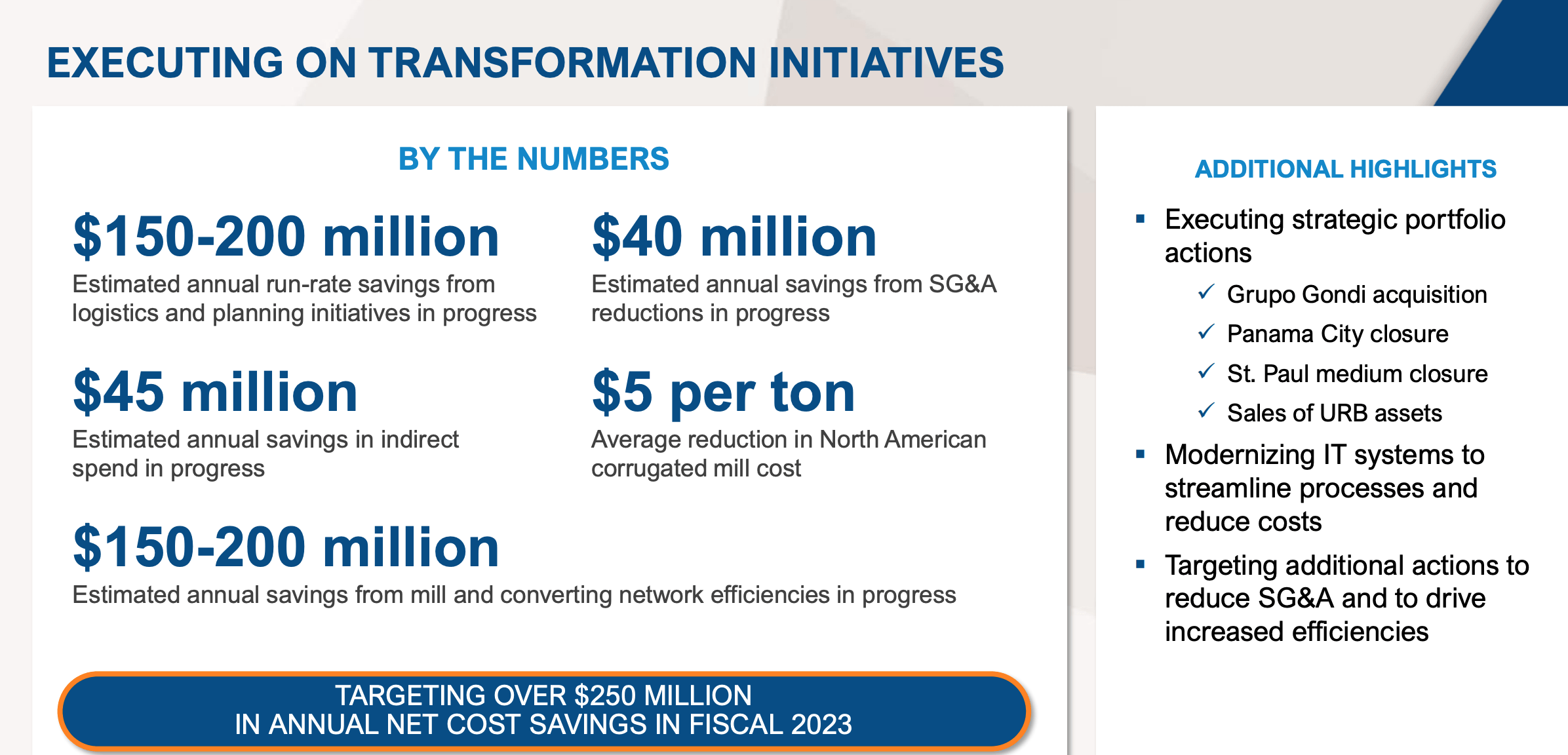

- Room for operational improvement - WestRock is the product of a series of mergers. As we sit today, WestRock's corrugated EBITDA margins (15-17%) lag competitor Packaging Corporation of America ( PKG ) which has consistently produced 22-24% EBITDA margins. While some of this is due to mix (PKG's focus on smaller regional customers), there is an opportunity to improve margins through operational improvement as shown below. With large scale acquisitions now complete, under CEO David Sewell (joined WestRock in March of 2021), WestRock is increasingly focused on integration/operational excellence.

{kind=link}

Cost Savings Targets (Investor Presentation)

- Some cost headwinds now becoming tailwinds - Natural gas and recycled fiber prices have significantly declined over the past 6 months though virgin fiber costs (tend to move the opposite direction of new home construction) have increased.

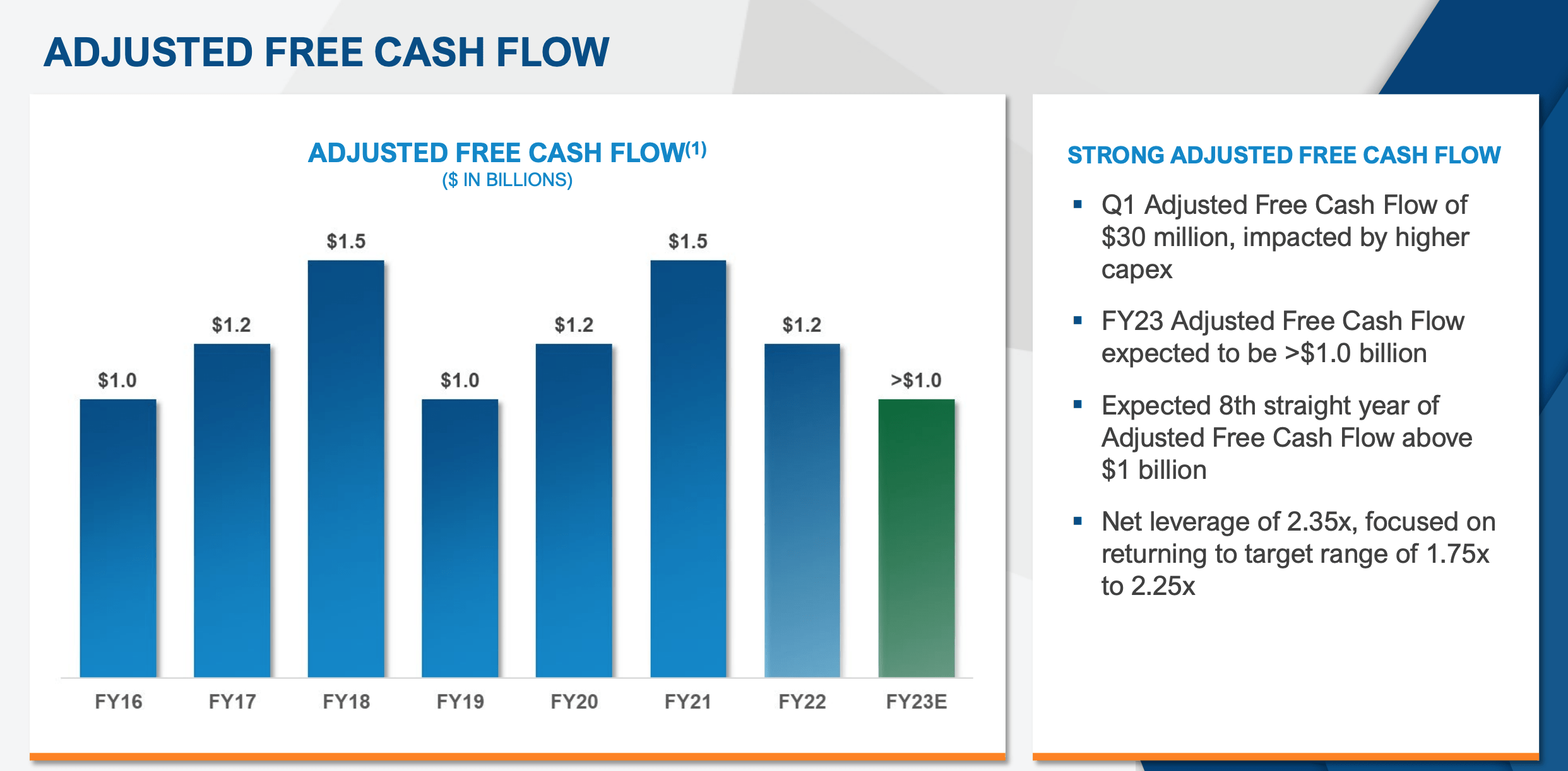

- Consistent History of Free Cashflow Generation - as shown below, WestRock has generated adjusted free cash flow of $1+ billion each year since 2016.

{kind=link}

Consistent Free Cashflow Generation (Investor Presentation)

- Manageable leverage profile - WestRock took on a heavy debt load to make acquisitions (Net Debt to EBITDA peaked at 3.2x in 2020) but is now committed to reducing leverage to 1.75-2.25x Net Debt/EBITDA (versus 2.35x currently).

Valuation

Using the average free cash flow generated over the past seven years and the current share count, WestRock has produced average FCF/share of $4.50. At the current share price of $35, WestRock trades at less than 8x its historical FCF/share, a 25-40% discount to peers like International Paper ( IP ) and Packaging Corporation of America.

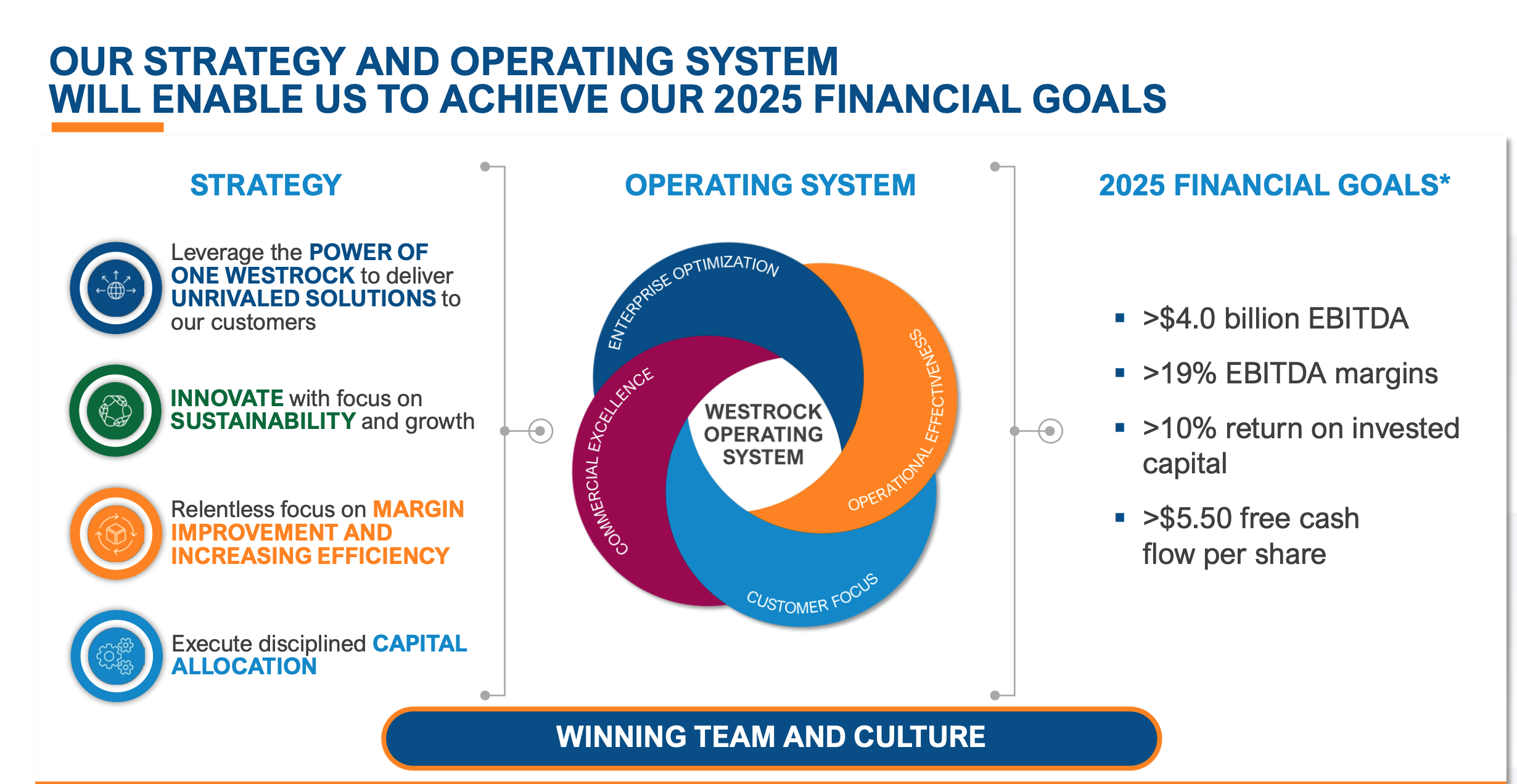

As shown below, at its 2022 investor day, WestRock management put forth a 2025 free cash flow per share target of $5.50+. Should the company achieve its $5.50/share in free cash flow objective, WestRock would be trading at just 6.4x FCF.

{kind=link}

2025 Financial Targets (Investor Presentation)

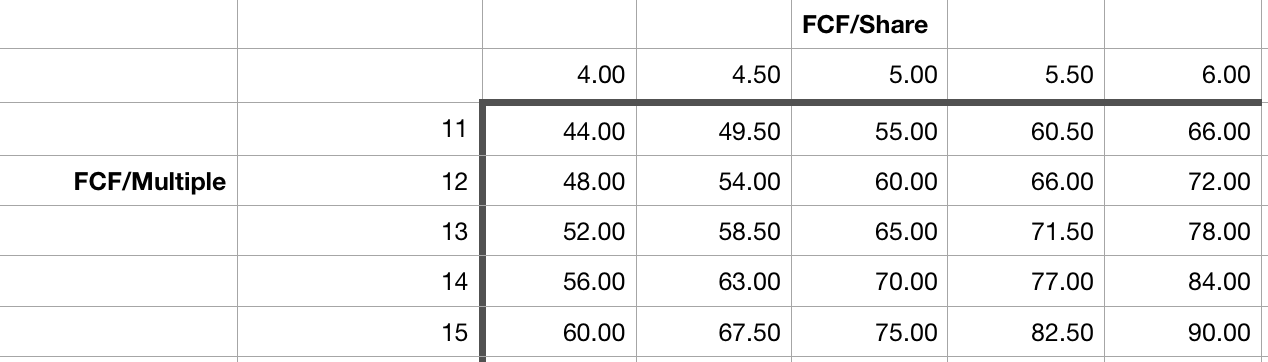

Ultimately, I think WestRock should trade somewhere between 11-15x FCF. Historically, WestRock has traded as high as 18x FCF (2018 and 2021). At the high end (15x) my multiple is reflective of WestRock's leading position in a relatively concentrated industry, stable demand profile, and expectations for GDP-ish growth. At the low end (11x), it contemplates volatility in input costs, supply and demand imbalances, and a low (7%) return on invested capital. Below I show a sensitivity table using a range of $4-6/share in FCF and 11-15x FCF:

{kind=link}

WestRock Valuation Sensitivity (Author Estimates)

Using the current share count, $4/share is the low end of WestRock's historical free cash flow generation while $6 would be achievement of management's 2025 investor day $5.50+ target. At the low end of my multiple and FCF/share ranges, WestRock would have a $44 estimated value and offers +23% upside. Should things work out according to management's plan ($6 in FCF/share) and investors reward the company with a 15x multiple, the stock could be worth $90/share (+156% upside).

Conclusion

While the near term outlook is murky, I believe it is reasonable to expect that WestRock will ultimately achieve higher levels of profitability. Should the company achieve management's targets, as shown above, I see significant upside in the shares. If for whatever reason results remain depressed, I believe that the stock has limited fundamental downside. As such, I see WestRock as an asymmetric investment opportunity.

For further details see:

WestRock: Asymmetric Opportunity At $35